Two High Yielding Dividend Giants To Look At Today

Guest post by Dylan Callaghan

When looking to add different stocks to your portfolio, we certainly don't advocate looking for yield first. The strength of an investment doesn't lie in the dividend yield but rather in the underlying company itself.

However, now and then, you'll find some Canadian stocks offering solid underlying fundamentals and high dividend yields. In this article, we're going to go over two of them.

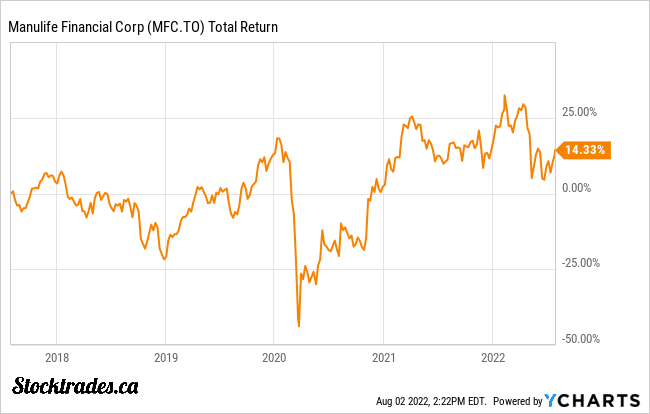

Manulife Financial (TSE:MFC, NYSE: MFC)

Manulife (MFC) provides life insurance and wealth management products and services to individuals and group customers in Canada, the United States, and Asia. Manulife is one of Canada’s "Big Three" life insurance companies (the other two are Sun Life and Great West Life). As of Dec. 31, 2021, Manulife reported assets under management or administration totaling roughly CAD 1.4 trillion.

The company has traded at discounted valuations compared to its peers since the financial crisis for one main reason: the company cut the dividend during the recession in 2008. Investors likely fear that Manulife will do the same if we head into a recession in 2022 or 2023.

The reality is that the company is in a much better financial position than it was in 2008, carrying a debt to equity ratio of only 0.28 and an interest coverage ratio of nearly 12. Even if times were to get tough, we not only don't foresee a dividend cut in the company's future, but we feel the company could drive further dividend growth.

Why? The company's dividend currently makes up only 12% of free cash flow and 30% of earnings. This buffer in the dividend payout ratio should let Manulife maintain and potentially even grow the dividend during turbulent times.

Although interest rates rising over the long term benefit Manulife, short-term rockiness in the bond market can cause earnings to be relatively volatile. But with this company trading at a near 50% discount to historical averages and less than 7 times expected earnings, it seems like the market is pricing-in worst-case scenarios at this point.

As a result, the company is now yielding 5.65% at the time of writing, meaning you'll collect $565 annually in dividends for every $10,000 you invest in Manulife.

This company may not be as fast-growing as a P&C insurer like Intact Financial (TSE:IFC). However, Manulife provides strong cash flow generation and steady income for Canadians. And as of right now, it looks to be attractively valued.

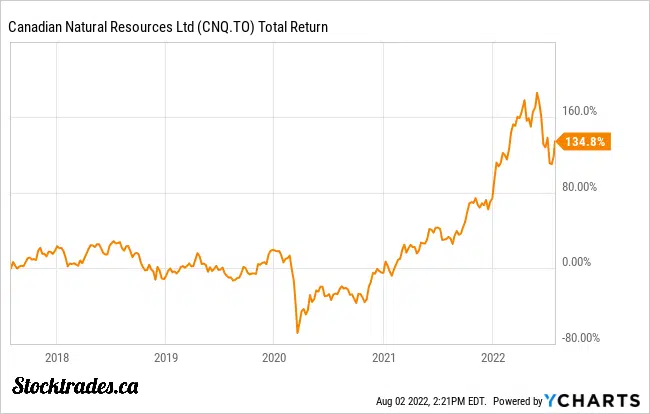

Canadian Natural Resources (TSE:CNQ)(NYSE:CNQ)

In our opinion, Canadian Natural Resources (CNQ) is the best oil producer in North America.

Canadian Natural Resources is one of western Canada's largest oil and natural gas producers, supplemented by operations in the North Sea and Offshore Africa. The company’s portfolio includes light and medium oil, heavy oil, bitumen, synthetic oil, natural gas liquids, and natural gas. Production averaged 1.16 million barrels of oil equivalent per day in 2020, and the company estimates that it holds over 11.5 billion boe of proven and probable crude oil and natural gas reserves.

Despite many junior, and even major producers like Suncor, cutting the dividend in 2020, Canadian Natural not only maintained its dividend during low oil prices, it raised the dividend, extending its dividend growth streak to more than 2 and a half decades.

The company can do this because of its rock-bottom break-even price on its oil barrels. The company can be profitable at $35~ WTI. So, the company often generates enough cash flow during high oil prices to maintain operations and the dividend during oil gluts.

A multi-year oil bull market maintaining $70+ WTI prices could see significant cash flow generation by Canadian Natural. As a result, it's trading at some attractive valuations.

There are fears that the oil and gas bull market is coming to an end, and as a result, investors have sold off Canadian Natural to the point where it's trading at only 8.5 times trailing cash flows and 6.5 times forward earnings. With a PEG ratio of 0.43, the market is not factoring enough forward growth into CNRL's share price.

And with this recent correction comes a high yield. Canadian Natural boasts a dividend yield of 4.24%, meaning you'll collect $424 in dividends yearly if you invest $10,000. There's a chance that investors could be even further rewarded with significant dividend increases and share buybacks in the future if oil can maintain its current levels.

More By This Author:

Top Canadian Semiconductor Stocks To Buy

Top Cryptocurrency ETFs To Buy In Canada

3 Top Canadian Large Cap Stocks To Buy In November

Disclaimer: You can read our full disclaimer here.