“In its boldest effort to protect the U.S. economy from the coronavirus, the Federal Reserve says it will buy as much government debt as it deems necessary and will also begin lending to small and large businesses and local governments to help them weather the crisis….The Fed’s announcement Monday removes any dollar limits from its plans to support the flow of credit through an economy that has been ravaged by the viral outbreak. The central bank’s all-out effort has now gone beyond even the extraordinary drive it made to rescue the economy from the 2008 financial crisis.” (The Associated Press, March 23, 2020)

The current US Fed policy of quantitative easing is really in fact a version of monetizing the public debt.

The idea of monetizing the debt is usually scary for the financial markets, since it is often associated with the thinking that government spending is out of control, and as well, with the expectation that a future wave of inflation on the way.

Monetizing debt is a simple process where the government issues bonds to cover its new spending. The central bank purchases the bonds from the secondary markets, and perpetually rolls them over. Thus, debt monetization leads to an increase in the money supply. In fact, there is no theoretical limit up to which the Fed can expand its balance sheet.

Massive purchases by the Fed may make it seem as if the Treasuries it bought don't exist, but they exist on the Fed's balance sheet, and technically, the US Treasury must pay the Fed back one day.

Until then, the Fed has given the federal government more money to spend, increasing the money supply, and monetizing the debt.

As already noted above, because of the Covid-19 crisis and the effective lockdown of most of the US economy, the US Government and the Fed both intervened massively to support the economy in this period of near suspended animation.

As well, because of the pandemic, most other advanced economies have also provided exceptionally large fiscal support programs, with the central banks, on their side, conducting similarly large purchases of government securities.

In the current weak global economic environment, massive fiscal policy injections supported by central bank debt monetization is entirely appropriate. Indeed, on the fiscal side, much more needs to be done. And of course, it would help if there was some fiscal and monetary policy coordination among the major nations, all aimed at supporting global growth.

The Huge Recent Increase In The Fed’s Balance Sheet

For much of post-war history, the Fed's balance sheet was a rather sleepy topic for economists. Of course, markets understood that small changes in the balance sheet could have dramatic effects on liquidity in all parts of the economy.

And given the size and economic leadership of the US economy, America’s central bank management affects the global economy and of course other central bank actions as well.

The importance of the US dollar even in the face of a rapidly expanding Chinese presence in the world economy remains quite solid. It also helped by the widely held view that the US dollar was, and still is, the closest we have to a real global currency.

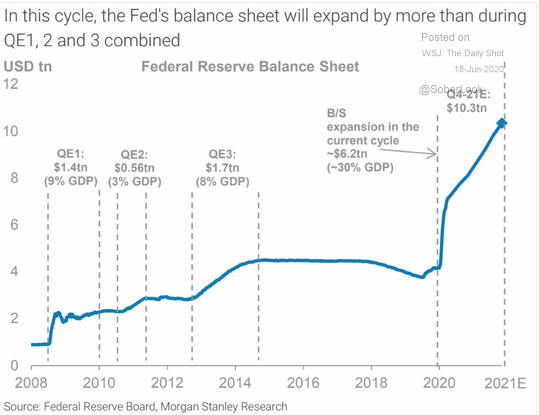

A glance at the following chart underscores how the US central bank policy has changed since the Great financial meltdown of 2008-09.

In that earlier economic crisis, aggressive monetary policy expansion was needed to manage the liquidity problems that emerged during the global meltdown, and to compensate for the rather meager fiscal support the Obama Administration was able to negotiate through Congress. Nevertheless, as the chart indicates, there was a huge expansion in the Fed balance sheet from the $1 trillion level after 2017.

Once again Fed policy and its balance sheet ate important for ensuring that the coming economic recovery is sustained. Thus, the Fed has cut its important benchmark federal funds target rate to a range of 0 percent to 0.25 percent.

As well, the Fed provided the important guidance that policy rates will remain around zero until the economy has fully weathered the economic collapse.

And as the following chart illustrates, the recent emergency measures taken by the Fed this time around far outweigh the measures taken after 2007.

That is, the balance sheet expansion this time is far larger than what occurred during the three previous phases of quantitative easing.

At the same time, the fiscal policy injection into the economy is far larger than what occurred back in 2008-09.

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.