Central Banks Should Forget About The 2% Inflation Target

“Despite years of monetary stimulus, inflation in the United States, Japan, and the eurozone continues to undershoot central banks’ 2% target. Rather than doubling down on their oft-missed goal, however, perhaps the Fed and other central banks should quietly stop pursuing it aggressively.” (Jeffrey Frankel, Project Syndicate, July 25, 2019)

This writer completely agrees with Jeffrey Frankel’s suggestion that central banks should give up on their notion of achieving a 2% inflation target.

The failure to achieve this target is well known for the larger central banks in the US, the Euro Area and Japan. Canada is also somewhat behind in achieving its 2% inflation target. If, with nearly fully employed economies in all cases, inflation remains below 2%, then so be it.

Coming after the Great Recession (2008-09) the monetary authorities of the large central banks took serious steps to boost inflationary expectations in the private sector. The steps they emphasized included the 2%-or-higher inflation objective, as well as massive quantitative easing which was also expected to boost inflationary expectations.

Nonetheless, inflation never really crept up very much and perhaps weaker than usual labour markets explain some of the slow reaction to monetary easing.

In the United States the US Fed was given the task by Congress to guide the economy to full employment and stable prices. While specific numbers were never specified, economists based on historical experience tend to think that stable prices and full employment were both difficult to achieve together at the same time. The Fed wisely chose its 2% inflation target as a practical compromise.

But generating a stable 2% inflation rate was easier to theorize about than to realize. There were in fact many intervening variables affecting this objective, including globalization pressures which tended to lower domestic wages and prices, and which also affected the employment statistics and the quality of work.Capital mobility has also increased over the past quarter century, and this has also tended to lower domestic inflation.

Much of the earlier thinking about potential tradeoffs between inflation and unemployment have been changed, as inflation expectations seem to have become unhinged from the new full employment reality in the US. Due to globalization pressures, many of the prices consumers pay simply don’t seem to respond to the strength or weakness of the economy.

Thus, one of the principal reasons why the Fed cut interest rates on July 31 is that inflation was running well below its 2% target.

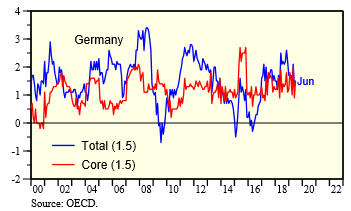

Consumer Price Index Inflation Rates, Key Countries

Arthur

I am in full agreement

Perhaps a target of nominal GDP would be better, implying Keynes' s money illusion is the key variable.