VIX closed above its Short-term support/resistance at 13.19, leaving it on an aggressive buy signal. This week has been another “inside” week, signifying indecision. The next important milestone is Cycle Top resistance at 24.18 where a long-term breakout of the downtrend may occur.

(Equities.com) When most business media folks talk about risk, they’re specifically referring to volatility. But true risk, as professional investors accept it, is defined as the probability of permanent capital loss. Volatility, however, is the variability of future expected prices. If we expect prices to charge upward or fall precipitously in the next month or two, then we’re expecting lots of volatility, but not necessarily increased risk (as defined by the probability of permanent capital loss). Most individual investors would be very glad to reflect on the difference between these two terms, and brand the difference in their minds.

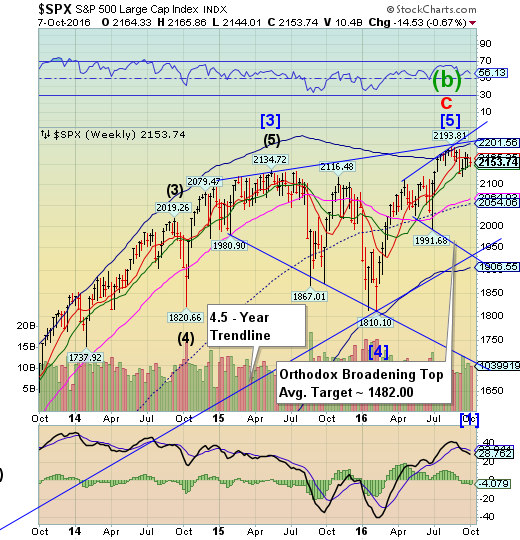

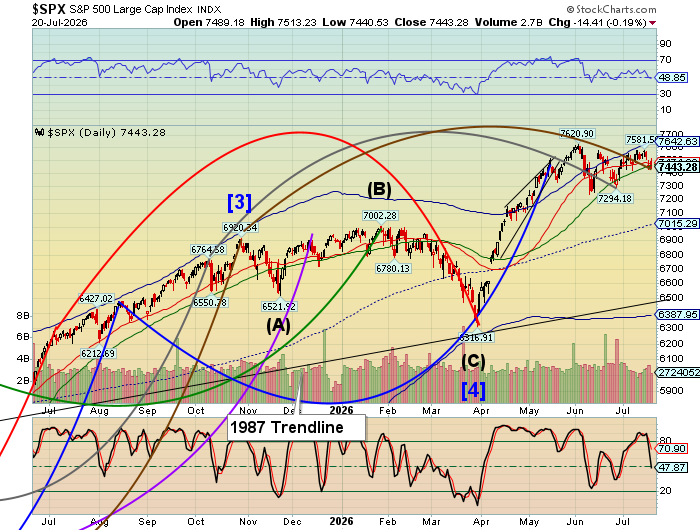

SPX has another inside week

SPX declined from its Short-term resistance at 2165.35, testing Intermediate-term support at 2147.37. It remains on a sell signal with weekly MACD confirming it. Long-term support and mid-Cycle support bertween 2064.02 and 2054.05 appear to be the next targets should a decline develop. However, the more important targets may be those of the two Orthodox Broadening /Tops. The Broadening Top trendline and 4.5-year trendline intersect near 1940.00. Should those supports be broken, a panic decline may follow.

(RealInvestmentAdvice) We seem to be stuck.

For the last couple of months, with the exception of the momentary blip to the downside, the market has spent its time within a fairly narrow trading range. For 43-days. the market traded within a 1% range before the “catastrophic plunge”(sarcasm) to support at 2125. Since then, the market has climbed, slowly, the bullish trend line into a fairly tight wedge – it’s been up, down and sideways.

NDX slides, but still above Cycle top support

NDX had a second loss week in the past month. It closed above its cycle Top support/resistance at 4849.17. However, a close beneath its short-term support at 4810.49 may put NDX on a sell signal.

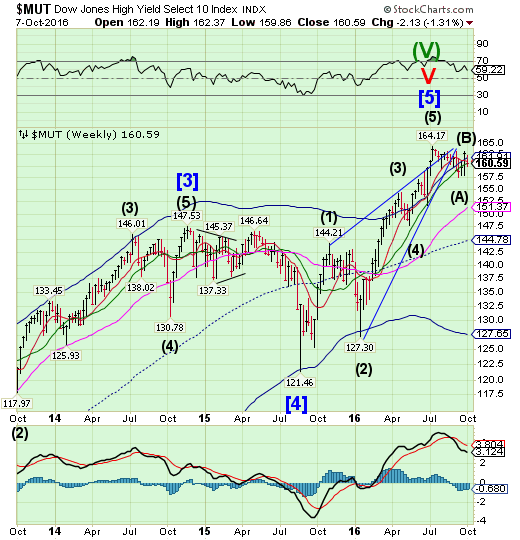

High Yield Bond Index has an indecisive week

The High Yield Bond Index closed the week 1 tick above its Intermediate-term support at 160.58. Earnings reports begin next week, giving us a window to examine not only profitability but ability to service debt.

