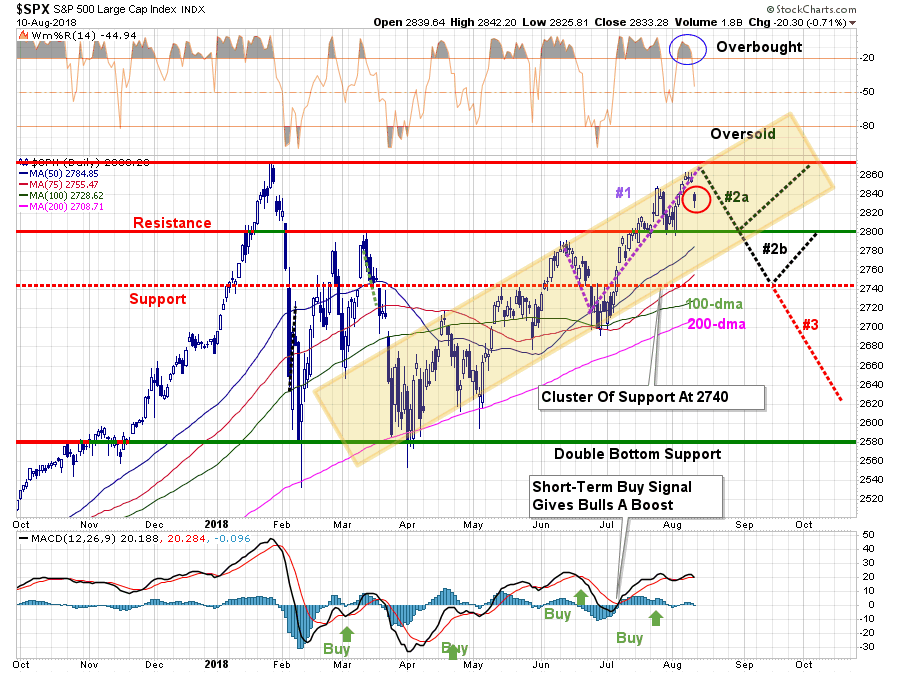

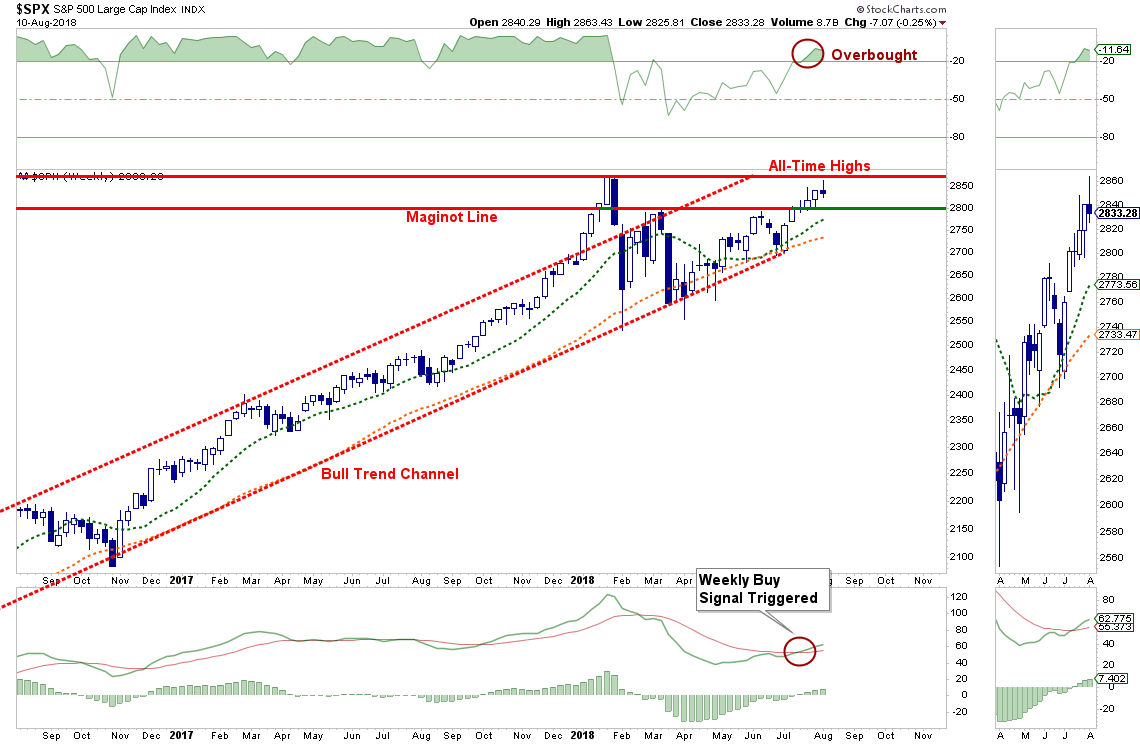

The Run Ends At The Highs

It always fascinates me how technical analysis is, more often than not, confirmed by some event. As I noted in last week’s missive:

“Currently, the ‘bulls’ remain clearly in charge of the market…for now. While it seems as if much of the ‘tariff talk’ has been priced into stocks, what likely hasn’t, as of yet, is the rising evidence of weakening economic data (ISM, employment, etc.), weakening consumer demand, and the impact of higher rates.

While on an intermediate-term basis these macro issues will matter, it is primarily just sentiment that matters in the short-term. From that perspective, the market retested the previous breakout above the March highs last week (the Maginot line) which keeps Pathway #1 intact. It also suggests that next week will likely see a test of the January highs.”

