Multi-Strategy Hedge Funds: Jack Of All Trades, Or Master Of None?

Image Source: Pexels

Citadel made $16 billion in profits in 2022, Millennium made $8.0 billion, and Point 72 made $2.4 billion. These returns are spectacular as all three are multi-strategy funds that allocate capital to hundreds of trading teams.

The goal is to harvest excess returns from many different sources and create a diversified portfolio. The expected return should be low, but still consistently positive and not very volatile. Citadel’s 38% return in 2022 had anything but these features.

Given such stellar performance, the interest in multi-strategy hedge funds has been rising again. We have explored this hedge fund type before and have not come away with a particularly positive impression. This article is a second take on multi-strategy hedge funds.

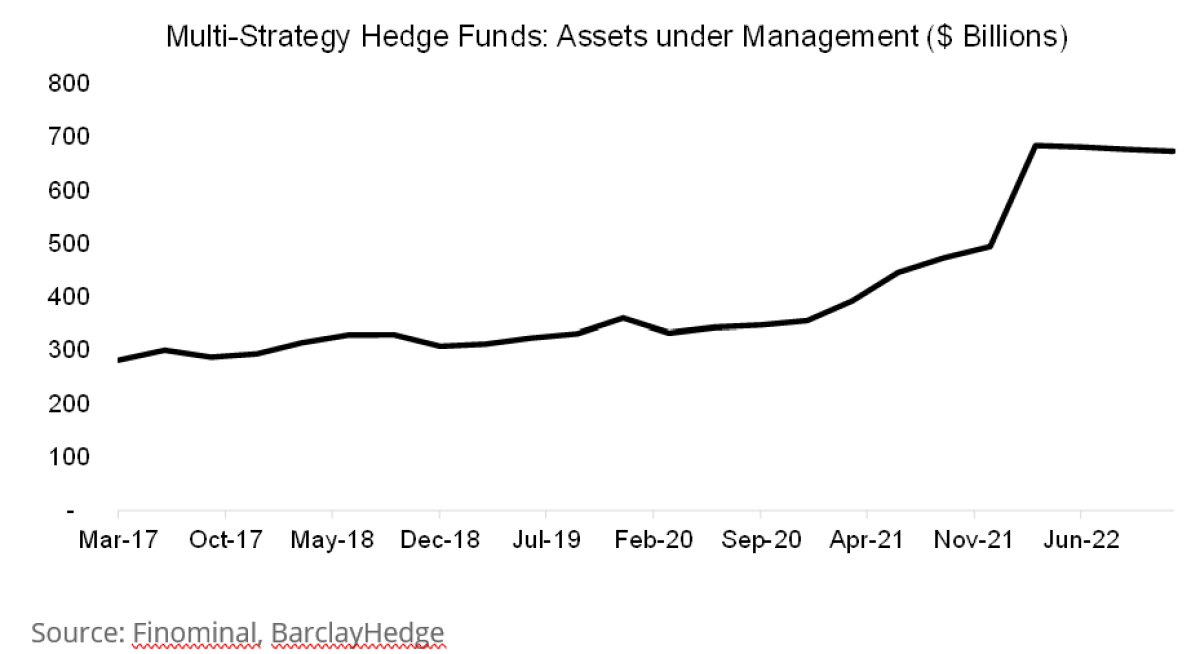

Assets Under Management

Reviewing the assets under management of multi-strategy hedge funds based on data from BarclayHedge highlights that these were approximately $300 billion between 2017 and 2020, but doubled thereafter. Perhaps this indicates that these funds have done well during the COVID-19 crisis that began in March 2020, and they were rewarded with new capital from allocators thereafter.

