Oil Market Weakness Suggests Recession More Likely Than Middle East War

Oil markets remain poised between fear of recession and fear of a US attack on Iran. But gradually it seems that fears about a war are reducing, while President Trump’s decision to ramp up the trade war with China makes recession far more likely.

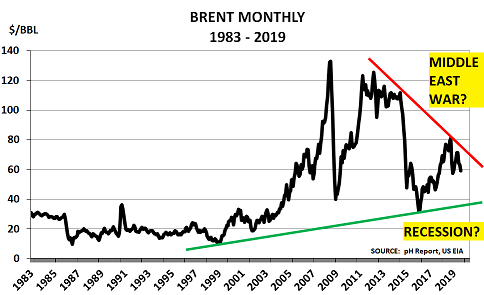

The chart of Brent prices captures the current uncertainties:

- It shows monthly prices for Brent since 1983 and highlights the conflicting risks

- The bulls have been battling to push prices higher, but their confidence is weakening

- The bears were hurt by the stimulus from US tax cuts and OPEC output cuts

- But June’s abandonment of the Iran attack lifted their confidence

As a member of the President’s national security advisory team has noted: “

This is a president who was elected to get us out of war. He doesn’t want war with Iran.”

With fears about a potential war reducing, at least for the moment, attention has instead turned to issues of supply and demand.And here, again, the balance of different factors has turned negative:

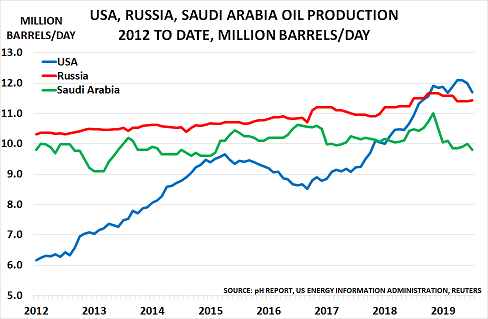

- As the second chart shows, supply from the 3 major countries remains at a high level

- The US is the largest producer, and August’s output is now recovering after the slowdown in the Gulf of Mexico due to Hurricane Barry, and the EIA is forecasting new record highs this year and 2020

- 3 new pipelines are also coming online during H2, which will boost US oil export potential

- Meanwhile Russia, as usual, has failed to follow through on its commitment to the OPEC cuts. Its output rose by 2% in January-July versus 2018, despite May/June’s contamination problems

- As always with OPEC output cuts, Saudi Arabia has been forced to fill the gap. Its volume dipped to 9.8 mbd in July, well below the 11 mbd peak last November

Overall, global supply has remained strong with EIA estimating Q2 output at 100.6 mbd versus 99.8 mbd in Q2 last year. Contrary to last year’s optimism over global economic recovery, EIA suggests Q2 consumption only rose to 100.3 mbd, versus 99.6 mbd in Q2 last year.

And the normally bullish International Energy Agency last week cut its demand forecast for this year and 2020 warning:

“The outlook is fragile with a greater likelihood of a downward revision than an upward one…Under our current assumptions, in 2020, the oil market will be well supplied.”

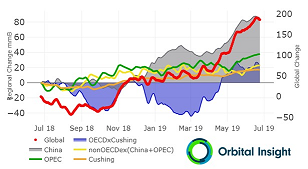

The third chart, from Orbital Insight, highlights the changes that have been taking place in inventory levels in the major regions.

Generated from satellite images of floating roof tank farms, it is based on estimates of the volume of oil in each tank, which are then aggregated to regional or country level.

Oil markets are by nature opaque. But Orbital’s data does show a very high correlation with EIA’s estimates forCushing – where the official data is very reliable.

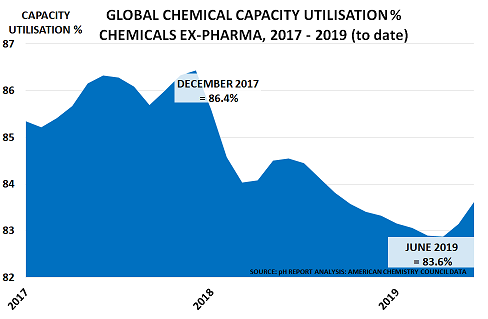

As discussed here many times before, the chemical industry is the best leading indicator for the global economy, due to its wide range of applications and geographic coverage.The fourth chart shows the steady downward trend since December 2017 in the data on Capacity Utilisation from the American Chemistry Council.

Q2 has shown the usual seasonal ‘bounce’,but key end-user markets such as electronics, autos and housing are also clearly weakening, as discussed last week for smartphones.And Bloomberg has reported that US inventory levels at major warehouses are close to being full.

I suggested back in May that prudent companies would develop a scenario approach that planned for both war and recession, given that the outcome was then essentially unknowable.

Today, both scenarios are clearly still possible. But it would seem sensible to now step up planning for recession, given the downbeat signals from oil and chemical markets.

Disclosure: I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this ...

more

Thank goodness recession is more likely than a Mideast war. That said, a recession rarely happens with such a loose Fed and with stimulus coming from the government from both lower taxation and higher spending. When it happens it will be due to inflation like Jimmy Carter under these circumstances which isn't happening anytime soon unless there is a energy issue due to a mid-east war, global trade wars actually end the cycle of overabundance, or a unforeseen disaster disrupts the markets to the point supply is radically more expensive.