Image Source: Pexels

Donald Trump and Xi Jinping's accord, the Bank of Japan's rate decision, and Federal Reserve Chair Jerome Powell's cautious remarks dominate investor focus amid upcoming European earnings reports. Asian markets are predominantly up on Thursday, influenced by the varied signals from Wall Street the previous night, as optimism grows regarding a trade agreement between the U.S. and China. Traders are also responding to the recent quarter-point interest rate reduction by the U.S. Federal Reserve. The Bank of Japan kept interest rates unchanged but reaffirmed its commitment to raising borrowing costs if the economy aligns with its forecasts, directing investor attention toward the possibility of a rate increase as early as December.

President Trump and President Xi engaged in a nearly two-hour meeting on Thursday, local time, during the APEC summit in South Korea. While aboard Air Force One, Trump praised the meeting as "amazing" and "outstanding". He announced that the fentanyl tariff on Chinese imports will be reduced to 10% immediately, while many other tariffs will stay in place. Trump also mentioned that China will start purchasing soybeans again without delay and confirmed that China will refrain from implementing rare earth controls. While Trump called it "amazing", markets remain cautious, awaiting China's perspective. Global stocks surged, with Chinese equities nearing decade highs.

The progressive Democrats 66 party appeared set to secure victory in the Dutch parliamentary elections after voters rejected Geert Wilders’ far-right Freedom Party and expressed support for more traditional political factions. Meanwhile, US President Donald Trump and South Korean President Lee Jae Myung completed a trade agreement on Wednesday, concluding months of negotiations over the implementation of a framework deal established in July. Nvidia reached a remarkable market capitalisation of $5 trillion on Wednesday, as Chief Executive Officer Jensen Huang’s series of acquisitions propels the boom in artificial intelligence to unprecedented levels.

The Fed cut rates by 25bps to a 3.75-4.0% target range, but Powell downplayed expectations for another cut in December, stating it’s “not a foregone conclusion.” He emphasized the need to wait, citing unclear data and FOMC divisions. Schmid dissented against the cut, while Miran supported a larger 50bps cut. The dot plot shows 9 of 19 members support no further cuts or only one more this year. Market expectations for a December cut dropped from ~90% to ~70%, with 2-year yields rising ~10bps to 3.6%. Equities initially reacted negatively but later recovered. QT will end on December 1, with maturing MBS holdings reinvested into T-bills and redeeming Treasuries reinvested into Treasuries.

The upcoming ECB meeting is expected to be uneventful, with consensus predicting the Depo rate to remain at 2% and minimal chances of a cut. Lagarde is unlikely to signal policy changes during her press conference. Inflation forecasts hover around 2%, placing the Governing Council in a stable position on price stability. Risks persist, with German fiscal stimulus offering optimism but weaker trade dynamics and potential impacts from Trump tariffs posing challenges. While Q3 GDP data is released today, external demand concerns are unlikely to influence policy decisions yet.

Overnight Headlines

- EZ GDP Set To Tick Higher; Growth Could Come From German Spending

- Lacking Impetus, ECB Likely To Hold Rates Again

- BoJ Holds Rates In First Meeting After Japan PM Takaichi’s Ascent

- Powell’s December Warning Exposes Hardening Divisions At Fed

- HKMA Cuts Base Rate By 25bps To 4.25%

- Trump Says Xi Meeting Yielded Fentanyl Tariff Cut To 10%

- Trump Orders Nuclear Weapons Trials After Russia Tests

- EU States Plan To Help Move Tanks Across Continent In Case Of War

- Dutch Far Right Loses Ground In Elections As Centrists Gain

- Google Revenue Soars To Record As AI Boom Lifts Cloud Business

- Microsoft’s Cloud Services Power Earnings Beyond Expectations

- Meta Projects Higher Expenses, Takes One-Time Tax Charge

- Starbucks Café Sales Stabilise After Prolonged Slide

- eBay Reports Q3 Sales, Merchandise Volume Rise

- Chipotle Cuts Outlook Again In 2025 On Weak Traffic

- ServiceNow Sees Strong AI-Driven Growth, Highlights Spending Cuts

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.1725 (EU1.2b), 1.1650 (EU948.5m), 1.2000 (EU933.8m)

- USD/JPY: 135.00 ($1.68b), 125.00 ($1.68b), 150.00 ($908m)

- USD/CAD: 1.4015 ($1.66b), 1.3675 ($1.1b), 1.3965 ($1.01b)

- USD/BRL: 5.3500 ($380m), 5.5125 ($320.3m)

- AUD/USD: 0.6515 (AUD864.9m), 0.6550 (AUD501.1m), 0.5700 (AUD481.4m)

- GBP/USD: 1.3000 (GBP367.7m)

- USD/CNY: 7.1250 ($449.1m), 7.1150 ($350m), 7.1200 ($300m)

- EUR/GBP: 0.8750 (EU429.1m)

CFTC Positions as of the Week Ending 9/10/25

-

October 1, 2025: During the shutdown of the federal government, Commitments of Traders Reports will not be published