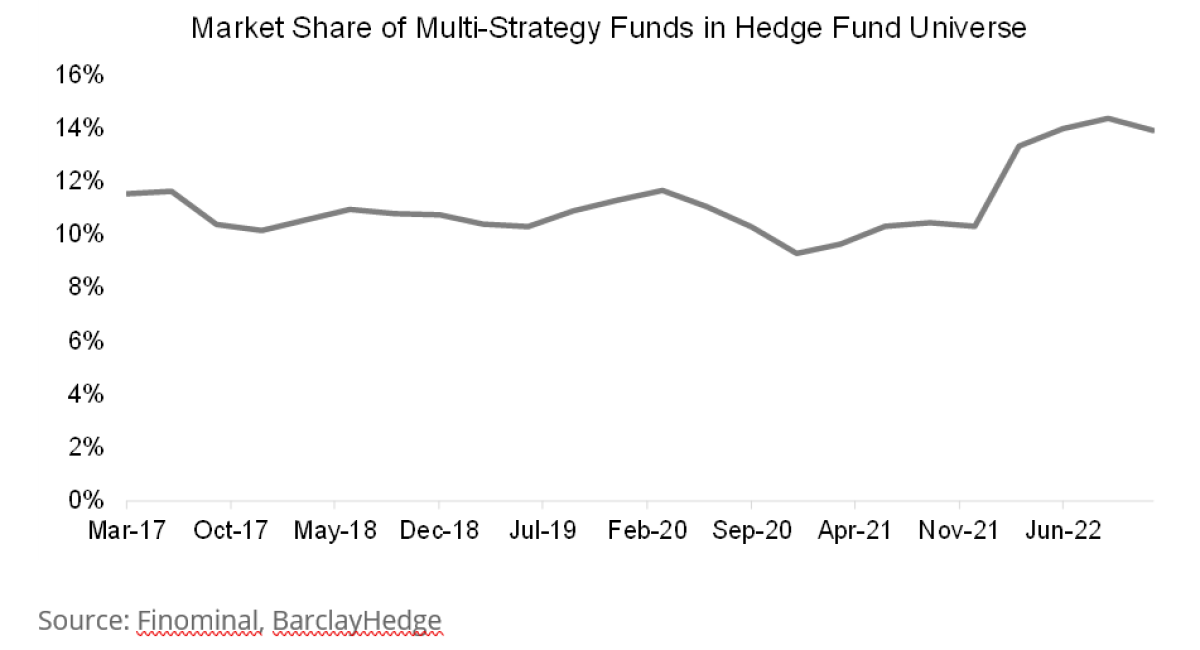

However, calculating the market share of multi-strategy funds as a proportion of the total assets of the hedge fund industry highlights that this has only increased marginally from 12% to 14% over the last five years.

It seems that the increase in assets under management can be attributed to the growth of the entire hedge fund industry, which increased its assets from approximately $3 to $4 trillion in 2020. However, it is questionable how much of this growth can be attributed to inflows from capital allocators versus existing assets appreciating in value. It is worth recalling that the S&P 500 ended the year higher in 2020, despite the global pandemic.

Performance

The idea of a multi-strategy hedge fund is to deploy capital to various teams that generate returns uncorrelated to the stock market and eachother. Risk management tends to be tight, and allocations are often reduced dramatically if drawdowns exceed certain targets, such as a 50% capital reduction at a 5% drawdown. The resulting portfolio tends to be market neutral and is often leveraged aggressively.

