The inflation report last week was met with a big sigh of relief by investors. Stocks and bonds rallied as the Fed’s Whip Inflation Now project seems to be finally bearing some fruit. In reality, inflation peaked months ago but the Fed hadn’t really caught on yet – they’re a little slow – and the market has been fearing that they would go too far and cause a recession. But surely, the market seemed to say, the moderation is so obvious now that even Jerome Powell can see that he’s done enough.

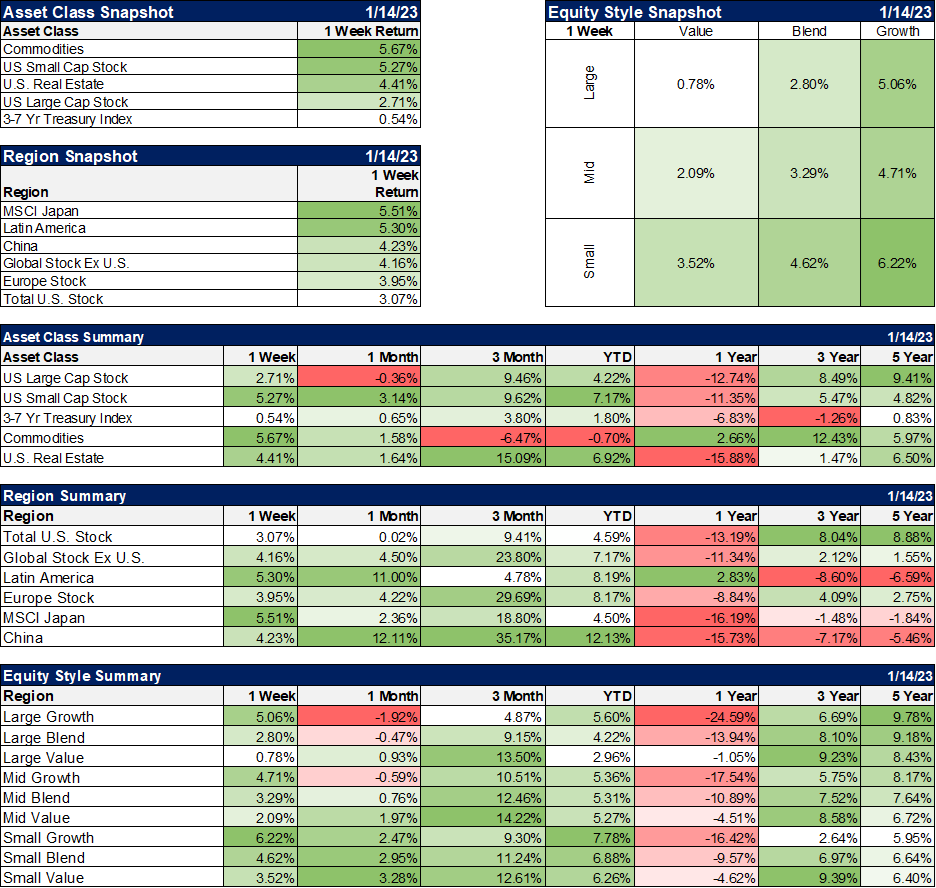

That being the case, the natural thing to do was buy stocks and investors did just that last week. The S&P 500 was up 2.7% on the week, continuing a rally that started in mid-October and has seen it rally 14.5% from its intraday low on October 13th. It isn’t just the S&P 500 up either. Small cap stocks are up 15.6%, mid cap 18.8%, and REITs 20% since October 13th. European stocks have done even better beating the US by a wide margin, up 41.7%. The more diversified international value index we hold (EFV) is up 30.3% from its low. International value was down less at the low (-22.3% vs -25.9%) and is now down just 4.3% year over year vs 12.9% for the S&P 500.

