Image Source: Unsplash

Asian tech shares fell on Friday, following Wall Street's decline due to slowing US inflation. The yen was volatile. Asian technology stocks dropped by up to 3.2%, with Japan and South Korea seeing the biggest losses. The Nasdaq 100 fell 2.2% as inflation data suggested a potential rate cut, leading to an exodus from tech megacaps.. Chinese shares in Hong Kong rose on hopes of policy support from the mainland's approaching Third Plenum, with Chinese property developers seeing a rise of over 6%. Despite the setback, global equities are on track for their sixth weekly gain, driven by Fed easing expectations. Treasury yields rose after the possibility of lower US interest rates drove 10-year yields down by seven basis points. Government bonds in Australia and New Zealand rose in response. The dollar index remained stable after a significant drop on Thursday.

The yen fluctuated as the Bank of Japan conducted rate checks, leading to speculation of market intervention, as usual, officials were not forthcoming with information, but Tokyo has clearly demonstrated its ability to intervene in the market at the right time. The sudden increase in the yen on Thursday followed data showing a lower-than-expected cooling of U.S. consumer inflation in June, leading analysts and traders to initially attribute the surge to options-related activity. However, the scale and speed of the movement eventually alerted the markets to the possibility of a Japanese intervention, which was similarly reported by local media. Given that recent interventions have had short-lived effects, Thursday's move likely provided the most impact for Tokyo. The absence of authorities from the currency market after the April-May intervention had raised questions about their restraint as the yen continued to reach new lows, but Thursday's developments have once again put traders on edge. It is also timely that Japan has a national holiday on Monday, which could result in low liquidity and potentially provide another opportune moment for Tokyo to take action. The focus on the yen briefly diverted attention from the main story, which remains on rates, with a September rate cut from the Federal Reserve almost fully expected. Even Fed Chair Jerome Powell, in his recent testimony before Congress, seemed to hint at the possibility of an easing cycle beginning in September, stating that the U.S. economy was no longer overheated. Stateside, President Joe Biden faced some challenges as he mistakenly mixed up the names of Vice President Kamala Harris and his Republican rival Donald Trump, just hours after referring to Ukrainian President Volodymyr Zelenskiy as Russian President Vladimir Putin before correcting himself at the NATO summit in Washington.

Overnight Newswire Updates of Note

- June Price Drop May Shorten The Fed's Last Mile On Inflation

- Biden: Israel, Hamas Have Agreed To My Ceasefire Deal Framework, But Gaps Remain

- UK's Starmer Urges NATO Allies To Boost Defence Spending

- Japan Top FX Diplomat Says Authorities To Take Action As Needed On Yen

- China Trade Balance (M/M) Jun: $+99.05 Bln

- Japan’s Industrial Production (M/M) May: 3.6% (prev 2.8%)

- New Zealand’s Business Manufacturing PMI (M/M) Jun: 41.1 (prevR 46.6)

- Singapore Q2 GDP (Y/Y): 2.9% (est 2.7%; prev 2.7)

- Ericsson Beats Estimates On Cost Cutting In Tough Market

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.0800 (1.7BLN), 1.0820-30 (1.5BLN), 1.0850 (2.4BLN)

- 1.0870-80 (1.1BLN), 1.0890-1.0900 (1.3BLN)

- USD/CHF: 0.8900 (636M), 0.8970-80 (481M), 0.9000 (587M)

- EUR/CHF: 0.9625-35 (1.8BLM). EUR/GBP: 0.8375 (300M)

- GBP/USD: 1.2850 (831M), 1.2905-10 (352M), 1.2925 (215M)

- AUD/USD: 0.6715 (493M), 0.6750-55 (525M), 0.6770 (590M)

- 0.6790-0.6800 (1.4BLN)

- AUD/NZD: 1.1060 (1.2BLN), 1.1100 (503M)

- USD/CAD: 1.3630 (1.1BLN), 1.3645-55 (1.6BLN)

- USD/JPY: 158.80 (501M), 159.00-05 (886M), 159.30 (441M), 160.00 (1.2BLN)

- AUD/JPY: 106.25 (500M), 107.50 (400M)

CFTC Data As Of 5/7/24

- JPY: -184,223 contracts

- EUR: -9,519 contracts

- GBP: 62,041 contracts

- CHF: -43,443 contracts

- Bitcoin: -912 contracts

- Equity fund managers cut S&P 500 CME net long position by 24,005 contracts to 953,130

