Weekly Market Pulse: Follow The Delphic Maxims

Know Thyself is the first of three Delphic maxims that were inscribed at the Temple at Delphi. The aphorism is most often associated with Socrates who, according to Plato’s dialogues, said, among many other wise things, “to know thyself is the beginning of wisdom”. But it was only the first of the three maxims and an investor needs to know all three. “Nothing to excess” and “certainty brings insanity” are the other two and are just as important as the one everyone remembers.

An investor must know him or herself because we humans are full of biases that affect our decision-making process. Some people will interpret every bit of news in a negative light while others see the silver lining in every dark cloud. I have been accused of the latter at times and I take that criticism seriously. It is hard to “know thyself” and I try to guard against my optimistic bias whenever I make decisions. But I am far from perfect so I just assume that there is a decent chance I’ll be wrong about any decision I make.

That doesn’t mean I don’t act on my views; it just means that I endeavor to quickly correct any mistake I do make. I learned a long time ago that in investing, slugging percentage is much more important than batting average. You can be wrong a lot – even more than half the time – and still make a good return if you make a lot when you are right and lose a little when you are wrong.

An investor also needs to be careful to do “nothing to excess”. I have written about this before, referring to how some investors think investing is an all-or-nothing exercise. If they believe something is going to happen – recession, inflation, dollar devaluation – they want to invest all or a substantial portion of their assets to benefit from their “vision”. I have said many times, that we don’t practice this “all or nothing” investing and if you expect us, for instance, to sell all our stocks and buy long-term Treasuries because the yield curve has inverted, you’re going to be disappointed. Humility is, by far, the most important character trait of a good investor.

“Nothing to excess” leads to the third maxim; “certainty leads to insanity”. One thing I am absolutely certain about when it comes to investing is that there are no certainties. Things that have never happened before happen all the time in markets and things that have always worked in the past often just stop working for seemingly no reason. Although, usually the reason is that everyone is doing the thing that has always worked rendering it no longer valid. My favorite example of this is the Dogs of the Dow, which worked for years – until everyone started using it in the 90s – and started working again after everyone abandoned it. Wall Street is really good at doing things to excess.

A good investor knows his own biases (know thyself), diversifies his portfolio (nothing to excess), and readily and quickly admits his mistakes (certainty leads to insanity). The first and third things are hard but the second one is completely in your control and pretty easy. Diversification is the only free lunch on Wall Street and millions of investors ignore it in favor of fancy, expensive dinners hosted by false oracles who tempt them with certainty.

I write about these pearls of wisdom today because I think we need them more today than ever before. Investors have convinced themselves that there is certainty today about the economy, that today’s conditions are so obvious that they warrant an extreme position. That one thing is, obviously, recession. The yield curves have inverted and therefore recession is inevitable, unavoidable. Because of this, they are doing the easy thing, sitting in cash – and at least getting paid for a change from the last decade – and waiting for the all-clear.

I am again reminded of the Keynesian beauty contest view of the markets. I’ve written about this before but to remind you of the concept here’s the Wikipedia entry:

Keynes described the action of rational agents in a market using an analogy based on a fictional newspaper contest, in which entrants are asked to choose the six most attractive faces from a hundred photographs. Those who picked the most popular faces are then eligible for a prize.

A naïve strategy would be to choose the face that, in the opinion of the entrant, is the most handsome. A more sophisticated contest entrant, wishing to maximize the chances of winning a prize, would think about what the majority perception of attractiveness is, and then make a selection based on some inference from their knowledge of public perceptions. This can be carried one step further to take into account the fact that other entrants would each have their own opinion of what public perceptions are. Thus the strategy can be extended to the next order and the next and so on, at each level attempting to predict the eventual outcome of the process based on the reasoning of other rational agents.

“It is not a case of choosing those [faces] that, to the best of one’s judgment, are really the prettiest, nor even those that average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth and higher degrees.” (Keynes, General Theory of Employment, Interest and Money, 1936).

Today, everyone knows the yield curve is inverted and that recession always follows yield curve inversions. Those investors who have convinced themselves that recession is inevitable have taken actions to protect themselves from what they know is coming. They’ve sold stocks and bought long-term bonds because in recessions, stocks fall and bonds rise.

The question is whether by doing so, they have created the very condition that causes them to fear recession. In fact, many of them anticipated the yield curve inversion – they could see it flattening – and took action well in advance of the actual event. But in doing so, did they cause the yield curve inversion they feared? The persistent inflow of capital to long-term government bond funds could certainly be interpreted that way. In addition, by selling early and pushing the stock market into a bear market, they may have influenced other investors to follow their lead. And as the yield curves continue to invert across more and more maturities, investors who haven’t acted yet feel an urgency to join the crowd in anticipating the recession that has defied the bears’ predictions by refusing to arrive.

