Key Market Outlook(s) and Pick(s)

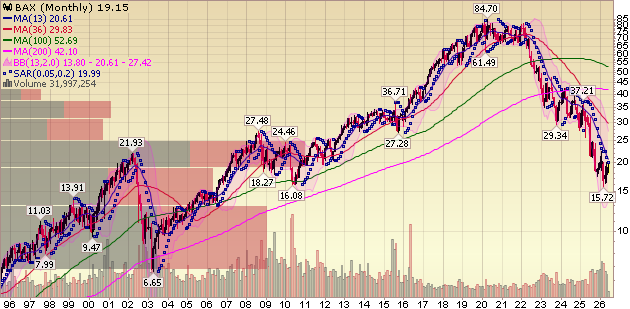

Baxter (BAX) Update

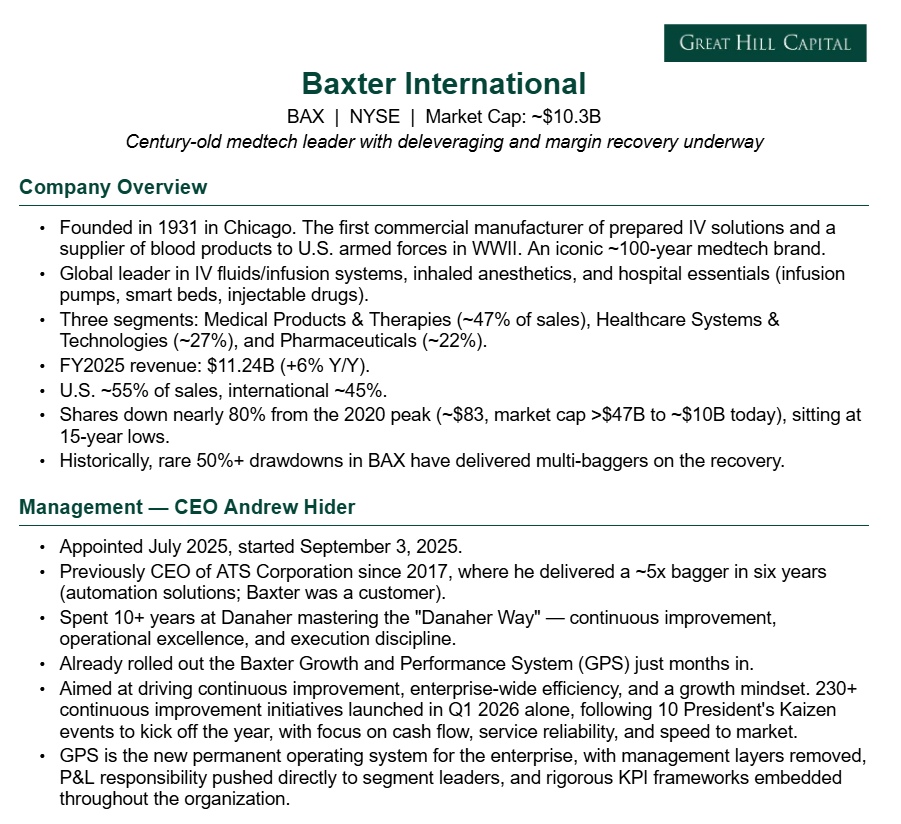

For newer readers, here’s a quick overview of the key drivers behind our thesis on Baxter, a century-old medtech leader where temporary headwinds and operational missteps have created an opportunity for a Danaher (DHR)-trained CEO to reset execution and restore normalized earnings power:

