Daily Market Outlook - Friday, April 4

Image Source: Pixabay

Asia has experienced another painful day following significant losses on Wall Street; the combined market value of S&P 500 companies plummeted by $2.4 trillion, marking their largest single-day decline since the onset of the coronavirus pandemic on March 16, 2020. Other Wall Street indexes also experienced significant drops. This severe market selloff followed Trump’s announcement on Wednesday of the most stringent trade barriers in over a century, prompting investors to seek safer assets. Taking their cue from US markets, Japanese markets tanked, with the Nikkei falling 2.75%, marking a staggering weekly decline of 9.6%, the largest drop since March 2020. Amid growing concerns about a global recession, especially in the U.S., traders have increased their expectations for more Federal Reserve rate cuts this year, believing that policymakers will need to act more decisively to support growth in the world's largest economy. Fed funds futures now indicate approximately 96 basis points of cuts by December, up from around 70 basis points just before Trump's tariffs were announced on Wednesday.

Ahead of today’s Non-Farm Payrolls release, it is noteworthy that US job cuts reported by Challenger rose sharply in March, reaching 275,000 for the month, surpassing the highs seen during both the dot-com bubble and the Global Financial Crisis. The notable aspect is not just the volume but also the composition of these layoffs. While other job statistics haven't indicated a rise in layoffs due to DOGE cuts, the Challenger reports show a clear trend, with government positions making up 79% of the jobs lost last month, a significant increase from the already high 36% in February. Such a rapid rate may be hard to maintain considering the overall scale of government employment, but the resulting effects on the broader economy could lead to private sector job cuts filling that void in the near future. Liberation Day might invoke some feelings of nostalgia for those in traditional manufacturing, yet for decision-makers throughout the economy, these pressures only add to the uncertainties generated by rising trade barriers. This presents significant downside risks for both economic growth and the value of the US dollar. Economists estimate that the U.S. economy added 135,000 jobs in March, down from 151,000 in February, ahead of the official report's release later today. Shortly after, Federal Reserve Chair Jerome Powell is scheduled to deliver a speech on the economic outlook.

The disruptive impact of U.S. government policies on trade and the size of the global impact may reshape perspectives on the economic data calendar. Next week, attention will focus on March U.S. CPI inflation data (Thursday), which is expected to show a favorable base effect, potentially lowering the headline rate by 0.2 percentage points to 2.6% year-on-year. However, given heightened market expectations, this may not carry significant weight (see chart). Another key U.S. release is the Fed minutes (Wednesday), where insights into the near-pausing of quantitative tightening (QT) will be closely scrutinised. Interestingly, typically less prominent releases like the monthly budget balance (Thursday) could garner attention if evidence of a "DOGE effect" surfaces. Beyond these, surveys both domestically and internationally may dominate headlines if tariff impacts become evident, as was recently observed with the ISM data. In the U.S., the NFIB small business survey (Tuesday) will be of interest, while globally, the Bank of Canada outlook survey (Monday), Australian consumer confidence data (Tuesday), and inflation expectations (Thursday) will also demand attention amidst various countries' trade data releases. In the U.K., the week appears relatively quiet ahead of February GDP data (Friday), though speeches from MPC members Lombardelli (Tuesday) and Breeden (Thursday) may provide some insights. Meanwhile, China's inflation—or potentially deflation—data for March (Thursday) could play a pivotal role in shaping market sentiment.

Overnight Newswire Updates of Note

- Europe Must Shift Defence Burden Away From US, Says Finland

- US Payrolls Report Expected To Be Eclipsed By Tariffs

- Treasuries Below 4% Again As Payrolls, Powell Speech Loom Large

- JPMorgan Sees Global Recession Odds At 60% If Tariffs Sustained

- Inflation Fears Add To Pressure On Federal Reserve

- UBS Wealth Downgrades US Stocks, Slashes Target On Tariff Blow

- VP Vance Downplays ‘One Bad Day’ For Markets, Promising Boom Later

- Republicans Weigh Using Power Of Congress To Rein In Trump On Tariffs

- Dollar May Trade With Moderate Upward Bias Vs Asian Currencies On Tariffs

- Oil Edges Lower, Weighed By US Tariffs, OPEC+ Supply Increase

- China’s Response To Tariffs Likely More Stimulus, Building Trade Ties

- BoJ’s Ueda Cites Heightened Uncertainty After Trump’s Tariffs

- Japan’s Stock Rout Deepens, Bonds Rally, Rate-hike Bets Fade

- Japan’s Household Spending Drops For First Time In Three Months

- Australia’s Household Spending Misses Estimates In February

- Samsung Stung By US Chip Restrictions, Seven & I Seeks Footing

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

- EUR/USD: 1.1000 (1.1BLN), 1.1030-35 (1BLN), 1.1050-55 (2BLN)

