Money Supply Growth: A Thesis With A Fatal Flaw

Recently, MarketWatch ran a provocative headline: “When the world’s largest asset manager and the Bond King both agree: Run to gold, silver, and bitcoin.” The article highlighted how Larry Fink’s BlackRock and Jeffrey Gundlach, often dubbed the “Bond King,” see deficits and “money printing” as reasons for investors to escape fiat currencies and pile into hard assets. As Gundlach put it:

“Deficits are out of control, the government is printing too much money, and the dollar is destined to decline.”

With a similar refrain, Larry Fink noted that “hard assets are one of the few places left to preserve wealth.”

At first glance, it sounds persuasive. After all, the U.S. is running record deficits, high debt levels, and the Federal Reserve recently cut interest rates, adding to fears of renewed money supply growth. However, a closer look at the fundamentals of modern money creation and the role of government deficits reveals that this thesis is too simplistic. Basic economics suggests a different conclusion: money supply growth is primarily a reflection of economic growth, government deficits actually contribute to private-sector savings, and gold’s price remains tethered to the dollar and real interest rates, which means a dollar rally could easily derail the “hard asset” trade.

In other words, while the thesis makes for a bold headline, it misses the underlying mechanics driving prosperity and asset prices.

Let’s dig into this topic further and start with money supply growth.

Money Supply Growth: An Economic Indicator

The first flaw in the “run to hard assets” narrative is its treatment of money supply growth. Popular commentary often assumes that rising money supply automatically debases the dollar and drives inflation, making gold and bitcoin the only safe havens. But this confuses cause and effect.

Modern economies operate under an endogenous money system, meaning banks create money in response to economic activity. As the Bank of England explained in its 2014 paper “Money creation in the modern economy,” it is not central banks that directly dictate broad money growth, but rather commercial banks extending credit when they see viable opportunities. Put simply: loans create deposits.

This is a crucially important point. The U.S. does not “print” money. All money is lent into existence.

Read that again.

This means that the growth of the money supply is closely follows the economy’s growth. When businesses expand, hire, and invest, banks extend more credit, and the money supply grows. Conversely, when the economy slows and loan demand weakens, money supply growth contracts, regardless of how much the Federal Reserve expands its balance sheet. We saw this after 2008: despite unprecedented quantitative easing, money growth and inflation remained subdued because banks hoarded reserves instead of lending. As discussed in “Debasement, What It Is And Isn’t:”

