Image Source: Pixabay

Following a subdued start due to the US President’s Day holiday on Monday, activity should ramp up. The UK has a particularly busy week ahead. It kicks off with employment and wage data on Tuesday. Although there have been concerns about sampling issues, there should be enough information to assess how the labour market is adapting to impending tax changes. BoE's Bailey will also address Bruegel early in the morning. January CPI will be reported on Wednesday. Service prices are expected to recover after a decline in airfares the previous month, though the significance may be less critical considering the rise in official forecasts for this year (due to higher energy costs, taxes, utilities, wages, etc.). The BoE might disregard this variation if the data overall indicates a growing slack. The UK data week will conclude with retail sales on Friday, which have shown improvement lately. However, weak confidence and risks in the labour market serve as a counterbalance to a general rise in real incomes. The market may be more attuned to any weaknesses. In the US, the calendar is relatively light, with the FOMC minutes being the main highlight on Wednesday, ahead of the early February surveys (including the flash PMIs – a common feature) on Friday. The Eurozone is also calm, with the only notable event being Tuesday’s ZEW alongside the updated surveys. In terms of central bank actions, the RBA is anticipated to implement its first rate cut of the cycle on Tuesday (25bps), followed by a likely 50bps reduction from the RBNZ on Wednesday.

Geopolitics remain prominent with news that discussions regarding the Russian-Ukraine situation are set to commence in Saudi Arabia this week, although the identities of the participants remain somewhat uncertain. The immediate threat of reciprocal tariffs from the U.S. has diminished until April, yet the potential for these tariffs to encompass levies based on value-added taxes in other nations continues to be a significant concern. The possibility, regardless of how misguided, of the U.S. imposing an extra 20% tariff on all imports from the EU, in addition to whatever other measures it chooses, and to varying extents on all other countries with VAT systems, is an extremely alarming scenario regarding its consequences for global economic growth.

Retail sales in the US for January tend to be unpredictable, as seasonal adjustments often fail to accurately reflect the significant nominal decline (around 20% month-on-month). The report released on Friday appeared notably weak against expectations. Advanced sales showed a decline of -0.9% month-on-month compared to a median estimate of -0.2%, while the more precise control group recorded an even larger miss at -0.8% month-on-month against a forecast of +0.3%. This was offset by modest upward revisions for December. However, the weakness was primarily evident in auto sales and non-store purchases (i.e., online spending). Annual comparisons remained stable within recent ranges. Still, following last week's inflation data, the headline numbers align with a more subdued demand narrative, likely reigniting hopes for US rate cuts this year and prompting some additional corrective selling of the USD (while the mid-term bullish perspective remains intact), influenced by slightly tighter short-term interest rate differentials.

French President Emmanuel Macron will convene an emergency European meeting on Monday in response to claims from U.S. authorities suggesting Europe will not engage in resolving the conflict. Moving forward, it is expected that the peace process will be handled exclusively between the United States and Russia. Additionally, a meeting of Eurozone finance ministers in Brussels on Monday is likely to influence market dynamics. Patrick Harker, President of the Federal Reserve Bank of Philadelphia, and Michelle Bowman, Governor of the Federal Reserve Board, are scheduled to deliver speeches.

Overnight Newswire Updates of Note

- ECB Watchers Are Now Forecasting Even Lower Rates For 2026

- Germany’s Key Politicians Vs Far-Right Candidate In Heated Debate

- Quarter Of UK Employers Plan To Cut Jobs Before Tax Rises Bite

- UK Chancellor Faces Bigger Budget Threat On OBR Bullish Forecasts

- Rightmove: UK Housing Feels The Drag From Tax Change

- UK Steps Up EU Talks Over Postwar Ukraine Peacekeeping Offer

- Trump: Putin ‘Wants To Stop Fighting’ In Ukraine

- XAU Buyers Regain Poise As Focus Shifts To US-Russia Meeting

- Pressure On BP To Merge With Shell, Creating National Oil Giant

- Bain Concedes To KKR In $4B Fight For Japan’s Fuji Soft

- Chinese President Xi Jinping Meets Key Chinese Business Leaders

- Japan’s Economy Expands Third Consecutive Quarter

- Yen Off Lows But Heavy Near 151.50 Amid Upbeat Japan's Q4 GDP

- Australia Set For First Rate Cut Since 2020 As Trade Risks Mount

- NZ PSI Edges Into Expansion After 10-Month Contraction

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0400 (400M), 1.0500 (4.7BLN), 1.0525-30 (1BLN)

- GBP/USD: 1.2450 (503M), 1.2625 (209M), 1.2650 (313M)

- AUD/USD: 0.6300 (494M)

- USD/CAD: 1.4220-30 (315M), 1.4285 (560M)

- USD/JPY: 151.50 (470M), 152.00-05 (1.3BLN), 152.20-25 (1BLN)

CFTC Data As Of 14/2/25

- The Euro holds a net short position of 64,425 contracts, while the Japanese Yen shows a net long position of 54,615 contracts. Bitcoin maintains a net short position of 367 contracts, and the Swiss Franc reports a net short position of 38,745 contracts. The British Pound registers a net short position of 3,168 contracts.

- Equity fund managers have increased their net long position in S&P 500 CME futures by 9,526 contracts, bringing the total to 929,941 contracts. Conversely, equity fund speculators have expanded their S&P 500 CME net short position by 33,021 contracts, reaching a total of 366,233 contracts.