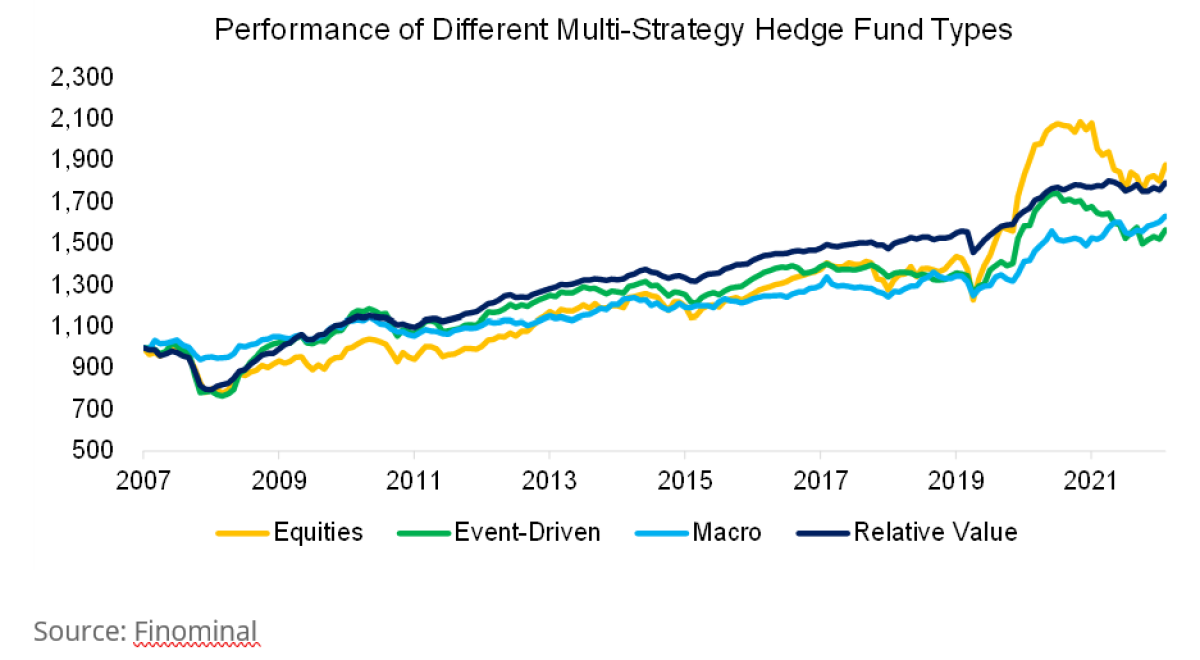

Next, we evaluate the performance of multi-strategy hedge funds by taking HFRI indices from HFRX that offer monthly returns since 2008. These are available for multi-strategy hedge funds focused on equities, event-driven, macro, and relative value. Theoretically, the returns of the four types should be completely different, but the performance since 2008 was remarkably similar.