(Bloomberg) More warning signs are flashing in the junk-bond market.

Investors that have been loading up on the securities as an alternative to ultra-low interest rates are now barely getting paid more than higher-ranking bank lenders, who would typically get their money back first in the event of a default. The difference in yields between junk bonds and the more senior leveraged loans is the narrowest in two years, data compiled by Bloomberg show.

“The risk-reward is getting skewed,” said Peter Tchir, head of macro strategy at Brean Capital LLC. “It’s a sign markets are not assigning enough risk to those high-yield bonds.”

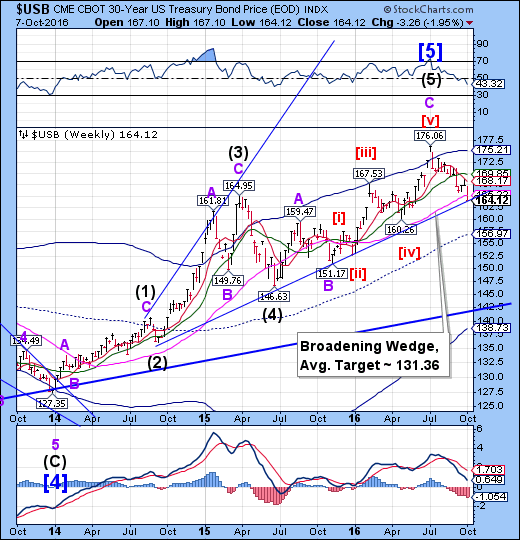

USB declines to the trendline

The Long Bond declined to the trendline of its Broadening Wedge formation. The Cycles Model suggests that a month-long rally may be in store. Whether this rally takes USB to or beyond its cycle top is still in question.

(WSJ) U.S. government bonds strengthened modestly Friday, ending a run of losses after the latest jobs fell a bit short of expectations.

The U.S. economy added 156,000 new jobs last month, compared with the forecast of 170,000 by economists polled by The Wall Street Journal. Average hourly earnings for private-sector workers rose 6 cents, or 0.2%, from the previous month.

Bonds were ultimately little influenced by the report, swinging back and forth from gains and losses before ending the day slightly higher.

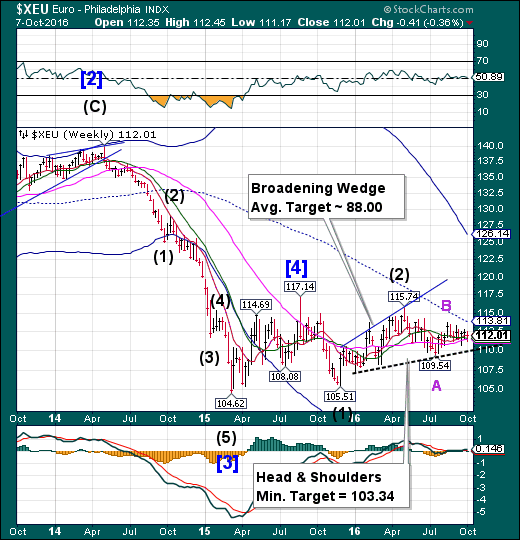

The Euro tests Intermediate-term support

The Euro challenged Intermediate-term support at 111.63. The Cycles Model suggests that the Euro may have additional strength for another week or so. However, a downside breakdown may change to weakness in a hurry.

(Bloomberg) Clearing has become a pawn in the post-Brexit battle for London’s financial services industry, but U.K. Chancellor of the Exchequer Philip Hammond says it may not necessarily be up for grabs after all.

Most interest-rate swaps trading and clearing in the euro currency takes place in the U.K., a feature that for years has made the European Central Bank uneasy. Hammond’s predecessor, George Osborne, fought a legal battle to protect that business and won. The battle for London’s $570 billion of daily euro derivatives trading was reawakened after Britons voted in June to leave the European Union.

