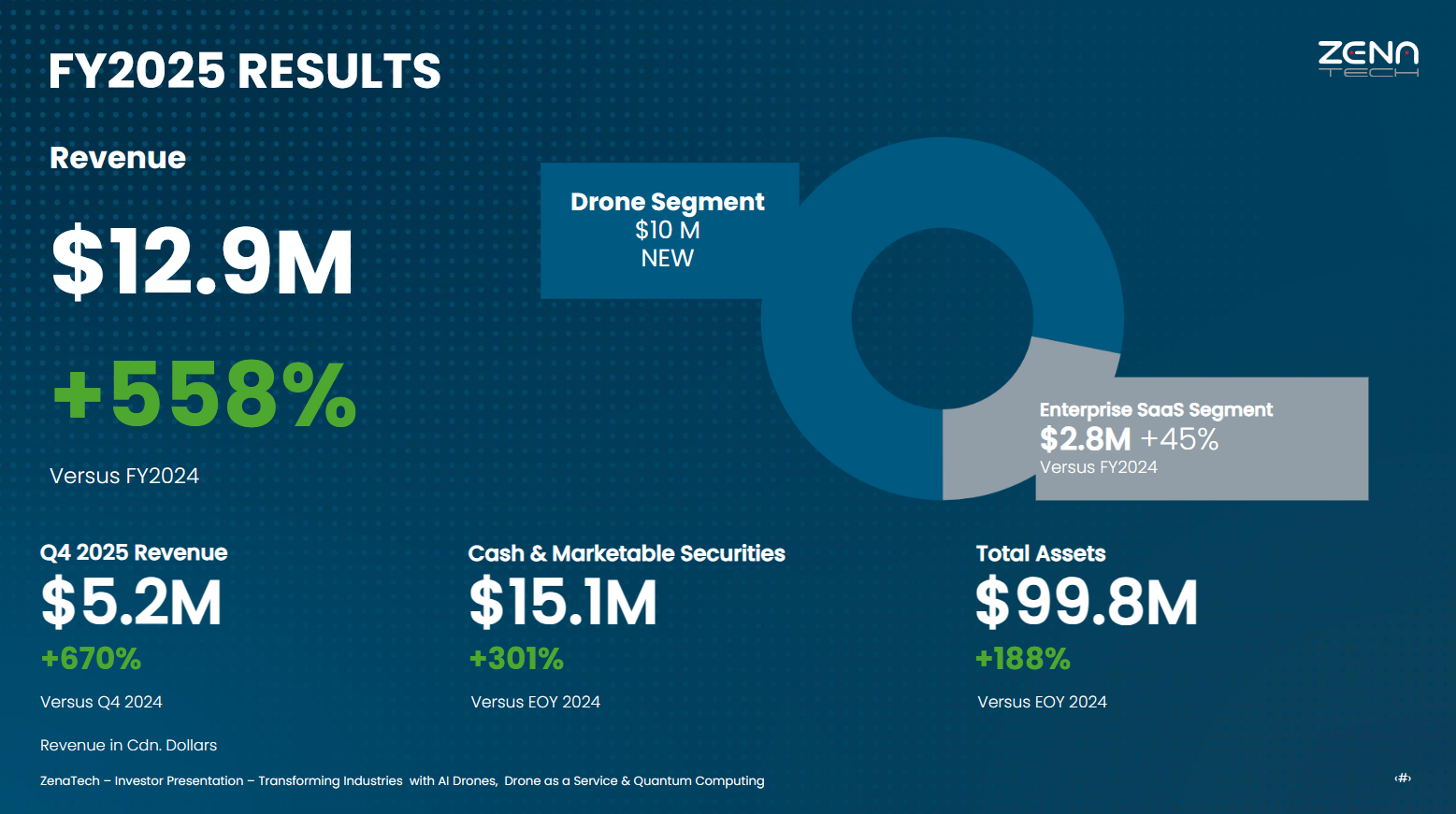

Zena Technologies (NASDAQ: ZENA) demonstrated in their annual filing that their rollup strategy of acquiring surveying business is working. They had record annual revenue of CAD$12.9 million and this was up 558% YoY and record quarterly revenue of CAD$5.2 million which was up 670% YoY. The company also segmented the revenue indicating that CAD$10.1 million came from Drone-as-a-Service (DaaS) and CAD$2.8 million came from the enterprise software segment. Maxim Group projected FY 2025 revenue of CAD$11.9 million and Q4 revenue of CAD$4.7 million. This was a sizable revenue beat and shows the underlying demand of DaaS and the strength of their rollup strategy.

