Higher Volatility Ahead

In our analyses, we regularly examine current movements, identify possible influencing factors, and assess the general market situation. However, these are not recommendations, but merely opinions and food for thought.

We are just a few days away from the election of the new US president – or US president. Of course, the outcome will have a major impact on the financial markets.

The financial markets work with expectations. No investor invests in the past, but only in the future – which is what expectations are. So it is obvious that the majority of investors represented on Wall Street are tipping for one favorite – or are already aligning their investments with the potential policies of the expected new US president. According to Wall Street, the winner of the US elections seems to be Donald Trump, which is also confirmed by most market observers in the media. According to Polymarket.com, he is currently leading by exactly two-thirds to one-third.

However, November 5 may not be as relevant for Wall Street as many expect. Should Trump actually win, the day's events are likely to return very quickly. Kamala Harris is likely to be the cause of two reasons for higher volatility. Investors would have to adjust their investment bets – in addition to the possible change in rhetoric from the Fed.

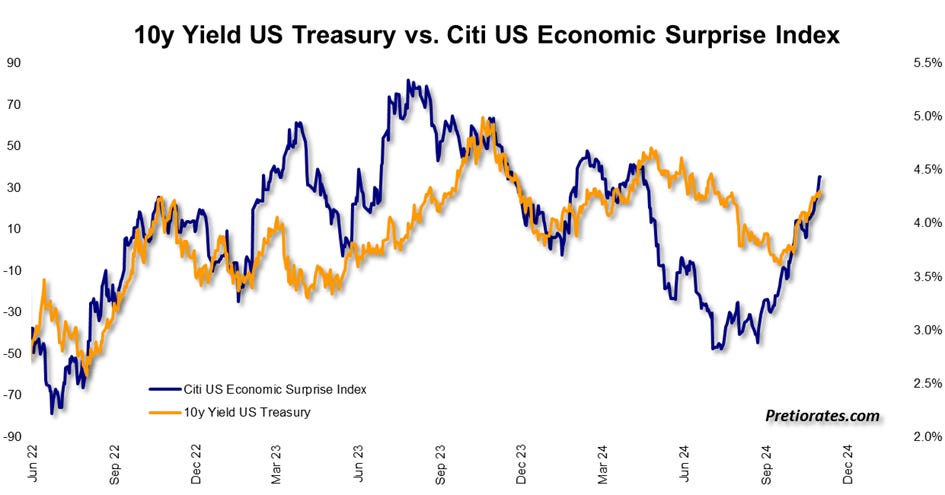

The US economy seems to continue to perform better than the majority of investors had expected. The Citi US Economic Surprise Index rose again in recent days, maintaining upward pressure on US market yields...

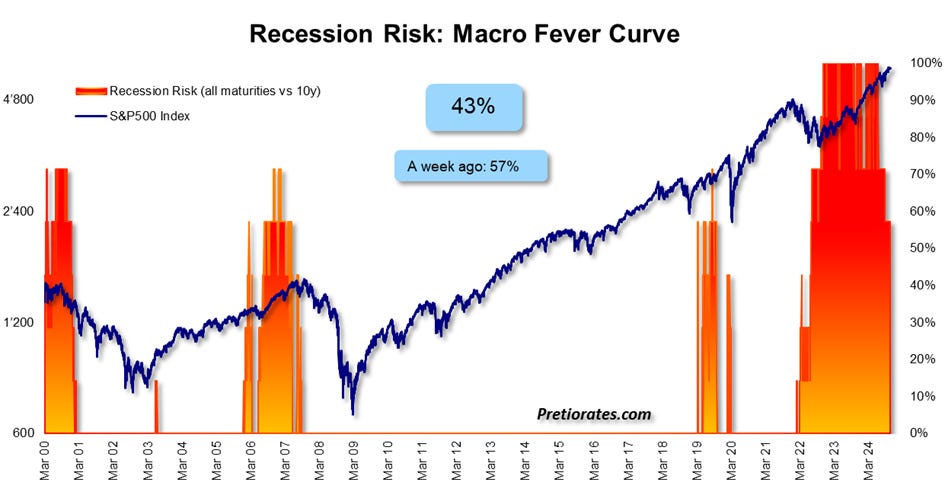

In fact, the risk of a US recession has also fallen from 57% to 43% over the past week.