EuroStoxx ends a three-week rally

The EuroStoxx 50 Index appears to be running out of strength, although it closes above its Long-term support at 2994.43. The wide swings suggest a return of volatility that may influence price to the downside, as the Bearish Flag suggests.

(CNBC) European stocks closed lower on Friday following disappointing U.S. jobs numbers and after a dramatic plunge in sterling early in Asia trading.

The pan-European STOXX 600 was down 0.9 percent, but the FTSE 100 index ended the day 0.76 percent higher, helped by mining stocks, as the companies benefit from a weaker pound.

The U.S. added 156,000 jobs in September, missing market expectations, and falling short of August's revised 167,000 figure. This could make the U.S. Federal Reserve more cautious about raising interest rates soon.

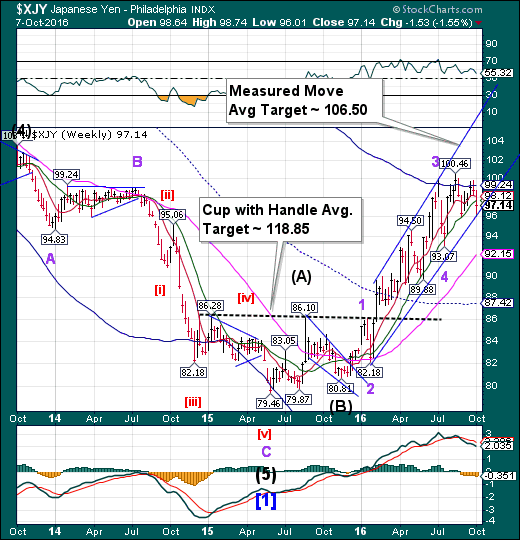

The Yen bounces off its trendline

The Yen bounced off the lower trendline of its 9-month old trading channel. This week’s low marks the end of a Master Cycle. There appears to be a new period of strength lasting through late October, giving it time to attempt to make its Cup with Handle target, or the lesser Measured Move target as it breaks above the Cycle Top resistance at 99.24.

(DailyFX) The Japanese Yen heads into the end of 2016 trading near multi-year highs versus the US Dollar, and economic developments suggest the JPY may finally break the ¥100 level before the year is through. Continued inaction from both the Bank of Japan and the US Federal Reserve represents the biggest risk to the USD/JPY exchange rate. Other key risks are the rise of trade protectionism and financial market volatility. And indeed, the status quo suggests the USD/JPY will likely fall further until we see major changes.

The Nikkei may have completed its bounce

The Nikkei appears to have completed its bounce out of its last Master cycle low on September 27. Maximum resistance appears to be at round number resistance at 17000.00. The Cycles Model suggests the decline may last through the end of October.

(JapanTimes) Amid a growing wait-and-see mood prior to the release of U.S. jobs data for September later in the day, the bellwether Nikkei average snapped its four-day winning streak on Friday.

The 225-issue Nikkei shed 39.01 points, or 0.23 percent, to close at 16,860.09 on the Tokyo Stock Exchange. On Thursday, the key market gauge rose 79.86 points.

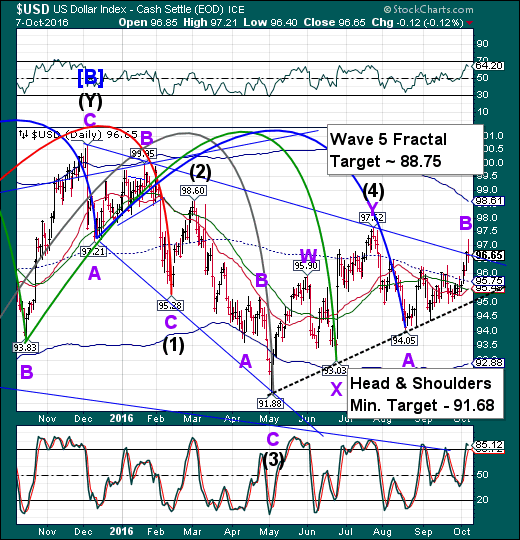

U.S. Dollar spikes the upper Descending Wedge trendline

USD spiked above the trendline of the Descending Wedge trendline, closing on it. The Cycles Model now suggests a reversal may be in the works. The next month may unhinge the Dollar bulls, since all the traders are on one side of the boat. The unwinding of those trades may cause a rapid move to the other side.

(Reuters) The dollar is likely to rise a bit further, but a tame U.S. rate hike outlook at a time of waning firepower from those global central banks still easing policy will limit its gains, according to a Reuters poll of foreign exchange strategists.

