Image Source: Pixabay

Treasury yields and the dollar are down, indicating a potential shift in investor sentiment, while stocks are slightly higher in Asia, suggesting cautious optimism among investors. The U.S. government may shut down on Wednesday if no agreement is reached. President Trump is set to meet with congressional leaders, but expectations for a resolution are low, as both parties might benefit politically from a shutdown. Analysts from Bank of America (BofA) estimate that a shutdown could reduce GDP by 0.1% per week, although this loss would be recovered once the government reopens. Historically, previous shutdowns have had minimal impact on financial markets, likely due to investor confidence that public pressure will lead to a resolution. The timing is concerning, as a shutdown could delay the September payrolls report and complicate the Federal Reserve's decision-making during its meeting on October 29. Currently, markets predict an 89% chance of a rate cut. New tariffs on big trucks, patented drugs, and other items are set to take effect on Wednesday, but details remain unclear. There are also considerations for imposing tariffs on foreign electronic devices based on chip counts, though specifics on implementation are uncertain. Trade partners may feel apprehensive about negotiating deals with the Trump administration due to the unpredictability of new tariffs. Trump is scheduled to attend a meeting with top U.S. military officials on Tuesday, called by Defense Secretary Hegseth. Investors are navigating a complex landscape with potential government shutdowns, shifting trade policies, and upcoming economic reports. The uncertainty surrounding these factors is likely to influence market behavior in the short term.

The August Personal Income and Outlays report revealed no major surprises. Headline PCE increased by 0.26% month-over-month, resulting in a year-over-year rate of 2.74%, up from 2.60%, which aligned with expectations. Core PCE held steady at a 0.23% month-over-month pace, with the year-over-year rate rising to 2.91% from 2.85% when considering the second decimal place. This outcome was broadly in line with forecasts. On the goods side, gasoline prices rose by 1.63% month-over-month, and food prices increased by 0.47% month-over-month. However, a significant rise in other durables, which saw a 1.97% month-over-month increase, was offset by declining prices for recreational goods and vehicles, which dropped by 1.71% month-over-month. In terms of services, transportation costs increased by 0.92% month-over-month, which was also reflected in nominal spending figures. Overall, there appears to be ongoing demand pressures influencing inflation, although it is challenging to identify any significant impacts from tariffs. Most price increases can be attributed to commodity fluctuations. The income and spending figures showed continued momentum, with income rising by 0.4% month-over-month and spending increasing by 0.6% month-over-month, both exceeding expectations by a tenth. When adjusted for inflation, these flows appear softer, yet there has not been a discernible shift in the trend. This situation contrasts with weaker survey data and a deterioration noted in employment reports, although the aggregate numbers tend to obscure a more rapid slowdown in individual real income growth.

In the coming week, the U.S. labor market will take center stage with a series of important data releases. Job openings will be reported on Tuesday, followed by the ADP employment report on Wednesday. Initial jobless claims are scheduled for Thursday, culminating in the monthly employment report on Friday. Even if the headline employment gain is weak, the low unemployment rate of 4.3% is likely to limit changes in expectations regarding the response of a divided Federal Reserve. On the U.S. front, consumer confidence data will also be released on Tuesday, along with factory orders data on Thursday. There will be a steady stream of Federal Reserve speakers, and attention will remain on the risks associated with a potential government shutdown. In the euro area, the flash September CPI print will be released on Wednesday, following data from member states such as Germany and France on Tuesday. With limited deviations from the 2% inflation target expected for the time being, policy expectations should remain relatively stable after these reports. In the UK, the most significant data release will likely be the Bank of England’s Decision Maker Panel on Thursday, especially as quality issues are increasingly impacting data from the Office for National Statistics (ONS). Additionally, several Monetary Policy Committee (MPC) members, including Lombardelli, Breeden, and Mann, will be speaking on Tuesday, and there may be important fiscal insights from the Labour Party conference occurring from Sunday to Wednesday. In Australia, the Reserve Bank of Australia (RBA) will announce its latest rate decision on Tuesday.

