Everything, Everywhere, All At Once

Image Source: Pixabay

The last major recession began in 2007. Since then, central banks have done everything in their power to avoid such an event. But then, inflation.

Today, central banks would choose a recession over prolonged inflation. The problem is, they can implement policies that will encourage a slowdown, but they don’t have much ability to adjust the severity of the slowdown. There is no volume knob they can turn to fine-tune the impact of their rate hikes.

To borrow a tired cliché, recessions can be described as a series of falling dominoes. In 2008, there was one giant domino: housing.

Today, there are lots of dominoes on the table, many of them wobbling. The dominoes I’m watching today all lead to one place: banks.

Banks are losing deposits because of the Fed. A year ago, the 3-month Treasury bill was paying 0.67%. Today it’s at 4.75%. Yet banks are not paying depositors. All the money the Fed injected into the system during the pandemic has been sitting in banks. Now those depositors want some yield. It’s not hard to find.

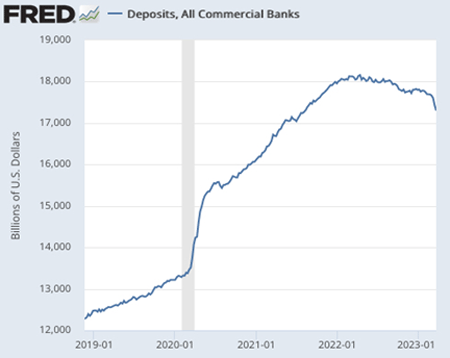

Total deposits at all US commercial banks hit a high of $18.15 trillion in April 2022. That number has since dropped to $17.3 trillion as of March 22 this year. Still high, but the trend is alarming—$850 billion of capital has left the banking system in the past 12 months.

Source: St. Louis FRED

The trend got underway when the Fed started hiking rates last year. The pace of deposit flight has not been linear and has radically accelerated since last month’s bank failures shook the confidence of depositors.

Jim Bianco (a must-follow on Twitter) makes a great point: deposit outflows aggravated the bank failures, and not the other way around, as big media is quick to claim.

Where did all that money go? Into higher-yielding investments like money market funds (MMFs) and T-bills. Data from the Investment Company Institute—an association representing investment funds—shows that total MMF assets jump $574 billion between mid-November 2022 and the end of March.

The pace of outflows took bankers by surprise because they are in some ways invisible. No one shows up at the teller desk asking for their money. Instead, you pick up your phone, click your favorite financial app, and move your cash in a matter of minutes. Your options go well beyond money market funds.

Today, there are ETFs like TBIL that invest in the latest 3-month Treasury bill, distribute monthly dividends, and offer instant liquidity (this is not an endorsement).

Cash has never been more portable. SVB saw $42 billion in outflows in one day. Much of that was probably done using a phone. Incredible.

Banks face a hard decision. They can either raise the rates they pay depositors, which reduces their profitability, or they can continue to keep savings rates low, and bleed deposits.

Either way, banks’ ability to lend could be impaired. Investors seem to agree. Here’s a chart of IAT, the iShares U.S. Regional Banks ETF:

Source: StockCharts.com

I believe this will lead to a liquidity crunch.

According to CNBC, there are $1.4 trillion in commercial real estate loans coming due in 2023 and 2024. Those loans will need to be refinanced. This is going to be a challenge with interest rates at current levels.

Add in a liquidity crunch, and “a challenge” turns into a much bigger problem. I discussed this with two of CBRE’s top members of their capital markets group. We went deep into what’s happening in the office sector, and where they both play in the $100+ million property market (there is a link to the video at the end of this letter).

It’s not pretty. The CMBS (commercial mortgage-backed security) market is locked up. Most banks have already walked away from the sector. Life Insurance companies are cherry-picking the absolute best properties to lend against, and even then, offering approximately 50% loans to value.

It's not just commercial real estate.

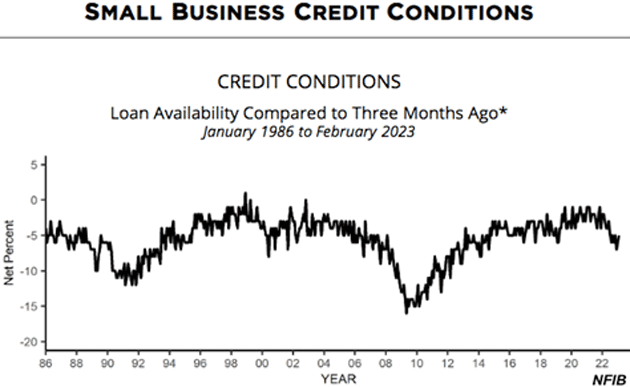

Source: National Federation of Independent Business

According to the National Federation of Independent Business (NFIB), access to credit recently dipped to an 8-year low (seen in the above chart). This data is the result of surveying business operators.

If a business sees a slowdown due to a recession, it may lean on its line of credit to get through. If banks are in search of cash, they might call the credit line—right when it is needed most.

These are when opportunities for well-capitalized investors arise. Private equity will have a field day… or will it?

Bloomberg recently published an excellent article on “hidden leverage” in the banking system (if you have a subscription, you can read it here). It notes that private equity firms, along with institutional investors and specialty lenders, are part of an intricate web of debt in our economy.

A company borrows from a bank, but it may also borrow from its private equity group owner, who in turn has borrowed debt directly. It makes calculating total leverage and interdependencies in the economy a real challenge. More on this next week.

More By This Author:

Disturbing ThoughtsAre Banks Signaling A Recession?

Recession Odds Rising