“With moving averages rising, this shifts Pathway #2a and #2b further out into the August and September time frames. The potential for a correction back to support before a second attempt at all-time highs would align with normal seasonal weakness heading into the Fall.”

As shown in the updated “pathway chart” above, the market did indeed attempt to test all-time highs in the market. But, as I noted, the overbought condition provided the fuel for a correction given the right catalyst.

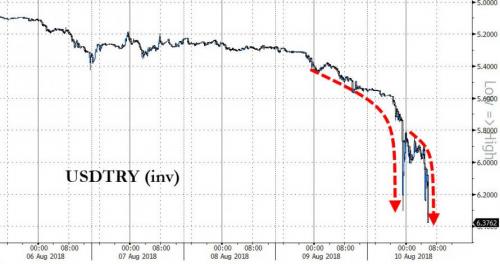

That catalyst appeared on Friday as the Lira plunged and Turkey edged closer to an economic crisis. As Daniel LaCalle noted:

“The Turkish Lira collapse should have surprised no one. Yet, in this bubble-justifying market, it did.”

“First and foremost, the lira decline has been ongoing for some time, and has nothing to do with the strength of the US dollar in 2018

The collapse of Turkey was an accident waiting to happen and is fully self-inflicted.”

We will come back to Turkey in a moment, but the important point here is with the market overbought, and extended following the recent run, we have been suggesting that holding onto cash in the short-term may be wise. As noted last week:

“With our portfolios nearly fully allocated, there are not a lot of actions we need to take currently as the markets continue to trend higher for now. We will continue to monitor our exposure and hedge risk accordingly, but with the weekly ‘buy signal’ registered, we are keeping our hedges limited and are widening our stops just a bit.

As noted above, a short-term correction is needed before adding further equity exposure to portfolios.”

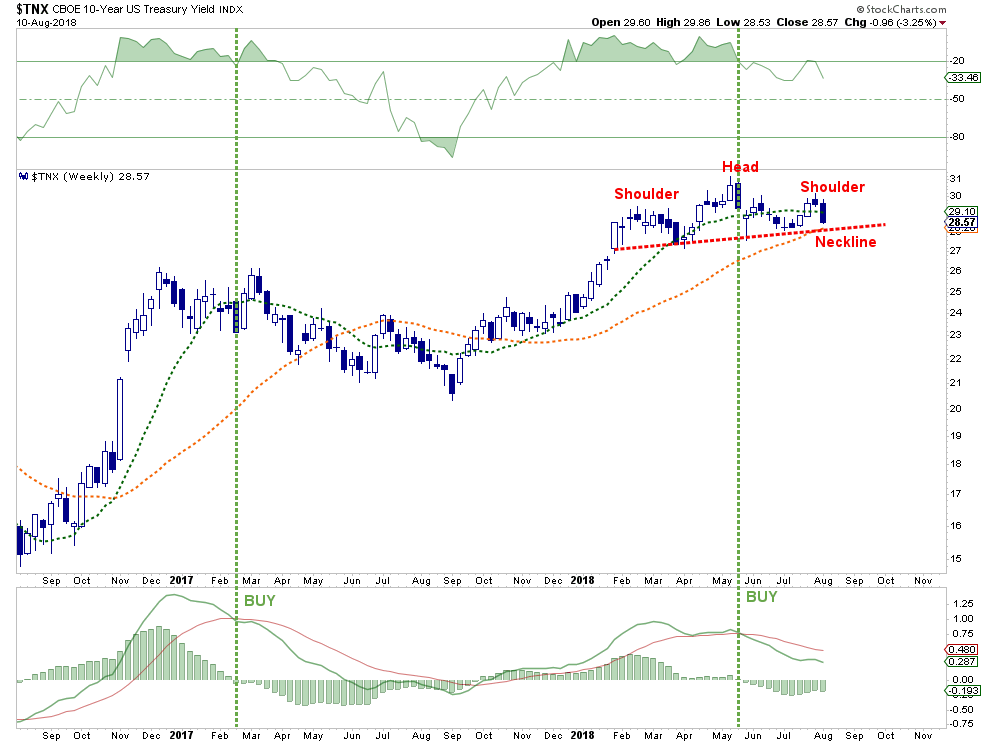

Also, last Tuesday, I discussed the bond yields were potentially signaling a problem for the market.

“On a very short-term basis, the 10-year Treasury yield has started a potential-topping process. Given that ‘yield’ is the inverse of the ‘price’ of bonds, the ‘buy’ and “sell” signals are also reversed.

As shown below, the 10-year yield appears to be forming the ‘right shoulder’ of a ‘head and shoulder’ topping formation and is currently on a short-term ‘buy’ signal. Such would suggest lower yields over the next couple of months.”

