Image source: Pixabay

It is hard not to conclude that a Canadian recession is underway given in the nature of the disappointing quarterly results of the Big Six banks. Almost uniformly within the industry, revenues stagnated or declined, loan loss provisions were ratcheted up and their loan book is flat-lined. None of these developments are cheerful news for bank investors. Without credit growth, an economy shrinks. Now the weakness is apparent in all the wrong places.

The most important feature concerning a bank is the “provision for credit losses” PCL by which the banks set aside funds to cover anticipated losses. RBC, for example, in the three months through January set aside C$813 million in PCL, a 53 percent increase from the same quarter last year. In other words, the bank underestimated its anticipated losses when reporting in 2023 Q1 and now needs to increase anticipated losses in response to a much weaker economy in 2024. Banks are recognizing that there is considerable stress in consumer lending, especially in mortgages, and they anticipate much higher delinquencies at the retail level.

With higher mortgage payments on the horizon for thousands of borrowers, meeting credit-card and auto-loan payment demands become more difficult. Homeowners will do almost anything to keep the mortgage payments from slipping into arrears, and, accordingly, may have to let non-mortgage debt service fall behind. PCLs are also building up in the corporate sector, especially where real estate assets are suffering from unfavorable macroeconomic conditions. Commercial lending has yet to feel the full crunch from post-COVID losses in the office and retail sectors.

Canadian banks have a reputation of being on the conservative side when dealing with allowances for bad debts. Some have argued, however, that the banks have not fully grasped the impact of this current rate cycle on many customers, i.e. PCLs are too low. All the more reason to acknowledge the seriousness of a sequential increase in the PCLs.

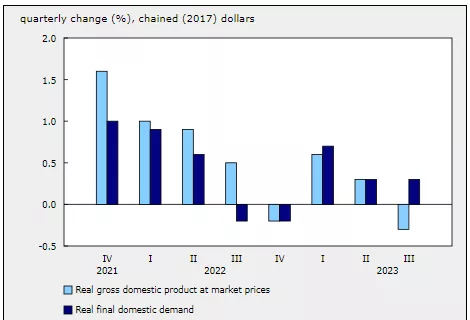

Canada GDP Growth

How are the banks contending with the recession? Aside from taking bigger PCLs, some are cutting their mortgage book. All banks are aggressively seeking core deposits to lower the cost of funding. Many banks are streamlining their operations, shedding labor, and reducing service levels. However, the real issue remains to generate more revenues and that does not seem likely in an economy that is contracting.

Where is the Bank of Canada in all this? No sign of any rate relief or loss of credit conditions affecting mortgages and other consumer debt. The longer the BoC remains silent, the greater the risk to economic growth.

More By This Author:

Does Canada Have A Productivity Problem?

Interpreting Canadian Job Numbers Is In The Eye Of The Beholder

Why Did The Canadian Federal Government Deficit Increased Dramatically In 2023 And Does It Matter

Comments

Log in or sign up to join the conversation.