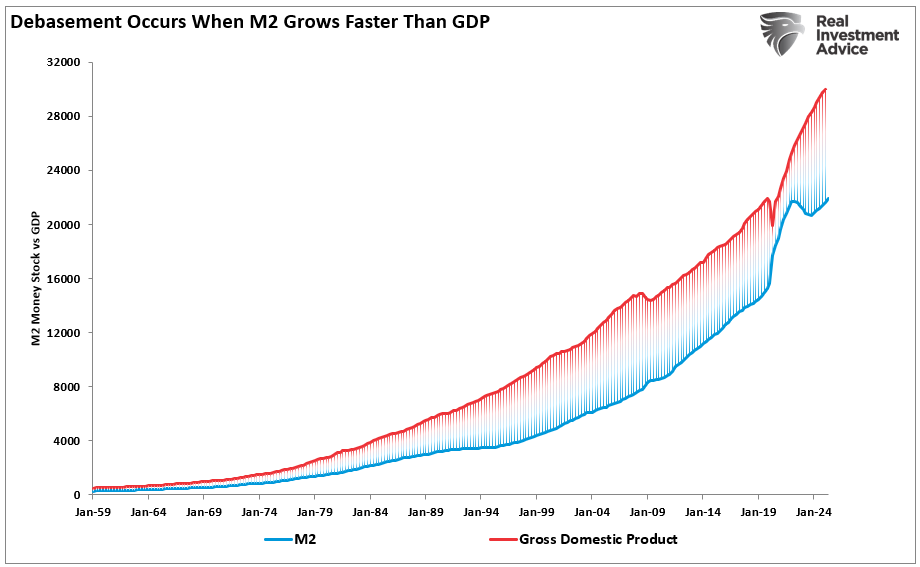

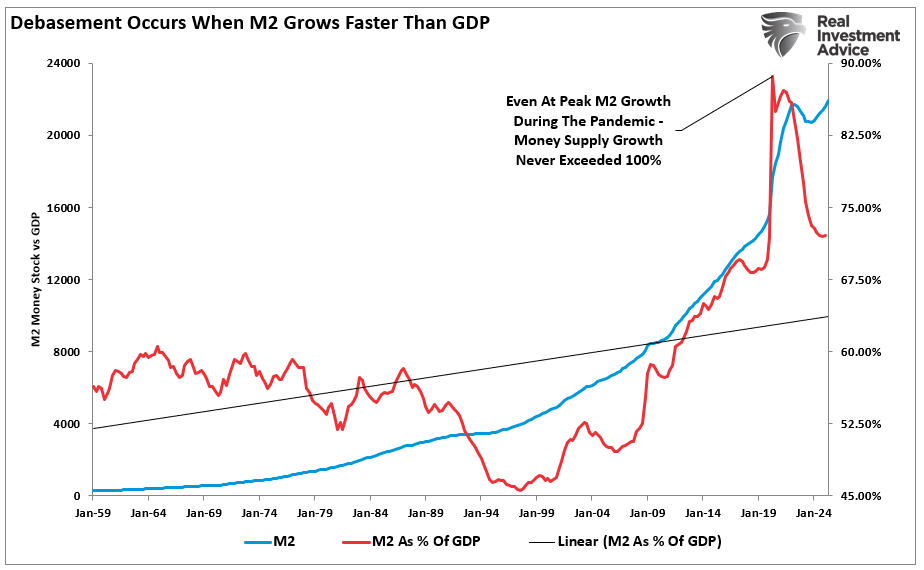

It’s easy to point to M2 charts and scream “debasement. “ However, the money supply must grow as the economy grows. If it doesn’t, deflationary risks emerge. Therefore, the key is whether money creation exceeds economic growth in a sustained way. Since 1959, the money supply has grown in alignment with economic growth.

A better way to assess this is by comparing M2 to GDP. Historically, the two have tracked closely. Even during the COVID shock, M2 as a percentage of GDP remained below 100%, meaning money supply growth was broadly aligned with economic output. Today, that ratio is falling, not rising.

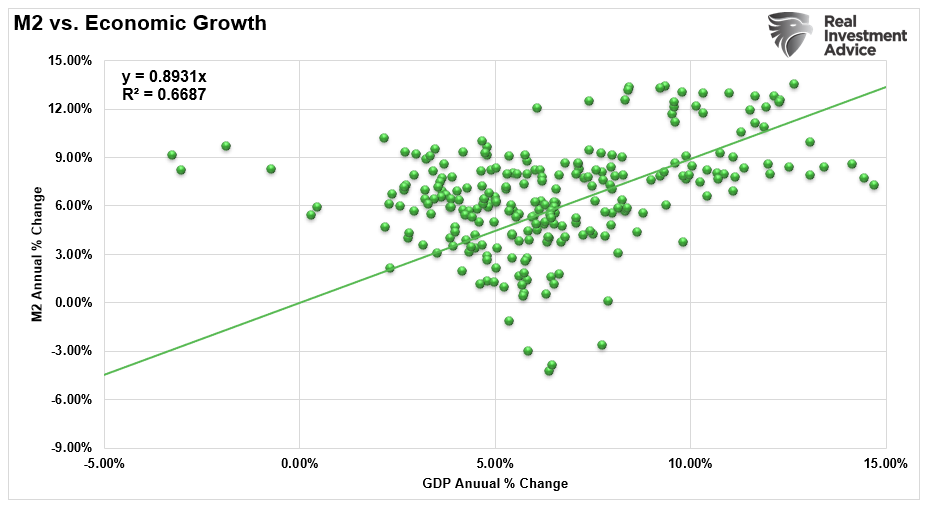

The reality is, as you would expect, that the growth rates of M2 and the economy are highly correlated.

If the dollar were truly being debased, you’d see a very different set of outcomes:

- Capital fleeing U.S. assets (stocks, bonds, gold, cryptocurrencies)

- A collapse in Treasury demand.

- A breakdown in global trade settled in dollars.

