A Couple Of Tough Weeks For Hedge Funds

Image Source: asbe-iStockPhoto

Hedge funds have experienced some of their worst performance ever over the last couple of weeks. Our best estimate of March performance has the industry down roughly 3%, with most of that loss being booked in the past week or so. This magnitude of losses over this time frame is not unheard of -- it happens roughly every couple years -- but it has been unusual to see such weak performance at a time when traditional portfolios have been pretty stable.

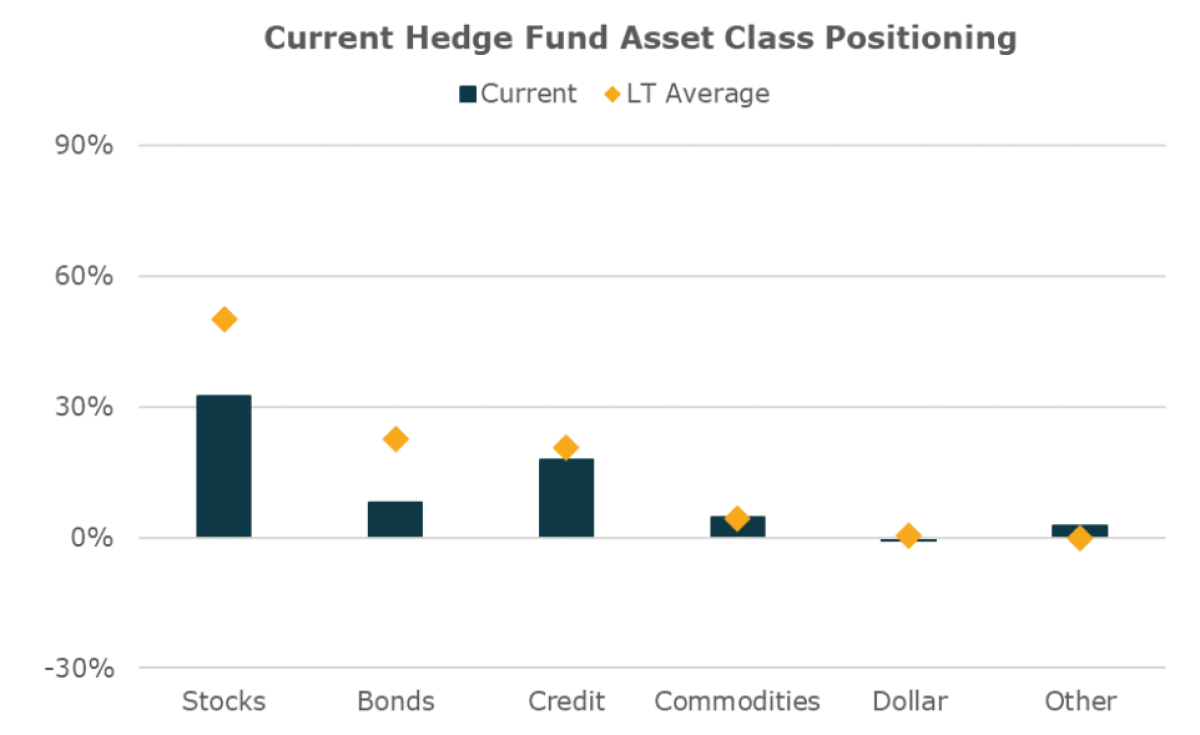

The reason is that nearly every hedge fund position tilt has underperformed. Hedge funds came into the period underweight with bonds, growth stocks, large-caps, and domestic stocks on a relative basis. While many of those bets had been doing well, nearly all of those bets reversed course as the stress on Silicon Valley Bank and Credit Suisse emerged.

The magnitude of the underperformance of these crowded trades suggests that an important driver has been hedge funds themselves rapidly de-grossing their books in response to elevated uncertainty and counterparty risks. While these positions have underperformed, there is an end in sight once managers get closer to desired risk targets and pricing shifts to offer potentially even better alpha opportunities.