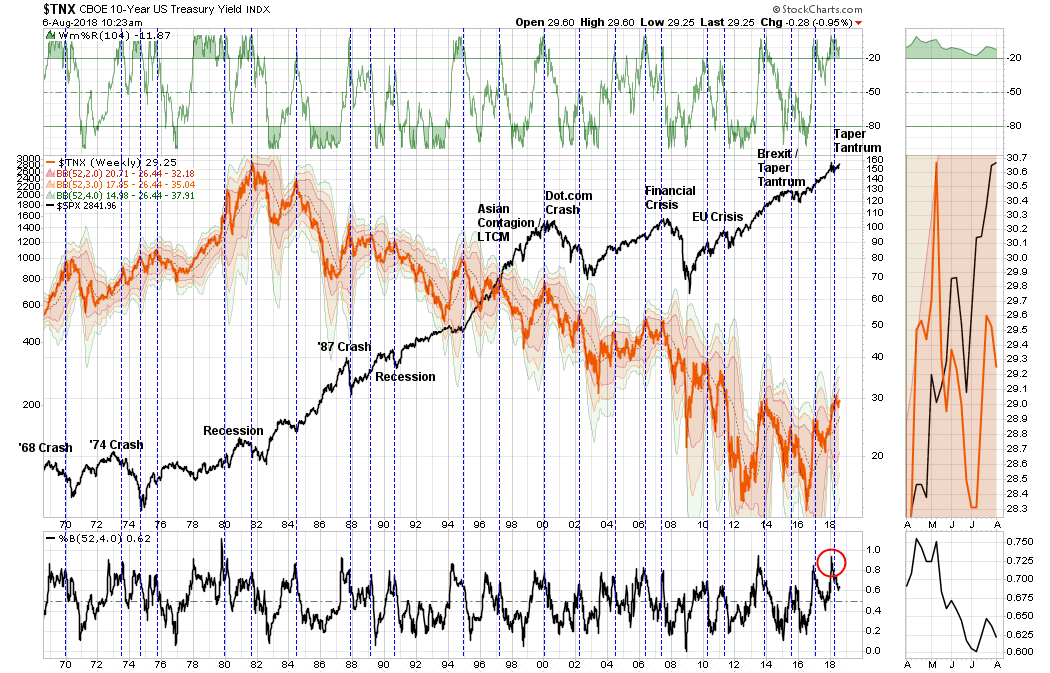

“The two ‘bond buy; signals above aren’t a rarity. The chart below expands this view back to 1970. There have only been a few times historically that yields have been this overbought and trading at 3 to 4 standard deviations above their one-year average.”

“The outcome for investors was never ideal.”

Now, back to Turkey.

Over the last couple of weeks, I have been repeatedly discussing the importance of rising geopolitical stresses from Iran, to Russia, China, and now Turkey. The common thread to all of these can be traced back to the current Administration and the fiscal policies currently being implemented.

While “tariffs” and an ongoing “trade war” have been largely dismissed in recent weeks in the exuberance to push the financial markets to all-time highs, the economic realities of higher interest rates, rising input costs from tariffs, economic impacts from sanctions, and tighter global liquidity are not a healthy mix for the economy or the markets.

Turkey is a far more relevant risk to the global economy than Greece was. As Daniel notes:

“On one hand, the exposure of eurozone banks like BBVA, BNP, Unicredit to Turkey is very relevant.Between 15% and 20% of all assets.

On the other hand, the rise in non-performing loans is evident. Turkey’s loans in US dollars account for around 30% of GDP according to the Washington Post, but loans in euro could be as much as another 20%. Turkey’s lenders and governments made the same incorrect bet that Argentina or Brazil made. Betting on a constantly weakening US dollar and that the Federal Reserve would not raise rates as announced. They were -obviously wrong. But that erroneous bet only adds to the already existing monetary and fiscal imbalances.”

Not bailing out Turkey,on the other hand, would cause amuch larger crisis than Greece was.”

A Risk Without A Backstop

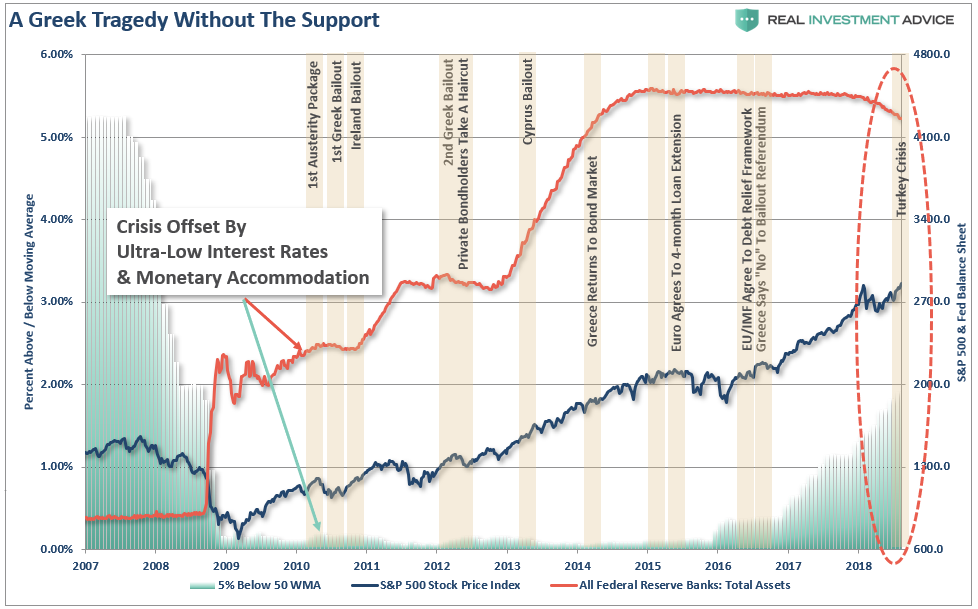

While many will likely quickly compare the current “Turkey Tragedy” with “Greece” and deem it to be a “non-event,” there is one difference you may want to pay attention to.

During the entirety of the Greek, Ireland, and Cyprus economic disasters, not to mention Brexit, the Federal Reserve was hard at work suppressing interest rates and pushing an unprecedented amount of liquidity into the financial markets. Not only was the Fed fast at work, but was joined by the Central Banks of Europe, China, Japan, and England. The chart below shows the timeline of the Greek crisis as compared to the S&P 500 and the Fed’s balance sheet.

