TM Editors' note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence.

Deeply mispriced with a negative enterprise value

Strong cash position of ~$30 million ignored

Misunderstood reaction to excellent Phase 2 SkinJect readout

Upside of Rare Disease Voucher could be close to $200 million

Multiple shots on goal de-risk story and multiply upside

Warrant holders suppressing stock looking for additional financing may regret move as strategic partners materialize with non-dilutive cash

Medicus Pharma Ltd. (Nasdaq: MDCX) remains one of the most mispriced small-cap biotech stories in the market. They have a microcap valuation of $19 million and approximately $30 mil is held in cash. This leaves them with two Phase 2 assets with a negative enterprise value. Typically, Phase 2 assets are conservatively valued between $200 million and $500 million not less than zero. Before Medicus even released its clinical results, the market was already severely mispricing the company at a $60 million market cap. Following the positive Phase 2 data, an initial rally was cut short by a Bear Raid that dragged the stock down to $0.40. The current million market cap is backed by cash. The valuation disconnect has gone from deeply undervalued to the realm of the absurd. While this kind of disconnect can persist for a while in small-cap biotech, it also creates the kind of asymmetry that investors often look for before a re-rating begins.

Bear Raid Premarket Runup & Plunge

Thursday, March 5, 2026: The Initial Bull Trap & 50% Plunge

● Premarket Action: The initial headline of positive Phase 2 data drove algorithmic buying and caused MDCX to spike aggressively in early premarket hours, reaching a high of $1.74. Retail momentum traders initially piled into the trade thinking the train was leaving the station but then shorts piled on fast.

● The Reversal: Institutional players focused on the disclosures in the press release and saw a protracted development pathway and exited en-mass fearing substantial dilution. The premarket gains evaporated completely before the regular session opened.

● Regular Session: The stock opened under severe selling pressure and experienced an intra-day collapse on heavy volume. MDCX closed the day at $0.68, representing a staggering 50.88% single-day loss from the previous day's close of $1.38.

Bear Thesis Based on the Fine Print But Nothing was New

The market was highly conditioned for a Bear Raid on the readout. In March of 2025 the company did a Reg A+ with 100% warrant coverage. Then did a warrant inducement deal in December 2025 nearly doubling the number of warrants. In addition, the company had a $1.5 million per month burn rate and was low on cash. The combination of these elements had investors on edge for a long period of time and primed to sell on any sign of weakness. The Bear Raid triggered the sell now ask questions later mentality initially, but the success of the raid and continued weakness was because there was a plausible narrative to the selloff. The Bears all pointed to fine print in the press release but the truth is that it was almost a carbon copy of the disclosures in January 2026:

1. Not Powered for Registration: The company disclosed that the study was not powered for registrational endpoints, meaning the FDA would require additional, large-scale, expensive clinical trials before any commercial approval could be sought.

2. The "Partnering-Focused" Model: Management emphasized a strategic pivot toward finding an external partner rather than commercializing the patch independently. The market interpreted this as an admission that Medicus lacked the capital to move forward alone.

3. Severe Cash Burn: Given their trailing 12-month net losses (~$34.5 million as of late 2025), investors realized that without an immediate partner, massive, dilutive equity raises (share printing) would be required to keep the lights on.

In January 2026 the company spelled out its plan. They were going to release their Phase 2 proof-of-concept study and pursue and End-of-Phase 2 (EOP2) in the first half of 2026. Of course, it wasn’t powered for a registrational trial and if investors weren’t so on edge, they might have remembered that. In addition, the company talked about its Partnering with Deloitte so this wasn’t a surprise either. The cash burn is just a reality of biotech and they had enough to get to the next milestone but investors forgot how to do math and bought the Bear Thesis hook line and sinker.

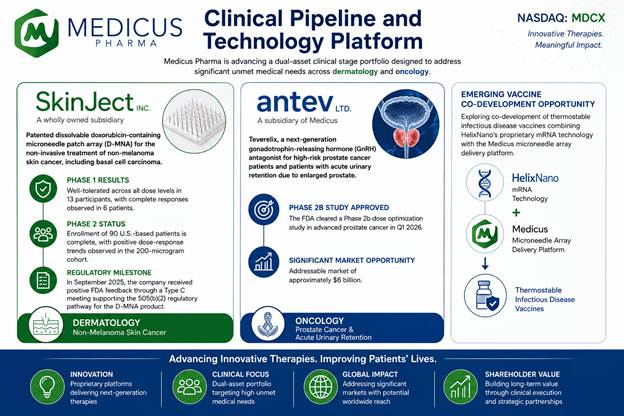

Company Background

Medicus is a value play so it's important that investors understand the company’s pipeline, technology, and goals. SkinJect is the name of their leading platform technology capable of dissolving basal cell skin cancer lesions. They came up with a patented dissolvable doxorubicin containing microneedle patch array that works as a non-invasive treatment of non-melanoma skin cancer like basal cell carcinoma (BCC). Their phase 2 proof of concept study results were excellent and set the stage for another trial that will use the highest dosage of 200ug. It also paved the way for them to submit an orphan drug application for Gorlin Syndrome which is a rare disorder of recurrent basal cell skin cancer where no approved lesion-direct therapies exist.