The Fed is still poised to pull the trigger in December, but its lingering hesitation in delivering even one rate hike this year after suggesting initially that four were in the pipeline has pushed the dollar down over 2 percent so far in 2016.

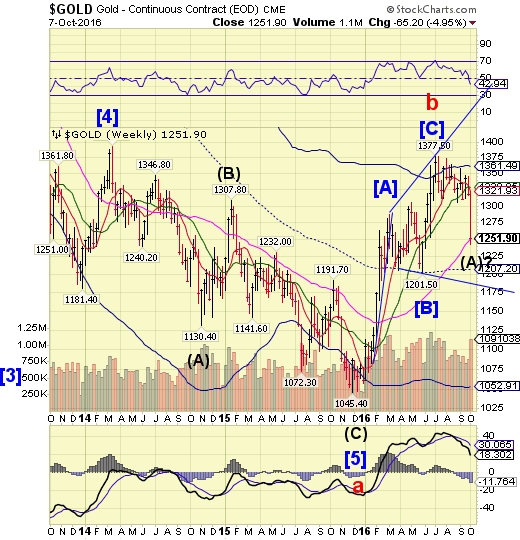

Gold falls to Long-term support

Gold declined to challenge its Long-term support at 1251.95, closing just beneath it. It is due for a bounce, according to the Cycles Model. A probable target may be weekly Short-term resistance at 1321.93. A deeper low awaits Gold In late October.

(CNBC) It's been a bruising week for gold prices, with the precious metal falling as low as $1,243 on Friday, for a 6 percent loss in a week's time — but John LaForge, the head of real asset strategy at Wells Fargo, thinks the worst is still ahead.

"Is the $60 drop in gold prices the beginning of a deeper dive? Our answer is yes, it may very well be," LaForge wrote in a Friday report. "The history of gold, and commodity super-cycles, says that gold may very well lose another $200/oz., testing the $1,050 level, before it is time to buy again."

Crude meets mid-Cycle resistance

Crude rallied to mid-cycle resistance at 51.61, ending its period of strength. There is now the probability of a month-long decline that may test the February low. After 6 months of being range-bound, traders are sanguine about the outlook for crude.

(Forbes) The last few days have been quite eventful for the commodity markets, particularly crude oil, as the anticipation of a production quota by the Organization of Petroleum Exporting Countries caused oil prices to move rapidly in the last week. The world’s largest cartel finally reached an understanding to cap their combined oil production between 32.5 and 33 million barrels per day, marking its first coordinated production quota in the last eight years. The news prompted the global benchmark of crude oil prices – WTI and Brent – to jump by 5%-6% in a single trading day. However, as the market absorbed the announcement, some of the industry experts have been doubtful about the improvement in the oil prices that the investors are expecting from the production cap.

Shanghai Index coming off a week-long vacation

The Shanghai Index tested trendline support at 2969.00 this week. A break of the Bearish Flag trendline may set the next decline in motion. The fractal Model suggests the Shanghai is due for another 1,000 point drop, possibly starting next week. The next Master Cycle low is due in mid-October.

(ZeroHedge) Almost exactly one year ago, we reported that as a result of the commodity crash of 2015, more than half of Chinese companies in the commodity sector did not generate enough cash flow to pay the interest on their debt. Months later this has manifested in a countrywide push for debt-for-equity exchanges, and outright bankruptcies including the first ever liquidation of a Chinese state-owned enterprise.

While dramatic, the question remained: what about other Chinese companies not directly involved in the commodity space? We now know the answer: according to Reuters, profits at roughly a quarter of all Chinese companies were too low in the first half of this year to cover their debt servicing obligations, i.e., merely the mandatory interest payment let along debt maturities, as earnings languish and loan burdens increase.

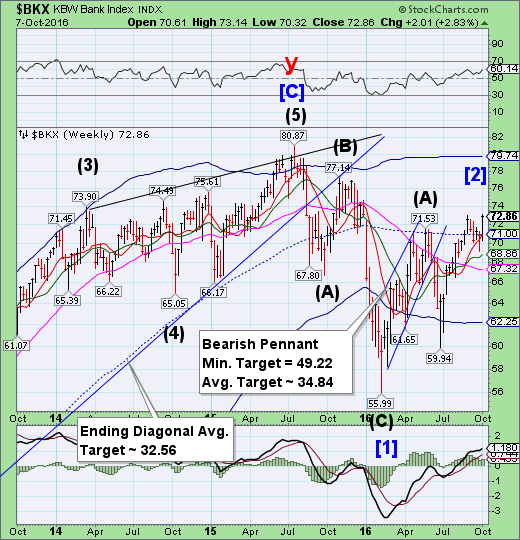

The Banking Index closes beneath mid-Cycle support

-- BKX spiked higher, completing its third week from its September 15 Master Cycle low. This indicates that the entire cycle is probably being delayed. Expect the decline to resume imminently.