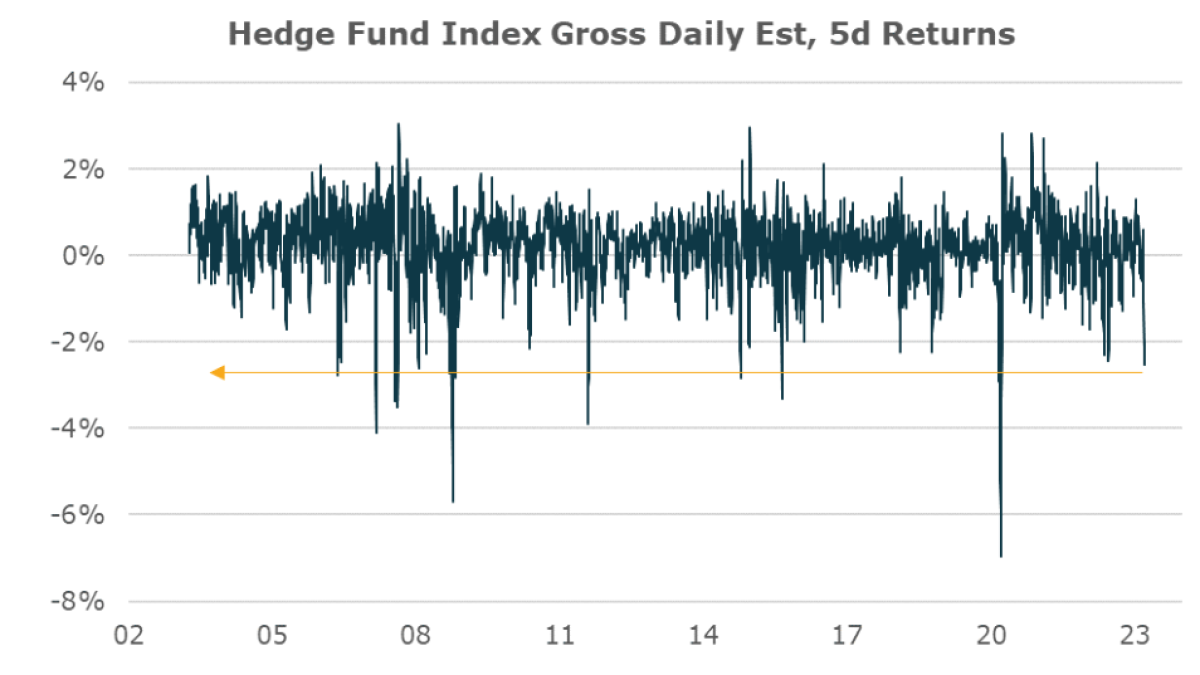

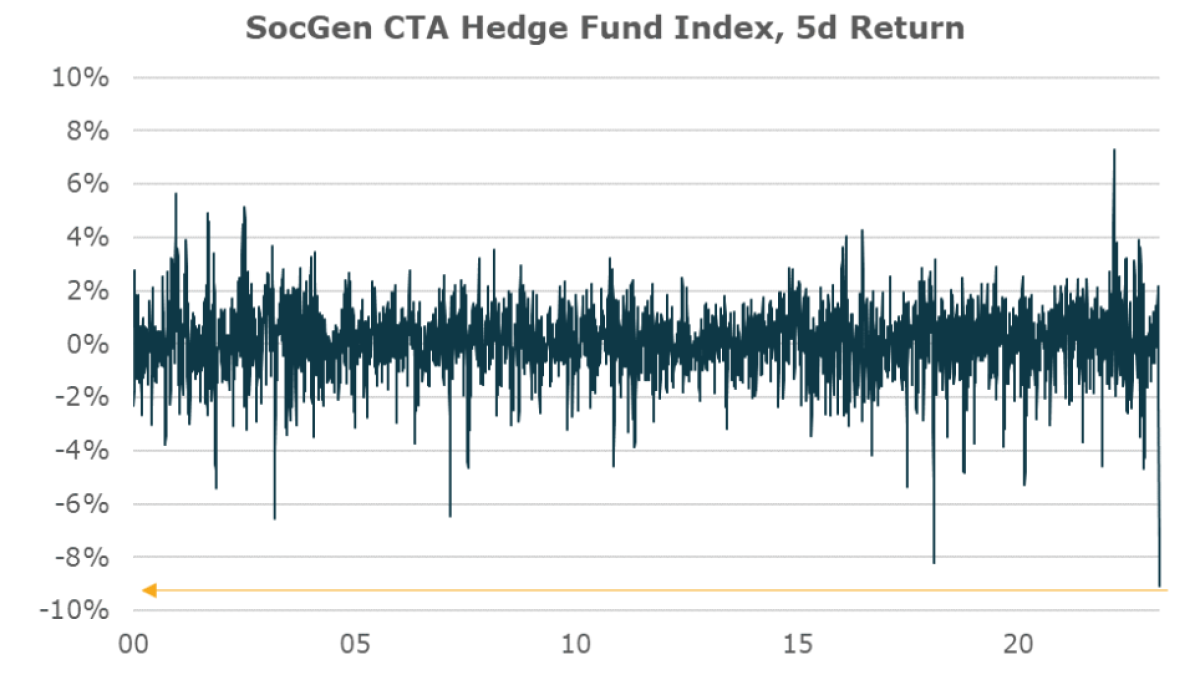

The first chart puts the recent weak performance into perspective, focusing on the previous week. Our best timely estimate of fund performance was down almost 3% on the week.

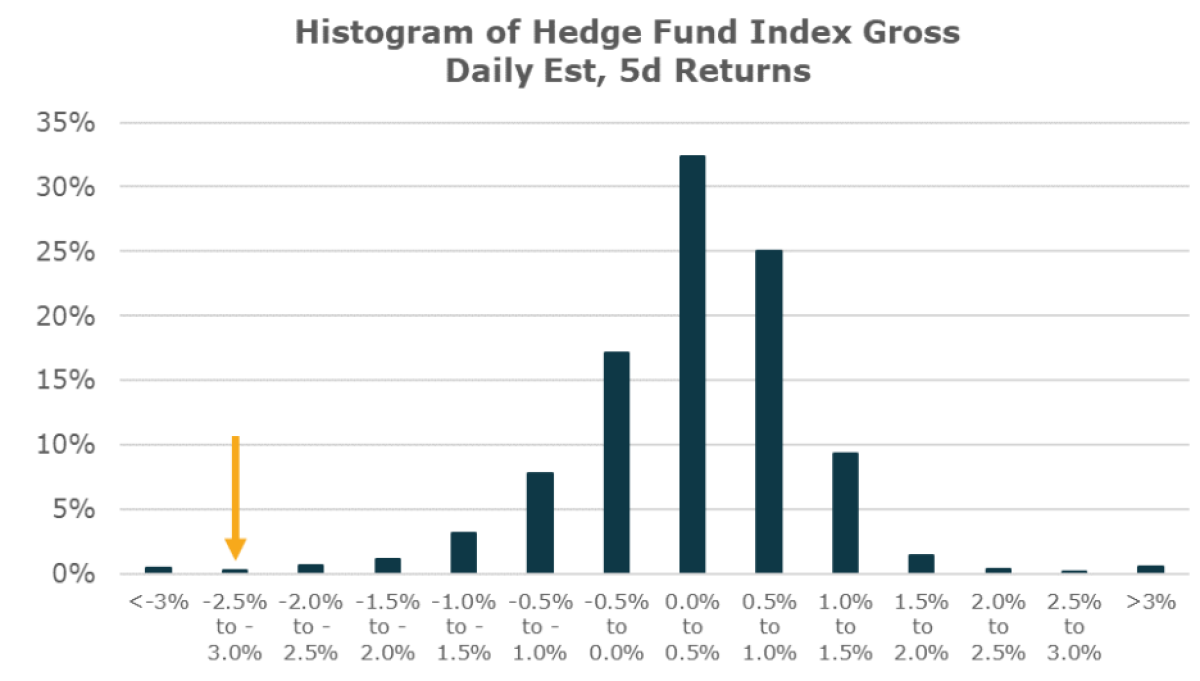

While a loss of that size feels considerable, it is a moderately common occurrence. The chart below shows a histogram of rolling five-day hedge fund performance since 2003. This magnitude of weakness happens about 1% of the time, or about one week every few years.

Hedge funds came into the period positioned for a continuation of the late cycle dynamics that had been in place for many months. Funds were considerably underweight duration as macro funds in particular put on large bets, expecting rates to continue to rise relative to what was priced in. They were also underweight equity risk coming into the period.

What equity risk they were taking was also rather conservatively positioned. Funds were significantly underweight growth stocks, large stocks, and US stocks relative to the rest of the world.