- Equity fund speculators trim S&P 500 CME net short position by 5,025 contracts to 293,675

Technical & Trade Views

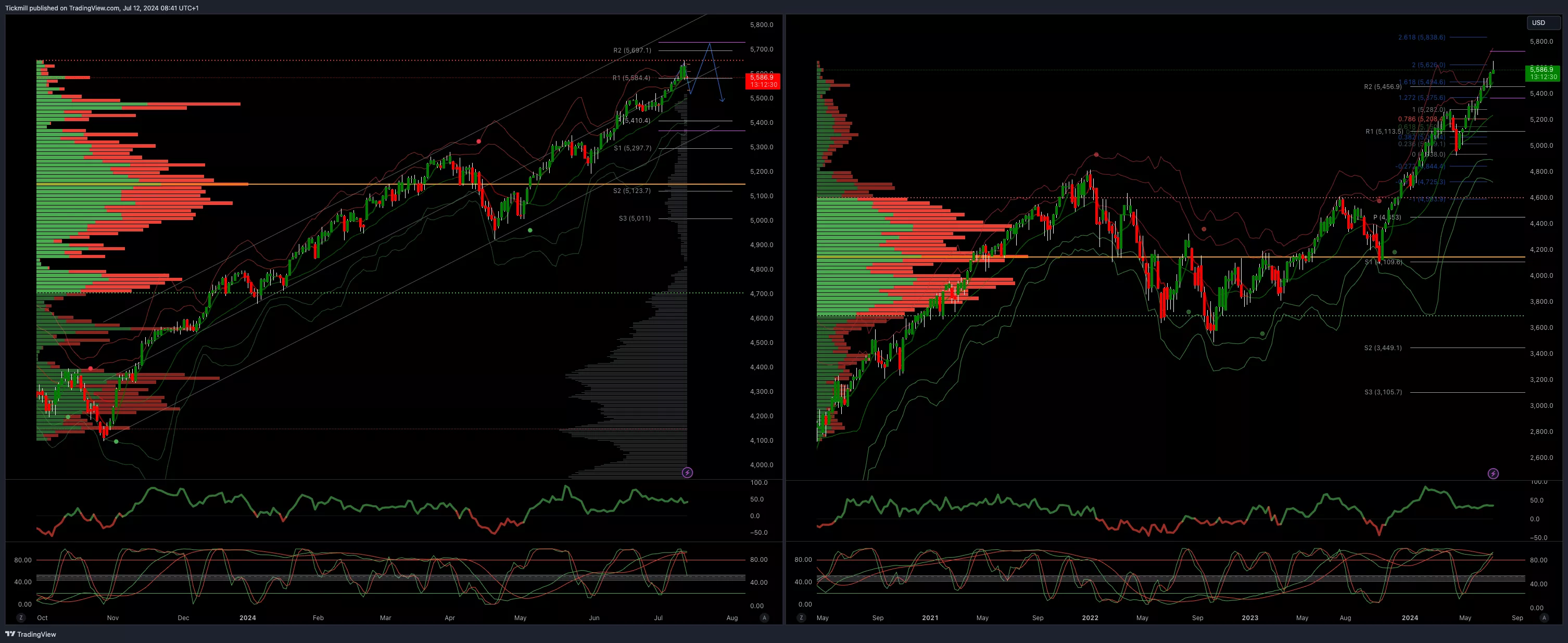

SP500 Bullish Above Bearish Below 5550

- Daily VWAP bullish

- Weekly VWAP bullish

- Below 5475 opens 5450

- Primary support 5400

- Primary objective is 5700

(Click on image to enlarge)