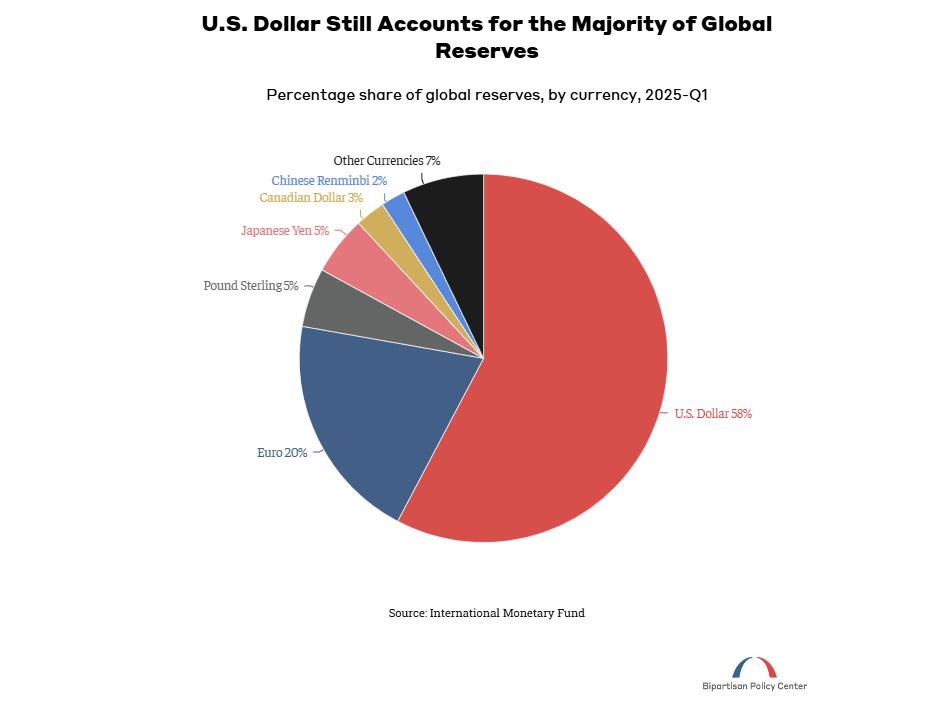

Instead, we see the opposite. Treasury demand remains robust. The dollar is still used in 88% of global foreign exchange transactions, 58% of international exchange reserves, and 54% of global trade. Central banks, sovereign wealth funds, and institutional investors continue to hold and accumulate U.S. assets.

Moreover, money supply must be understood alongside velocity — how quickly money circulates. The Federal Reserve’s own data show that M2 velocity collapsed after the global financial crisis and again during the pandemic, neutralizing fears of runaway inflation. Growth in money supply, therefore, is not inherently destabilizing. More often than not, it is a sign of economic vitality.

Debts and Deficits Are Private-Sector Surpluses

The second flaw in the thesis is its treatment of government deficits. Gundlach’s warning that “deficits are out of control” is a popular refrain, but it misses the accounting reality: one sector’s deficit is another’s surplus. By definition, when the government runs a deficit, those dollars end up as net financial assets in the hands of the private sector.

This isn’t just theory; it was demonstrated in real time during 2020 and 2021. Record government spending and transfer payments pushed the household saving rate to an all-time high of 33%. The Bureau of Economic Analysis reported that households accumulated trillions in excess savings as stimulus checks and unemployment benefits landed in their accounts. That deficit spending became private wealth, fueling consumption once the economy reopened.

In other words, deficits are not inherently destructive. They fund spending that becomes income for households and businesses, supporting economic activity. In fact, deficits often stabilize the economy during recessions, providing the private sector with liquidity and balance sheet repair.

Treasuries, the byproduct of deficits, are not “worthless paper” as the alarmist narrative suggests. On the contrary, they are among the most demanded safe assets in the world. Treasuries are the bedrock of global finance, from pensions and banks to foreign central banks and stablecoin issuers. They provide collateral, safety, and yield, all of which support, rather than undermine, the dollar’s global role. As ” Myth Busting” notes, the often-repeated narrative that foreigners are selling U.S. Treasuries is false.

