As Congress considers Biden’s stimulus package, economists are debating the merits of a $1.9 trillion relief package. The debate centers on whether the government response is appropriate or goes well-beyond what is needed to promote recovery. Former Secretary-Treasurer, Larry Summers, on one side, argues that the proposed is excessive, possibly resulting in the economy overheating and ultimately leading to an acceleration in inflation. Countering his argument, the current Treasury Secretary, Janet Yellen, advocates that the administration has to “go big” this time. Former Obama officials recognize that the government’s response to the 2008 crisis was well short of the mark, consequently the economy never really fully recovered from that financial crisis. Today’s COVID-19 crisis, they argue, is even deeper and more destructive than that of 2008.

The economics profession continuously examines the multiplier effects of government expenditures in response to economic crises. How large is the stimulus impact of fiscal spending? By definition, the fiscal multiplier is the change in real GDP caused by an increase in government spending. For example, if government spending increases by one dollar and this results in a 50 cent increase in GDP, then the government consumption multiplier is 0.5. So, just how impactful are government expenditures to kick start an economy and restore economic growth?

In his most recent report to clients, Lacy Hunt of the Hoisington Investment Management tackles this issue. He concludes that:

“Despite the fact that much of the expenditures by the federal government are useful to provide a cushion from lost income and output, the size of the outlays has created some concern regarding future inflation. That particular debate can revolve around the macroeconomic effects of fiscal stimuli (fiscal multipliers) …. It is our conclusion that U.S. fiscal multipliers are in fact negative for noninvestment type of spending.

Lacy Hunt highlights that excessive debt is one of the key factors contributing to the failure of fiscal multipliers, to wit:

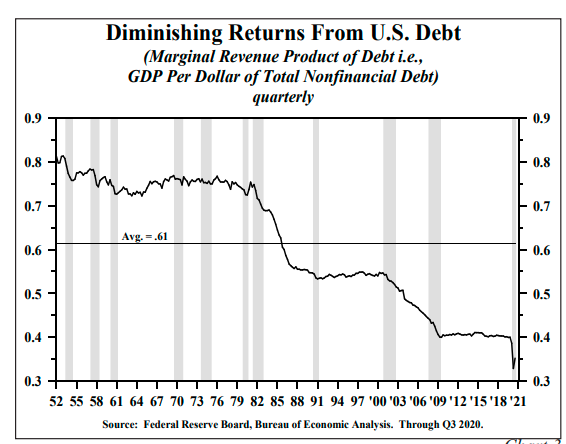

“When debt capital, like any other factor of production, is overused its marginal revenue product declines. This serves as a persistent drag on economic activity that restrains growth despite the best efforts of monetary and fiscal policy.”

The accompanying chart dramatically documents that the US has persistently suffered from declining marginal productivity of debt since the late 1980s. The pandemic has resulted in further destruction of capital in the economy. Daily, there are reports of specific industries experiencing historic losses. Also, physical capital in commercial real estate and the travel industry, for example, is at great risk of shrinking the longer the pandemic continues. The severity of the downturn has decimated tens of thousands of small businesses. This loss of productive capital only contributes to diminishing returns from debt.

(Click on image to enlarge)

Government stimulus efforts are fully financed by debt creation. Hence, we should not expect any real lasting boost to the economic performance from these stimuli programs. With each additional dollar of debt, we continue to get less bang for the buck. Hunt concludes that with “the debilitating impact on the growth of excessive debt and the restriction of the zero bound on monetary stimulus, a secular inflation cycle is not at hand”. The financial markets are anticipating a rapid bounce back, if not a boom, starting later in 2021, once the economy is fully open. However, Hunt’s analysis dismisses the prospect of inflationary conditions, hence he remains quite bullish on long-term bond yields falling.

Comments

Log in or sign up to join the conversation.