Not surprisingly, corrections in the market were quickly arrested as floods of liquidity, and assurances from the Fed of ongoing accommodative support, kept Wall Street in coordinated play.

Today, the world is vastly different. As Turkey hits center stage with its current economic and debt crisis, the Fed is hard at work reducing monetary accommodation and hiking interest rates. Japan, China, and the ECB have all signaled they too are beginning to slow monetary interventions.

Without a safety net this time, the current crisis in Turkey may well reveal the fragility of the global financial system once again.

As always, it is the unexpected event which starts the chain reaction.

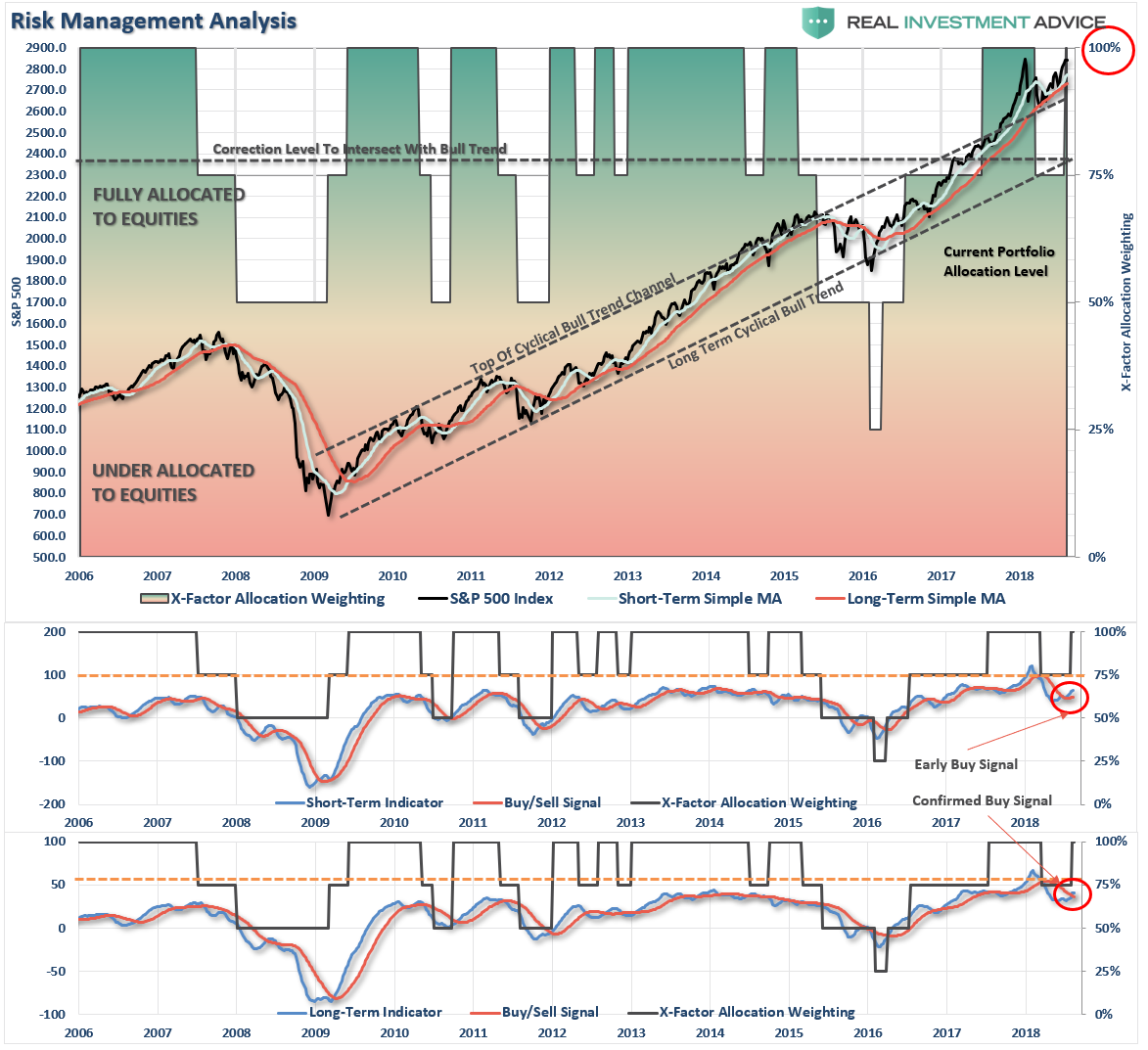

Weekly Buy Signal Update

As discussed last week, the weekly “buy signal” is in and is confirmed.

The EQUITY portion of the allocation is also adjusted based on current market risk. Earlier this year, the equity risk portion of the allocation model was reduced from 100% to 75% due to a triggering of a confirmed “sell” signal in mid-February.

We used the bounce into early March to “sell into” BEFORE lowering the allocation model to 75%.

Likewise, while we upgraded the “buy signal” last week, we suggested waiting for a correction back to previous support before increasing allocations further.

As a reminder, there are 4-primary indicators to the model:

- 1st signal – short-term warning signal. Only an alert to pay attention to portfolio risk.

- 2nd signal – reduce equity by 25%.

- 3rd signal – (Moving average cross-over) reduce equity by another 25%.

- 4th signal – (Trend change) – reduce equity by another 25% and short the market.

However, it is important to note these signals are based on “weekly” data and are intermediate-term in nature. Therefore, by the time these longer-term indicators are triggered, the very short-term conditions of the market are generally either very overbought, or oversold.