Forgive me for being the party pooper but I think this might be just a tad overdone. The inflation report was pretty good last week, continuing the moderation that started in July of last year. I’d hardly give credit to the Fed though. About the only thing I can directly credit to their interest rate hikes is the whopping 2.4% drop in national housing prices. Did the Fed have anything to do with the drop in used car prices which are down every month since last June and 8.8% year over year? How about the 9.4% drop in gas prices last month? Or the 3% drop in airfares? How about the 1.8% drop in bacon prices (thank the Lord!)? To be fair, they didn’t have much to do with the 2% rise in egg prices either. It is certainly true that inflation has cooled considerably since last year. The CPI is up a total of 0.9% over the last 6 months and if that keeps up, I’d say mission accomplished. But, relative price changes like these happen all the time and have nothing to do with real inflation, which is about the value of the dollar. Inflation is higher during times of dollar weakness. And the dollar has most certainly not been weak recently.

(Click on image to enlarge)

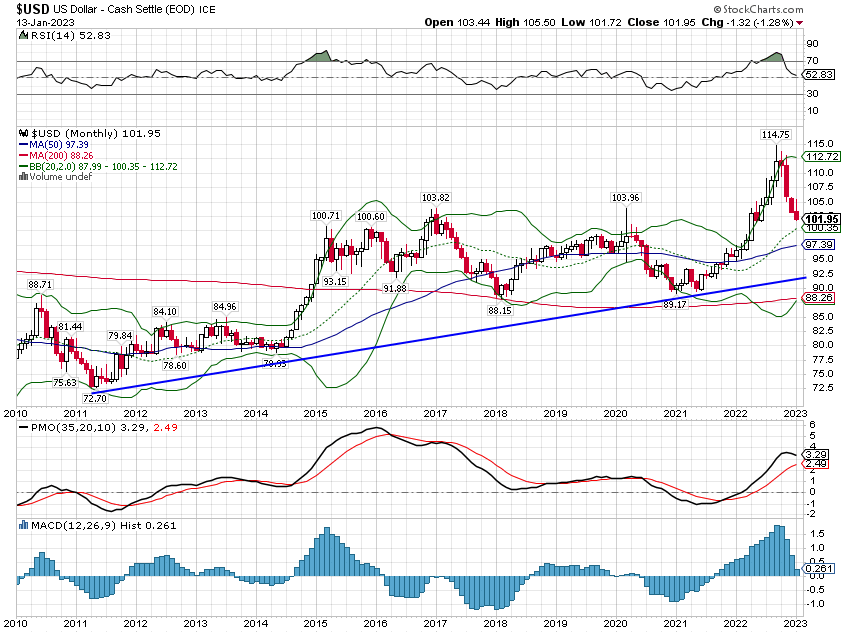

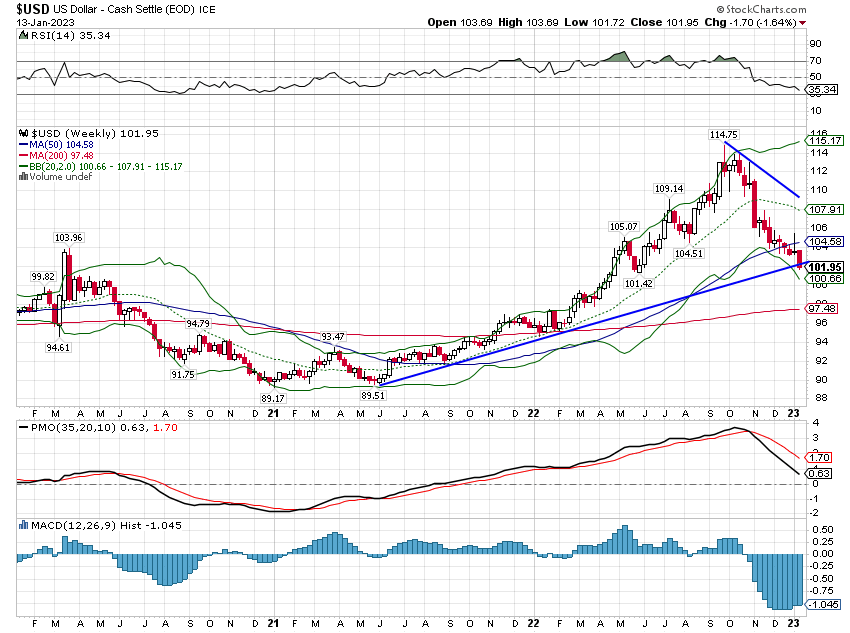

If you look over a longer time frame, you can see that last year we rose into the upper band of a wide trading range that has persisted since the late 1980s.