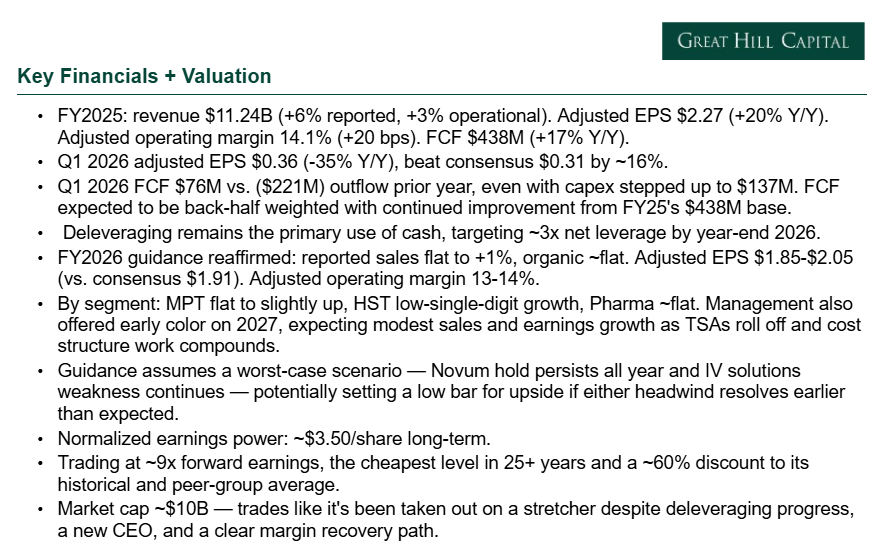

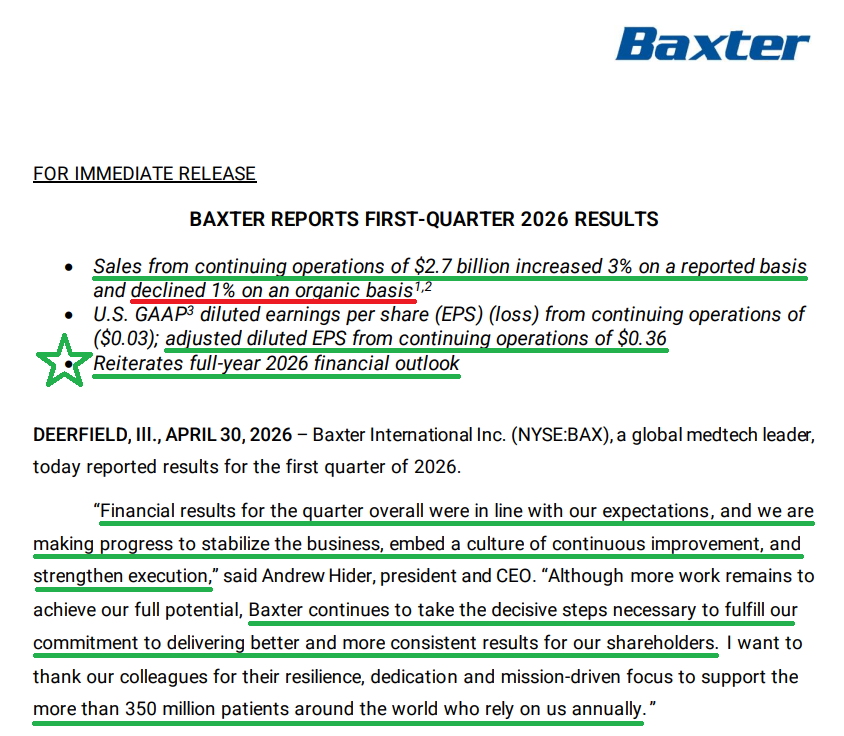

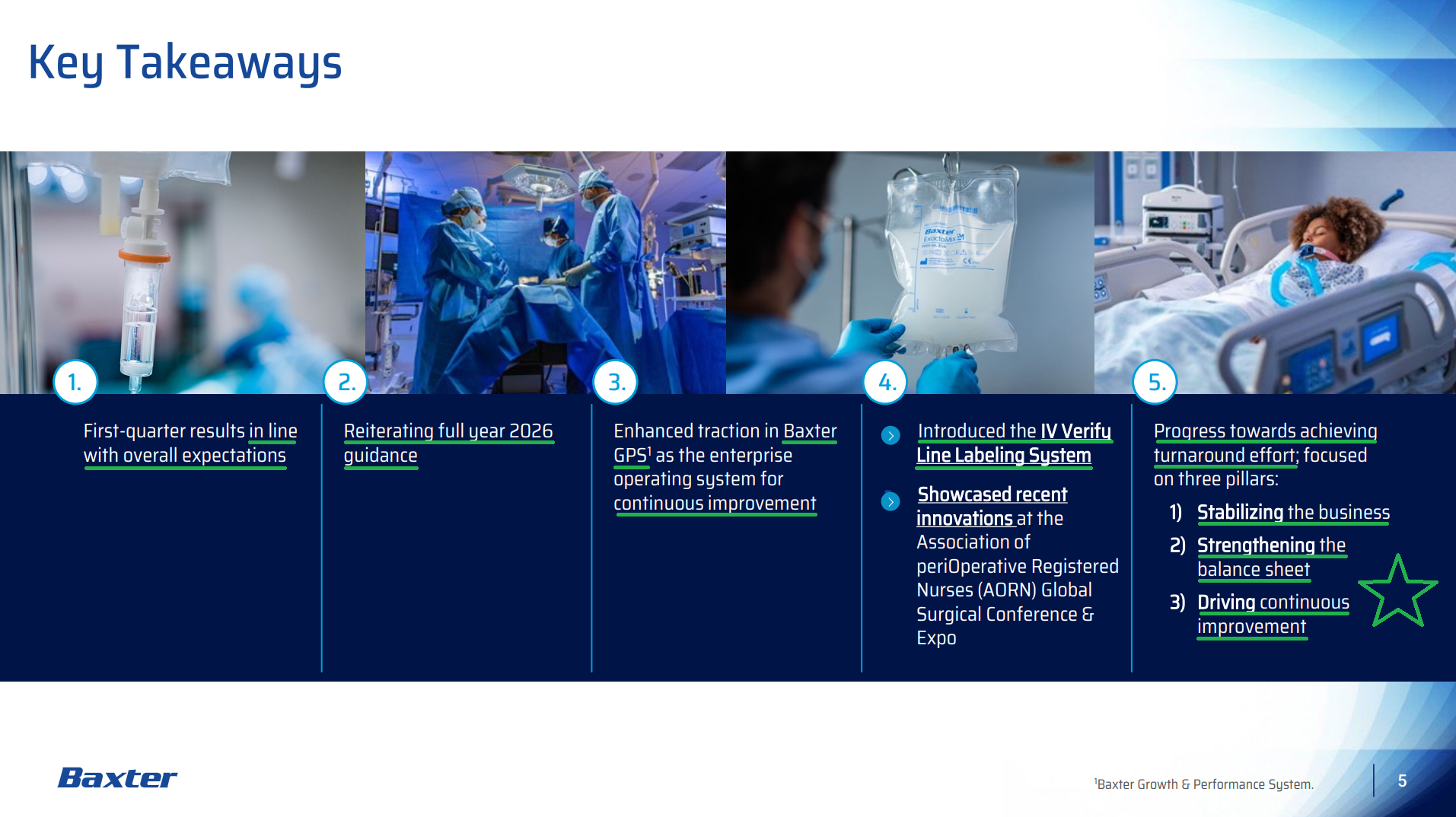

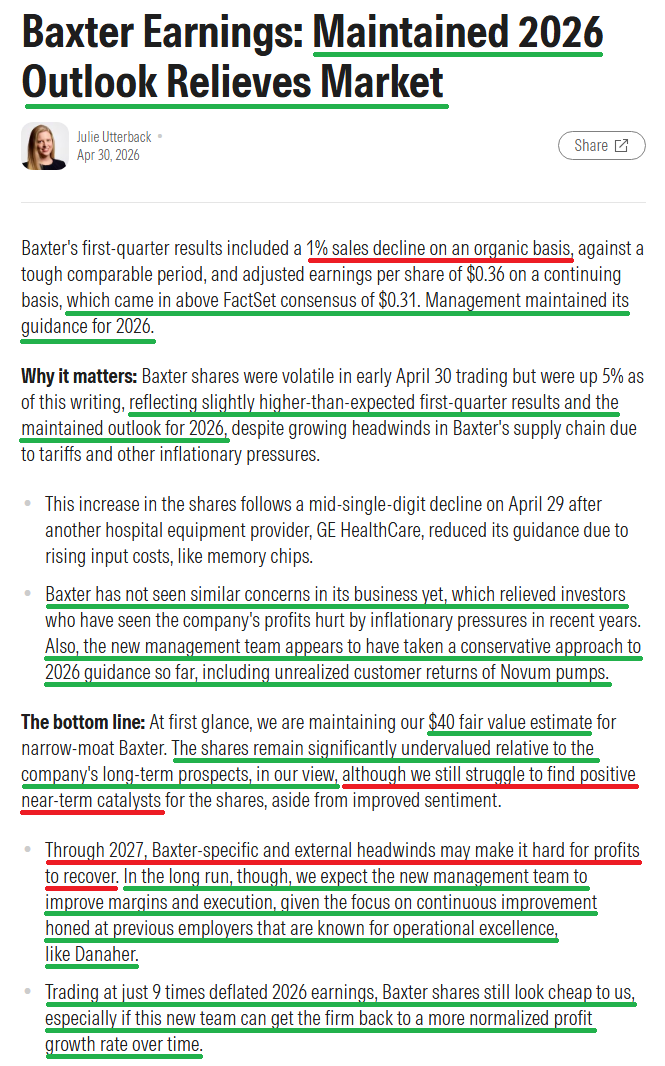

Baxter International delivered something we haven’t seen from the company in quite some time: a clean quarter of execution. Three quarters into CEO Andrew Hider’s tenure and following his initial kitchen-sink reset, the company beat on both the top line ($2.7B vs. $2.62B consensus) and bottom line ($0.36 vs. $0.31 consensus) while reaffirming full-year guidance.

That isn’t to say everything has been fixed overnight. Baxter is still working through several well-known overhangs, most notably the Novum IQ ship-and-hold issue and the IV Solutions