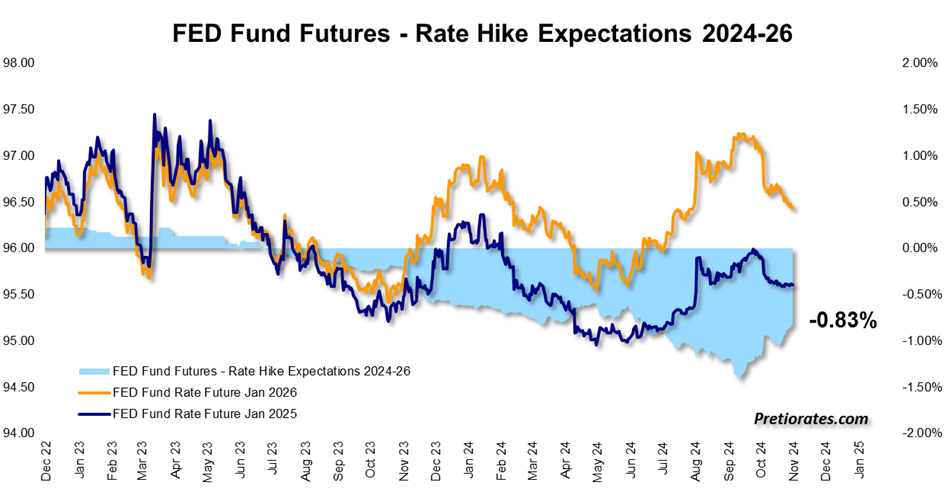

The Fed should be pleased about this, but is therefore more likely to have to deal with higher interest rates - in order to slow down the economy. Hopes of lower interest rates are therefore continuing to fade, as can also be seen in the futures: After interest rate cuts of 1.50 % were expected by the end of 2025 as recently as September, the figure is currently 83 basis points...

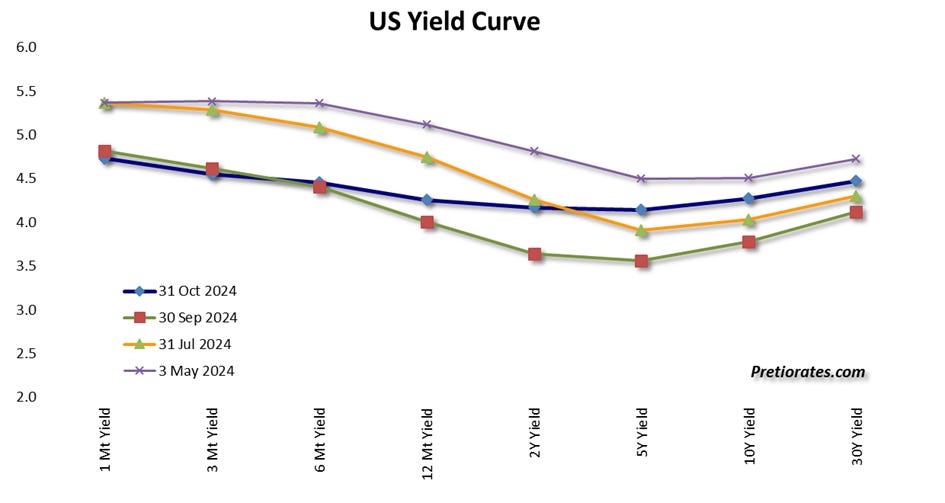

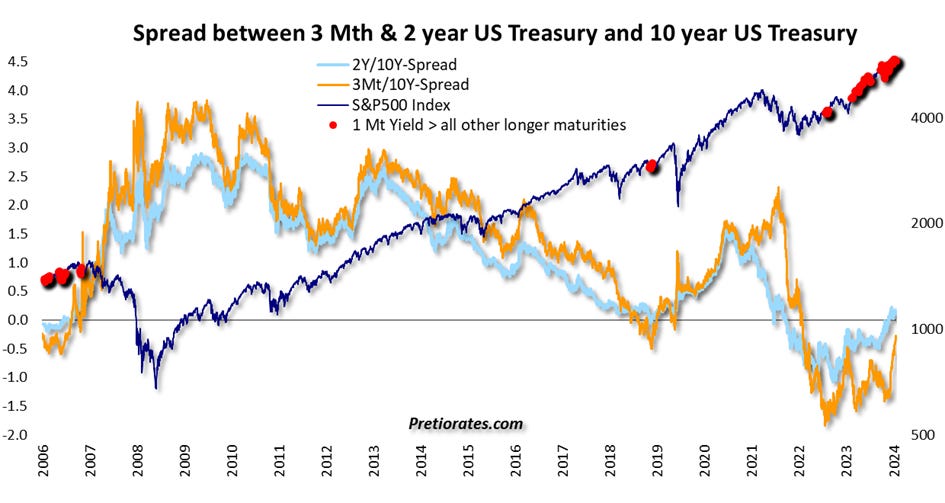

This can also be seen in the yield curve... The maturities over 2 and 5 years in particular have reached a significantly higher level since September (green line)...

The market likes to compare the yield between the two maturities over two and ten years (light blue line). If the 10-year yield is lower than the 2-year yield, this has often indicated a recession in the past. In fact, this has been the case over the past two years - without a recession occurring to date.

