Let’s discuss the right and the wrong answers.

At International Economic Forum today, Putin says, “Any country can at any moment be deprived of access to its legitimate assets, which are placed in dollars or euros, as well as to Western financial payment infrastructure.“

That is correct.

And it’s why there is global talk of dollar avoidance. But how easy is it?

Santiago Capital

The rest of the world can set up new currencies, new payment systems, and new financial infrastructure. But there is nothing they can do to make the USD fall vs its fiat peers if US does not want it to happen.

I am surprised by that answer because I believe Santiago Capital knows better.

I agree with Santiago on continued dollar dominance for reasons explained below.

However, I disagree with the idea other nations can do nothing if the US does not want it to happen.

China can force the dollar dominance issue.

Five Things China Can Do

Float the yuan

End capital controls

Stop export subsidies

Be willing to have trade deficits

Build the world’s largest (or very large) global bond market.

China could do points 1-4 immediately, and there is not a thing the US could do about it. In fact, the US would cheer, and so would the rest of the world.

Point 5 would follow, eventually.

You might say China won’t do those things. And I agree. Which is why I expect US dollar dominance to continue.

And it’s why BRICS and BRICS-solutions are nonsense as well. BRICS won’t go anywhere without China, and China is going nowhere.

What About the Euro?

The Euro flunks point five. It is fundamentally flawed by design, and that design is etched in a treaty that’s nearly impossible to fix.

The structural flaw is a lack of eurobonds. There are only bonds of Germany, Spain, Italy, France, etc., all trading with different interest rates and different default risks.

Moreover, it takes the EU decades to do anything significant because of its consensus structure. One nation can, and frequently does, hold up trade agreements, budget proposals, and defense proposals.

And finally, Germany runs a persistent and massive trade surplus, exporting significantly more goods than it imports.

So, Germany flunks point 4 as well. The EU itself runs a trade surplus.

Questions of the Day

Q: Why does the world accumulate dollars?

A: The US runs a trade deficit with most of the word.

As a direct result of huge persistent trade deficits, the world accumulates US dollars.

Q: What does the world do with the dollars?

A: Recycles them into US assets mainly US Treasuries and Agencies.

Q: Is this why the US has the world’s biggest bond market?

A: Yes, that plus huge recurring fiscal debt and a mountain of debt held by the public to the tune of $31 trillion, $39 trillion total.

Q: Can the US do anything about this?

A: Only superficially, without a complete global financial rework.

Trump tried tariffs. Well guess what? Tariffs didn’t work and won’t.

Tariffs will not stop deficit spending in congress or the resultant flood of US dollars. And it did not even make huge dents in the trade deficit.

The US could implement capital controls, put a tax on buying US treasuries, or put negative interest rates on foreign held treasuries etc.

But all of those would involve serious risks and possibly start a currency crisis. Importantly, those non-solutions would not fix fundamental problems.

The Fundamental Problems

There is no brake on deficit spending. Congress can and does keep raising the ceiling and spending more and more.

There is no brake on trade deficits.

Gold provided those brakes. When Nixon closed the gold redeemability window in 1971, all brakes were removed.

The US consumer became the buyer of last result. Later on, there were no brakes on Chinese exports.

China can fix this but doesn’t want to. Germany does not want to fix its reliance on exports either.

There is a lot of moaning in all corners of the world. However, China, the EU, and the rest of the world are all more happy with the US being the consumer of last resort than they are to fix the fundamental problems.

Congress is happy to slosh around more dollars too. At the first sign of trouble Congress and the Fed are johnny$-on-the-spot. Republicans only preach fiscal conservative ideas when Democrats are in charge.

Heck, we have massive deficits and a mountain of debt further piling up without even being in recession.

What to Expect

Nonsense about BRICS has been endless for over a decade. And it will continue.

So will nonsense about the dollar heading to zero and countries doing something about the dollar.

But inflation is a problem. Stock market bubbles are a problem. Deficit spending is a problem.

Sustainability of the Setup

Q: Is this sustainable?

A: No.

Q: When does it end?

A: I have no idea, nor does anyone else.

Q: How does it end?

A: A global currency crisis.

Q: What’s the role of Bitcoin in the crisis?

A: None.

Q: What’s the role of gold following the crisis?

A: I don’t know.

Q: What about the petrodollar?