Overnight Headlines

- OPEC+ Seen Likely To Approve Another Output Hike For November

- Gold Holds Near Record As Traders Weigh US Shutdown, Fed Rates

- Asian Currencies Mostly Strengthen Amid US Govt Shutdown Risks

- China Industrial Profit Rose Sharply In August

- UK Job Postings Fall, Firms Downbeat About Outlook, Surveys Show

- Trump To Host Last-Ditch Talks To Avoid Government Shutdown

- Fed’s Miran Math May Overstate Impact Of Immigration On Inflation

- Trump And Netanyahu Set For Crunch Talks Over New Gaza Peace Plan

- Iran Hit With Reimposition Of Sanctions Over Its Nuclear Programme

- Occidental Petroleum In Talks To Sell OxyChem Unit, FT Says

- Sony Financial Debut On Tokyo Stock Exchange After Spinoff

- AI Boom Powers Triple-Digit Gains In China’s Hardware Stocks

- China’s Markets Shed ‘Uninvestable’ Tag As Global Funds Return

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- USD/JPY: 147.00 (275M), 147.50-55 (376M), 148.00 (260M), 150.70 (410M)

- EUR/JPY: 174.45 (568M). USD/CHF: 0.8140 (270M). AUD/JPY: 0.9500 (500M)

- GBP/USD: 1.3300 (324M), 1.3355-65 (262M), 1.3550 (361M)

- EUR/GBP: 0.8640 (322M), 0.8700 (322M), 0.8730-35 (571M), 0.8780-85 (608M)

- AUD/USD: 0.6470 (360M), 0.6550-60. (517M), 0.6600 (412M)

- 0.6625 (2.0BLN), 0.6725 (2.32BLN), 0.6810 (573M)

- USD/CAD: 1.3785-95 (428M), 1.3800-10 (1.4BLN), 1.3875-80 (713M)

- 1.3940-50 (239M), 1.3960 (236M), 1.3990 (574M)

CFTC Positions as of the Week Ending 26/9/25

- Speculators trim CBOT US Treasury bonds futures net short position by 15,347 contracts to 78,791

- Speculators trim CBOT US Ultrabond Treasury futures net short position by 7,408 contracts to 270,759

- Speculators increase CBOT US 10-year Treasury futures net short position by 24,817 contracts to 844,116

- Speculators increase CBOT US 5-year Treasury futures net short position by 16,670 contracts to 2,453,444

- Speculators trim CBOT US 2-year Treasury futures net short position by 103,272 contracts to 1,300,198

- Equity fund managers raise S&P 500 CME net long position by 20,454 contracts to 912,089

- Equity fund speculators trim S&P 500 CME net short position by 31,451 contracts to 443,946

- Japanese yen net long position is 79,500 contracts

- Euro net long position is 114,345 contracts

- British pound net short position is -1,964 contracts

- Swiss franc posts net short position of -23,018 contracts

- Bitcoin net long position is 79 contracts.

Technical & Trade Views

SP500

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 6440 Target 6666

- Below 6600 Target 6500

(Click on image to enlarge)

