Trend Profiles Revive Outlook For US, Big-Cap And Growth Equities

Forecasts that relative underperformers in the equities space are poised for a turnaround is a hardy perennial, but the expected change always seems to be postponed for several of the usual suspects. Notably, projections that foreign, small-cap, and value stocks are set to outperform their broad US, large-cap, and growth counterparts are facing new headwinds this year.

Profiling trends through pairs of ETFs continue to tell a story of failed breakouts and frustrated expectations, based on data through yesterday’s close (Mar. 27). Let’s start with US vs. foreign shares. Last year’s sharp losses for equities nearly everywhere gave equities ex-US a lift in relative terms. But the foreign edge is fading so far this year as US shares (VTI) and foreign developed markets (VEA) post comparable results following a reversal of fortunes for American stocks.

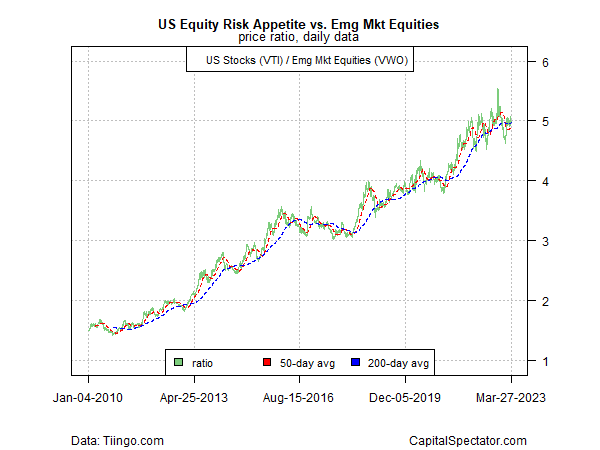

The trend barely wavered for US stocks (VTI) over shares in emerging markets (VWO). The VTI:VWO ratio wobbled a bit over the past year, but the upside bias for US companies has emerged no worse for wear on this front

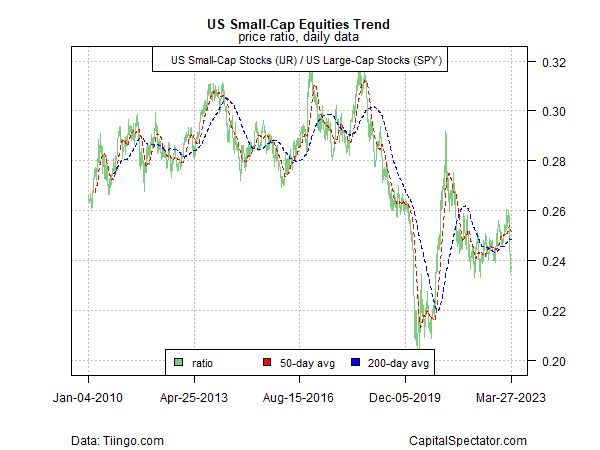

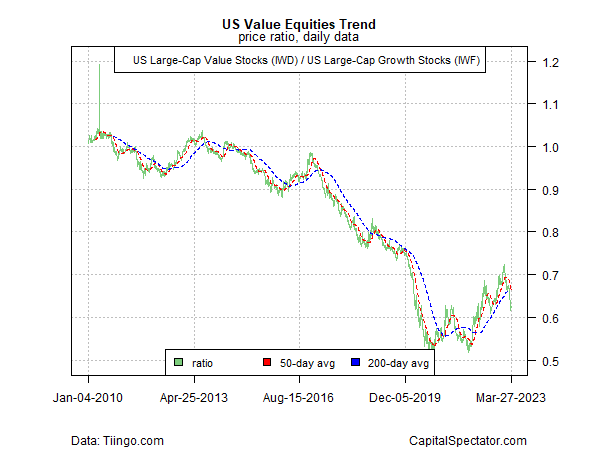

Within the US market, there has been renewed hope that value and small-cap shares would finally enjoy rallies that outperform growth and big-cap shares, respectively. Recent history offered reason to think that these trend changes had finally arrived, but the latest market activity has again dashed those hopes.

The relative strength for small-cap stocks (IJR) has fallen hard lately vs. big-cap names (SPY).

A similar reversal of fortunes befell the recent rebound in value stocks (IWD) over growth shares (IWF) in the large-cap space.

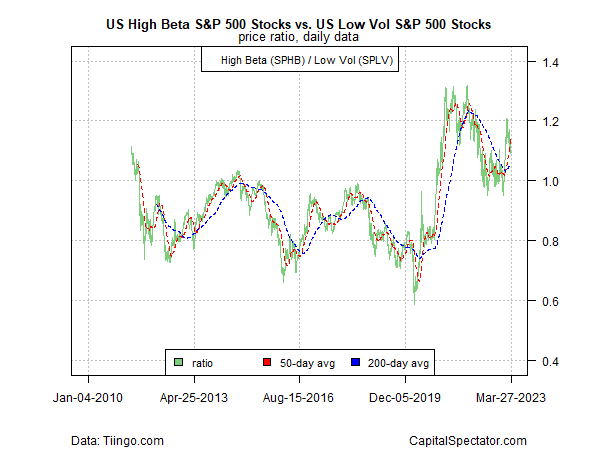

Part of the unwinding of relative strength for value and small-cap risk factors is linked to the revival in risk-on sentiment generally for US equities, based on the ratio for high-beta stocks (SPHB) vs. low-volatility names (SPLV).

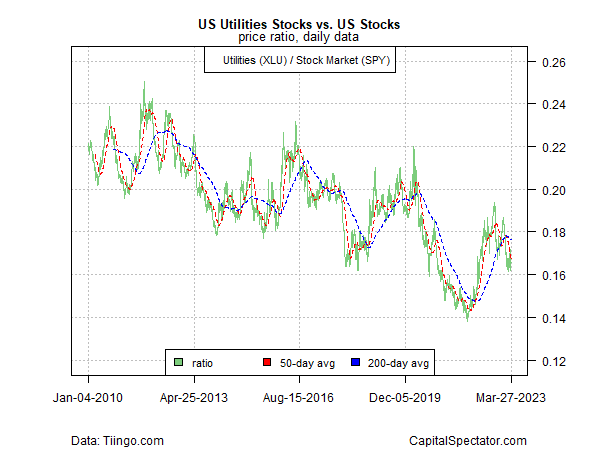

The rebound in risk-on sentiment is also clear from the renewed weakness in the perceived safe haven of utilities stocks (XLU) vs. broad-defined equities (SPY).

To the extent that firmer confidence about the future and animal spirits have created new headwinds for small-cap, value and foreign shares, the recent bank turmoil in the US may be a sign that it’s premature to give up hope for those long-suffering markets. The caveat, of course, is that relative outperformance won’t count for much if the bear market resumes for risk assets generally.

More By This Author:

Global Markets Rallied Last Week, Except For Property Shares

US Bonds Rally As Market Considers Pause Or End For Rate Hikes

Another Fed Rate Hike Keeps Policy Modestly Tight

Disclosure: None.