(Click on image to enlarge)

There are three zones within which the dollar has traded over the last 35 years or so. When the dollar is in the middle band, from roughly 90 to 105, the economy is fairly stable, nominal, and real. When the dollar is in the upper or lower bands, the economy is vulnerable to crisis. The period from 2000 through 2002, the end of the last strong dollar period, corresponds to the unwinding of the dot com bubble and the various corporate scandals such as Enron. The S&P 500 was down all three years.

The period starts in 2006 – 2009, when the dollar passes into the lower zone, is well known and requires no description. The period from 2009 to 2015, a weak dollar period, is one where we seemed to be always on the edge of another crisis. The Eurozone crisis – Draghi’s “whatever it takes” to preserve the Euro – was in this period and the US economy nearly fell into recession.

The period from mid-2015 to 2022 was another fairly calm period, COVID notwithstanding. You might notice though that we’ve just spent a good portion of 2022 in the upper red zone. Isn’t it interesting that this period echoes the previous uber-strong dollar period from 2000 to 2002?

While we remember that earlier period as the unwinding of the dot com era, the dot com stocks were really just a sideshow. The real story then was the unwinding of the tech bubble, the one that existed in companies with actual revenue and earnings. We just spent the last year unwinding a bubble in crypto that looks an awful lot like the dot com stocks – no revenue or earnings or plan – and a bubble in profitable tech companies. Do you think that’s a coincidence? I don’t.

The inflation we’ve experienced over the last year was real – prices really did rise – but it was not one driven by a weak dollar. It was driven by the pandemic distortions caused by massive government intervention in the economy that affected both demand and supply to a degree never seen before in modern times. In a sense, we had a supply and a demand shock simultaneously, although I’d put more emphasis on the demand side. Now, as the interventions fade – and yes they will fade over time – so will the effect. I would not expect prices to fall back to the previous level but the inflation rate should moderate – for now. With the dollar now back in the stability zone, the direction of inflation will likely depend on whether it can stay there.