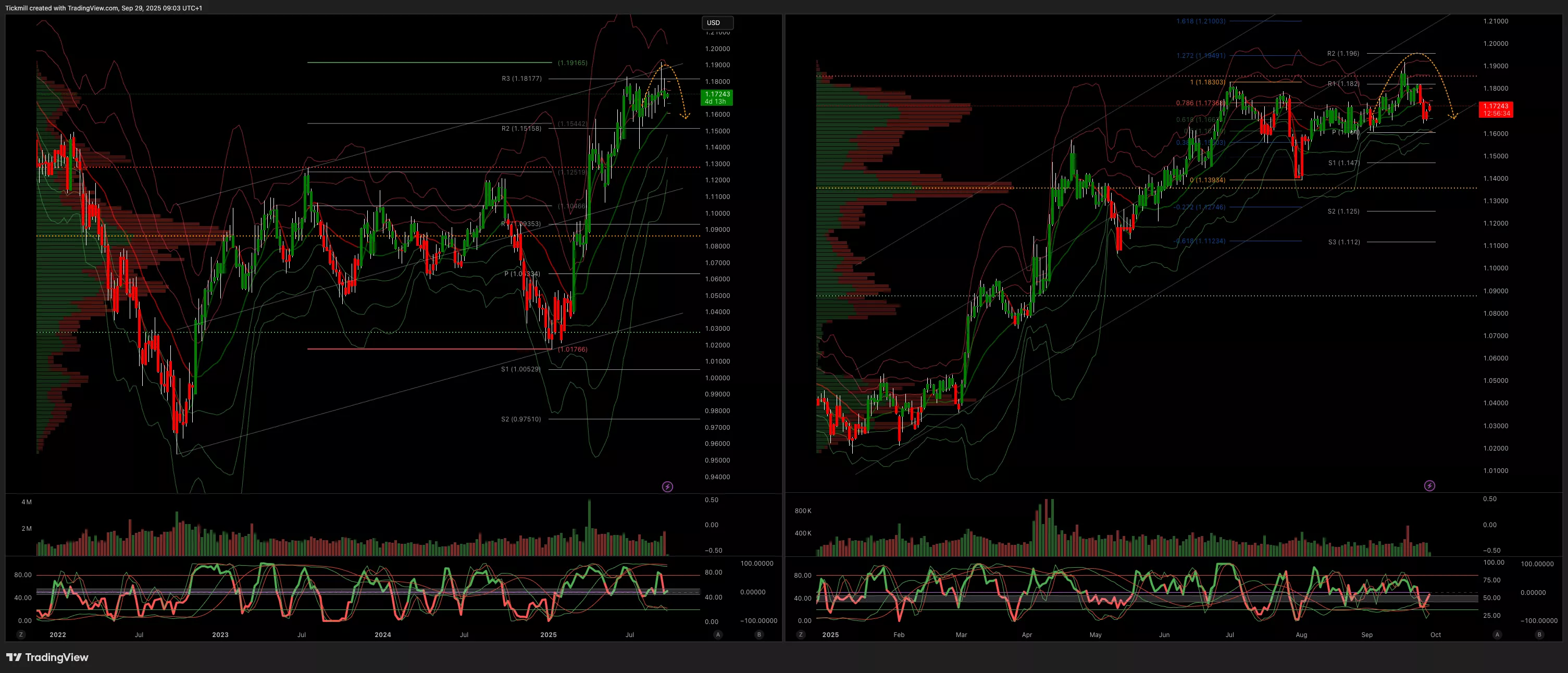

EURUSD

- Daily VWAP Bearish

- Weekly VWAP Bullish

- Below 1.1750 Target 1.15

- Above 1.18 Target 1.1910

(Click on image to enlarge)