(ZeroHedge) Early in 2016, when oil prices were plunging and when US banks were careful to push up their loan loss reserves to exposed E&P loans, we noted something surprising: Canadian banks had barely taken any loss reserves to their exposure in the oil and gas sector.

As and RBC report calculated at the time, if they used the same average reserve level as that applied by US banks, Canadian banks' current loss allowance excluding RBC would surge from $170MM to over $2.5 billion, resulting in a substantial hit to earnings, and potentially impairing the banks' ability to service dividends and future cash distributions.

For months this discrepancy persisted even as oil remained well below last year's levels, leaving Canadian bank watchers stumped as to just how Canadian banks planned to pull this particular "Exxon" without suffering balance sheet impariment, until this morning when we may have gotten the answer how the local Canadian money centers "planned" to resolve this odd accounting gimmick.

(ZeroHedge) So much for last week's rumor of an imminent reduction in the DOJ $14 billion settlement, which sent the price of DB soaring, and propelled the global stock market higher.

Moments ago, Reuters reported that the German government is pursuing "discreet talks" with U.S. authorities to help Deutsche Bank secure a swift settlement over the sale of toxic mortgage bonds.

German officials have, until now, played down their role in the standoff, saying it is up to Deutsche to work out a deal with the DOJ, which is demanding $14 billion to settle RMBS misselling claims. But now it has been confirmed that Berlin government officials are hoping to "facilitate a quick deal that would buy Deutsche Bank time to regain its footing."

(ZeroHedge) It would appear the powers-that-be have just stumbled on to the ugly fact that all the bailed-in depositor money in the world won't stop the novated, rehypothecated, collateral chain collapse contagion that Deutsche Bank's $40 trillion-plus derivatives book's Damocles sword hangs over the status quo. However, being the problem-solving types, the European technocrats have a 'fair-share' solution - back a derivative clearing-house with taxpayer money to solve the new too-biggest-to-fail problem "that no one saw coming."

While the "rules" right nbow are that everyone from shareholders, bondholders, and depositors alike on up the capital structure are supposedly "bailed-in" to save an ailing bank, this problem is just way too big.

(ZeroHedge) Nearly four years after it was first revealed that Deutsche Bank had engaged in various shady deals at the height of the financial crisis designed to mask Monte Paschi's financial woes, on October 1 Italy finally charged the German lender and 6 of its current and former managers, including the infamous Michele Faissola (much more on him soon), Michele Foresti and Ivor Dunbar, for colluding to falsify the accounts of Italy’s third-biggest bank, Monte Paschi, and manipulate the market. Two former executives at Nomura Holdings Inc. and five at Banca Monte dei Paschi di Siena were also charged.

As Bloomberg reported, prosecutors have been reconstructing how Monte Paschi’s former managers misrepresented the lender’s finances in the years through the two deals signed with Deutsche Bank in 2008 and Nomura in 2009.The investigation revealed Monte Paschi arranged the transactions to hide billions in losses that led to false accounting between 2008 and 2012, according to a prosecutors’ statement released Jan. 14, when they completed the investigation.

(ZeroHedge) In addition to 100s more job cuts, Deutsche Bank stock is tumbling on the back of Bloomberg reports that the German government isn’t in talks with the U.S. Department of Justice over Deutsche Bank.

-

There are no talks taking place with the DoJ, German government official says on customary condition of anonymity

-

German government has always made clear that this is about talks between the U.S. authorities and Deutsche Bank: official

And the reaction is a heavy volume dump...

ZeroHedge) Despite proclamations from various officials, business leaders, and mainstream media pundits that Deutsche Bank's demise was: a) driven by speculators, b) not driven by any need for liquidity, because c) the bank has plenty of capital... it doesn't. As Bloomberg reports, no matter how much the DoJ fine is watered-down (don't expect much), the most systemically dangerous bank in the world is holding informal talks with securities firms to explore options including raising capital; but while the lender has several options, as one analyst noted rather awkwardly, "they’re all unattractive."

After three straight days up - soaring 25% off last Friday's lows, thanks to a disproven rumor of a pending settlement with the DoJ - Deutsche Bank closed down 4% from its opening highs today, beginning the slow path to catch down to CDS-implied pain...

Have a great weekend!

Comments

Log in or sign up to join the conversation.