Antev is the name of their other platform technology. They submitted their phase 2 protocol for Acute Urinary Retention using their GnRH antagonist called Teverelix. The drug is designed to treat high risk prostate cancer patients with cardiovascular issues by stabilizing hormone levels which end up suppressing the prostate cancer growth. Partnering their assets is their primary focus for both of these platforms.

Phase 2 Data Controversy Mitigated

We can sift through the nuances of the phase 2 data but the bottom line is that the data was quite good considering it was a proof-of-concept trial. The market players initially focused on the control arm because the first data point at 29 days demonstrated biological activity. What the pundits missed from their analysis is that the needling of the patch or the device itself will have an impact on the skin. In fact, the company has a MOU with HelixNano to combine their mRNA vaccine platform with Medicus Pharma’s dissolvable microneedle array delivery system to develop a room temperature vaccine patch.

Market players simply forgot that the microneedling patch by itself stimulates the trafficking of immune cells which ultimately led to the resolution of the cancer in a number of control subjects. The scientific team at MDCX knew there could be an effect, but it was never measured. This is why the data on day 57 was so consequential, as it helps them inform the phase 3 design of their pivotal trial. The future control arm will likely be designed to use a patch with no microneedles.

The Problem SkinJect Solves

The market is not connecting the dots that the standard treatment for basal cell carcinoma is the Mohs Surgery and that there is a nationwide shortage of these specialized surgeons. There are 5 million cases of basal cell carcinoma diagnosed annually but only 5,000 trained Mohs surgeons with a capacity of 1 million lesions per year. There is currently a backlog of 7 million untreated lesions. SkinJect is actually a form of triage for the patient while they wait for an available Mohs surgeon. There is also a cost savings element. The Mohs surgery costs about $2,500 per procedure and this cost can run, while SkinJect is modeled around a roughly $1,000 course of treatment, including three patch applications over two weeks. In the Mohs procedure they are basically gouging out the cancer which is a painful procedure and typically leaves scars behind compared to a SkinJect treatment which is a painless, office-based treatment that can compete on convenience and cost while preserving a clear clinical role for surgery in higher-risk lesions.

Orphan Drug Upside

The Orphan Drug Act was approved in 1983 and it took about 15 years before there were maybe 5 approvals per year in the early 2000’s. Contrast that to now, the Orphan Drug approvals represent over half of the new drugs approved today. Gorlin syndrome is a rare genetic condition that results in hundreds of thousands of recurrent basal cell lesions that pop up over the patient's lifetime. SkinJect with its ability to melt away the lesion would be a transformative treatment compared to the frequent surgeries required to remove the BCC lesions that leave behind scarring. Approximately 11,000 patients in the USA are living with Gorlin Syndrome and over 100 babies are born with it each year.

Gorlin syndrome also qualifies for Rare Pediatric Disease (PRD) Designation which means an approval could yield a Priority Review Voucher (PRV) which was recently sold by Rocket Pharmaceuticals (Nasdaq: RCKT) for $180 million. The company filed for Orphan Drug Designation (ODD) in April 2026 after they reported excellent efficacy data from their Phase 2 for BCC which means they might hear back from the FDA in the Sept / October time frame. The ODD is a major catalyst typically worth tens to hundreds of million in value creation depending on the disease indication and the potential for 7 years of market exclusivity on approval, which provides a competitive moat for MDCX.

Teverelix: A Second Shot on Goal

The bullish case for MDCX is not just SkinJect. The company’s second asset, Teverelix, a long‑acting GnRH antagonist, offers a second shot on goal while diversifying the pipeline. The asset was purchased a year ago for a 17% stake in MDCX. The drug was designed to treat acute urinary retention in advanced prostate patients who have cardiovasculature risk. The current GnRH antagonists are not safe for this subpopulation. It is expected that Teverelix will reduce the cardiotoxicity and be the best-in-class treatment option for the 300K - 500K men living with advanced prostate cancer. This market is worth roughly $4.0 billion annually. In February 2026 they got the approval to proceed with a Phase 2b which is a 5 month trial on 40 men. Now with money in the bank investors may get some clinical trial advancement that puts a registrational trial in 2027. Many investors may have forgotten, but the announcement last year to acquire Antev boosted the stock price by almost 90% gaining close to $50 million in market cap. Unfortunately this was followed by a massive downdraft from a financing deal from Maxim that issued shares at $3.10 with 100% warrant coverage. Putting this into context is needed as investors understand how $50 million of market cap was created by the Antev announcement and then quickly erased by a small but dilutive financing. This underscores how quickly sentiment can reverse in a microcap biotech if investment bankers fail to find the right investors that understand the value of their investment.