“While the model is being increased back to 100% of target, we will selectively add equity exposure during short-term corrective actions in the market.”

The drop in the market on Friday will likely continue into early next week. The most logical level of support currently is 2800 which will provide a better entry point to increase equity exposure. With the markets headed into two of the toughest months of the year, historically speaking, a bit of extra caution is advised when it comes to the amount of risk you are currently taking with your money.

Use weakness that does NOT violate support at 2800 to cautiously add exposure.

Investing is not a competition. It is a game won through patience, diligence and risk avoidance.

A Quick Trip Through History

By Doug Kass

“A bull market is like sex. It feels best just before it ends.” – Warren Buffett

Today it can be argued that the stock market is as uncritically loved (with the S&P Index at an elevated 2850) as it was unreasonably loathed nearly nine and a half years ago (with the S&P Index at a horrifying 666).

Investors are prone to be bullish at the end of a Bull Market when prices are high and bearish at the bottom of a Bear Market when prices are low – as speculation is a social activity carried on by herds and what I like to call “Group Stink.’

Since the mass of people have most of the money, the crowd is more often than not on the winning team.

However, when the majority is confident in view, are all on the same side of the boat and have fully discounted a profitable future (“first level” v. “second level” thinking) —Mr. Market becomes vulnerable to a surprise as markets become exposed to the unexpected. We may imagine the financial future, but it can never be surely known.

We know the past and the present and, at times (and perhaps too often) we project the familiar out into the unknown. At inflection points, this act of projecting the familiar frequently produces unsatisfactory results.

History teaches us investment lessons but it doesn’t tell us which lessons to apply and when.

As Howard Marks writes,

“The markets are a classroom where lessons are taught every day. The keys to investment success lie in observing and learning.”

I have observed that, at the end of every Bull Market, progress is blurred and becomes fantasy. A new Utopianism dominates financial thinking and the consensus is swayed towards the notion of a long and uninterrupted economic and profit boom – world without risk.

(Who can ever forget Peter Schwarz’s and Peter Leyden’s, Wired Magazine (1997) article, ” The Long Boom: A History of the Future, 1980-2020?)

Markets tend to make opinions. There is a strong inclination and nature to extrapolate as “group stink“ is the favorite market odor. Or as The Divine Ms M regularly writes,

“There is nothing like price to change sentiment.”

We are nearly a decade into an economic recovery and Bull Market. We must look for signposts – both fundamental (as I outline every morning in my Diary) and anecdotal.

Market tops come in all shapes and colors.

Perhaps the first stock market crash (Kipper und Wipper), occurred in 1623. It was caused by fraudulent foreign coins minted in the Holy Roman Empire for the purpose of raising funds at the start of the Thirty Years War.

Fourteen years later it was the Tulip Mania Bubble in the Netherlands during which contracts for bulbs of tulips reached extraordinarily high prices (which suddenly collapsed).

A century later, in The Mississippi Bubble, Banque Royale by John Law stopped payments of its note in exchange for specie and as a result caused an economic collapse in France.

The South Sea Bubble of 1720 affected early European stock markets during the early days of chartered joint stock companies.

Fast forward to The Panic of 1901 which lasted three years and was sparked by the assassination of President McKinley to be followed by a severe drought.

Six years later a panic followed President Roosevelt’s attack on the railroad monopolies (think Alphabet’s Google (GOOGL) and Amazon (AMZN) ).

Over history, and as we have moved towards an increasingly flat and interconnected world, the dominoes of currency have had broad economic and investment ramifications – becoming ever more influential contributors to possible stock market panic in a U.S. dollar debt-denominated world. (See the recent collapse of Russian and Turkish currencies, as an example, of modern day risks).

Consider some other, more recent warning signs in history that produced market tops:

- A failed leveraged buyout of (UAL) led to a stock market plunge in 1989 (undermined future leveraged deals).

- The Russian Debt Crisis in 1998 happened when the ruble was devalued and Russia defaulted on its debt.

- The ill-fated Time Warner/AOL combination closed minutes before the Nasdaq top in 2000. (Ultimately the OTC market fell by -81% in the next few years).

- Goldman Sachs’ 2007 Abacus CDO deal preceded the mortgage derivative fiasco that led to the Great Recession.

Maybe this market top, too, will be caused by the unexpected – choreographed by a modern day P. T. Barnum, an ostrobogulous Elon Musk and his sui generis automobile.