- Speculators shifted to a net long position in CBOT US Treasury bond futures, climbing to 44,001 contracts for the week ending February 11, compared to the previous 4,927 contracts. Additionally, they reduced the net short position in CBOT US ultrabond Treasury futures by 3,675 contracts, now standing at 239,941 contracts. However, speculators increased the net short position in CBOT US 2-year Treasury futures by 79,988 contracts, totaling 1,298,612 contracts, and raised the net short position in CBOT US 10-year Treasury futures by 43,331 contracts, now at 751,034 contracts. Meanwhile, the net short position in CBOT US 5-year Treasury futures was trimmed by 65,931 contracts, bringing the total to 1,861,735 contracts.

Technical & Trade Views

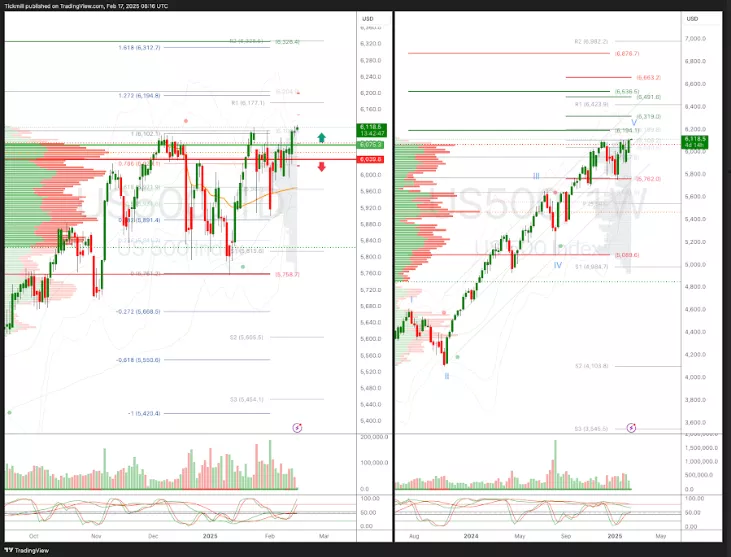

SP500 Pivot 6040

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness Into March 7th

- Long above 6075 target 6195

- Short Below 6045 target 5743

(Click on image to enlarge)

EURUSD Pivot 1.0435

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into March 30th

- Above 1.0505 target 1.0634

- Below 1.0435 target 0.9758

(Click on image to enlarge)

GBPUSD Pivot 1.2614

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into March 10th

- Above 1.2685 target 1.2812

- Below 1.2615 target 1.1878

(Click on image to enlarge)

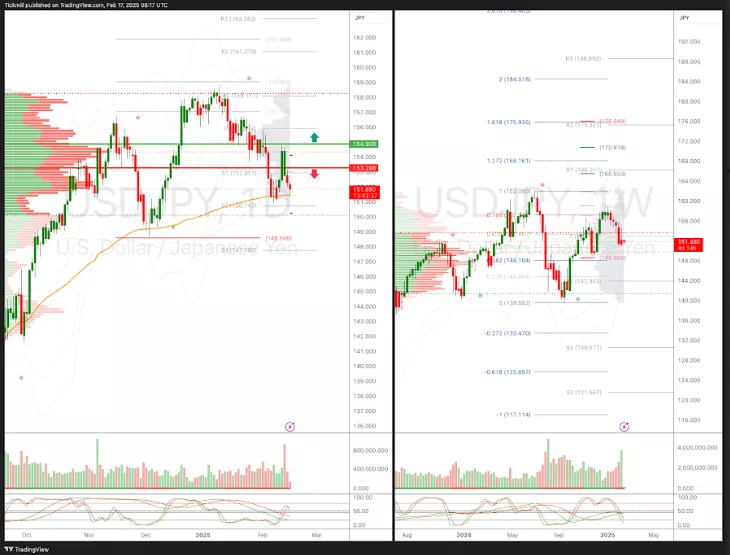

USDJPY Pivot 153.77

- Daily VWAP bullish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 1.5377 target 165.50

- Below 152.41 target 150

(Click on image to enlarge)

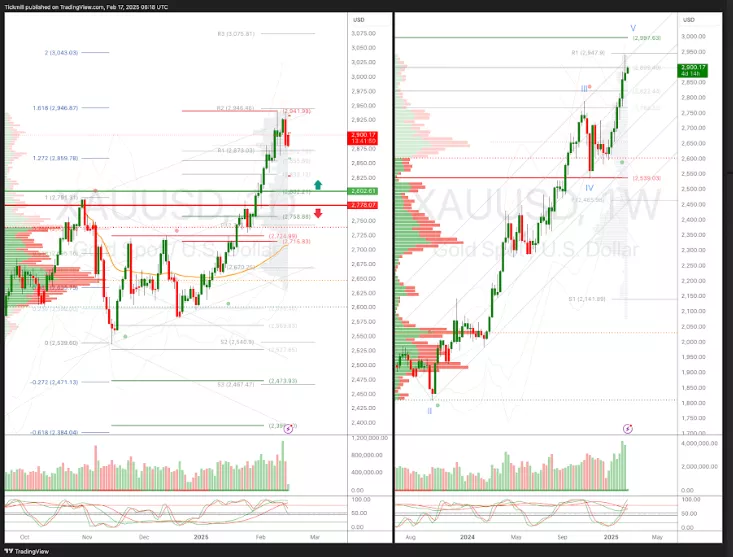

XAUUSD Pivot 2692

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests volatile bullishness into Feb 22nd

- Above 2725 target 2997

- Below 2692 target 2475

(Click on image to enlarge)

BTCUSD Pivot 101,960

- Daily VWAP bearish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 104,020 target 110,000

- Below 101,942 target 86,266

(Click on image to enlarge)

More By This Author:

Daily Market Outlook - Friday, Feb. 14

FTSE In The Red As Heavyweight Profit Taking Weighs

Daily Market Outlook - Thursday, Feb. 13

Comments

Log in or sign up to join the conversation.