A: Good question. See below

On April 14, 2026 I commented The Petrodollar Theory Is Dead. It Never Made Sense to Begin With

Several readers asked me to discuss the petrodollar. Here are two pertinent theories.

Also see What Does CFR’s Brad Setser Say About Petrodollar Myth and Reality?

“The glory days of the petrodollar are over,” says Brad Setser.

That’s assuming there ever were glory days, something that Setser definitely hints at in his post.

Dollar avoidance is not that easy or it would have happened in a major way already.

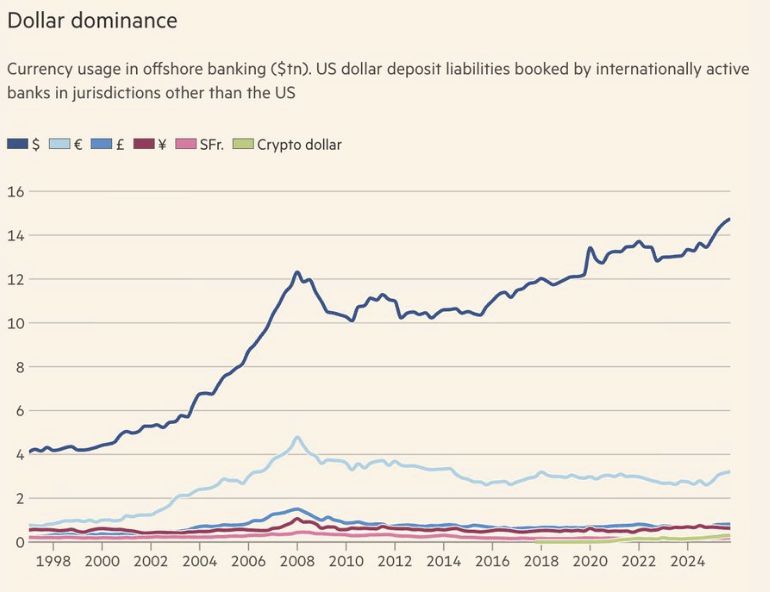

Offshore US Dollars Surge Over the $14 Trillion Mark, Where’s De-Dollarization?

Finally, please see Offshore US Dollars Surge Over the $14 Trillion Mark, Where’s De-Dollarization?

Is de-dollarization happening? If so, where and how?

There is nothing strange about the surge in dollars. Indeed, it’s the expected behavior.

Expected Behavior Explanation

The US runs trade deficits every year.

Those dollars accumulate overseas

Other US dollar funding originates overseas.

My 2019 post is still accurate.

Flashback September 19, 2019: Nixon Shock, the Reserve Currency Curse, and a Pending Currency Crisis

Forget the Yuan

Many expect China to overtake the US and for the yuan to replace the dollar as the world’s reserve currency.

Such talk is nonsense. The reserve currency holder needs to meet several requirements of which China meets none.

Reserve Currency Curse

The reserve currency irony is that despite protestations of US advantage, no country wants the alleged advantages the US purportedly receives.

Trump would be very pleased if the Yen, yuan, and Euro rose vs the dollar, and US exports rose.

Does Japan want a strong currency? China? The EU?

Since no one really wants it, having the reserve currency is best viewed as a “curse” not an “exorbitant privilege“.

Trade Wars and Currency Wars

If you peel off the layers hidden over the years, Trump’s trade wars are really an effort by Trump to shed the “reserve currency curse“.

Global Consumers of Last Resort

The US is stuck with the reserve currency because we have the largest, most open capital markets in the world, the world’s largest bond market, and a far better business climate than the EU, China, or Japan.

To ensure the US remains the curse holder, the EU and Japan have negative rates, China does not float the Yuan but props up corrupt SOEs, and Germany punishes the rest of the EU.

A currency crisis awaits as the current path is not sustainable.

Timing and conditions of the crisis are not knowable. It can start anywhere but I suspect the EU, Japan, or China as opposed to the US.

Meanwhile, I suggest holding at least some gold.

This is unsustainable but no one can tell you when the system finally has a heart attack over it.

Meanwhile, dollar avoidance is not that easy or it would have happened in a major way already.

China, in particular, is not interested in doing what it takes. It wasn’t interested in 2019 and it still isn’t today.

Comments

Log in or sign up to join the conversation.