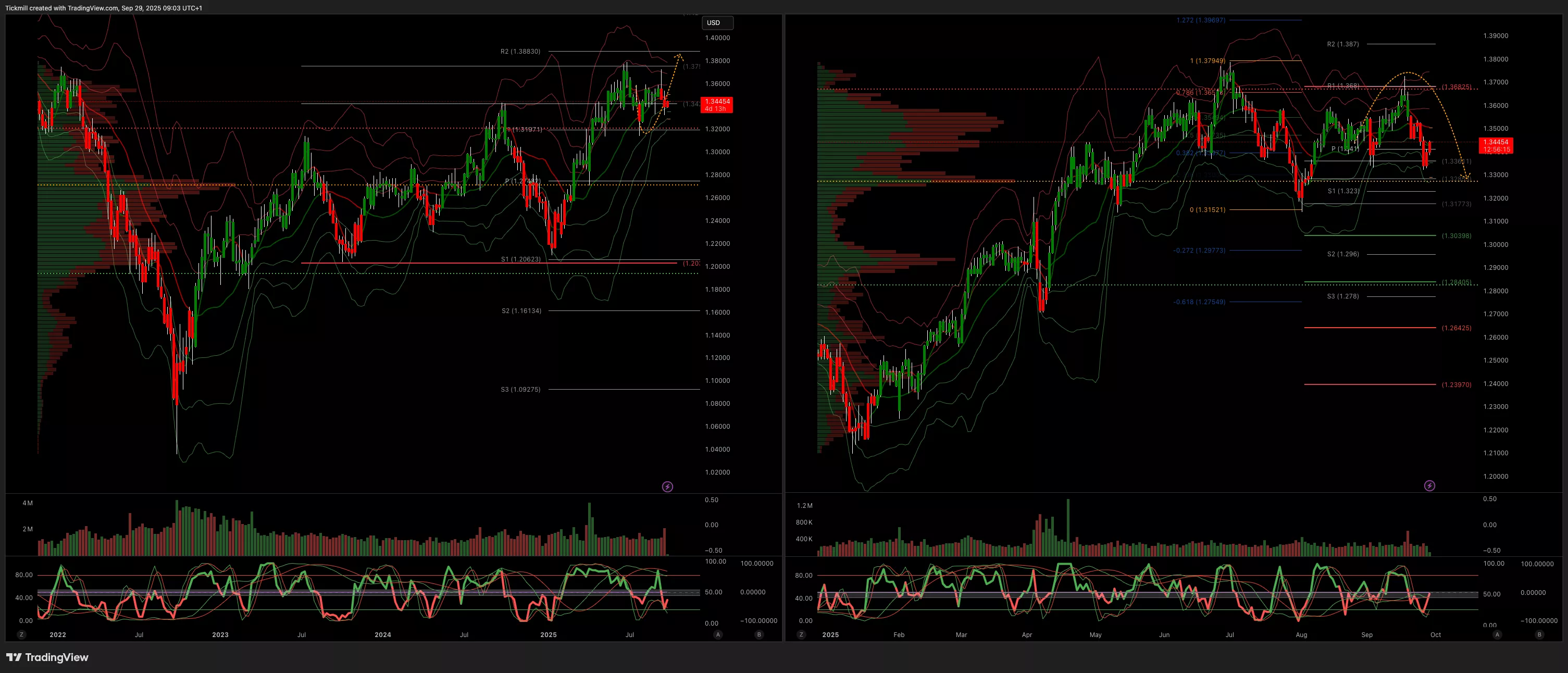

GBPUSD

- Daily VWAP Bearish

- Weekly VWAP Bearish

- Below 1.36 Target 1.30

- Above 1.3650 Target 1.3850

(Click on image to enlarge)