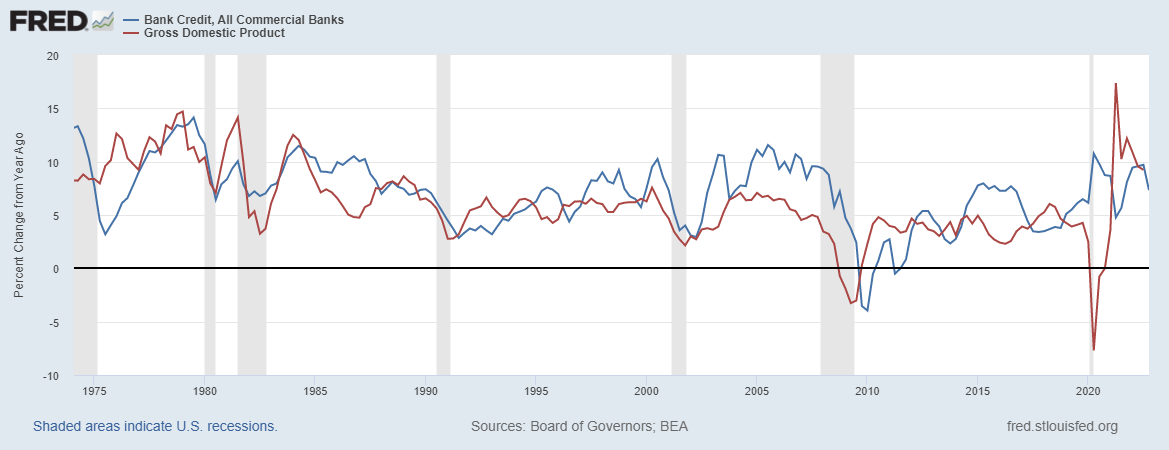

The fact is that rate hikes have not had much to do with the economic slowdown and indeed haven’t managed to slow things all that much at all on a nominal basis. It certainly hasn’t affected bank lending. With the QE bonanza coming to an end, banks seem to have gotten back to their roots of actually lending money. Total bank credit is up nearly $1 trillion in the last year and the lending is across multiple sectors. Real estate lending is up 11.3% ($540 billion) over the last year. And no, that hasn’t slowed recently with the slowdown in residential; the year-over-year rate of change is still accelerating. C&I loans are up 14.6% over the last year although that one may have peaked. Consumer loans are up 11% year over year. The year-over-year change in total bank credit is correlated with the year-over-year change in NGDP and CPI so the fact that its rate of change has moderated some recently would seem to be good news, as the drop seems to have mostly come out of inflation.

(Click on image to enlarge)

The slowdown in goods spending over the last year has been modest (-0.7% real) but entirely expected and offset by a rise in services spending (+3.5% real). You might remember me talking about that over a year ago; it wasn’t that hard to figure out. A big part of the recent slowdown appears to be nothing more than an inventory correction on the goods side of the economy. We knew there was a lot of over-ordering of goods during the pandemic as supply chains became strained and everyone saw the resulting inventory mess at Walmart, Target, and a few other retailers. Walmart appears to have solved its inventory issues, other retailers are getting there and inventory-to-sales ratios were already rolling over in October when we got our last full look at inventories. But if preliminary inventory numbers are any indication the correction is likely already nearing its end. By the way, this inventory correction is likely the source of the recent weakness in the ISM reports. The bullwhip effect we heard so much about last year so far looks more like a riding crop.

Having said all that, I would not get too comfortable with the economy right now. There is a modest slowing underway and it seems like everyone is bracing for things to get worse. Preparing for a recession could prove a self-fulfilling prophecy. Banks are starting to set aside reserves for future loan losses and it’s hard to envision bank lending continuing to expand at the current pace in that environment. Of course, a drop in the rate of change isn’t necessarily a bad thing if it moderates at say 5% growth. That’s where those healthy household and corporate balance sheets might come in handy. A tightening of lending standards, which we’ve already started to see, might not lead to much of a reduction in actual lending. In fact, it might be a healthy development.