- 1.1100 (250M), 1.1120 (601M), 1.1150 (251M)

- EUR/CHF: 0.9575 (420M)

- GBP/USD: 1.3050 (344M)

- AUD/USD: 0.6180 (951M), 0.6200 (1.6BLN), 0.6240 (515M), 0.6300 (1.4BLN)

- 0.6350 (2.3BLN), 0.6400 (550M)

- USD/CAD: 1.4050-60 (1.2BLN), 1.4075 (340M), 1.4100 (620M)

- 1.4135 (355M), 1.4150 (584M)

- USD/JPY: 145.00 (270M), 145.75 (300M), 147.00 (1.4BLN)

CFTC Data As Of 28/3/25

- Equity fund managers have increased their S&P 500 CME net long position by 83,572 contracts, bringing the total to 915,841. Meanwhile, equity fund speculators have raised their S&P 500 CME net short position by 41,376 contracts, now totalling 236,867. Speculators have also expanded their CBOT

- US Treasury bonds futures net short position by 24,765 contracts to reach 38,275. Additionally, they have reduced their CBOT US Ultrabond Treasury futures net short position by 14,792 contracts, now at 232,366. The CBOT US 10-year Treasury futures net short position has been trimmed by 71,284 contracts, bringing it to 810,090. Speculators have reduced their CBOT US 5-year Treasury futures net short position by 5,853 contracts to total 1,900,087, and the CBOT US 2-year Treasury futures net short position has been cut by 38,970 contracts, now standing at 1,181,586.

- The Japanese yen holds a net long position of 125,376 contracts, while the Swiss franc reports a net short position of -37,593. The British pound has a net long position of 44,283 contracts, and Bitcoin holds a net long position of 1,179 contracts.

Technical & Trade Views

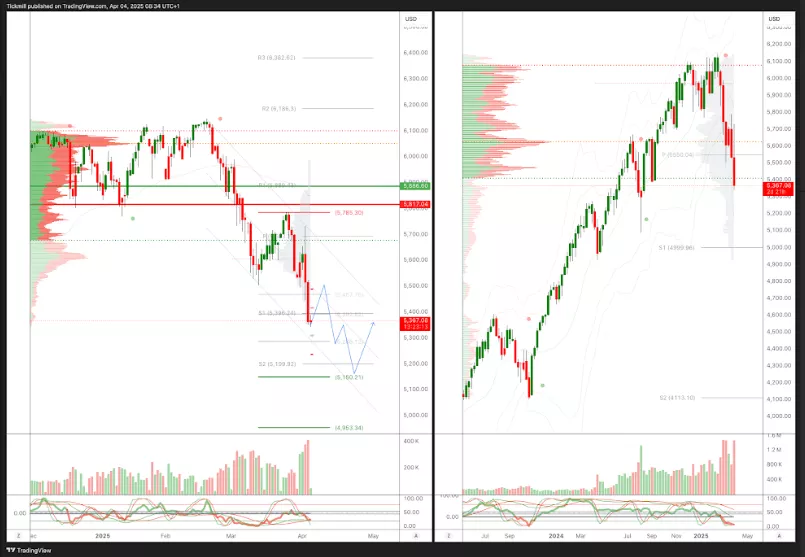

SP500 Pivot 5790

- Daily VWAP bearish

- Weekly VWAP bearish

- Seasonality suggests bullishness into late April

- Above 5885 target 5950

- Below 5815 target 5415

(Click on image to enlarge)

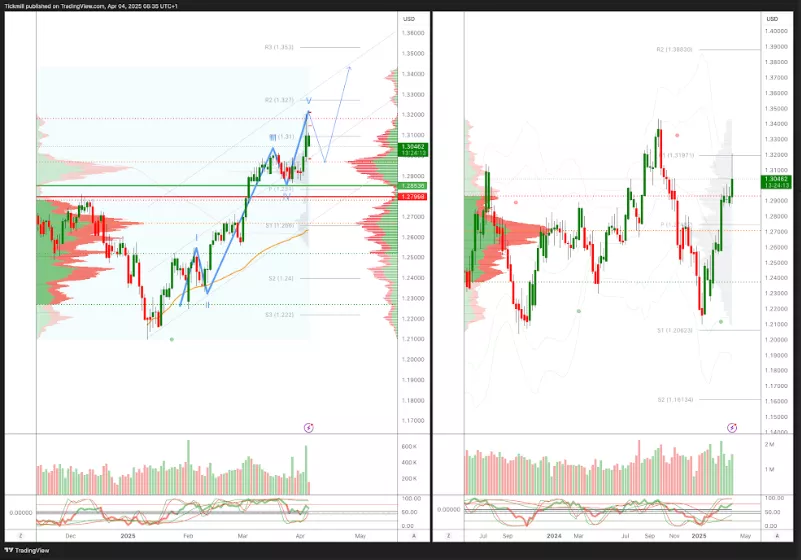

EURUSD Pivot 1.0750

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into the end of April

- Above 1.0750 target 1.11

- Below 1.0690 target 1.0550

(Click on image to enlarge)