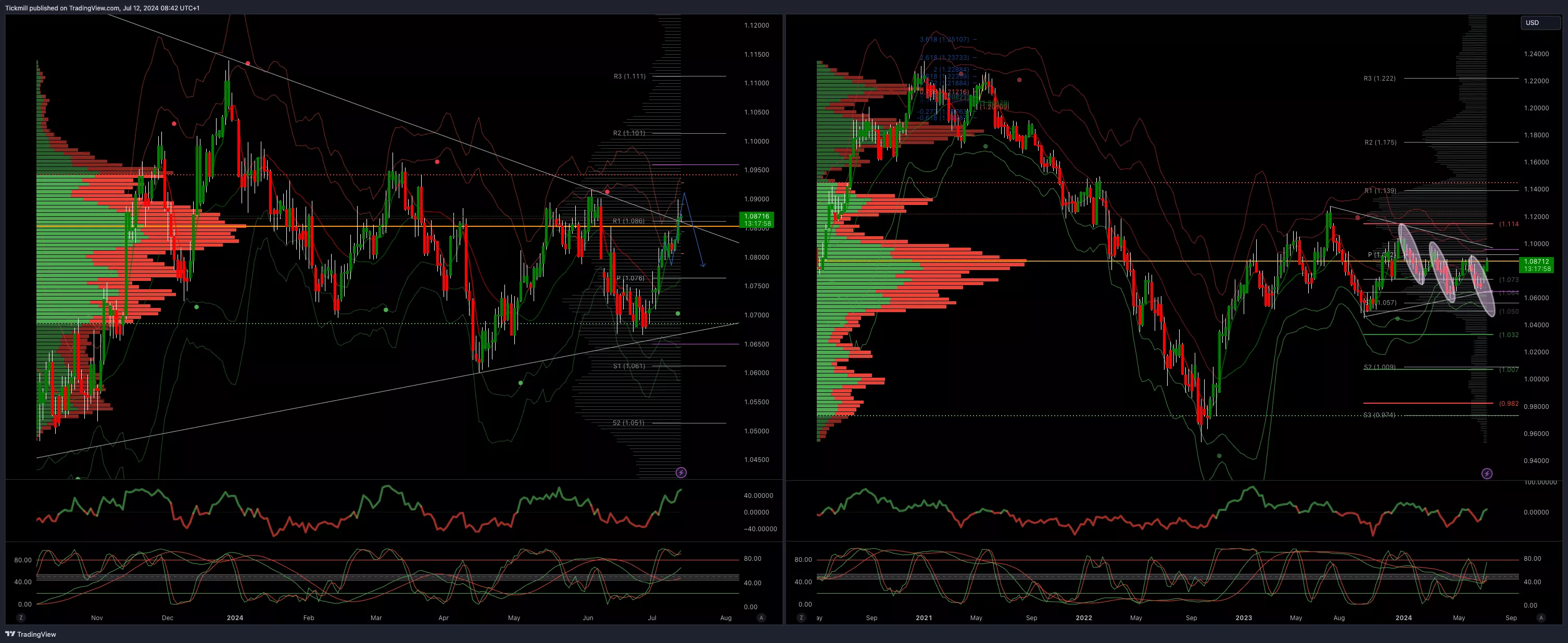

EURUSD Bullish Above Bearish Below 1.0750

- Daily VWAP bullish

- Weekly VWAP bearish

- Above 1.880 opens 1.0940

- Primary resistance 1.0981

- Primary objective is 1.0650

(Click on image to enlarge)