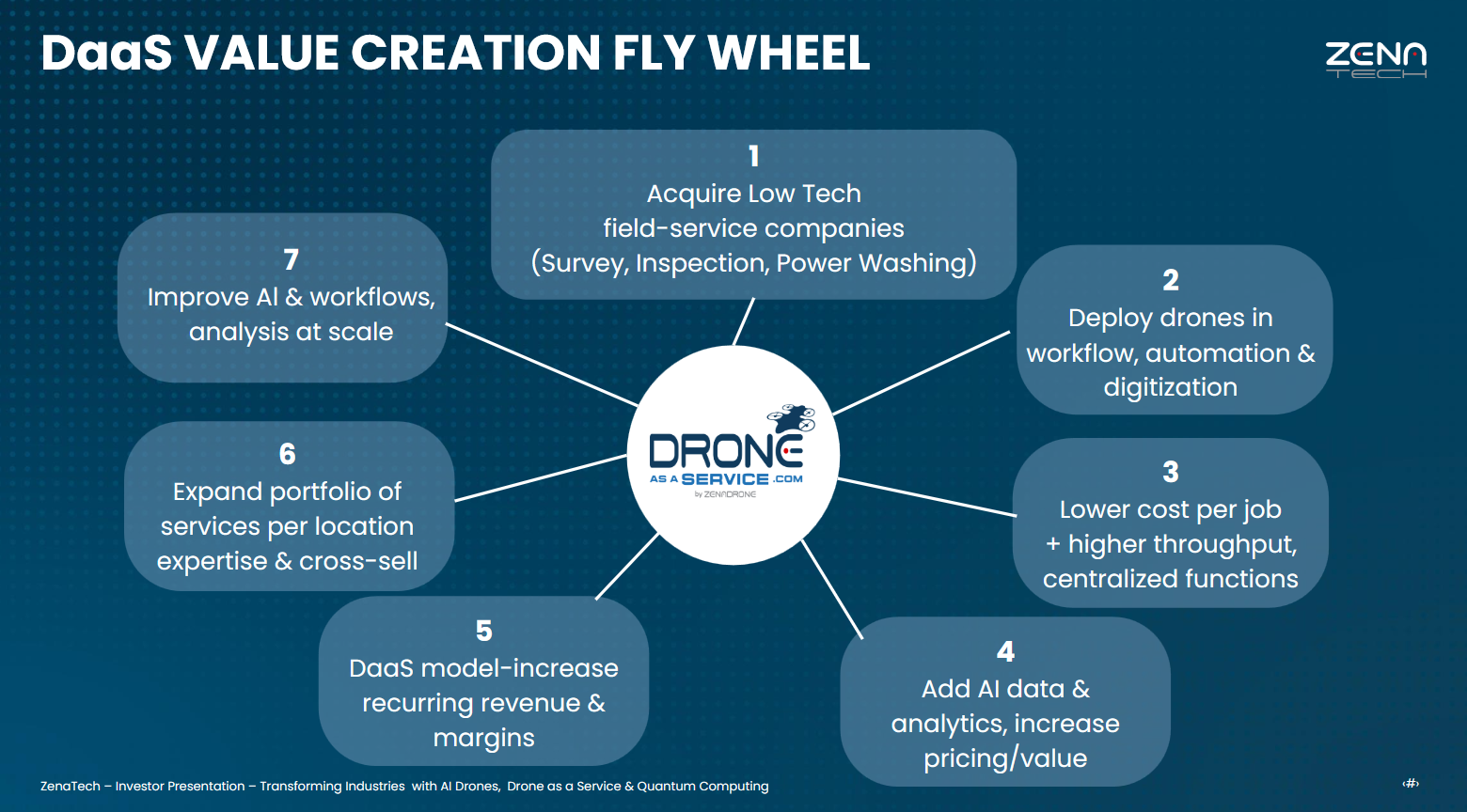

Genesis of the Drone-as-a-Service (DaaS) Business

ZENA started as a software and technology company, expanded into drones, and then identified an opportunity to create a Drone-as-a-Service market. The company is vertically integrated and uses its own ZenaDrones. Their DaaS strategy sells drone services to both business and government customers. Through their acquisitions, ZENA already serves county, municipal, and federal public-works customers, along with its existing land surveying customer base. Rather than selling or renting drones to these customers, the company provides turnkey DaaS. It transports the drones to the service site along with the technicians, the specialized software, and most importantly the technicians with the operational know-how, and regulatory coverage needed to complete the work.