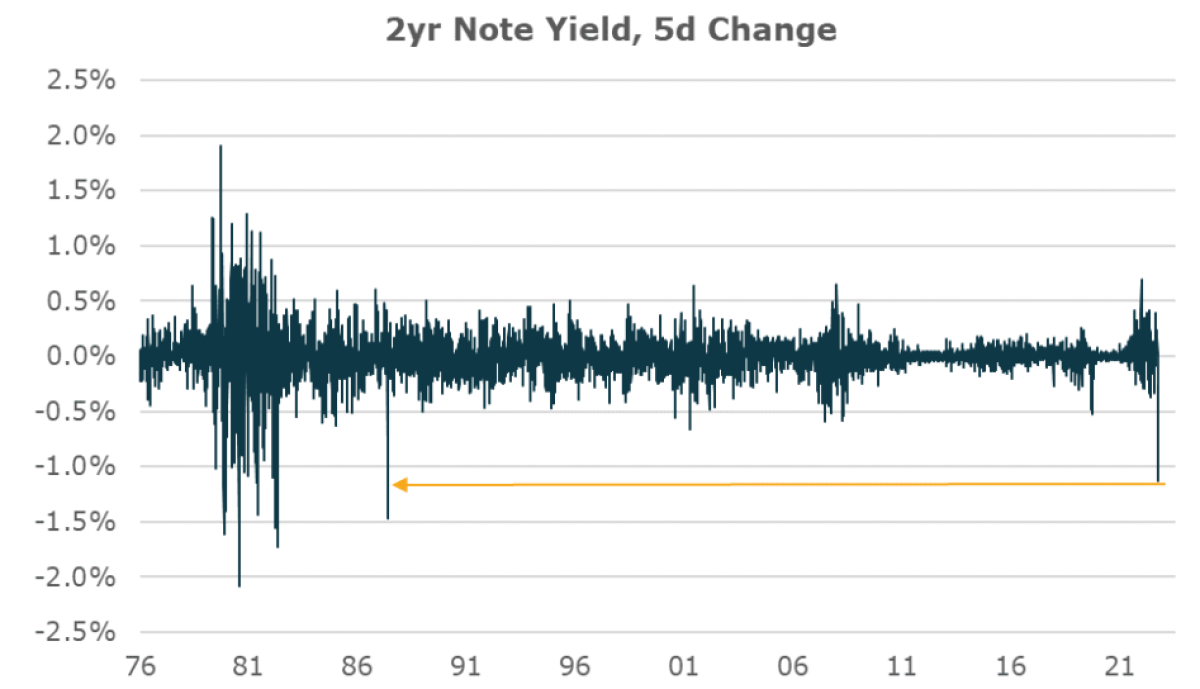

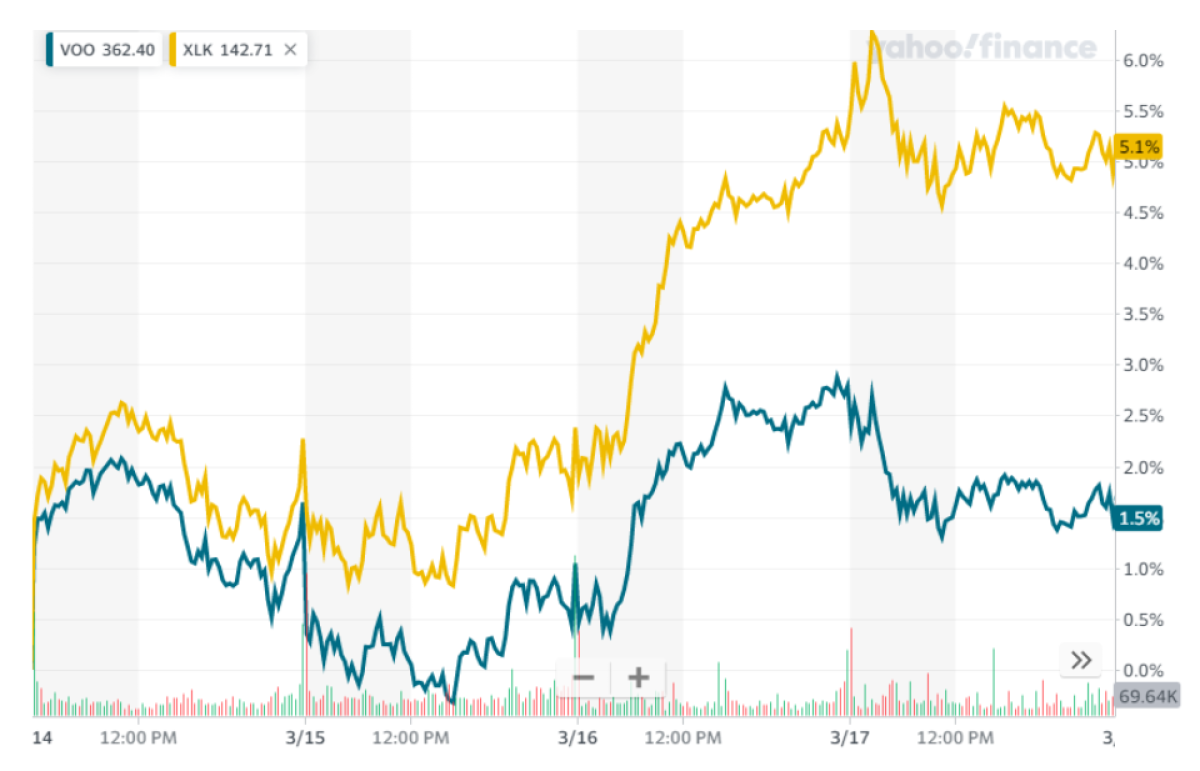

As the SVB issues emerged, nearly all these position tilts underperformed. The most substantial was macro funds' significant short positions in the 2-year interest rate. Rates on 2-year bonds fell more the previous week than any other time since the ‘87 crash. There are indications that funds may have been caught in a short-squeeze dynamic and were being margin called on their positions, which exacerbated the declines in rates.

Trend following approaches also experienced a uniquely poor period as well, with the CTA index seeing its worst week of performance in 25 years. Many of these funds were positioned for a continuation of the inflationary, late cycle tightening of monetary policy.

The deflationary risk from a banking crisis quickly drove a change in fundamental conditions and market action, which caught many of these funds offside. Part of what exacerbated the moves was also the way that these funds adjusting their positioning in response to extreme, counter-trend market action.

Stock picking funds also experienced what looks to be a short squeeze dynamic, as well. Nearly all the major tilts these funds had in place underperformed the week. The breadth of the underperformance of their tilts (many of which were unrelated to each other or counterintuitive) suggests de-grossing may have been a big driver.

Funds came into the period significantly underweight growth stocks. But even as financial risk rose, growth stocks outperformed significantly.

Similarly, funds were positioned specifically short the tech sector. Those stocks saw some of the best performance in the market last week.

Funds came into the period overweight foreign stocks relative to US stocks, positions which saw similar underperformance last week. The unusual outcome of a banking crisis in the US resulting in US stock outperformance suggests de-grossing was likely playing a role.

Finally, small-caps particularly underperformed during the period relative to large-caps. Many funds entered the period underweight large companies given their relatively high comparative valuations. The significant underperformance of smaller companies, the vast majority of which were unrelated to regional banks, suggests other influences than views on relative fundamentals.