If that is true – and I’m not certain it is – then who are the people buying stocks over the last two months? Those are the second-degree thinkers in Keynes beauty contest. The second-degree thinkers believe that if everyone believes recession is coming and they’ve already acted on that belief, there is no one left to sell and the market can – and has – found a bottom. So they have been buying despite their own knowledge of yield curve inversions.

Then there are the third-degree thinkers. They were quietly buying over the summer, acting with the second-degree thinkers but they’ve stopped now. Why? Because they know that a lot of people know what the second-degree thinkers know and have acted on it already – they’ve bought stocks. The third-degree thinker believes the second-degree thinkers have nearly exhausted their buying power and that it is prudent to wait for more information. The third degree is uncertain about the economic outlook, trying to guard against excessive optimism, not making any big bets, and is still holding some cash. We are the third degree.

Environment

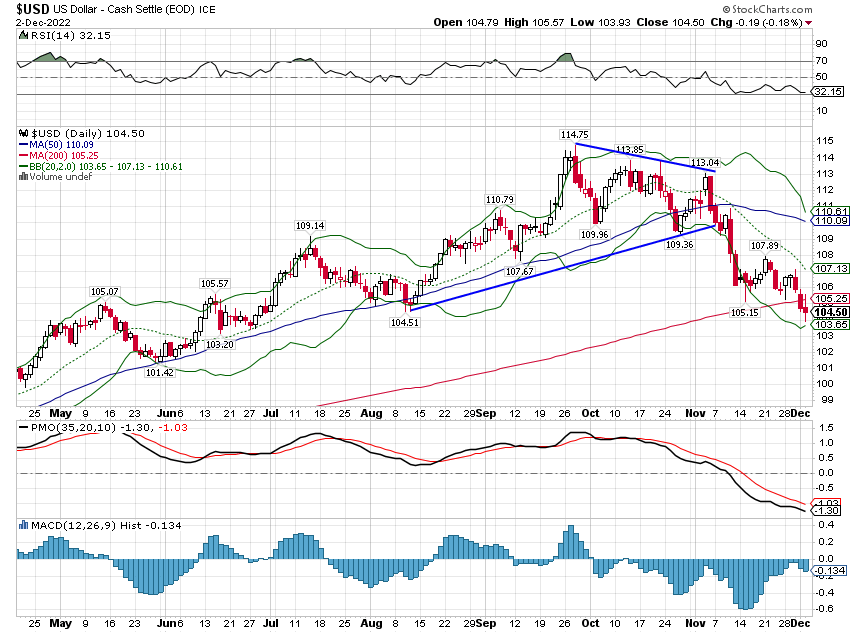

The dollar index closed below its 200-day moving average last week for the first time since June 2021. The 200-day MA is a metric commonly used to define whether an asset is in an uptrend or downtrend. I already made the determination that the dollar was in a short-term downtrend several weeks ago (early November) when it broke under the previous uptrend line of around 110. This move below the 200-day is mere confirmation of the short-term downtrend.

(Click on image to enlarge)

While I still expect to see the dollar fall to the 102 area, in the short term, the buck is oversold and a bounce would not be unexpected. A move up to near the 108 to 110 area would likely resolve the oversold condition and set the stage for further declines. Speculators continue to reduce their bullish bets but are still quite long. I’d guess that any rally would be seen as an opportunity to reduce exposure going into year-end.

This decline in the dollar has primarily been driven by the Euro as growth expectations there rise relative to the US. The energy situation in Europe appears resolved for now but it is a long-term problem that will take more than a few months to remedy. Winter looms and I don’t think anyone knows if they have sufficient supply to avoid more pain.

