Strait of Hormuz opening this month?

A Debate Over the Strait and Demand Destruction

Fat Pitch

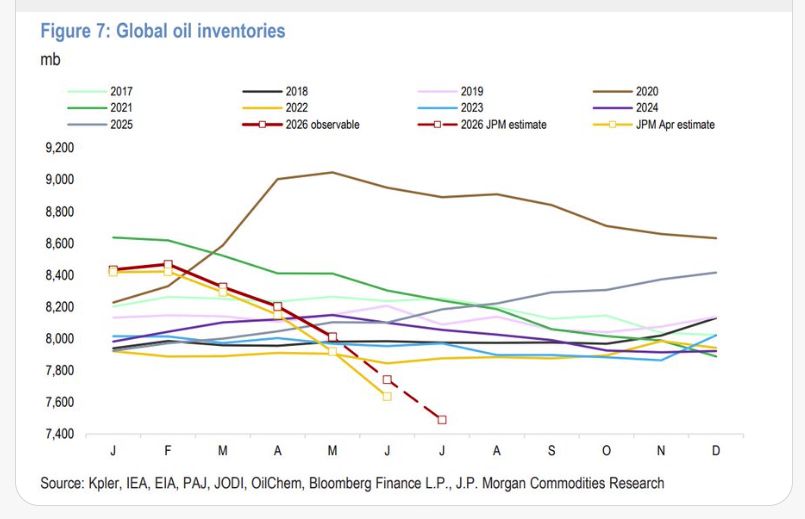

In their latest oil report, J.P. Morgan reiterates that their base case continues to assume the Strait reopens in June. They previously anticipated this happening “one way or another,” and despite the lack of an official agreement, they are refusing to budge on that timeline.

Because the blockade has persisted, they’ve officially updated their projected trajectory for global inventory usage. The timeline has shifted out by one month: JPM now explicitly notes that they expect visible inventories to reach critical stress levels in late June, approaching absolute operational floor levels by September.

Right now, both paper and physical markets appear incredibly comfortable with this prolonged closure. Volatility has collapsed, and Dated Brent’s physical premium over front-month futures has retraced from a frantic $36 in April to just $2 today.

Why? A combination of clandestine “hopping” vessels spoofing transponders, upside supply surprises from Brazil and Venezuela, and massive demand destruction (led by China taking a 3.8 mbd import hit) has cushioned the blow.

But this calm depends entirely on the calendar.

JPM warns that the alternative path is far less comfortable. If their June reopening assumption fails, each additional month of closure will lift average Brent prices by roughly $5 in 3Q26 and a massive $15 in 4Q26, driven by accelerating inventory depletion.

Conclusion: of course sell oil and buy $SPCX on track to achieve 1 trillion EBITDA any minute now.

The Wrong Question

Art Berman is correct that “When will Iran make a deal?” is the wrong question.

But he flunks the right question.

Berman’s Proposed Right Question

Q: Berman’s Proposed Right Question: “What does Iran need that it doesn’t already have?”

A: Berman’s Proposed Answer: Not much.

That’s ridiculous. Iran is in hyperinflation pain, people are suffering, and it is short of hard cash.

However, Iran has a shown propensity to ignore pain. Trump, by contrast, and like all bullies, is susceptible to pain. And Trump, unlike Iran, has midterm elections to worry about.

The True Right Question

Q: How much more pain can Trump put up with?

A: No one knows.

Unknown is where we will be until Trump capitulates.

I agree with JP Morgan that Trump will open the strait. But it won’t be by force. It will be by capitulation, when Trump has had enough.

What complicates the setup are Trump’s own previous statements on release of funds and surrender demands.

In addition, Trump wants to appease the warmongers, those who were against the war, and Israel simultaneously.

That’s mission impossible.

Iran Not on Verge of Collapse

I side with Brett. But that’s not the right question anyway.

What would force Trump’s hand is the correct line of thinking.

Trump will capitulate is my base position. Time is on Iran’s side. But if I am wrong, my fallback position is a catastrophic war.

In my alternate scenario, Iran would go after the region’s desalinization plants and oil infrastructure.

Iran has escalation capability well beyond what Trump can do. This is why we are in a ceasefire now, and why Trump repeatedly backs off threats.

Expect Surrender or a Catastrophic War

$300 billion was an opening salvo to make $30 billion look great.

Trump will wave the white flag and brag about it because Iran is not going to capitulate.

CENTCOM Lies

“All missiles intercepted” says CENTCOM.

Yeah right. Some missile were intercepted by the ground.

Timing

JP Morgan says they “expect visible inventories to reach critical stress levels in late June, approaching absolute operational floor levels by September.”

Q: Are June and September the right months?

A: Once again, nobody can say for sure.

But it’s not just “visible” inventories that matter. Does China have hidden inventories? Are we correctly counting inventories in the first place?

Real Shock Still Coming?

THE RESILIENCE THAT BOUGHT TIME

➡️ China slashed its oil imports by nearly 40 percent in May, offsetting up to a fifth of the lost supply.