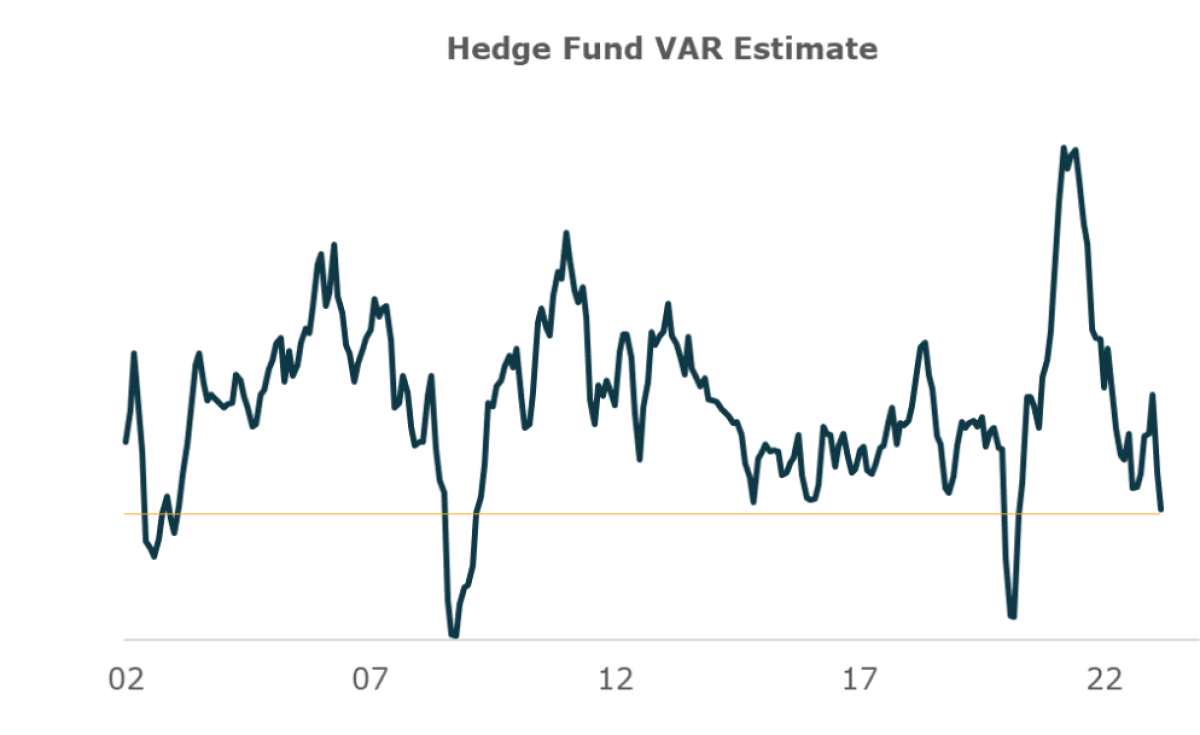

While it has been a rough couple of weeks for hedge funds, there is some relief in sight. The significant recent de-grossing by funds has brought VaR - a measure of risk - from already low levels to by far their lowest outside of the COVID-19 crisis and 2008. As the pace of de-risking slows, there is likely to be less pressure on the crowded hedge fund positions discussed above.

Those positions still have strong fundamental underpinnings that, if anything, have gotten more attractive as markets have priced in a relatively catastrophic deflationary crisis and sector differentials have widened further. While there is never any certainty about how things will play out, there does appear to be more opportunities for hedge funds to generate differentiated returns ahead.

For decades, hedge fund strategies have demonstrated the ability to outperform index investing, and there are good reasons to think that will continue given the resources these funds put into generating alpha. By their nature, these funds derive their returns by seeing corporate or economic environment trends ahead of others and positioning for them.

Those that have followed funds over time have seen this approach work well. But there will be some times like we have recently experienced when trends abruptly reverse for whatever reason (COVID-19, bank crises, etc.), and crowded positions are squeezed, thus causing underperformance. For investors, the trade-off is going through these short-term periods of underperformance to gain access to longer periods of alpha generation.

About the Author

Bob Elliott is the Co-Founder, CEO, and CIO of Unlimited, which uses machine learning to create index replication ETFs of 2&20 style alternative investments like hedge funds, venture capital, and private equity.

Prior to founding Unlimited, Bob was a Senior Investment Executive at Bridgewater Associates where he served on the Investment Committee (G7) and created investment strategies across equities, fixed income, credit, exchange rates, and commodities, including many used in the flagship Pure Alpha fund.

He also built and led Ray Dalio’s personal investment research team for nearly a decade. He’s the author of hundreds of Bridgewater’s widely read Daily Observations, and directly counseled some of the world’s foremost policymakers and institutional investors on economic and investing issues.

Bob has also served as an advisor and executive at several startups including CircleUp, an investment company focused on early-stage consumer brands. There he revamped the investment strategy for the company’s $150 million venture funds approaches to improve decision making. He was also the co-founder of GiveWell, a startup charity evaluator which now directs more than $500 million in annual contributions.

Bob holds a BA in History and Science from Harvard.

More By This Author:

Multi-Strategy Hedge Funds: Jack Of All Trades, Or Master Of None?

Ark Innovation Vs. Invesco Nasdaq In The Dot.Com Bust

Nailing Alternative Investment Portfolio Construction: What Are We Working With?