Correlations

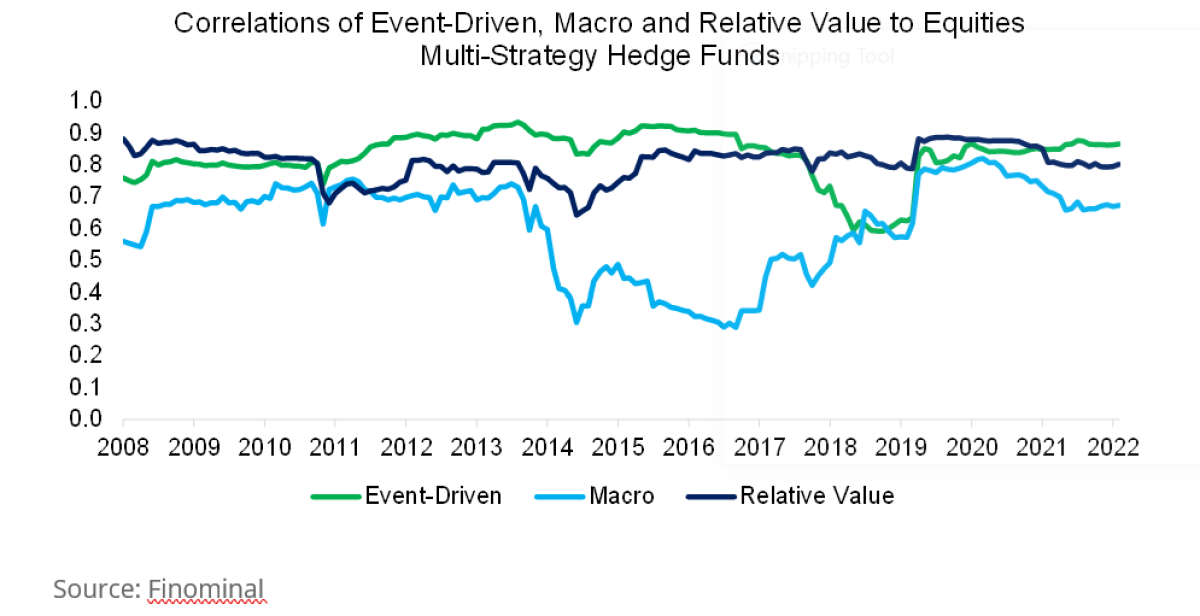

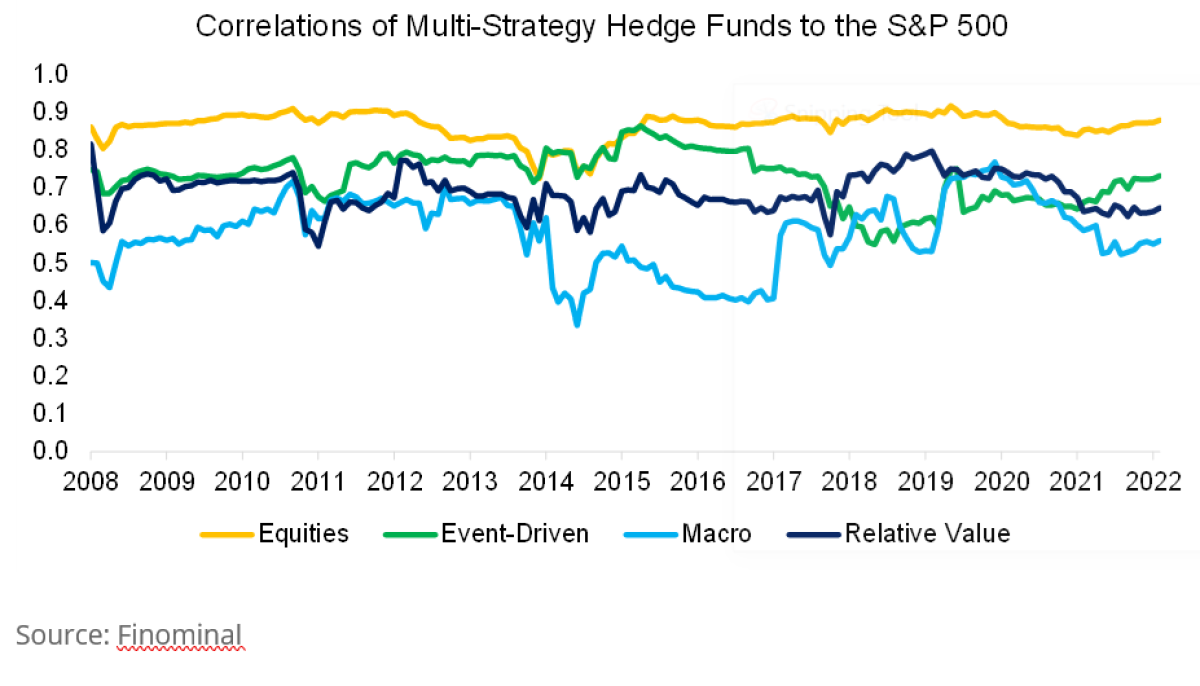

Given the comparable performance, we calculate the 36-month rolling correlations of the event-driven, macro, and relative value strategies to the equity strategy. The average correlations between 2008 and 2022 ranged from 0.6 for macro to 0.8 for event-driven.

Naturally, these correlations are too high, as these should be completely uncorrelated given the different areas of focus. For example, a macro trading team might speculate on the US dollar appreciating versus the Japanese yen, compared to an equities team betting on a recovery of the value factor by going long cheap stocks and short expensive stocks.

The high correlations indicate that these four types of multi-strategy hedge funds offered the same risk exposure. Given their drawdowns in 2008 during the global financial crisis and in 2020 during the COVID-19 pandemic, this likely is simple exposure to the stock market.

Calculating the rolling 36-month correlations to the S&P 500 confirms this, as these ranged from 0.6 to 0.9. Global macro offered the largest diversification benefits -- but not significant ones, given a correlation of 0.6 to stocks.

Naturally, this begs the question of what these multi-strategy fund managers are allocating to as the various trading teams seem to be offering just beta to equities, which most investors already have exposure to. As previously noted, there does not seem to be a lot of hedging going on.