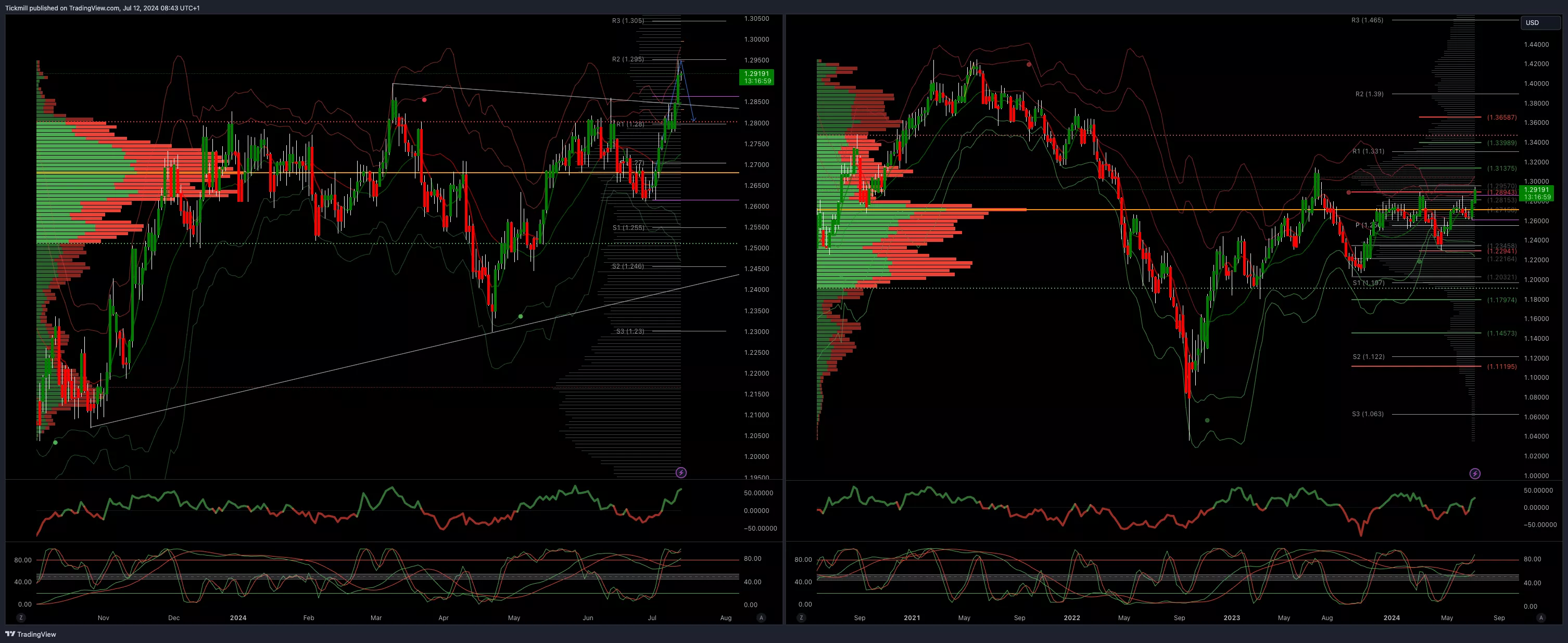

GBPUSD Bullish Above Bearish Below 1.27

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 1.29 opens 1.3130

- Primary resistance is 1.2890

- Primary objective 1.2570

(Click on image to enlarge)