reset. The key difference today is that these challenges are no longer open-ended risks but rather known issues that have been fully incorporated into guidance, creating a “worst-case” framework that sets a low bar for upside surprises should anything go right.

Most importantly, both issues remain temporary and fixable, and with the stock still down ~75% from its all-time highs, we believe investors are being more than compensated to wait while management works through them.

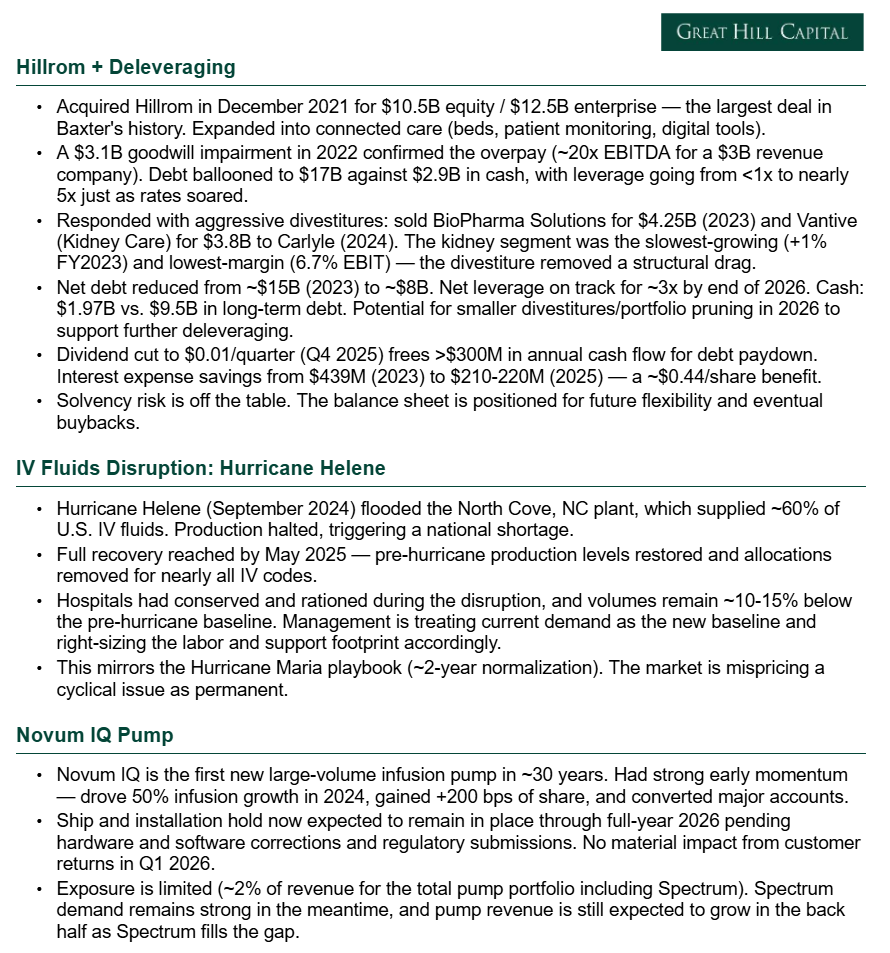

On the Novum IQ front, management is still assuming the ship-and-hold remains in place through year-end as hardware and software correction efforts progress. So far, the company has yet to see a material impact from customer returns, a positive sign that customers are willing to stick with Baxter through the correction process and further supports our belief that the situation is manageable. While management continues to prudently incorporate the possibility of higher customer returns into full-year guidance, it is worth remembering that the entire infusion pump portfolio accounts for only ~2% of company sales, limiting overall exposure. Encouragingly, Spectrum is seeing strong customer demand and is helping offset the Novum overhang, which management expects will allow the overall pump franchise to return to growth as recall-related headwinds are lapped in the back half of the year.