“There’s a sucker born every minute.” – P.T. Barnum

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

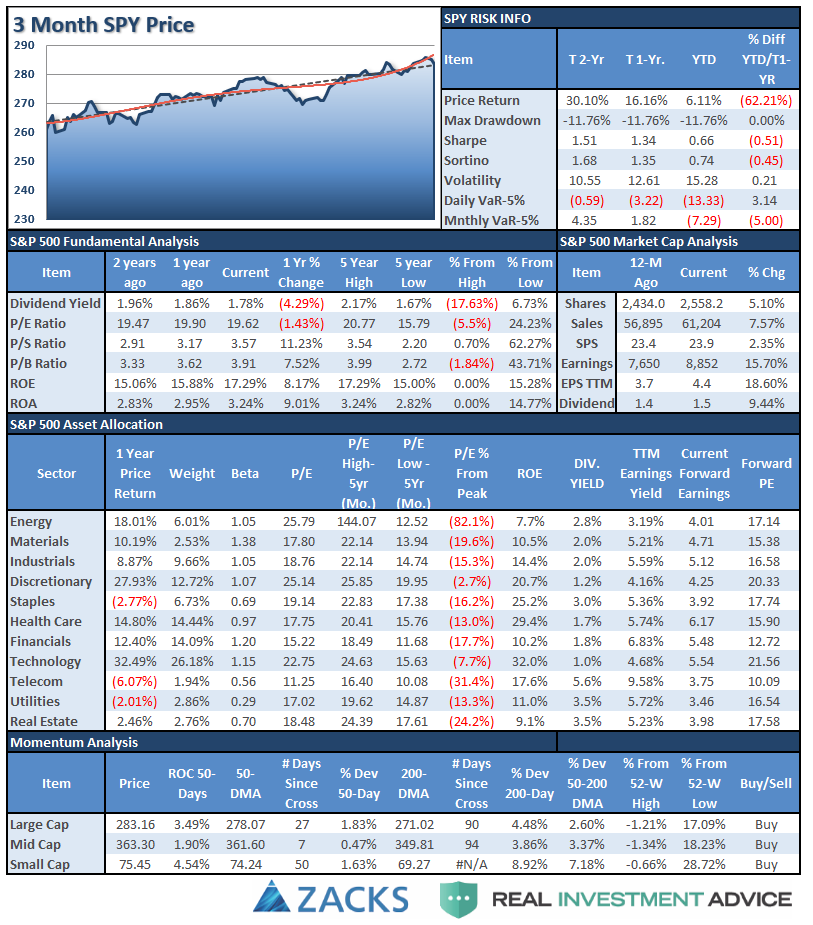

S&P 500 Tear Sheet

Performance Analysis

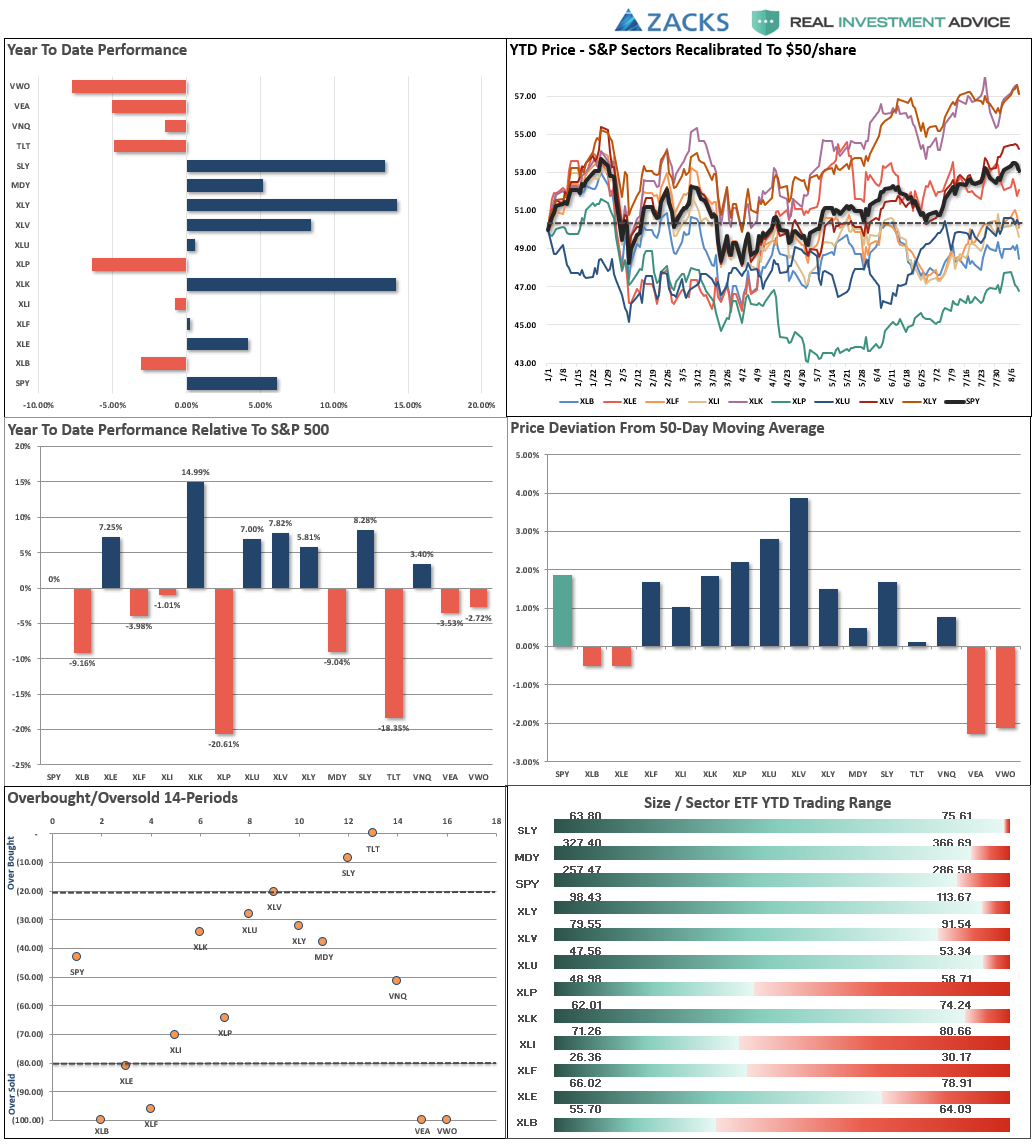

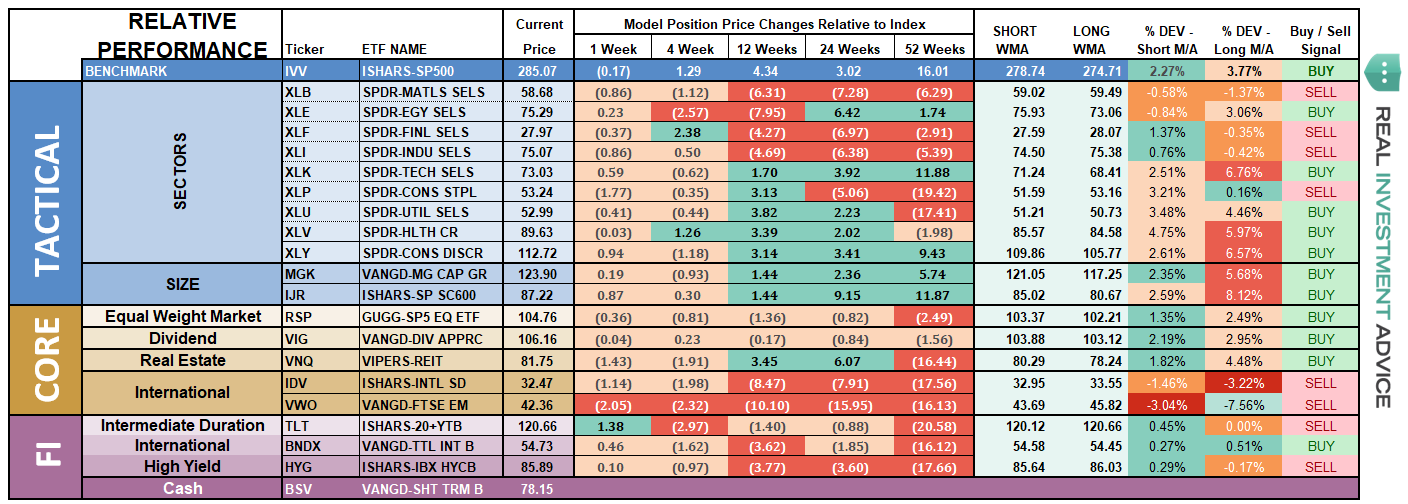

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Discretionary and Technology – Last week we said that after taking profits in Technology, look for a correction back to support. The same goes for discretionary holdings as well. After a brief push to all-time highs, these market leaders are extremely overbought and exhausted. Take some profits and watch for a short-term correction back to support. The trends for both remain very bullish right now, and the pullback provides an opportunity to rebalance sector holdings back to target weights.

Healthcare, Staples, and Utilities – After a massive run in Healthcare stocks, take some profits and look for a pullback to support to add additional exposure if warranted. Likewise, Staples have been part of the sector rotation flow following a long period of underperformance. A pullback to the 50-dma will provide a decent opportunity to add exposure if needed. Utilities also continue to perform well here as money continues to rotate into previously “hated” sectors. Look for a correction back to the 50-dma as well to add exposure.

Financial, Energy, Industrial, and Material Industrials and Materials continue to be weighed upon by the ebbs and flows of a trade war. Given the unpredictability of “White House” policy, we have remained out of the sector for the time being until some certainty returns. While the trend for Energy remains in place, we remain market weight holdings due to lack of relative performance. After a brief spurt in financials, look for a pullback to the 200-dma to add exposure. Our overriding concern for banks continues to be the decline of the “yield curve.”

Small-Cap and Mid Cap continue to perform well as of late. We noted two weeks ago, that after small and mid-caps broke out of a multi-top trading range, we needed a pull-back to add further exposure. After having previously added exposure to these markets, we will look to add to current holdings on a pullback to support which holds.