According to Linda Montgomery, Vice President of Corporate Development and Investor Relations, the company is targeting under-digitized industries by delivering faster and better data with its own drones. Target applications include land surveys, powerline inspections, renewable-energy infrastructure inspection and maintenance, power washing, and precision agriculture. In this model, customers are buying outcomes rather than equipment, pilots, or software licenses. The model can be structured as an annual membership or subscription with usage-based fees, or as pay-per-use services, with the goal of building recurring revenue.

Land surveying is the first vertical, not the whole vision. The drone acts as a force multiplier for a licensed land surveyor by allowing one surveyor to complete the work faster. Think about land surveying situations in hilly or mountainous terrain where walking about is much slower than flying over. The productivity advantage is rooted more in speed and efficiency than in job-site safety. Safety becomes a stronger selling point in inspection and maintenance applications, where drones can reduce the need for workers to climb ladders or operate in hot, hazardous, or hard-to-access environments.

The Margin Story

Unfortunately there is no clean breakdown of the quarterly revenues or COGS from the annual report but we can estimate. Based on the historical percentage of revenue and accelerating revenue from DaaS the CAD$ 5.2 million breaks down to CAD$ 4.35 million for DaaS and CAD$ 0.85 million for SaaS.

The reason investors need to monitor DaaS gross margin is to ensure the acquisition strategy is working. ZENA is acquiring companies that are already profitable, but the strategy still depends on integrating drones into those businesses and improving margins. The acquisitions need to generate recurring revenue, steady cash flow, and expanding profitability so that operating cash flow can pay off seller notes over their three-year term. This latest quarter suggests the company is moving in that direction.

Balance Sheet Strength

More acquisitions are planned and their balance sheet strengthened. They have CAD$ 15.1 million in cash and marketable securities and that number is up 301% YoY. Their total assets are CAD$ 99.8 million. On May 7th they completed another acquisition in Australia that has 3 sites which really expanded its global footprint. The company also has advanced geospatial mapping and LiDAR-based data capture. LiDAR is 3D Laser scanning that creates point clouds that can create hyper-accurate 3D digital replicas of structures or even landscapes. Australia is mineral rich and this technology gives them a chance to start servicing mining, public works, and infrastructure sectors, but don’t discount their growing global presence and what this corporate know-how means.

Acquisitions take a period of time to work. ZENA acquired a cleaning and power-washing company, signed an LOI for another building-cleaning company, and acquired a cell-tower inspection, design, and maintenance business. ZENA estimated it takes about 6 months to integrate the company and get an operator up to speed on using the drone more efficiently which translates in higher revenue and profitability. These acquisitions show the bigger plan is to create a diversified DaaS platform across multiple service categories while centralizing back-office, data, and operational functions.

Defense and Government Contracts

Over the past 8 years ZENA had invested time and resources pursuing government contracts but the past 3 years investors have seen the tempo pickup. The first paid trials with the U.S. Air Force and Navy began around 2023, and the company is now engaging program managers within the Department of Defense and other defense agencies to secure demonstrations, pilot programs, and ultimately contracts. All this investment has positioned themselves to be at the right time and right place. In the near term, that effort appears focused on the inventory management drone and the ZenaDrone 1000 for specialized cargo missions such as medical supplies and blood transport.

The certification path has also evolved. Rather than describing Green UAS and Blue UAS as two fully separate sequential hurdles, it is more accurate to refer to a combined Green and Blue UAS certification pathway. Blue UAS remains the key milestone because it is required to access the Department of Defense procurement list, while Green UAS now functions more as a commercial-industry certification. ZENA is pursuing both, with Blue UAS as the more strategically important objective.

