While the headlines surrounding the August Employment Situation report seemed to focus on the moderating pace of new hiring activity, in my humble opinion, the bigger story was the sizable drop in the unemployment rate.

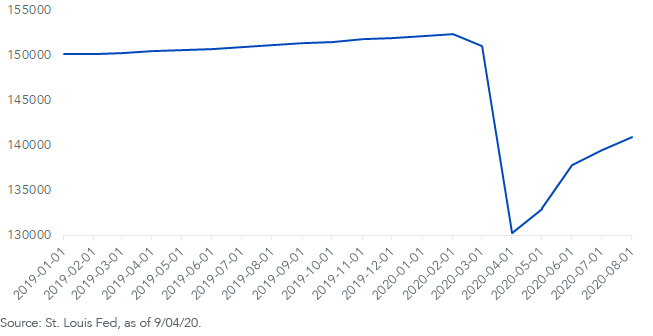

The markets and headlines tend to focus more on nonfarm payrolls (new hiring), and I have no quarrel with that, so let’s first get some perspective on that front. Total nonfarm payrolls rose by about 1.4 million workers, right around consensus forecasts. However, the overall gain was elevated by the hiring of 238,000 temporary census employees. Nevertheless, job gains were broadly based, which is an encouraging sign. New hiring has now recouped nearly 50% of the total job losses that occurred during March and April.

Total Nonfarm Payrolls

Back to my main focus, the unemployment rate. It shrank 1.8 percentage points in August, falling to 8.4%. The most important part of this update is that the decline came in the wake of a huge gain of 968,000 in the civilian labor force (another encouraging sign). However, civilian employment surged by nearly 3.8 million workers, or nearly four times the increase in the labor force—it’s just simple math.

Unemployment Rate

Bond Market Implications

As of this writing, the U.S. 10-Year Treasury yield had reversed some of last week’s decline, heading back up to the 0.70% mark. For the near term, I envision more of the same—a range-bound pattern. But, as I noted in last week’s blog post on the Federal Reserve (Fed), a move back toward the 1% threshold remains the base case.

With the Fed’s new ‘average inflation targeting’ policy framework, the monthly jobs report will be losing some of its cachet. We all know the Fed won’t be raising rates for quite a while even if we get some blowout job reports in the months to come. Remember, there will be no more pre-emptive rate hikes to ward off potential inflation. The Fed will have to wait to see the ‘whites of inflation’s eyes’ before pulling the trigger.

How Should Fixed Income Investors Consider Positioning Their Portfolios?

Fixed-income investors should consider duration shortening strategies with the goal of complementing core bond holdings. The WisdomTree Interest Rate Hedged High Yield Bond Fund (HYZD) can be paired with the WisdomTree Yield Enhanced U.S. Aggregate Bond Fund (AGGY) to potentially achieve this outcome.

Comments

Log in or sign up to join the conversation.