Emerging and International Markets were removed in January from portfolios on the basis that “trade wars” and “rising rates” were not good for these groups. With the addition of the “Turkey Crisis,” ongoing tariffs, and trade wars, there is simply no reason to add “drag” to a portfolio currently. Cash is outperforming emerging and international markets currently.

Dividends and Equal weight continue to hold their own and we continue to hold our allocations to these “core holdings.” We will overweight these positions on a pullback to support that does not violate that level.

Gold – Despite the hopes for a resurgence in Gold, any sign of life has yet to occur as the “fear” of a stock market correction has all but disappeared. We have had NO gold exposure in portfolios since 2013 as there is no reason to add a “drag” on portfolio performance by holding declining or under performing assets.

However, if you are still hanging onto Gold we have been consistently providing stop loss levels and sell points since May of this year. These points have continued to decline. With gold very oversold on a short-term basis, if you are still long the metal, your stop has been lowered from $117 three weeks ago, to $114 this week. A rally sale point has also declined from the previous level of $121 to $117.

Bonds – This past week, bonds rallied sharply as money looked for “safety” amid the concerns of a collapse in the Turkish Lira. The rally last week establishes a series of rising bottoms for bonds and we are close to registering a very important “BUY” signal for bonds. As noted previously, we remain out of trading positions currently but remain long “core” bond holdings mostly in floating rate and shorter duration exposure. However, if we register a confirmed “buy” signal we will add trading positions back into portfolios.

REIT’s keep bouncing off the 50-dma like clockwork. Despite rising rates, the sector has continued to catch a share of money flows and the entire backdrop is bullish for REIT’s. However, with the sector very overbought, take profits and rebalance back to weight and look for pullbacks to support to add exposure.