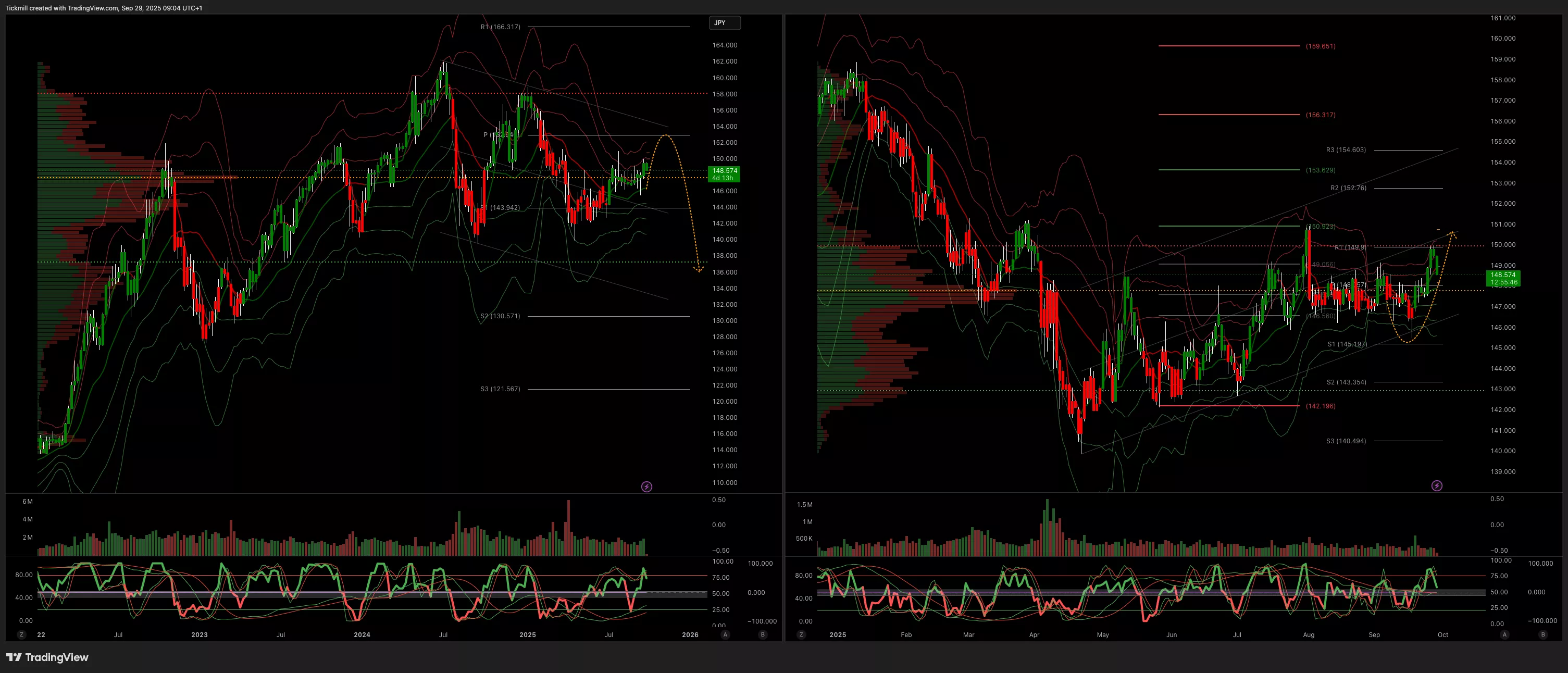

USDJPY

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Below 1.49 Target 1.45

- Above 1.51 Target 1.54

(Click on image to enlarge)

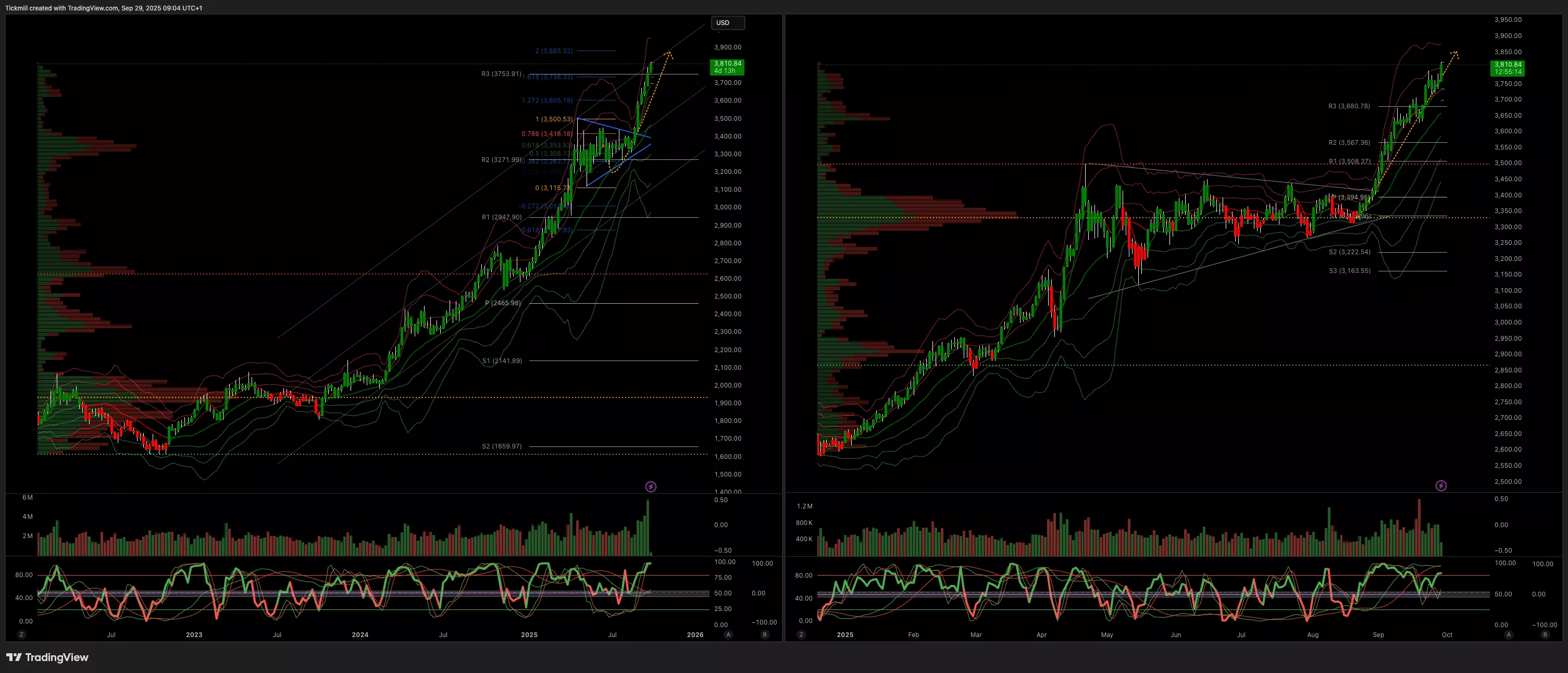

XAUUSD

- Daily VWAP Bullish

- Weekly VWAP Bullish

- Above 3600 Target 3800

- Below 3500 Target 3400

(Click on image to enlarge)