Meanwhile, the IV Solutions business has largely been right-sized for a new baseline demand environment that sits ~10% to 15% below historical levels. With the cost structure adjusted accordingly and volume comps becoming normalized, management expects the business to return to a steady low single-digit growth profile beginning in the back half of the year.

Investors also received some welcome news on the macro front, where exposure to oil and memory chip shortages, both of which plagued the company during the 2022 downturn, appear increasingly manageable today. Revenue exposure to the Middle East remains below 2% of sales, while Baxter’s exposure to oil-related input costs has been cut by more than half following the Kidney Care divestiture. At the same time, management reported no material disruptions related to memory chip supply constraints.

All positive developments. But at the end of the day, the investment case ultimately comes down to controlling what Baxter can control, and that comes back to execution.

After years of operational missteps, surprise headwinds, and guidance cuts, the path forward is relatively straightforward: rebuild credibility by consistently delivering on what management says it will do. We continue to believe that a handful of clean quarters of execution will go a long way toward setting the stage for what should be Baxter’s first truly “normal” operating year in 2027.

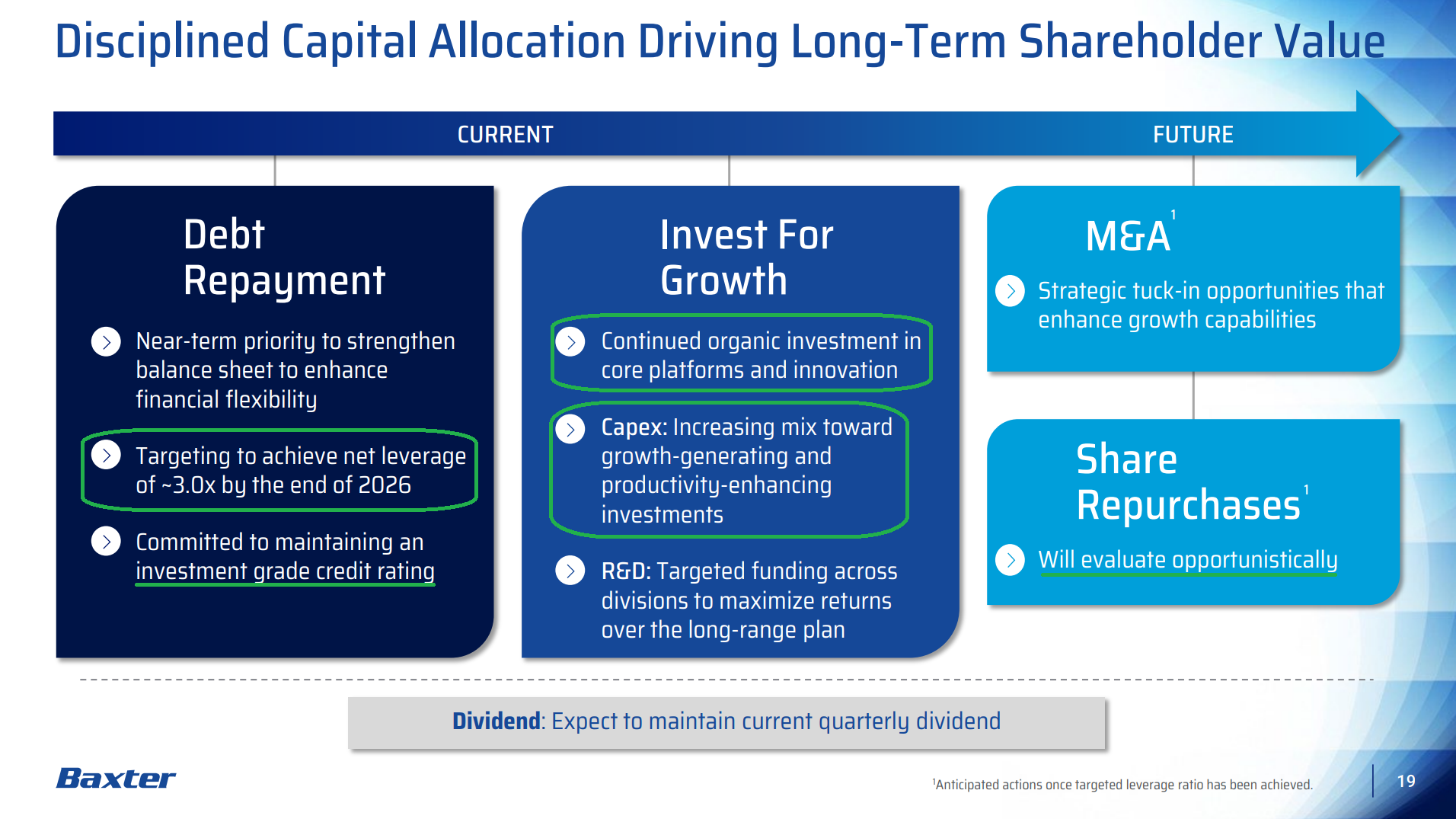

This is when stranded Kidney Care costs, currently the largest drag on overall profitability, finally begin to roll off. At the same time, Baxter will reach its long-awaited 3x net leverage target by year-end 2026, cost structure initiatives will be fully reflected in the run rate, and both the IV Solutions reset and Novum recall will be firmly in the rearview mirror.

Combined, these factors position Baxter for a return to low single-digit growth and the first steps toward a recovery in normalized earnings power, with the stock price following alongside.

Getting there is all about near-term execution, which is precisely what Hider was brought in to deliver. Taking a page from the Danaher playbook and drawing on the decade he spent there, Hider is bringing a culture of continuous improvement, operational discipline, and accountability to a Baxter that has been long overdue for all three.

At the end of the day, this isn’t a business that requires reinventing the wheel or putting data centers on the moon. This is IV bags, infusion pumps, hospital beds, and the like. Boring is beautiful, and for the first time in a long time, Baxter is starting to look the part.

