This coming week marks the return of Treasury bill net issuance. We had been in a period of paydowns, where the Treasury was issuing fewer bills than were maturing, and that flips in July back to net issuance, with the Treasury offering more bills than are maturing. This week brings about $39 billion in net new issuance, with $17 billion on Tuesday the 7th and another $12 billion on Thursday the 9th.

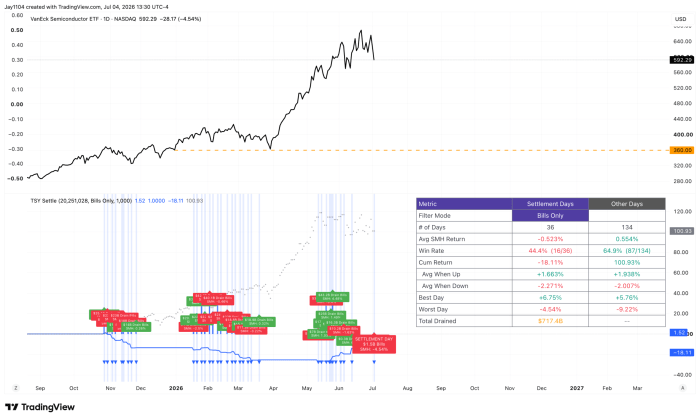

The reason we care so much about this is what tends to happen on Treasury bill settlement dates. Going back to the end of October, semiconductors have risen only 40% of the time on settlement dates, with the SMH down 52 basis points on average. On non-settlement dates, the SMH has risen 65% of the time, with an average gain of 55 basis points.

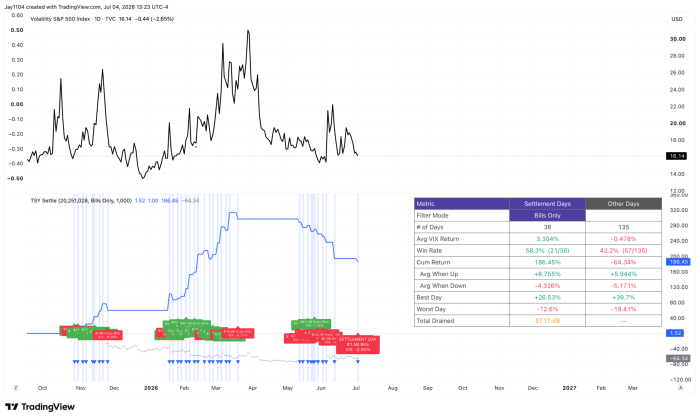

Interestingly, Treasury bonds have performed better on bill settlement dates than on non-settlement dates, while the VIX has risen on settlement days 58% of the time and declined 42% of the time. So it isn’t just that the market tends to go down on settlement dates; volatility tends to be higher, too.

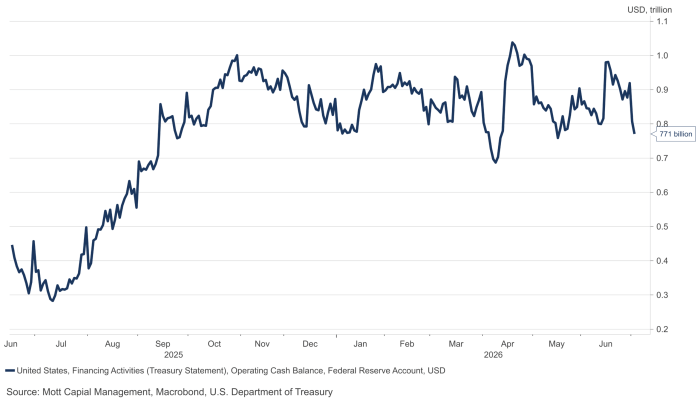

The reason this is happening now is that the TGA (the Treasury General Account, the government’s checking account at the Fed) has gone from about $1 trillion down to about $771 billion, and the Treasury now needs to rebuild it back toward the $1 trillion mark. The Treasury has already laid this out: modest reductions to short-dated bill auction sizes in June, around mid-month tax receipts, then incrementally larger bill auctions across the curve in July, continuing until we get closer to the September 15 tax date, when a period of paydowns is likely to return. Treasury estimates the TGA could peak at $1 trillion in late July and sit around $950 billion at the end of September.

The quarterly refunding documentation indicates about $348 billion in total bill issuance during the July-to-September quarter, so the sizes we’re seeing this week should continue to increase over the next several weeks and could become rather large. That likely means the TGA will begin to refill quickly, which will weigh on reserve balances, currently around $3.1 trillion. Those should get pushed back toward the $2.75 to $2.8 trillion range, possibly toward the lower end as we saw in October.

Comments

Log in or sign up to join the conversation.