Image Source: Pixabay

Market Analysis

In somewhat of a classic move, the World Board left both their US corn & soybean 2022/23 supply/demand data unchanged despite both crops’ stocks being below the trade’s March expectations. The USDA did up wheat’s 2022/23 carryover by 30 million bu by reducing wheat’s feed demand to reflect this crop’s larger quarterly stocks.

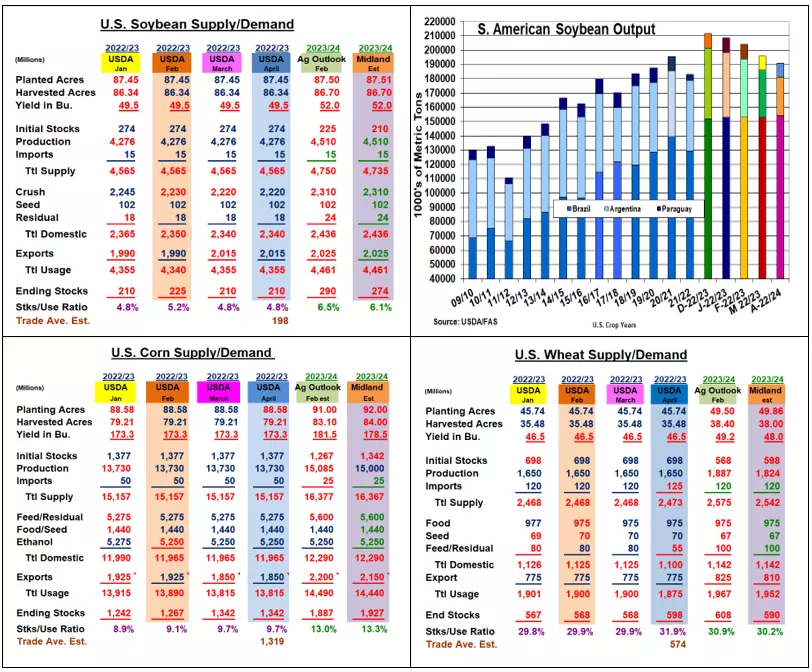

After last month’s 3.3% lower-than-expected March quarterly stocks, all eyes were focused on the USDA’s 2022/23 soybean ending stocks. Instead of a 10-15 million smaller carryover, the World Board left its 2022/23 S&D unchanged. The USDA didn’t up exports or increase their residual demand to reflect last month’s 30 million bu difference actual & the calculated March demand. It appears they are optimistic about finding these lost bushels so kept 22/23s stocks unchanged. This year’s March residual demand being at 156 million bu, the highest in 7 years, suggests 2022’s US yield could be over-estimated. Interestingly, the USDA did lower Argentina’s crop by 6 mmt to 27, but upped Brazil’s crop by 1 to 153 mmt. 2023’s 22.5 mmt decline in Argentina’s output from December (45.5% drop) didn’t up US exports or change the USDA’s world stocks that stayed at 100 mmt this month.

The USDA’s unchanged 22/23 corn stocks wasn’t as big of a surprise given this feed grains 70 million bu lower March stocks. Since a high portion of corn’s feed demand comes from on-farm supplies, waiting until June’s data to revise this demand or make a call about crop size seems appropriate. S Am’s overall output was near estimates with Argentina down 3 mmt to 37 while Brazil was unchanged at 125 mmt. Similar to beans, the USDA sliced only 1 mmt from their world stocks to 295.4 mmt despite their lower S AM crop ideas. The USDA upped its wheat imports by 5 million while de- creasing feed demand by 25 million to reflect March’s higher stocks than expected. 2023’s 598 million US wheat stocks remain at their lowest level since 2013/14. With numerous reports of US Plains wheat fields being zero-out because of the current drought, the market focus will be quickly returning to the US new-crop prospects.

What’s Ahead:

After no USDA demand changes for soybeans and corn, the market focus will now switch to 2023/24’s US and World crop output potential. Russia’s chatter about leaving the Black Sea Corridor deal adds to market nervousness. Looking to add 10% in May sales at $15.35-50 & $6.70-80 and 20% for Chicago May wheat at $7.30-45. Move new-crop bean and corn sales to 30% at $13.60 and $5.80.

More By This Author:

2022 US Plantings Were Mixed, But March Corn & Bean Stocks Were LowerUS Planting Intentions/Q-STKS

Reaction To USDA's March 2023 Prospective Plantings And Grain Stocks

Comments

Log in or sign up to join the conversation.