Q1 Earnings Breakdown

10 Key Points

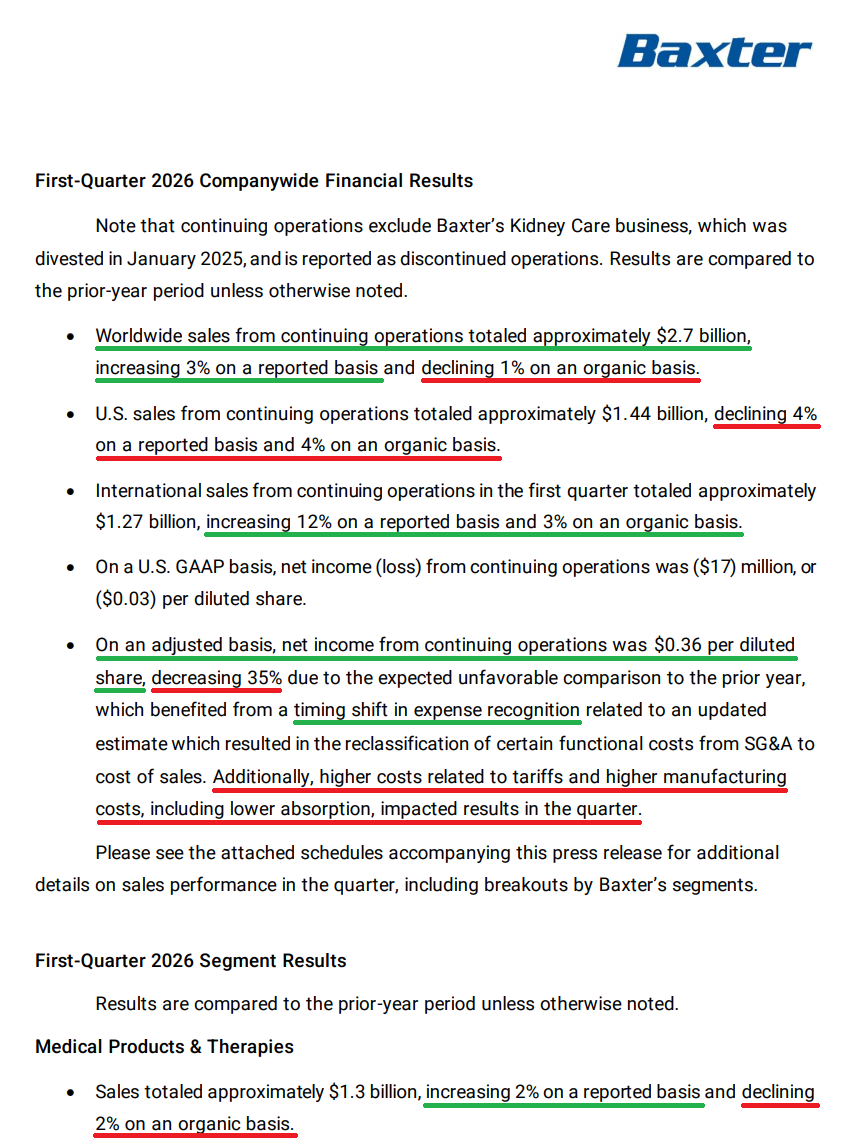

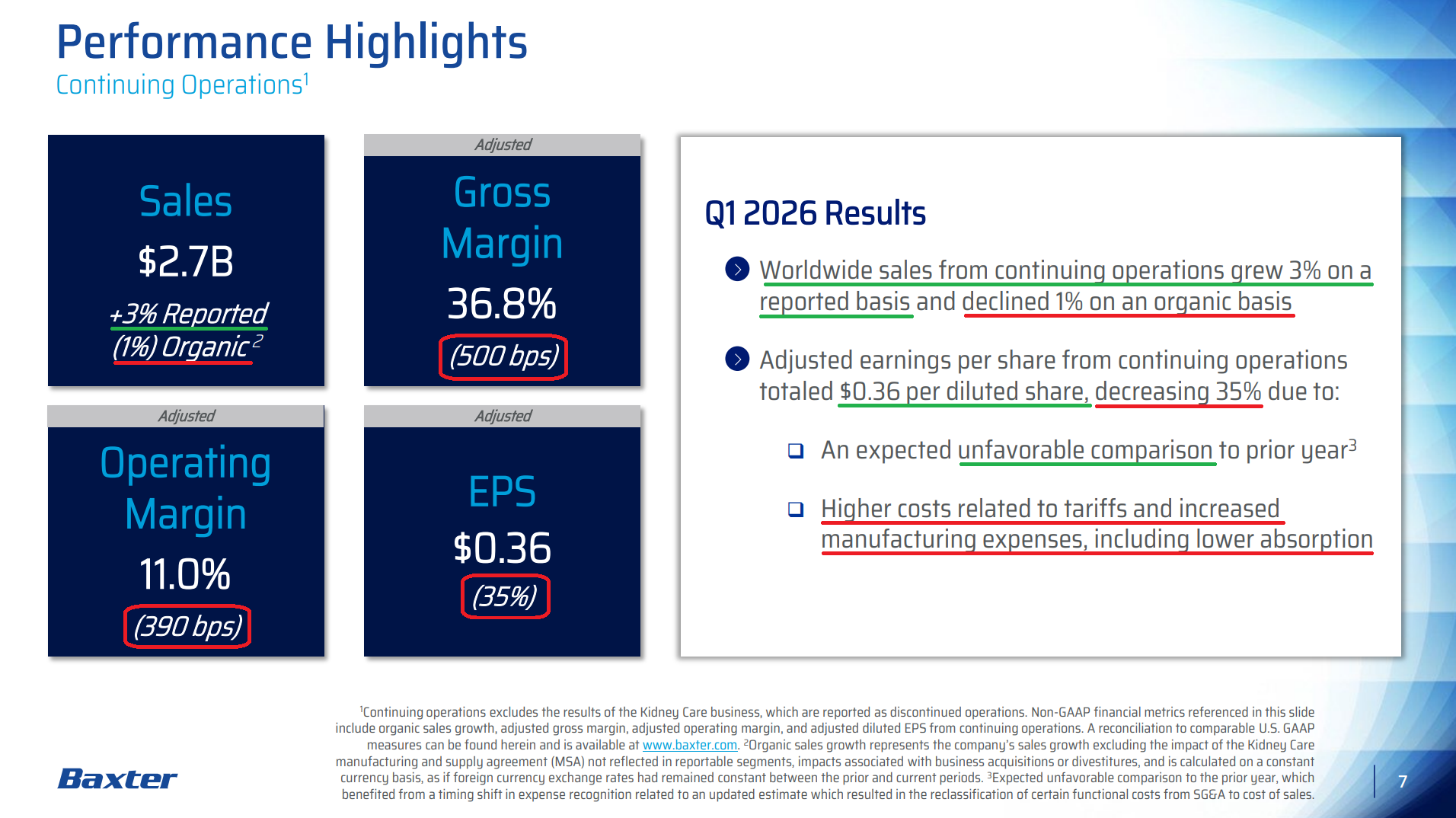