However, the Fed is increasingly tracking the correlation of maturities over three months and ten years (orange line). And there has been a lot of action on this line over the past few days: from a level clearly in negative territory, it has risen massively towards the positive zone. This movement could mean that the US Federal Reserve is now also scaling back its fear of a recession - and thus its rhetoric for further interest rate cuts.

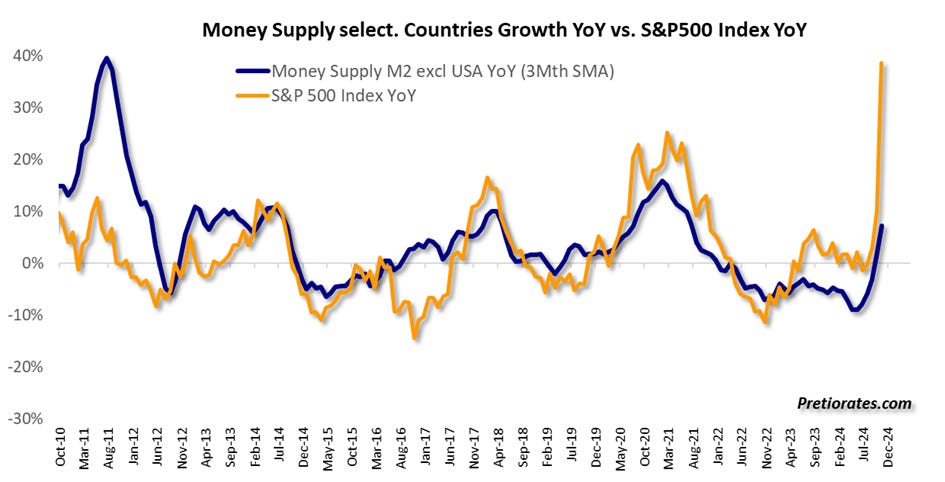

Lower hopes for lower interest rates are unlikely to please the stock market. Lower interest rates result in higher liquidity (money supply), which is positive for the development of share prices. The opposite is the case if interest rates do not fall. This is clearly shown by the high correlation in the following chart. And the problem here is that the stock market has already realized a great deal of advance praise with higher share prices. Correction potential???

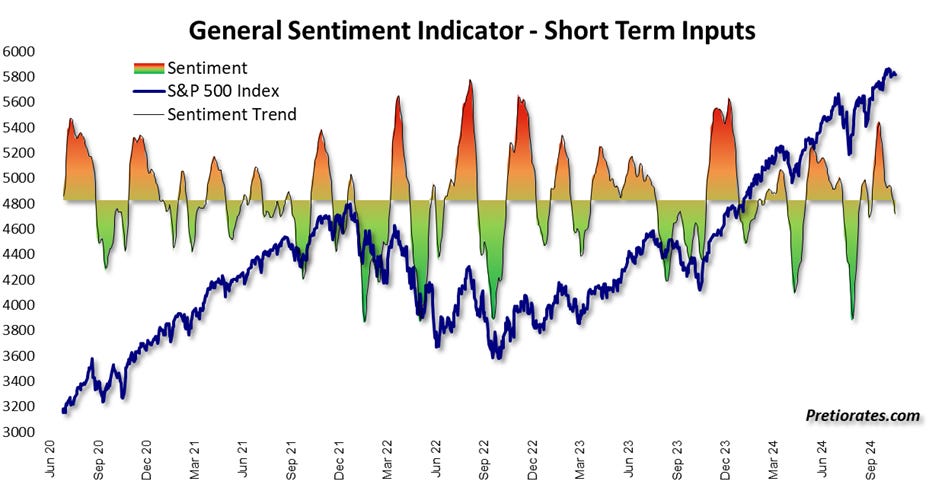

This can already be seen in the sentiment (of the short-term inputs), which recently fell from very bullish back into the negative zone. This development is often accompanied by the start of corrective phases on Wall Street...

