.jpg")

Bonds are so boring, so why are they so important? This is a refrain often heard at times when equity markets are robust, almost to the exclusion of all other investments available to the average saver. Do bonds stand a chance in attracting investors, given the excitement of buying equities into future space travel,or into AI and related data centers, or into soaring energy markets? Yet, bonds determine pension fund valuations, mortgage rates, and corporate borrowing costs throughout the economy. More importantly, bonds directly affect government borrowing costs, and hence tax expenditures. In short, every fundamental aspect of economic life is tied directly or indirectly to the most boring market one can imagine.

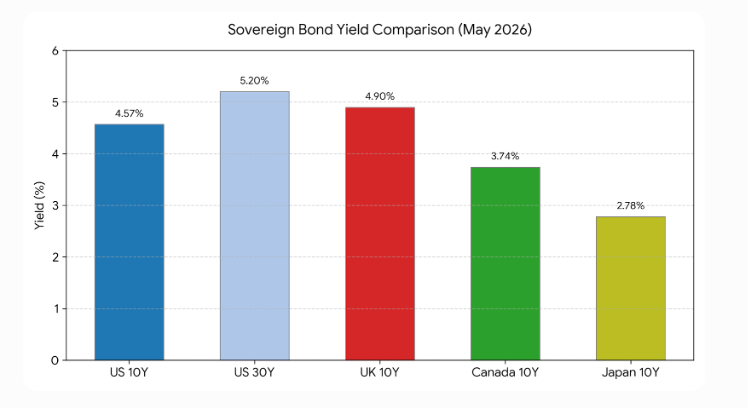

Universally, bond yields are on a relatively steep rise. US Treasuries have touched the highest level in 19 years. Recent Treasury auctions have proven a disappointment as investor appetite was weak, following the release of producers’ price data that signalled that inflation is surging . Once contemplating rate cuts, the Federal Reserve has hinted that rate hikes may be needed should these inflationary conditions worsen. UK gilts, reached a multiyear high as political uncertainty rattled investors. Canadian yields have been pulled upwards in step with those in the US, despite the fact that Canada has a lower inflation rate. The Bank of Japan has been on a steady march to raise its long-term bond yields, reaching a 30-year high recently. None of these central banks have given any hint that rates will come off, and investors have staked out positions accordingly.

So, what do bondholders look for in deciding how much to pay for a bond, what yield is needed to offer adequate protection over the long term?

Inflation expectations. Investors need to think in terms of a 5,10 and 30 years time horizons in a bond purchase. Accordingly, there is a market which quotes yield for a 5-year bond, 5- years from today. Ultimately, however,investors rely on experience and intuition in buying yield over the very long term.

Debt levels do have some influence on the “ term premium” required by investors to guard against future inflation. Much has been written about the surge in US federal debt and whether it is sustainable. In general, debt levels have some influence on this premium for countries, even those with reliable central banks, so solvency is less of an issue. But there is the lingering concern that central banks will ultimately inflate away much of the debt.

Real Rates (inflation adjusted yields) are considered to the true measure of rates that operate economy-wide. The pricing of Treasury Inflation-Protected Securities (TIPS) adjust each year to reflect the most inflation data. These are limited in issuance and not widely sought. Although not all investors think in “ real terms” when it comes to fixed income, it is necessary to calculate implicitly the real rate at the time of purchase.

A world in which long-date bonds are 5% plus has direct implications for the economy. Mortgage rates are derived from bond yields, and so far these levels will continue to retard housing’s contribution to overall economic growth. So far, corporate bond rates have held steady, and the spreads between corporate and government debt is stable. However, any weakness in profits will result in spreads widening and ultimately degrading credit quality. Finally, governments at all levels will have to devote more revenues to service current and future borrowing costs. The bond vigilantes never go away.

Comments

Log in or sign up to join the conversation.