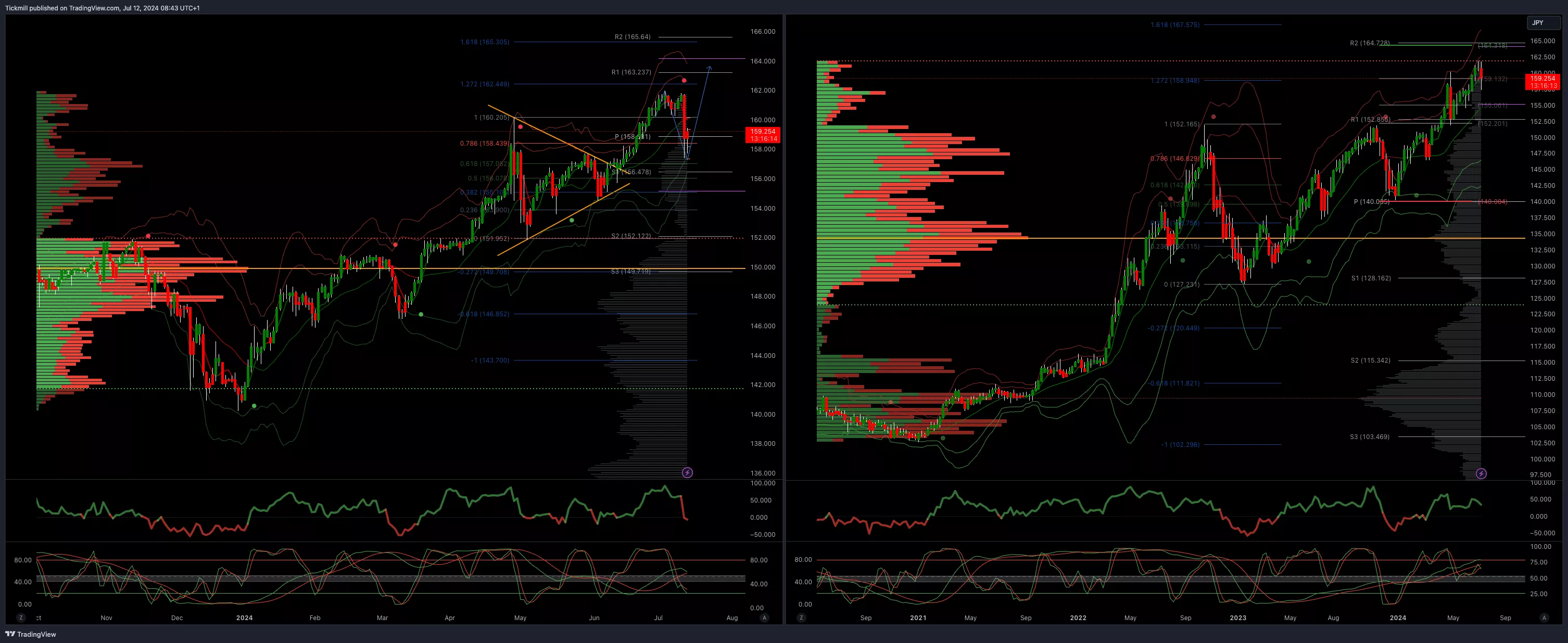

USDJPY Bullish Above Bearish Below 160

- Daily VWAP bearish

- Weekly VWAP bullish

- Below 157.60 opens 157.10

- Primary support 152

- Primary objective is 164

(Click on image to enlarge)

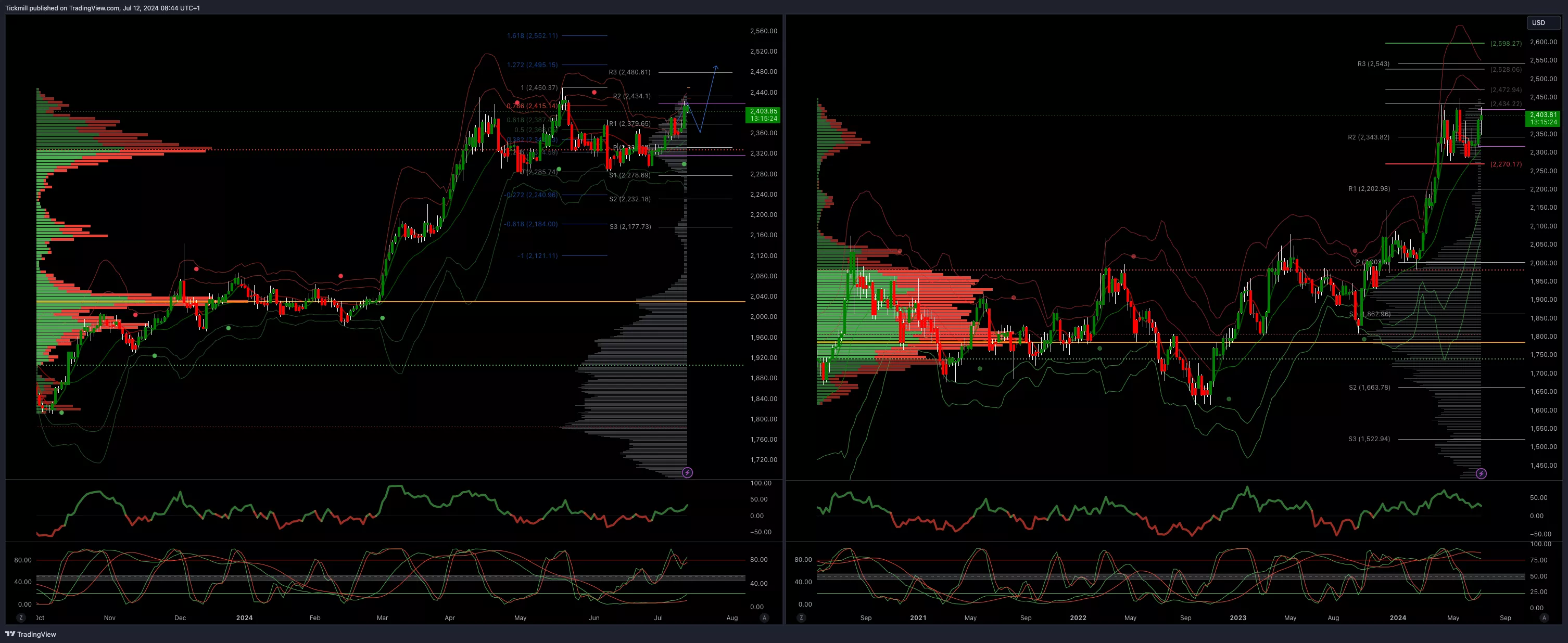

XAUUSD Bullish Above Bearish Below 2345

- Daily VWAP bullish

- Weekly VWAP bullish

- Above 2415 opens 2495

- Primary resistance 2387

- Primary objective is 2262

(Click on image to enlarge)