Technical & Trade Views

SP500

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 6872 Target 6952

- Below 6862 Target 6808

(Click on image to enlarge)

EURUSD

- Daily VWAP Bullish

- Weekly VWAP Bearish

- Below 1.1668 Target 1.1526

- Above 1.1668 Target 1.1739

(Click on image to enlarge)

GBPUSD

- Daily VWAP Bearish

- Weekly VWAP Bearish

- Below 1.33 Target 1.3085

- Above 1.33 Target 1.3369

(Click on image to enlarge)

USDJPY

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Below 150.50 Target 147.78

- Above 150.50 Target 154.48

(Click on image to enlarge)

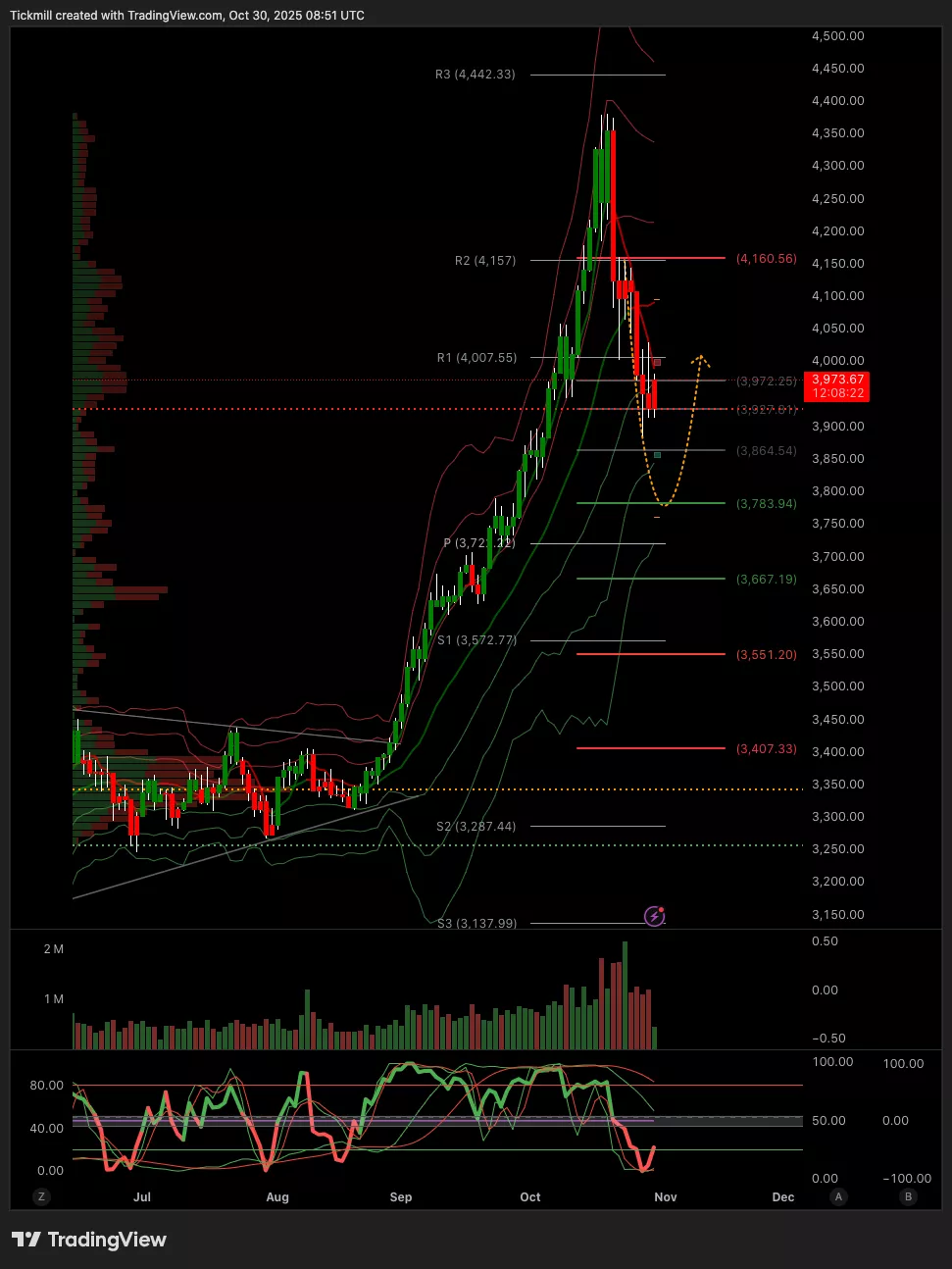

XAUUSD

- Daily VWAP Bearish

- Weekly VWAP Bullish

- Above 4046 Target 4345

- Below 4046 Target 3684

(Click on image to enlarge)

BTCUSD

- Daily VWAP Bearish

- Weekly VWAP Bearish

- Above 113k Target 118k

- Below 112k Target 107k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Wednesday, Oct. 29

Daily Market Outlook - Wednesday, Oct. 29

The FTSE Finish Line - Tuesday, Oct. 28

Comments

Log in or sign up to join the conversation.