GBPUSD Pivot 1.28

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bullishness into late April

- Above 1.2850 target 1.32

- Below 1.2790 target 1.2660

(Click on image to enlarge)

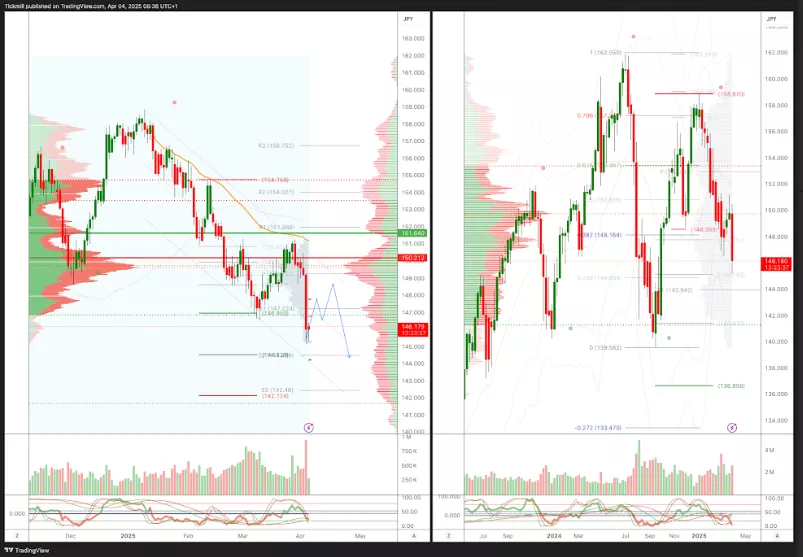

USDJPY Pivot 150.50

- Daily VWAP bearish

- Weekly VWAP bullish

- Seasonality suggests bullishness into Apr 9th

- Above 1.52 target 153.80

- Below 150.50 target 145

(Click on image to enlarge)

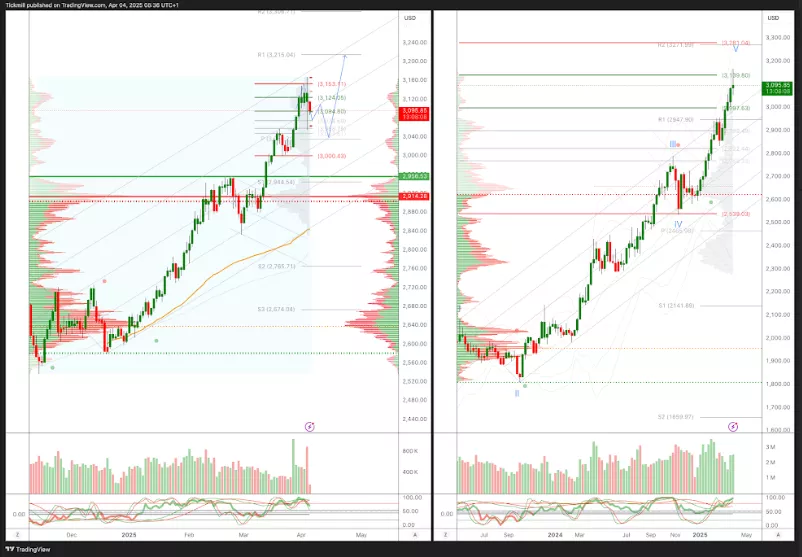

XAUUSD Pivot 2950

- Daily VWAP bullish

- Weekly VWAP bullish

- Seasonality suggests bearishness into mid/late April

- Above 2900 target 3100

- Below 2880 target 2835

(Click on image to enlarge)

BTCUSD Pivot 90k

- Daily VWAP bearish

- Weekly VWAP bearish

- Seasonality suggests bullishness into Apr 9th

- Above 97k target 105k

- Below 95k target 65k

(Click on image to enlarge)

More By This Author:

The FTSE Finish Line - Thursday, April 3

Daily Market Outlook - Thursday, April 3

The FTSE Finish Line - Wednesday, April 2