It will be a holiday-shortened trading week, with markets closed on Friday, June 19. That means OPEX is pushed forward by one day to Thursday, June 18, while VIX OPEX takes place on June 17. Additionally, this week brings a Bank of Japan rate decision on June 16, an FOMC rate decision on June 17, and a Bank of England rate announcement on June 18. As a result, market mechanics should be on full display, especially following reports over the weekend of a potential deal between the U.S. and Iran.

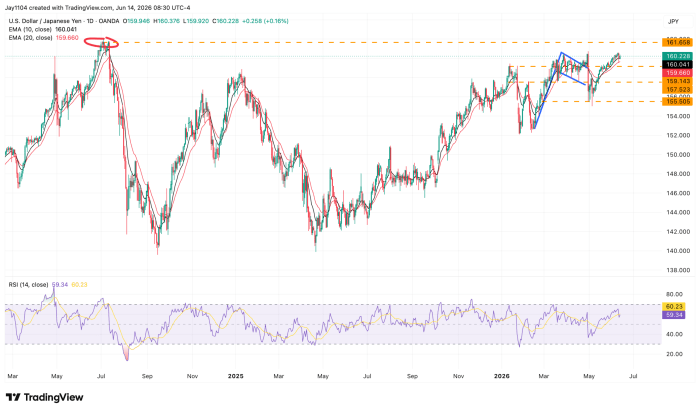

The BOJ is expected to raise rates at this week’s meeting, and even with much of that move already priced into the market, you would not know it from looking at the yen, which continues to weaken against the dollar. Since Japan imports nearly all of its energy, higher energy prices tend to hurt the yen; if oil prices begin to fall due to a US-Iran deal, USD/JPY could start to ease. But absent that, one has to wonder what it will take to reverse the pair’s upward trend.

The Japanese government is not fond of USD/JPY trading above 160. We know that because whenever the exchange rate reaches that area, officials begin conducting “rate checks” or intervene directly in the market.

The rate-check episode pushed the yen back to 152, while the two rounds of intervention only managed to drive it back to 155. Neither effort produced a lasting result. As a result, the government’s only remaining option to support the yen may be for the BOJ to raise rates and signal further hikes. Otherwise, a move above the July 2024 highs near 162 seems very real.

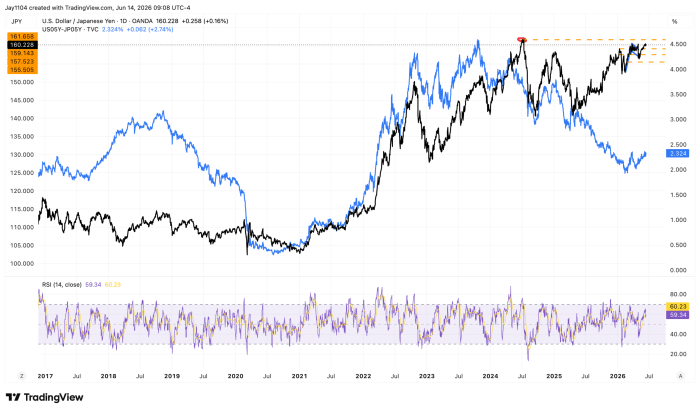

For the longest time, this trade was driven by interest rate differentials, until it wasn’t.

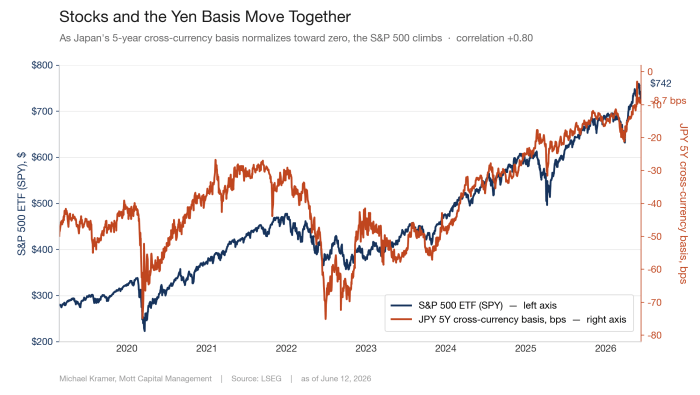

What is even more surprising is that the cost of hedging yen exposure has not been this cheap in years. In many ways, the yen hedge has effectively become the S&P 500 (SPY) trade, with the two moving almost in lockstep for years.