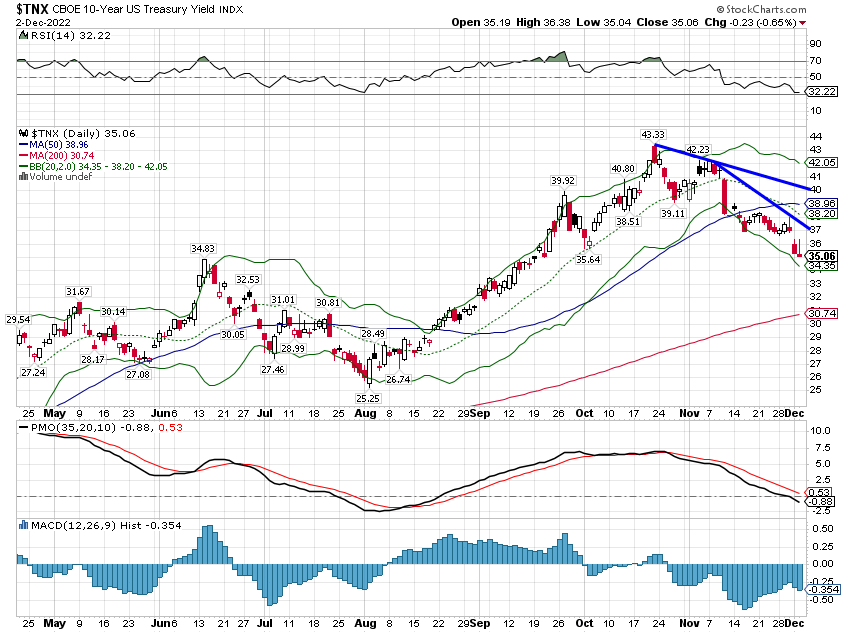

The 10-year Treasury yield’s short-term downtrend persists as well, the economic data continues to show moderating inflation and a slowing economy. The economy is slowing but it is interesting that the best indicators of that continue to be sentiment based. The Chicago PMI printed at 37.2, a level that has only been seen in previous recessions. Consumer confidence was also less than expected and the expectations component was less than 80, a level the Conference Board says “suggests the likelihood of a recession remains elevated.” The ISM manufacturing survey fell below 50 as well. At 49 the index is only slightly above the level ISM associates with recession (48.7).

The hard data, by contrast, remains pretty strong with personal income and spending both better than expected and well above the inflation rate, the employment data better than expected, jobless claims still low, job openings down but still elevated while house prices and core PCE prices were better than expected. Construction spending was down as were pending home sales in about the least surprising reports of the week.

None of that is to say that the US economy is trending in the right direction. Sentiment does often lead the hard data so we are probably still heading for recession sometime next year. But it is interesting that a lot of the sentiment data is at levels we associate with market bottoms. The Chicago PMI, for instance, hit its low in the 2008 recession in March of 2009, the very month the stock market hit bottom. Maybe it has more to fall but with the index at 37 I ask you: is today’s economy in any way as bad as it was in the closing months of 2008? I certainly don’t think so.

Of more importance to me is the drop last week in the 10-year TIPS yield, which fell 28 basis points on the week and closed at 1.08%. That yield was 1.74% as recently as a month ago and represents a large drop in real growth expectations in a very short period of time. The 5-year TIPS yield has fallen from 1.92% at the end of September to 1.16% today. You might also notice that means the TIPS curve is now inverted like most every other yield curve.

Having said that, we aren’t quite ready to extend the duration of our bond portfolio and bet on a near-term recession. Bonds have come off their lows very strongly but like everything else these days has probably moved too far, too fast. We extended duration once this year already – too early it turned out – and will likely do so again, but for now, I’m content to sit with our intermediate duration and wait for bonds to pull back from their overbought condition. I am always loathe to chase markets that have moved up or down quickly. Markets tend to moderate unless there is some kind of crisis (which I don’t think there is right now but potential fallout from crypto is starting to worry me).

(Click on image to enlarge)