Environment

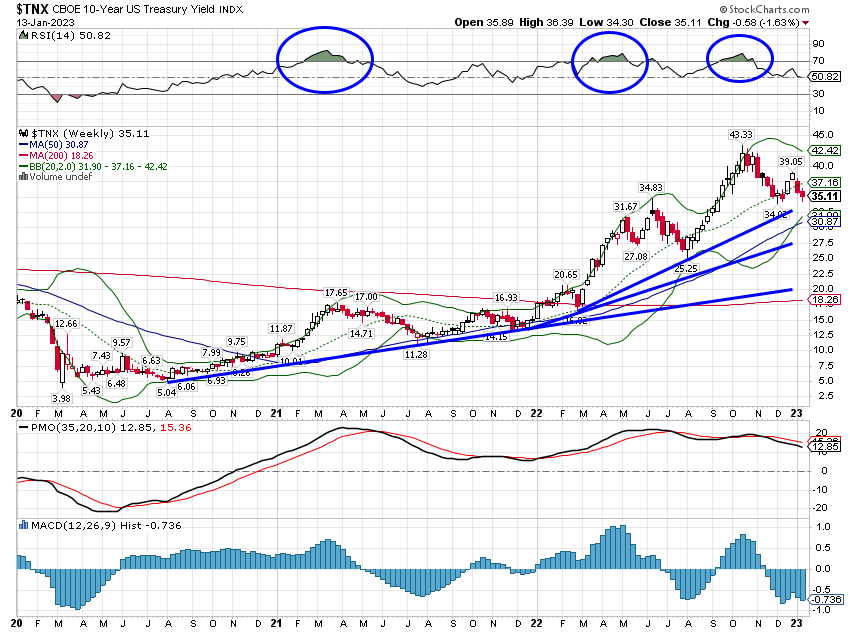

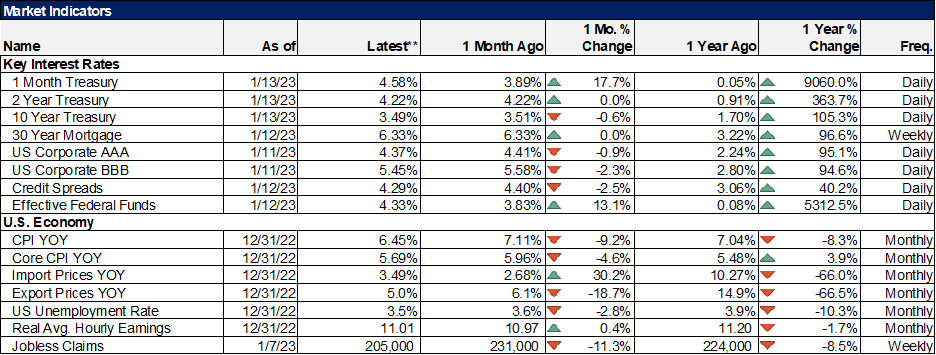

The 10 year Treasury yield fell about 6 basis points last week; the CPI report was priced in. The short-term trend is still down and the intermediate-term trend is still up. With a plethora of economic data next week, we may get a clue about whether the intermediate uptrend will hold. Inflation expectations continue to moderate. 5 year and 10 year breakeven inflation rates are 2.18% and 2.2% respectively. The 5 year, 5 year forward (5 year expectations starting 5 year from now) breakeven is 2.16%. Last week’s CPI report did show inflation moderating but the market is exhibiting a high degree of confidence that future inflation will fall pretty dramatically from where it is today. Keep in mind that December’s extreme cold weather and the disruptions it caused are likely to affect the data.

(Click on image to enlarge)

The short-term trend of the dollar is still down as well. The intermediate-term uptrend is hanging by a thread. If the data for December comes in weak – and I wouldn’t be surprised by that at all – then it may finally break down. Still, I wouldn’t expect a dramatic downdraft. Speculators have turned pretty bullish on the Euro and are as long as they’ve been since the summer of ’20. Specs are still short the Yen, C$, A$, and Pound so there may be some more dollar downside but the Euro is the biggest weight in the index. If we move lower next week, I’d expect 100 to be good support.

(Click on image to enlarge)

Markets

It was everything up last week with commodities leading the way on the back of a big rise in crude oil (+8.3%) and copper (+7.8%). Crude looks like it has put in a bottom but that probably depends on the economic outlook. On that front, it is worth noting that Brent and WTI are both now in contango; demand appears to have weakened in the near term. It was easier to dismiss when it was just WTI but the Brent/crude spread has narrowed considerably so this is looking more like a demand problem despite last week’s rally. The contango is not deep so it won’t take much optimism to flip it to backwardation but for now, I’d be wary of the rally in crude.

The copper market has also flipped to contango over the last month, also an indication of weak near-term demand. That seems odd with all the hoopla around China’s reopening, especially with inventories low and a production shortfall expected this year. This bears watching closely as these are not the only markets that are showing weak demand. Again, though, the contango is small and is consistent with the recent economic data which has been weaker but not too weak.