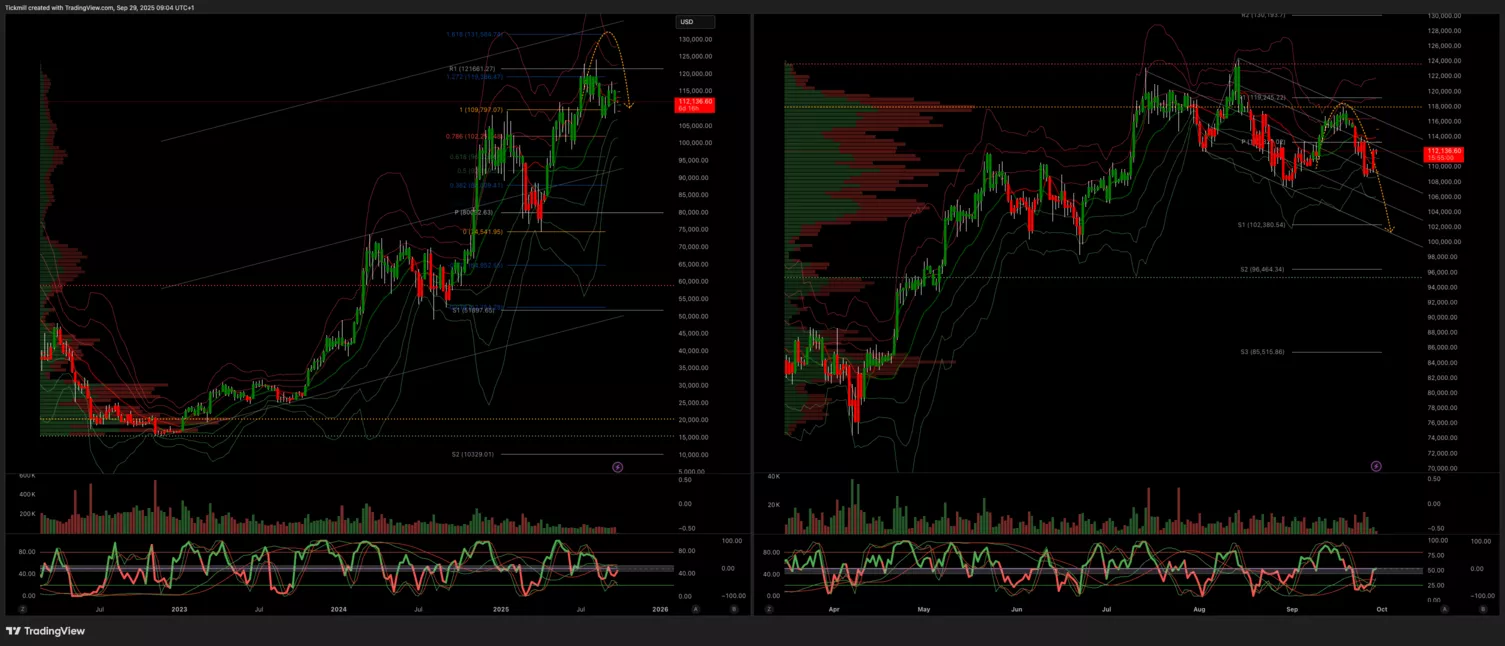

BTCUSD

- Daily VWAP Bearish

- Weekly VWAP Bullish

- Above 110k Target 118k

- Below 109k Target 105k

(Click on image to enlarge)

More By This Author:

Daily Market Outlook - Thursday, Sep. 25

Daily Market Outlook - Wednesday, Sep. 24

The FTSE Finish Line - Tuesday, Sep. 23

Comments

Log in or sign up to join the conversation.