➡️ The United States increased crude and fuel exports by more than 2 million barrels a day above last year’s average.

➡️ The Trump administration released 172 million barrels from strategic reserves at record speed, including 1.4 million barrels a day in a single week.

➡️ Gulf producers rerouted millions of barrels daily through pipelines to the Red Sea and Fujairah while a trickle of tankers still moved through the strait.THE BUFFERS RUNNING OUT

➡️ Global inventories are now drawing down at a record pace of 70 to 80 million barrels every single week.

➡️ US crude stocks have fallen to the lowest level in more than two decades.

➡️ Critical storage at Cushing, Oklahoma is approaching operational lows just as summer demand rises.

➡️ Analysts calculate the market has already lost the equivalent of a billion barrels of oil with no replacement in sight.THE BLOOMBERG WARNING

➡️ Greg Sharenow warned that you cannot keep tightening the system by 70 to 80 million barrels a week forever.

➡️ The buffers that absorbed the shock are now depleted and the market has little flexibility left.

➡️ Even relatively small new outages could trigger violent price spikes from here.

➡️ The anticipation of a quick peace deal has kept traders on the sidelines, but the physical hole in supply remains.

Goldman Sachs vs JP Morgan

The only way I see demand destruction bringing things into balance is a recession. That’s a statement, not a recession call.

But here is some other demand destruction, caused by high prices.

Question of the Day

Q: Will Brent crude hit $120+ before the end of 2026?

A: It depends on the timing of Trump’s surrender and what the true levels of oil reserves (seen and unseen) are.

Will the Strait Open this Year

Actually, it’s up to what deal is acceptable to both sides, but primarily the terms of Trump’s surrender.

Drop your sharpest analysis — I’m looking for a serious, high-signal discussion. No memes, no noise, no hype.

“We project the market to return to oversupply from September 2026 due to a lack of material damage to the regional oil infrastructure, rapid recovery in Middle East production, strong non-OPEC supply growth and potential OPEC output increases beyond pre-conflict quotas.”

There is no “high-signal” because there is no answer to many basic questions.

Will the war escalate?

What are the true levels of reserves?

Will Trump and Iran make a deal before reserves hit critical levels?

Are we in a guaranteed no global slowdown economy?

Fitch’s September projection presumes no war escalation, less damage than currently admitted, more oil inventories than widely believed, a quick reopening of the strait, sanctions off Iran, a meaningful ramp in Venezuela production, and no weakening global demand.

It’s a forecast that presumes everything will go right from here. Alternatively, demand destruction is so great we have oversupply by September.

It’s not physically impossible, but it is highly unlikely.

Trump’s Options Unchanged for Months

How everything plays out depends on what action Trump takes and when he takes it.

Trump still has the same three options he has had since the ceasefire started on April 7, 2026.

Trump’s Three Options

Military Escalation

Wait Iran Out

Agree to a Deal Acceptable to Iran

Military Escalation Option Is Flawed

A military operation to remove Iran’s nuclear material could take years with no guarantee of success. Indeed, I would expect this to fail just like we failed in Afghanistan and Vietnam.

The US production of defense systems is running low. The US and the Mideast is defending against $30,000 drones with much more expensive options that are in short supply.

Importantly, it is Iran, not the US, with huge escalation threats. Iran, if attacked, could go after desalinization plants in the region. Literally, the entire nation of Saudi Arabia would have to evacuate in days if its desalinization plants were hit.

Trump seems resigned to the above facts, which is why a ceasefire is in place.

Trump has learned nothing from history. Iran has much higher tolerance for pain than Trump expected.

Never before has a blockade worked. It inevitably increases the resolve of those being attacked. In this case, Trump and Israel killed the Iranian leadership who were willing to negotiate.

Waiting Iran out is not an option because Iran has chosen to wait the US out. And Iran has a much higher tolerance for pain.

Agree to a Deal Acceptable to Iran

When you throw away every option that doesn’t work, you are left with options that will work. That is option three, no matter how distasteful.

It is Trump who is desperate for a deal, not Iran.

For discussion, please see Frustrated Trump Ups Terms for a Deal with Iran. What’s Going On?

Many see this as a sign of no deal. I suggest something else.

Also see Hello. We Are Again Discussing the Terms of Trump’s Surrender to Iran

It’s only a matter of time before Trump waves the white flag.

Note that a huge market pullback, if one is starting, will add more pressure on Trump even if oil stabilizes.

Regardless, there are many technical and fundamental reasons for oil to go in either direction from here.

What Are the Technical and Fundamental Outlooks for Oil Prices?

In case you missed it, please see What Are the Technical and Fundamental Outlooks for Oil Prices?

The technical picture is very clear, yet unresolved. There’s also a debate over reserves and fundamentals.

I discuss the technical picture as well as the Exxon view vs Anas Alhajji’s view on reserve drawdowns.

Alhajji says there is no crude drawdown. Click above link for discussion.

Comments

Log in or sign up to join the conversation.