“This falsehood stems from a misunderstanding of how international finance operates. A large majority of foreign trade occurs in dollars. Accordingly, foreign nations must hold dollars. Whether in a bank or through direct purchases of bonds, a significant percentage of the dollars, also known as reserves, end up in the Treasury market. Unless another currency usurps the dollar’s reserve status, this will continue to be the case. Moreover, global economic growth and inflation lead to increased dollar trade, resulting in more dollar reserves and, ultimately, more US Treasury holdings by foreign investors.

As some claim, selling large amounts of Treasuries would likely lead to significant losses for the sellers due to the impact it would have on the bond market and their remaining bond holdings. Thus, the myth of a mass sell-off is unfounded, as it would be financially counterproductive for foreign investors, who rely on Treasuries’ stability and interest payments”.

But what about the other claims?

Gold’s Risk: The Dollar and Real Rates

Even if one accepts that deficits and money supply growth are inflationary, the bullish thesis on gold runs into another significant problem: the U.S. dollar. Gold is priced in dollars, and history shows that gold often weakens when the dollar strengthens and when real interest rates rise.

The World Gold Council and CME data confirm that the opportunity cost of holding gold, which pays no income, rises when real rates increase. Similarly, a stronger dollar makes gold more expensive in foreign currencies, dampening demand. That relationship has been evident for decades and was particularly sharp during 2014–2016, when the dollar surged, and gold fell by more than 40%.

What could spark another dollar rally today? Ironically, the same deficits and growth that Gundlach and Fink worry about. If U.S. growth outpaces Europe’s and Asia’s, capital inflows will increase the dollar. If the Federal Reserve remains less dovish than other central banks, rate differentials will widen in the dollar’s favor. In risk-off environments, global investors often seek the safety of dollar-denominated assets, creating demand for treasuries and strengthening the dollar further.

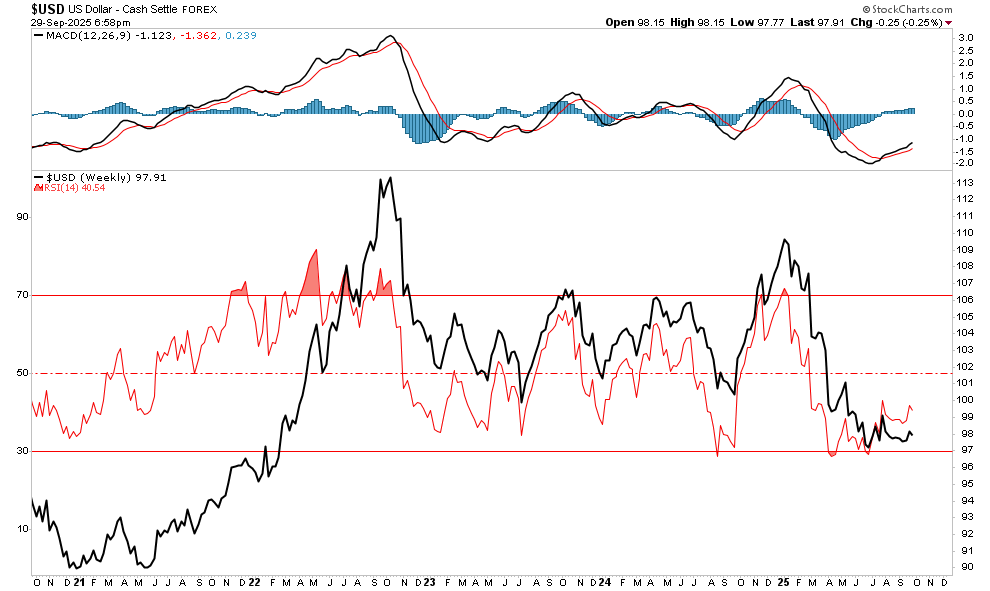

Furthermore, the technical backdrop for a dollar rally is becoming very compelling. After the extreme dollar rally in 2022, the more extreme overbought condition has fully reversed, and the dollar has built a strong base.

(Click on image to enlarge)

Another potential boost to the dollar is a rather massive short position against the currency. If economic growth improves, as Wall Street expects, and the dollar rallies, traders will be forced to cover, providing an additional tailwind to a dollar rally.