Time and again, it has seemed as though the relationship was on the verge of breaking down, only for it to reassert itself. Every attempt to call for a sustained reversal has proven wrong.

That is what makes the current setup so interesting. Despite a BOJ that appears poised to tighten policy further and growing concern about the yen’s weakness, the cost of protection remains exceptionally low. The market continues to show little urgency to hedge against a stronger yen, even as USD/JPY trades near levels that have previously triggered official intervention.

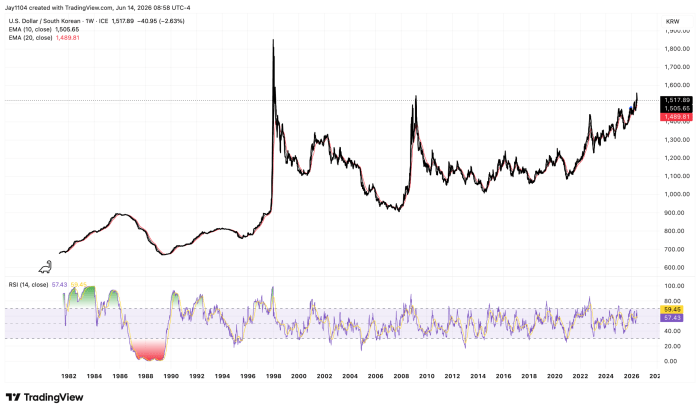

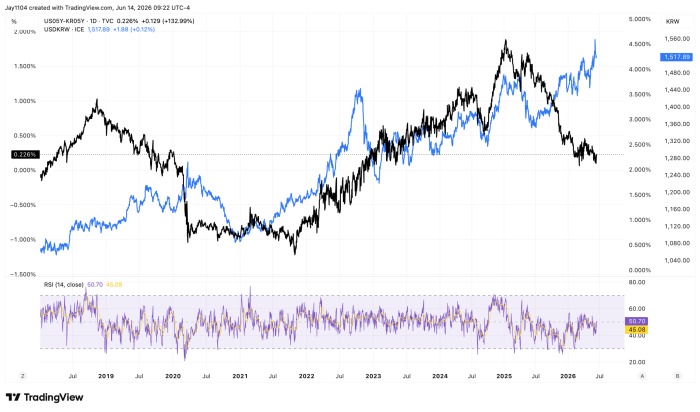

The same can be said for the Korean won. Despite South Korea’s exports being heavily tied to AI-related semiconductor demand, the won has weakened to levels not seen since the 2008/09 financial crisis.

This is important because there are, once again, reports that South Korea plans to work with the U.S. government to address weaknesses in its currency.

For a long time, interest rate differentials also appeared to drive this trade. But just like USD/JPY, the relationship between rate differentials and USD/KRW has broken down.

Despite the spread moving in a direction that should have supported the won, the currency has continued to weaken. That suggests factors beyond interest rate differentials are now playing a larger role in determining the exchange rate.

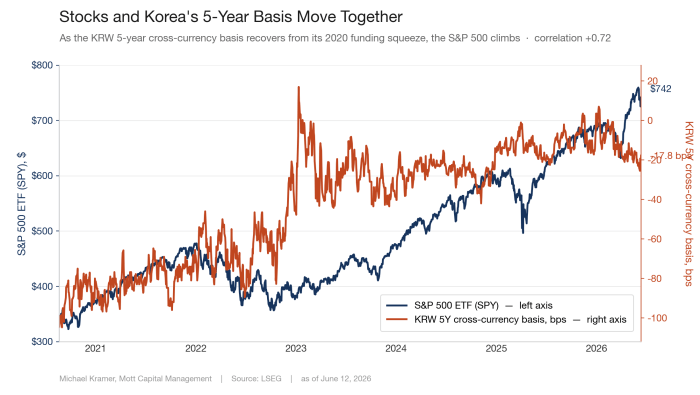

Again, the story is the same for hedging demand on USD/KRW, which shows a strong correlation with the S&P 500.

From this angle, a rising U.S. stock market and a weaker local currency are a win–win for Japanese and Korean investors — they profit on the stocks, then again on the stronger dollar when they bring the money home. That is precisely why no one is rushing to hedge, and why protection keeps getting cheaper: the trade feeds itself. If Japan and Korea are serious about stabilizing their currencies, that incentive is what they have to break. It’s something to watch all week, given the BOJ rate announcement and the headlines coming out of Korea.

Comments

Log in or sign up to join the conversation.