There are 11 million vacancies in the US so for the economy to have only created 194,000 jobs in September shows that this is a supply problem and is not demand-related. The competition for workers is intense and this will push up wages and increase inflation pressures. This argues for a dialing back of the Fed stimulus on November 3rd.

Major jobs miss, led by government cuts

Well, that has thrown a spanner in the works. Payrolls rose just 194k in September versus the 500k consensus, which if hit would have cemented expectations for a November 3rd taper decision from the Federal Reserve. There were 169k of upward revisions, but this is still a big miss.

The details show private payrolls rose 317k while the number of government workers fell 123k, which is a major surprise and surely will be reversed at some point. Within private employment the goods sector produced decent jobs (52k), but the leisure and hospitality sector posted a gain of just 74k with the chart below showing that this is where much of the lost jobs since the pandemic started still reside – along with government and education & health. The rest of the economy is back to where they were pre-pandemic, which is at least one crumb of comfort.

Employment by sector – peak to trough and peak to current (millions of jobs)

Source: Macrobond, ING

Where are the workers?

Despite this disappointment, there was a big drop in the unemployment rate from 5.2% to 4.8% with household employment rising 526k. The participation rate actually fell, which offers more evidence that the decline in worker participation is going to be a longer-lasting story than many (including the Fed) think. Surprisingly, employment as a proportion of people of working age is still no better than the levels we saw in the depths of the Global Financial Crisis.

The return of in person schooling was supposed to see potential workers flooding back, as was the ending of extended and uprated unemployment benefits, yet there is no sign of this happening yet. Remember that half of all states ended these benefits in July so for no improvement in worker participation come September suggests major rigidities in the labor market.

Labor participation rate and employment as a proportion of working-age population

Source: Macrobond, ING

Cash buffers mean people have no urgency to return?

It is possible that households have built up savings buffers and don’t have any urgency to return – cash, checking and time savings deposits have increased $3.5tn since the end of 2019. That said we are coming up to holiday season and with household expenses set to rise this could incentivize more people to seek work. Consequently, we may see an acceleration in job creation in the November and December reports.

Or is it more permanent through early retirement?

Even if workers do return we strongly suspect labor participation will remain below pre-pandemic levels for quite a while. We believe there is a more permanent loss of potential workers driven more by people taking early retirement. The thought of returning to the office and the daily commute may seem unpalatable for many people and with surging equity markets having boosted 401k pension plans, early retirement may seem a very attractive option. On top of this border closures will have hurt immigration and slower birth rates mean fewer young workers entering the workplace.

We see ongoing labor supply issues

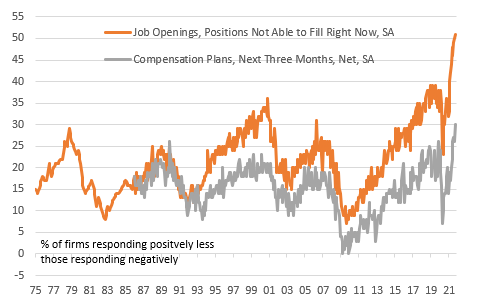

If correct, labor market shortages could persist for a good deal longer, which will mean companies increasingly bidding up pay to attract staff. This was the story from the National Federation of Independent Business survey yesterday, which showed record highs for companies with vacancies they can’t fill, the proportion of companies that are raising compensation, and the proportion that are set to hike compensation even further in coming months. Elevated quit rates suggest that companies may also have to do so to retain the staff they currently have. Either way, it points to more inflation pressures for the Fed to respond to.

NFIB survey shows firms can't find workers and are raising pay aggressively

Source: Macrobond, ING

Wage pressures = inflation pressures = Fed taper

As for what this means for the November 3rd taper decision. Well, it makes it a much closer call, but we still narrowly favor it happening. Private payrolls still posted a reasonable increase and with the wage story moving higher and companies struggle to find staff it continues to be a labor supply issue that is holding back jobs rather than demand – remember that there are 11 million vacancies in the United States right now. With inflation pressures in the economy continuing to build this argues for a dialing back of the stimulus.

Comments

Log in or sign up to join the conversation.