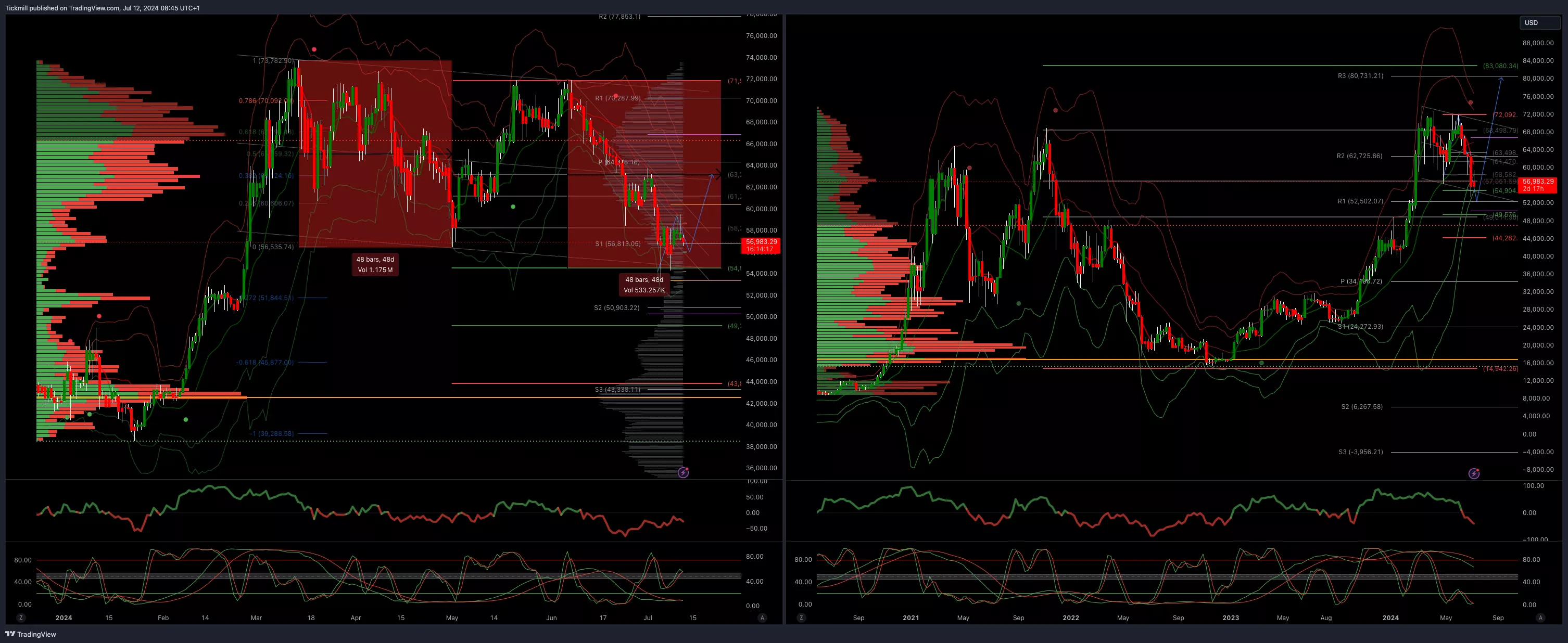

BTCUSD Bullish Above Bearish below 60000

- Daily VWAP bearish

- Weekly VWAP bearish

- Above 67000 opens 70000

- Primary support is 50000

Primary objective is 54500 - TARGET ACHIEVED NEW PATTERN EMERGING

(Click on image to enlarge)

More By This Author:

FTSE Flatlining As Markets Mull Continued US Inflation Pullback

Daily Market Outlook - Thursday, July 11

FTSE Rebounds After Tuesday Marked Worst Day In Month

Comments

Log in or sign up to join the conversation.