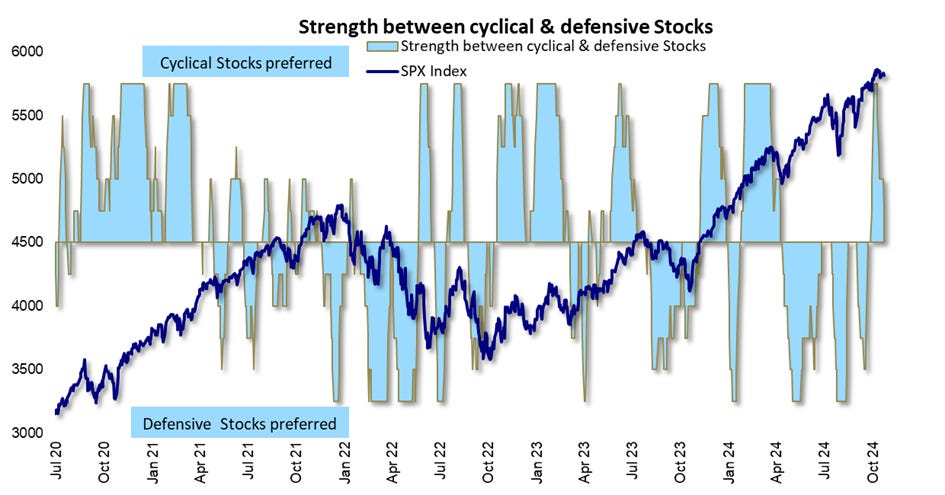

Investors are also already reacting to the fact that shares in cyclical companies are less popular. Typical of a more cautious attitude...

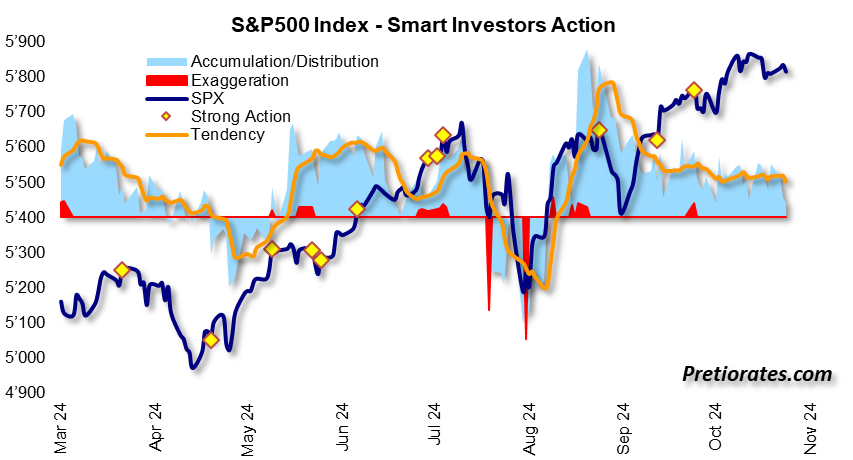

In the S&P500, on the other hand, accumulation is still taking place, albeit at a rather cautious level...

However, the mood seems to be shifting from optimism to pessimism...

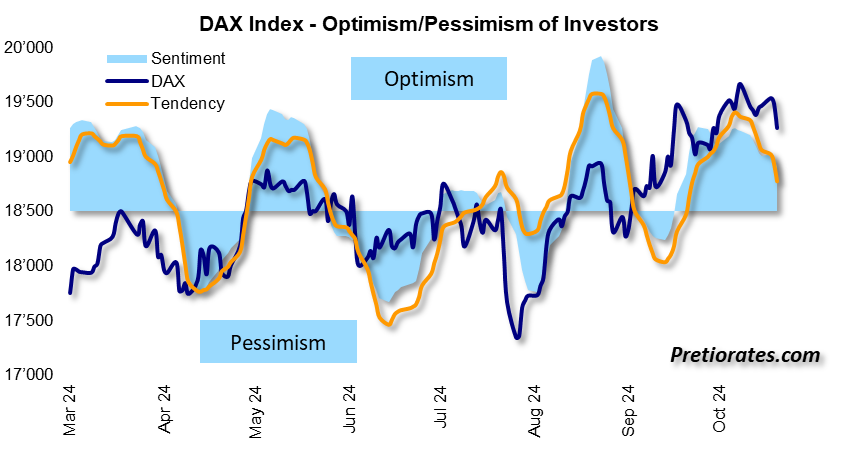

The same picture can be seen in the European market. What applies to the German DAX index can be seen in almost all other European indices: optimism is declining significantly...

A deterioration in sentiment could lie ahead. And the days after the election could play a decisive role in this. If, as expected, it is Donald Trump, the “buy the rumor, sell the fact” strategy is likely to come into play. However, if it is Kamala Harris, some of Wall Street's bets will have to be offset. Higher volatility therefore seems almost guaranteed.

That’s it for today!

And don’t forget to recommend us - with the button below.

Remember, we are not making any recommendations for investments, we are just giving you ideas for your own analysis and decisions! Do your own due dilligence!

We wish you successful investments!

More By This Author:

Are Hopes Of Lower Interest Rates Still Alive?

Believe It Or Not, The Euphoria In The Precious Metals Market Is Still Too Low

Inflation Seems To Be Dying, But It Is Not Dead

Disclaimer: The information & opinions published by Pretiorates.com or "Pretiorates Thoughts" are for information purposes only and do not constitute investment advice. They are solely ...

more