Financial Analysis

At the end of May MDCX announced $22 million in Non-Dilutive Financing. The funding came from an institutional investor who released $12 million immediately and put $10 million in a collateralized deposit account to be released upon achieving certain milestones. These were secure promissory notes with a 8.75% interest and an OID of 6.5%. The $10 million had no OID and interest of 5%. The company reported Q1 2026 cash equivalents of $6.4 mil, but the financing boosted their proforma cash position to $30 million. Additional guidance projected a cash runway of 2 years which works out to a quarterly burn rate of $3.75 million. Before their latest Phase 2 readout they were burning about $8.0 million a quarter so the new plan suggested a sizable tightening of their belts. The company also indicated they would be repaying $2.5 million in outstanding debt. While the debt increase leverages their balance sheet it also reduces the likelihood of equity dilution at the current levels. They have approximately 40 million shares in the OS and a current market cap of $19 million. Warrant holders have 4 million 5 yr warrants at a $2.00 strike price

Risks

All biotechs have some element of regulatory risk, but the good news is that MDCX is pursuing the FDA’s 505(b)(2) Regulatory pathway. This approval is based on a different mode of administration of the already approved drug like doxorubicin. The 505(b)(2) pathway reduces the risk, cost, and time by allowing the drug company to use the existing safety and efficacy information to make their case that the different delivery mechanism is up to FDA standards.

The riskiest biotechs are the ones with only one drug going after a single indication. Platform technologies that have one drug but can target multiple indications get to take multiple shots on goal to reduce the risk that the medicine will not work. The SkinJet platform is pursuing the 505(b)(2) and Orphan Drug Designation (ODD) for Gorlin Syndrome patients with multiple or inoperable BCCs. The company also has another Phase 2 asset called Teverelix which is a gonadotrophin-releasing hormone GnRH antagonist, that helps high-risk prostate cancer patients deal with acute urinary retention (AUR) episodes due to enlarged prostate.

Another risk is related to the adoption of the product. Assuming it gets approval they still have to get the doctors to buy into using this as an alternative to the Mohs surgery and getting the proper reimbursements in place. Rounding off the list of risks is the dilution risk which is standard in every biotech, but in MDCX it is somewhat mitigated by the debt capital from a strategic institutional investor.

Management and Board

The management team is led by their CEO, Raza Bokhari, MD who is a physician entrepreneur who led Medicus through the acquisition of Antev, guided the filing of an Orphan Drug Designation application, and completed a $22 million non-dilutive financing. Faisal Mehmud, MD is the Chief Medical Officer (CMO) responsible for the clinical trial and has experience in all phases of clinical trial development. Cathy McMorris serves on MDCX’s board of directors. She was one of the highest-ranking republican Representatives and has experience in healthcare policy, regulatory issues and championed legislation on drug pricing, FDA modernization, and rare disease research. Her perspective will be very useful in navigating the regulatory landscape which she ironically helped build.

Investment Summary

Hopefully this article leads investors to the conclusion that the current valuation of MDCX is absurdly low. The management team continues to make all the right moves derisking the company by bolstering the pipeline. However, it's apparent that the financing completed almost a year ago simply attracted the wrong element in the stock. For over a year the stock has been under pressure as investors have been fearing another dilutive financing that just hasn’t happened. The March selloff was a calculated move by the shorts to hijack the narrative and paint a positive readout as negative and instill the fear of another bad financing deal. The bear thesis is rooted in the concept that the trial was not favorable because there was fine print in the press release. The reality is that the fine print is a near copy of their strategy professed months earlier. So it's nothing new.

The market may have over-reacted to the data readout but a number of positive developments with tremendous value creation have failed to reverse the movement in the stock price. The announcement of the filing of an orphan drug designation along with a non-dilutive financing for $22 million did little to excite investors. These are major catalysts that should have rocketed price higher but instead there was a ho hum response.

Holding the stock down are a number of outstanding warrants held by the likes of Armistice Capital and Hudson Bay who may be leveraging them to artificially depress the stock price. MDCX is for the patient investor willing to see through the structure players desire to get cheap stock and focus on the clinical and regulatory narrative. The real upside is going to start after the volume reaches a tipping point. That volume is needed to neutralize the warrant position. It's very clear that the company has about 3-4 shots on goal and some within the next year. There is very little downside risk with a powerful political ally like Cathy McMorris sitting on their board and tremendous upside on reaching any regulatory milestone.

Comments

Log in or sign up to join the conversation.