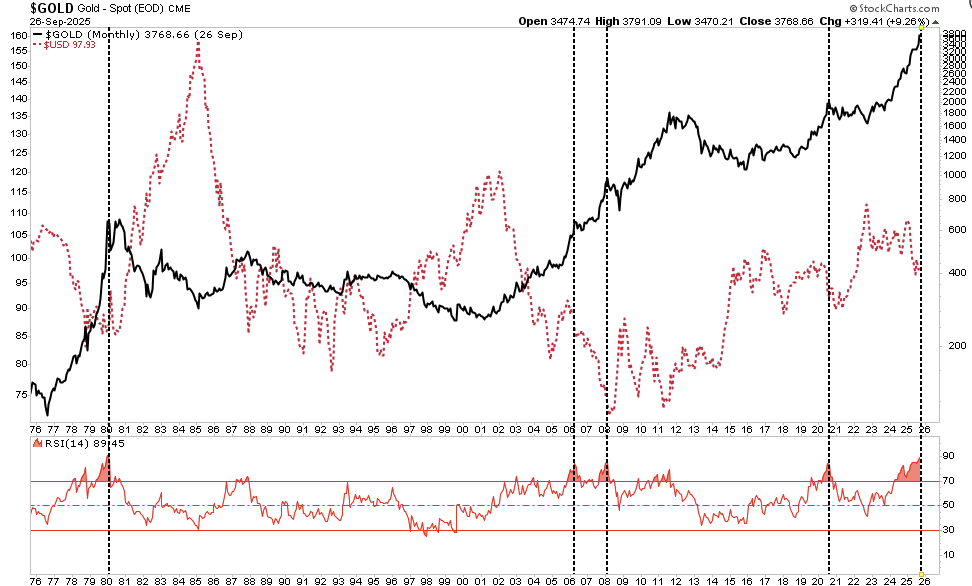

Should such a dollar rally occur, gold prices would likely face a sharp reversal. That dynamic undermines the claim that deficits and money growth guarantee higher gold prices. The relationship between gold and the dollar is a key macro driver that cannot be ignored. As shown, gold carries a negative correlation to the dollar, and previous periods of extreme overbought conditions in gold against a backdrop of a rising dollar had investor consequences.

(Click on image to enlarge)

Conclusion: Focus on Fundamentals, Not Fear

Bold calls to “run to gold, silver, and bitcoin” make for strong headlines, but they oversimplify the reality of modern finance. As we’ve seen, money supply growth is not inherently a sign of debasement but reflects economic expansion. Far from being destructive, government deficits flow directly into private-sector savings and stabilize household balance sheets. And gold’s trajectory is less about deficits than real rates and the dollar’s path.

For investors, the key is not to chase fear-driven narratives but to focus on fundamentals. The dollar remains the world’s reserve currency, supported by demand for Treasuries, deep capital markets, and the rule of law. Unless another currency rivals its scale and liquidity, the dollar will continue to anchor the system. That means gold, silver, and bitcoin should be seen as tools for diversification, not as wholesale replacements for dollar-based assets.

As such, investors should focus on matters concerning long-term investment outcomes.

- Track economic growth and money supply together. A rising money supply in line with GDP is a healthy signal; watch for persistent divergences instead of reacting to charts in isolation.

- Monitor real interest rates. Gold’s opportunity cost rises when real yields move higher. Use shifts in real rates as a guide for adjusting precious metals exposure.

- Follow dollar cycles. The dollar’s strength or weakness often dictates the outcomes of gold, silver, and bitcoin. Align positioning with the dollar’s broader trend.

- Balance portfolios. Use gold, silver, and bitcoin as diversifiers, not core holdings. Maintain exposure to productive assets that benefit from growth.

- Assess debt sustainability. The real risk is debt growing faster than the economy; track whether fiscal policy supports long-term growth.

In short, investors should focus less on the fear of deficits and more on the fundamentals of growth, real rates, and the dollar. Discipline, diversification, and attention to economic cycles remain the foundations of long-term wealth preservation.

Leave the narratives for shills, fear-mongers, and those promoting a product.

More By This Author:

Inflation In Focus: What Market Data Tells Us

Beyond Meat Surges: Another Meme Ponzi?

Leveraged ETFs: Yet Another Sign Of Rampant Speculation

Disclaimer: Click here to read the full disclaimer.