Markets

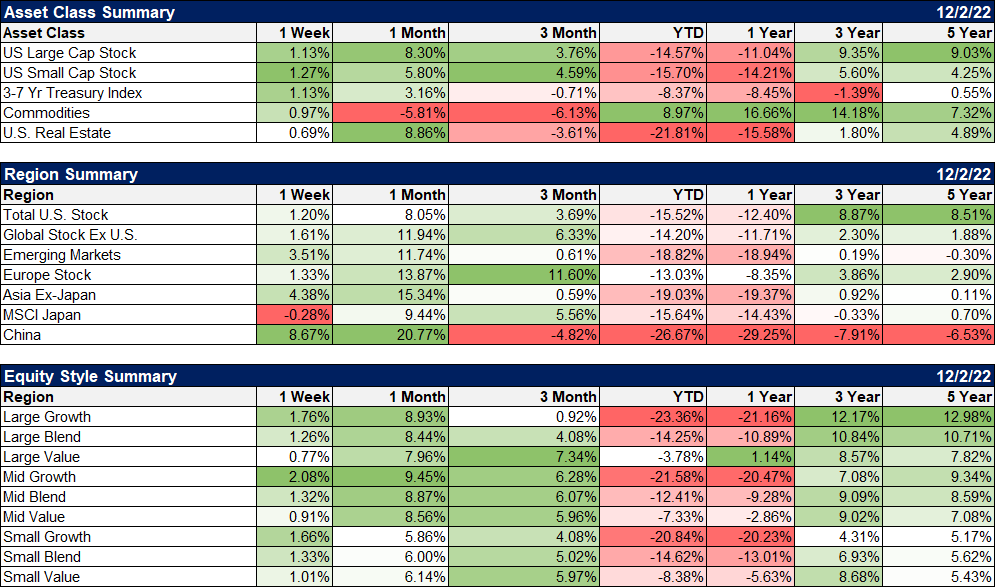

Will wonders never cease? Stocks, bonds, real estate, and commodities were all up last week, the first clean sweep in quite a while. That came despite a 1.5% drop Monday and a rough start to Friday after the employment report. The stock market has been very resilient lately with almost every downtick finding a buyer. Sentiment has, in my opinion, gotten a little too bullish in the short term and while everyone else is looking for Santa Claus and his rally, I’m watching for the Grinch.

Our portfolios had a good week, obviously, with all the asset classes in our portfolios higher. Our moderate risk portfolios were up a tad less than 1% on the week. Having an allocation to gold (+2.5%) and international value (+1.3%) helped to offset the underperformance of US value.

Globally, EM stocks, with a large allocation to China, were the big outperformers. That isn’t surprising with the weak dollar but it may prove fleeting if the dollar isn’t actually entering a sustained downtrend. EM ex-China also outperformed last week (+1.6%) but not as much. Latin America had a very good week, up 4.5%.

(Click on image to enlarge)

Cyclicals did well last week but so did most everything. The biggest underperformer was energy which fell despite a rally in crude oil for the week. I think we are finally getting the pullback I’ve been looking for. I think a 15% correction would be perfectly normal and healthy. We’ll see how the market reacts to the non-action of OPEC + over the weekend.

(Click on image to enlarge)

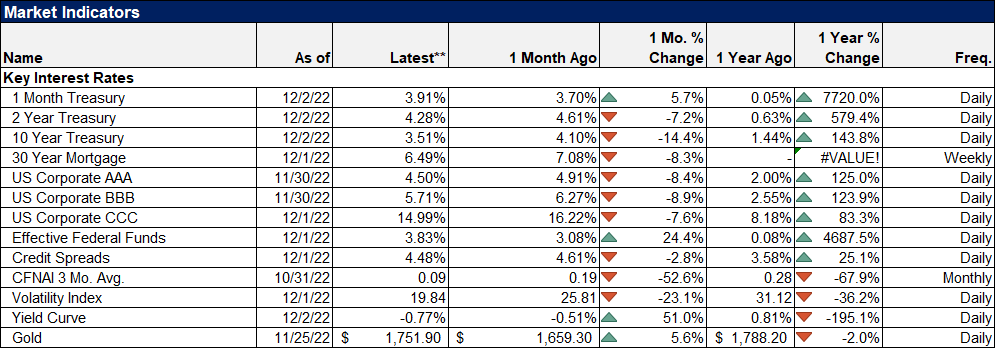

Mortgage rates were down again last week but the spread over the 10-year is still high at about 2.8%.

Credit spreads also continue to narrow, one of the few recession indicators still not pointing in that direction. The move up in gold (not fully reflected in this chart; gold close at $1809.60) is consistent with falling 10-year TIPS yields.

(Click on image to enlarge)

I don’t know if others think about markets as I do but I do know that the Keynesian beauty contest is valid. It has been tested more than once using real people and second and third-level thinkers consistently produce more accurate results. I find the exercise useful but it does have its limitations, namely that it is impossible to know what other people are thinking when they do the things they do. But I have been at this for a long time and I can tell you with certainty that knowledge of the yield curve is more widespread today than it has ever been. And that worrying about things that everyone else is already worried about is not usually a good use of my time.

In seeking to offset my optimistic bias, I assume we will have a recession as the yield curve predicts. But the yield curve doesn’t say anything about when the recession will hit or how deep it might be. I have heard a lot of people opine recently, myself included, that it would be unprecedented for the stock market to bottom before the recession even arrived. But if that is how things turn out, I won’t be surprised one bit. Remember the Dogs of the Dow.

No one knows what the future holds, certainly not me. But we can all remember the Delphic Maxims and try to be better investors. That’s what I try to do every day.

More By This Author:

Market Currents: Outlook On Commodities And Gold

Weekly Market Pulse: Currency Illusion

Market Currents: Why Pick Stocks?

Disclosure: This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any ...

more