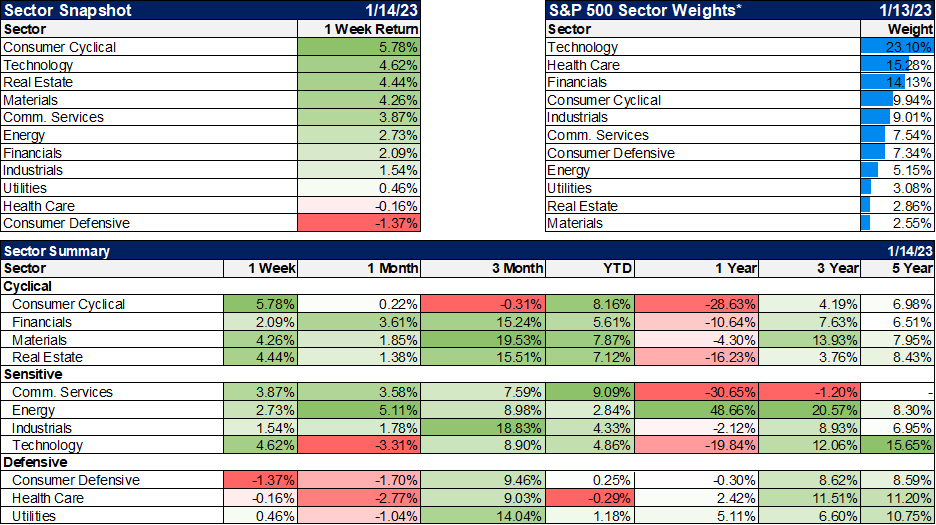

It was also a week of more speculative activity with small cap and growth stocks outperforming strongly. The CPI report last week firmed up the consensus around rate hikes (February is now a 94% chance of 25 basis points and the bet is that it will be the last one) and a soft landing is rapidly becoming the consensus. I’m reluctant to make that bet, at least for now. The economic trend is still weaker and until that changes I think you have to assume the trend will continue. The uptick in the University of Michigan consumer sentiment reading last week was encouraging but the near-term data seems likely to continue to show weakness.

International markets also outperformed last week on a weaker dollar with Latin America and Japan leading the way. Latin America was up despite continued political drama with Peru and Brazil both seeing demonstrations against the current administrations. Japan was mostly a Yen story with the currency up 3.3% on the week. That could get interesting this week as the BOJ’s 10 year JGB peg is again being challenged.

The bet on a better economy shows up in the sector report too as Consumer Defensive was down the most for the week. Consumer cyclicals showed the biggest upside along with materials and real estate. Even technology joined the rally as semiconductors were up over 6%.

(Click on image to enlarge)

(Click on image to enlarge)

Economic Indicators

Corporate bonds were quite strong last week and credit spreads continued to narrow. High yield spreads peaked in July at nearly 6% and have now fallen all the way back to 4.29%. That is still above the lows near 3% set late last year but not worrisome. The market is obviously not very concerned about any potential economic downturn.

The Treasury yield curve is starting to normalize in the long end. The 30 year/10 year spread is now positive and the 10 year/5 year spread is down to just 10 basis points. The very short end of the curve continues to see 1 month bill yields rise while the 2 year continues to trade sideways as it has since late September. A re-steepening of the long end doesn’t mean much in the short term but if we start to see short-term rates fall rapidly that is an indication the market is anticipating imminent rate cuts and would obviously not be a good sign. But we aren’t there yet so we remain cautious but not overly concerned just yet.

(Click on image to enlarge)

The Fed has spent the last year trying to convince the market that it would do whatever it takes to bring down inflation. Their preferred method of doing so has involved a pace of rate hikes like we’ve never seen. And inflation, as measured by the CPI, has come down. But correlation is not causation and the Fed’s rate hikes do not seem to be having much of an effect on credit markets where they presumably should.

We’ve had a period of good news on the inflation front lately and the markets like that. But continued high nominal growth means the path to an acceptable CPI rate of change is unlikely to be a straight line. The dollar has only just come down from the danger zone and a rebound from here seems likely, at least short term. We may well avoid recession this year but that doesn’t mean it’s all clear for stocks and bonds. And there are still fairly good odds on a recession. Stay cautious…for now.

More By This Author:

Market Trends: Large Cap EquityWeekly Market Pulse: The Consensus Will Be Wrong

Great News! Consumer Sentiment Is Awful

Comments

Log in or sign up to join the conversation.