ZENA’s product lineup is broader than a single defense drone. The ZenaDrone 1000 is a multifunction medium-sized heavy-lift cargo drone used for ISR, specialized cargo, and some commercial applications such as precision agriculture, with payload capacity of up to 88 pounds. The ZenaDrone 2000 is an interceptor drone based on the ZenaDrone 1000 platform that uses gas rather than batteries to extend flight time; the company has not publicly disclosed a price for this system. The Interceptor P-1 is a smaller one-way expendable interceptor drone expected to sell for under $5,000, and the broader defense ecosystem also includes the IQ Glider marine launch and refueling station.

The IQ series expands the commercial and government product set further: IQ Nano for indoor inventory management, IQ Square for outdoor inspections, IQ Quad for land surveys, and IQ Aqua as an underwater drone for mine detection and commercial use cases. The ZenaDrone 2000 is a maritime drone selling for $50,000 that launches from a ship and then surveys a region of airspace looking for slow moving swarms of drones and then uses AI to identify and track the threat and engage the swarm drones closer to their origin. It is gas powered which extends its operating range. They were also tasked to come up with an interceptor drone designed to sell under $5000.

One R&D site in Baton Rouge, Zena AI, is focused specifically on advanced AI applications for the military, including Eagle Eye. Meanwhile, the company’s core R&D team of about 20 people in Dubai is working on quantum projects, extreme-weather and weather-forecasting applications, and traffic-management systems that analyze real-time data from multiple drone fleets or swarms.

ZENA’s drone fleet is a unique mix of hardware and software, but the software appears to be their competitive advantage. One of the capabilities the military is looking for is the ability to operate autonomously in GPS-denied environments when the enemy uses jamming or spoofing to mess up the targeting capability of the drones. There are also GPS-challenged conditions in dense urban corridors , industrial facilities, and underground sites, and BLOVS missions where their new quantum navigation systems use quantum physics coupled with AI and hyper accurate terrain mapping to find their intended target.

They have a number of drones that are in consideration and are at the final stages of the certification process. What makes this so exciting from an investment viewpoint is that none of this potential is represented in the existing analysts projections and this represents a significant tailwind.

Risks

The question on investors' minds is squarely related to ZENA’s ability to roll up their acquisitions. This is execution risk. Their goal is to create efficiencies in the business that translate into more revenue that drops to the bottom line and pays off the debt within a 3 year term. These are definitive acquisitions so if they don't actively manage their portfolio of over 20 companies they could see their margins erode and not generate enough cash flow to pay back the notes. The good news is with 20+ acquisitions they have diversified the risk of having a bad acquisition having a material impact on the entire business.

If their acquisition targets fail to integrate or generate synergies or fail to scale revenue there is the real possibility of dilution in the future. Within the next 2 years they would have to consider the possibility of raising more capital to pay off the notes or a possible restructuring of the notes.

Doing business with the government is a risky proposition because development costs and certifications are needed just to bid on projects. There is a chance that the company may never recover their investments developing drones for the Department of War. Offsetting this risk is the dual use capability of most of their drones. They have drones with a chassis that could be used for defense or commercial purposes.

Investment Summary

ZenaTech’s latest annual results indicate the rollup strategy is working. They had record quarterly revenue of CAD$5.2 million and a Q4 beat that came in above expectations. The company’s earnings report reflected a positive revenue trend that the acquisitions are increasing their margins. In the background, their SaaS business is profitable and growing. Their continued investment in R&D is keeping them competitive and their quantum navigation tech might be best of breed.

They have many strengths, but execution is by far the biggest risk. ZENA needs to keep integrating acquisitions while holding healthy DaaS gross margins. If they can convert their revenue and margin gains into sustainable cash flow that covers the debt, more investors will support the long term narrative. The good news is that ZENA has several strong tailwinds. Whether it’s rising commercial drone adoption, new defense contracts, or a growing mix of higher‑value services, even one major win could permanently shift their revenue trajectory.

Recent news suggests growing optimism about ZENA winning a major defense award. Ongoing conflict in the Middle East has increased demand for drone technology, and the administration’s proposed $1.5 trillion Pentagon budget includes funding for a “Golden Dome” missile‑defense system along with expanded drone and counter‑drone capabilities. With ZENA’s AI tools, software suite, and manufacturing capacity, they appear well‑positioned for future contract awards. For now, the core DaaS business is covering overhead while investors wait for a transformative military deal that could turn the stock into a long‑term multibagger.

Comments

Log in or sign up to join the conversation.