Multi-Strategy Hedge Fund Replication

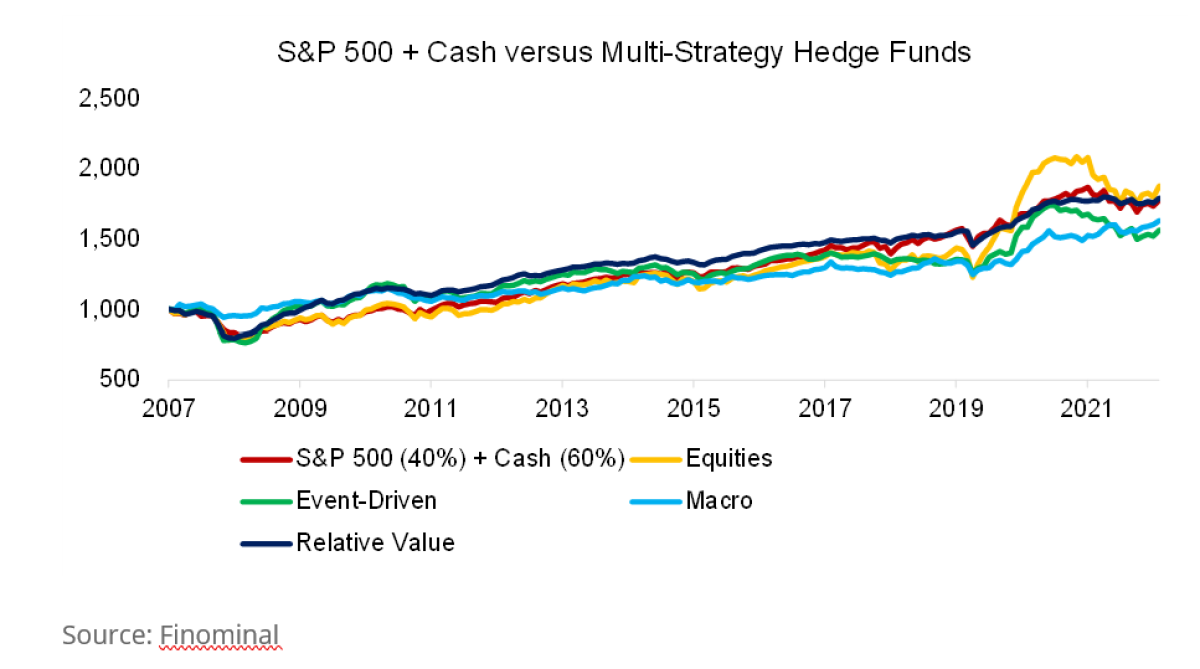

We can replicate multi-strategy hedge funds simply via a portfolio comprised of the S&P 500 and cash. Allocating 40% to stocks and 60% to non-interest-bearing cash would have generated a performance that is almost identical to that of the multi-strategy hedge funds in the period from 2008 to 2022.

Further Thoughts

Our second take on multi-strategy hedge funds confirms our first analysis, namely that these funds primarily offer beta to the stock market and therefore limited diversification benefits. However, this is the conclusion for the average fund, and there are a few select funds like Millennium that have established remarkable track records. Is it worth pursuing these?

Although this may seem desirable, it is not. Some funds made extraordinary amounts of money in 2022, but others lost equal amounts. TCI, which had a stellar track record of 13 profitable years, lost $8 billion. On average, capital allocators will get the average return, which is anything but desirable.

About the Author

Nicolas Rabener is the founder & CEO of Finomial (formerly FactorResearch) and previously founded Jackdaw Capital, an award-winning quantitative hedge fund. Before that, Nicolas worked at GIC and Citigroup. Nicolas holds an MSc from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km ultra-marathon).

More By This Author:

Ark Innovation Vs. Invesco Nasdaq In The Dot.Com Bust

Nailing Alternative Investment Portfolio Construction: What Are We Working With?

Exploring the Link Between Lumber Prices and Timber Markets