Bank of Japan (BoJ) officials are increasingly discussing the weak yen as a source of inflation. Their concern is that prolonged yen weakness raises import costs and encourages businesses to pass those costs on to consumers. Bear in mind that Japan imports almost 100% of its energy needs and a large portion of other essential materials and goods. The graph below shows that the yen has depreciated by about 35% over the last five years. Moreover, as we will discuss shortly, the yen is now approaching the lows of August 2024.

The BoJ is widely expected to hold its policy rate at 0.75% at next week’s meeting, but we expect it to hear more from the bank about the weak yen and its influence on inflation. If currency-driven inflation intensifies and the public continues to pressure politicians over inflation concerns, the yen could force the BoJ to pursue additional rate hikes to strengthen the currency.

Why do we care? In August 2024, the S&P 500 fell by slightly over 10% in a matter of days. This was the result of a rapidly strengthening yen. As the yen appreciated, many traders were forced to reverse yen carry trades. Simply put, these traders borrowed cheap money in Japan and invested the money in U.S. stocks and bonds. The economics of the yen carry trade depend on a weak yen. Thus, when we hear the BoJ express concern about a weak yen, we must remember that the yen carry trade can be powerful. This is not a call to action, but we advise monitoring the BoJ and the yen.

(Click on image to enlarge)

What To Watch Today

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

Yesterday, we discussed the rather significant bet being made on the “reflation” theme. As shown, the factors that are most tied to that reflation theme are now very overbought and extended. In fact, all the factors have shifted up and to the right as markets have continued to push higher in recent months. However, from a contrarian perspective, this is also where opportunity likely will present itself.

Eventually, for whatever reason, earnings disappointment, economic slowdown, or a credit-related issue will cause the market to rotate from the more aggressive to defensive positioning. When that will occur is anyone’s guess. However, historically, these rotations have occurred regularly, and as an investor, it is vital not to become too complacent with overly aggressive positioning. Ironically, one of the areas that was most overbought in the fall of last year (Mega-cap Growth) has rotated to the most oversold, along with large cap growth, low beta, and quality factors. In other words, a rotation could be from the non-profitable small-cap indices into the higher quality, revenue-generating behemoths of the market.

However, for now, the game is afoot as risk sentiment remains very elevated and investors are chasing assets into the New Year. The good news is that the market has broadened significantly, with everything from small caps to international markets rallying to new all-time highs.

As of now, there seems to be very little risk in investing in the markets, so equity exposures should remain high. However, many of these markets are pushing into increasingly overbought territory, so don’t forget to take profits and rebalance risk accordingly.

Notably, a rotation will occur; it is just the timing that needs to be right.

Oil Prices Buck The Reflation Narrative

There is a growing chorus calling for an economic acceleration and a resulting surge in corporate earnings. They base their forecast on easing financial conditions, including lower rates and QE, fiscal stimulus, and the promise of productivity gains from AI. Equity markets appear to embrace this narrative, as many stock factors and sectors that lagged mega-cap stocks are outperforming the market.

This optimism from economists and investors clashes with oil prices. As shown below, crude oil has been in decline for the better part of four years and shows no signs of reversing. Historically, sustained economic acceleration has been accompanied by rising energy demand and higher oil prices as transportation, manufacturing, and industrial activity intensify. The absence of that positive price response suggests that the growth narrative may be more financial than fundamental.

In short, weak oil prices are not confirming economic reacceleration; they are quietly warning that headline optimism is running ahead of underlying, energy-intensive activity. A reversal in higher oil prices would improve the prospects of an economic acceleration.

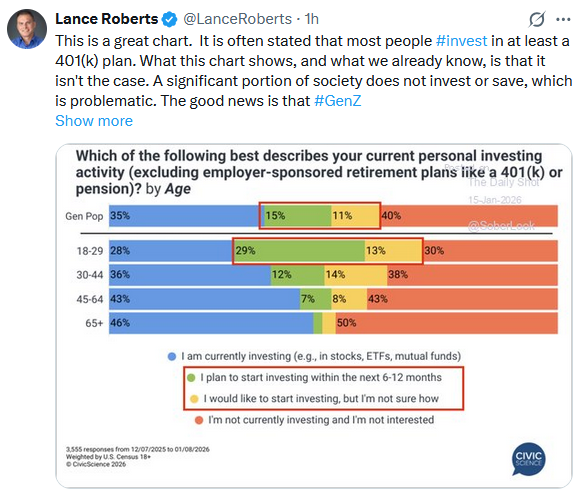

Tweet of the Day

More By This Author:

Luxury Slump Bankrupts Saks Fifth AvenueThe Silver Surge: Micro Bubble Or Reasonable Valuation?

Transportation Stocks Are At Odds With Truck Sales

Comments

Log in or sign up to join the conversation.