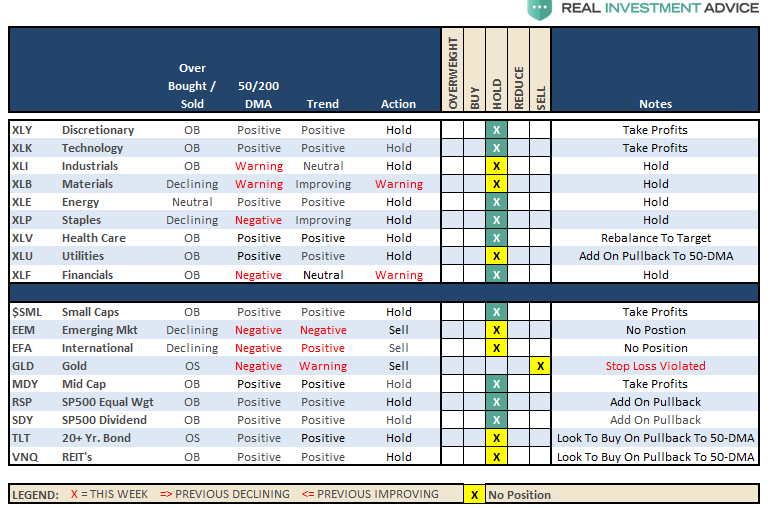

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

As I noted two weeks ago, the market’s improvement allowed us the ability to further increase equity exposure in portfolios in anticipation of registering a confirmed buy signal. However, given that August and September are historically weak months for the market, we will remain a bit more cautious on the how and when we increase holdings in our models.

The cluster of support at the 50- and 100-dma remains in place which limits much of the downside risk currently. But the current pullback to previous support at 2800 will likely provide an opportunity to add further exposure and bring portfolios closer to target model weights.

We will be looking to take the following actions on the next opportunity in the market.

- New clients: Add 50% of target equity allocations.

- Equity Model: Increase equity holdings to full weights.

- Equity/ETF blended – increase equity holdings to full weight and overweight domestic ETF “core holdings” to offset lack of international exposure.

- ETF Model: Overweight core “domestic” indices to offset lack of international exposure. Overweight outperforming sectors to offset underweights in under performing sectors.

- Option-Wrapped Equity Model bring all position to target weights and add “collars” opportunistically.

Again, we are moving cautiously. There is mounting evidence of short to intermediate-term risk that we are very aware of. However, the trend of the market remains positive and we realize that short-term performance is just as important as long-term. It is always a challenge to marry both.

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these action either by reducing, selling, or hedging, if the market environment changes for the worse.

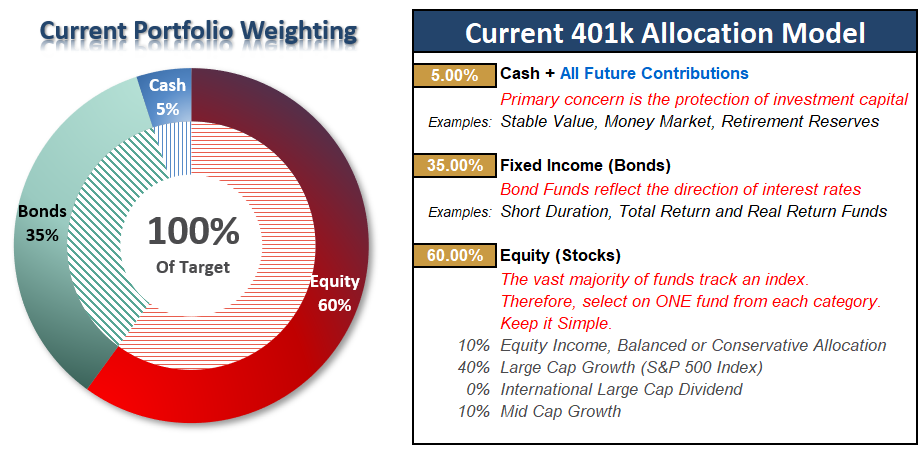

THE REAL 401k PLAN MANAGER

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Wait For It….

As I discussed last week:

“The market did trigger a weekly confirmed ‘buy’ two week’s ago as we previously discussed. However, as noted in the main part of missive above, by the time these signals occur the market has generally gotten either overbought or oversold in the short-term.”

That “overbought” condition usually provides a better opportunity in the near-term to increase exposure in portfolios if you remain patient. The pullback on Friday is providing that opportunity.

I suspect that next week could see some more weakness given the previous overbought condition combined with concerns over Turkey.

While there is “no requirement” to make immediate adjustments to your 401k plan, you should balance your portfolio to your personal level of risk tolerance, you can use a pullback to support to continue taking the following actions we discussed previously.

- If you are overweight equities – reduce international and emerging market exposure and add to domestic exposure if needed to bring portfolios in line to target weights.

- If you are underweight equities – begin increasing exposure towards domestic equity in small steps. (1/3 of what is required to reach target allocations.)

- If you are at target equity allocations currently just rebalance weights to focus on domestic holdings.

While will officially upgraded our allocation model back to 100% exposure, there is no rush in immediately adding additional equity risk. Do so opportunistically.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more

Lance, Lance, Lance, with so much in the middle of your article about how fragile the market is, how the Fed (and other central banks) will not be there to provide support if something goes wrong, and how much contagion possibility exists with the Turkish lira crisis, why on earth would you be counseling clients to cautiously move up to full 100% equity exposure -- especially in an article with the giveaway title "The Run Ends at the Highs." Here we are moving back to an all-time high at at time with all the fragility you describe, and you're counseling investors to buy in more??? --David Haggith The Great Recession Blog