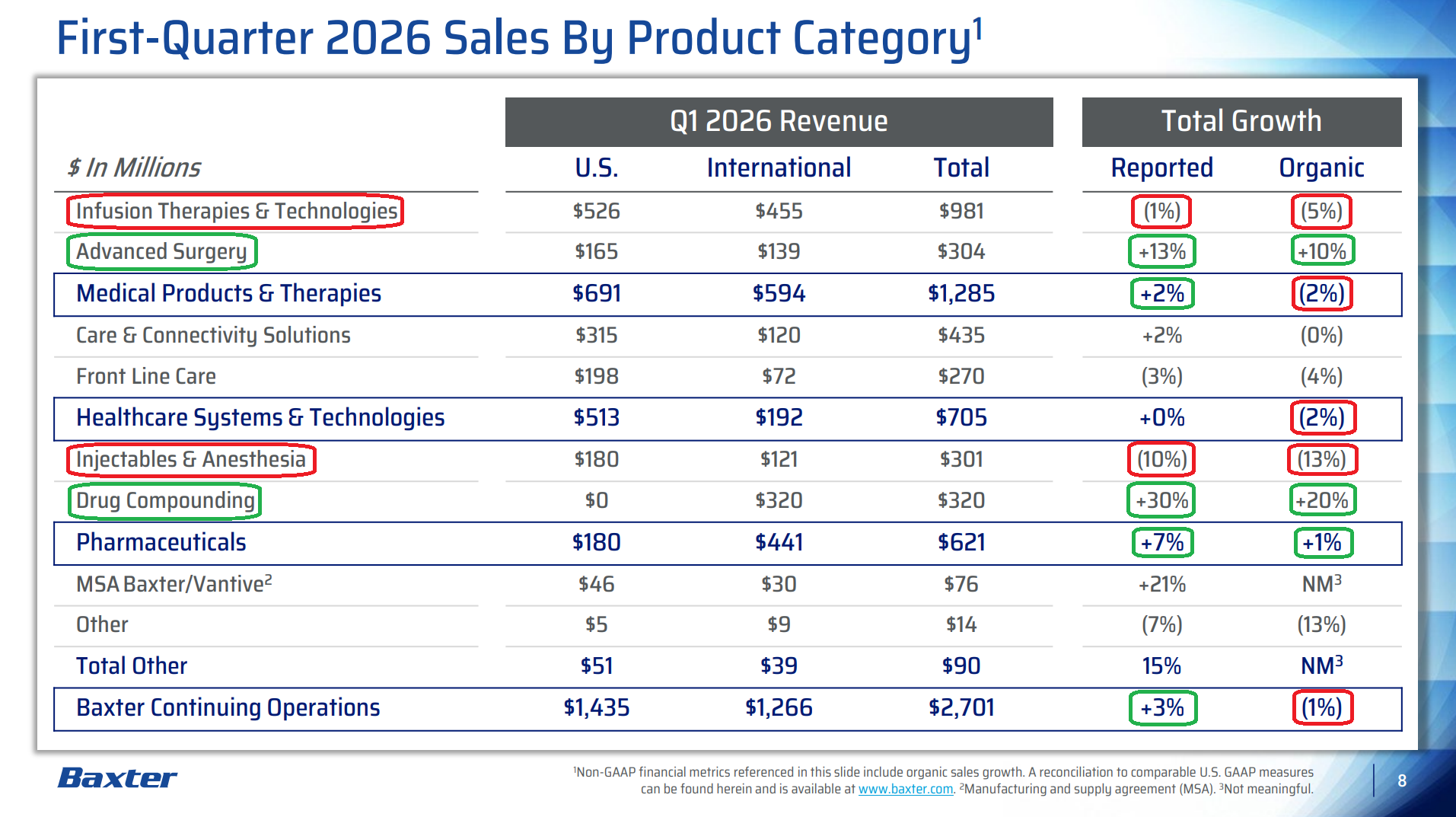

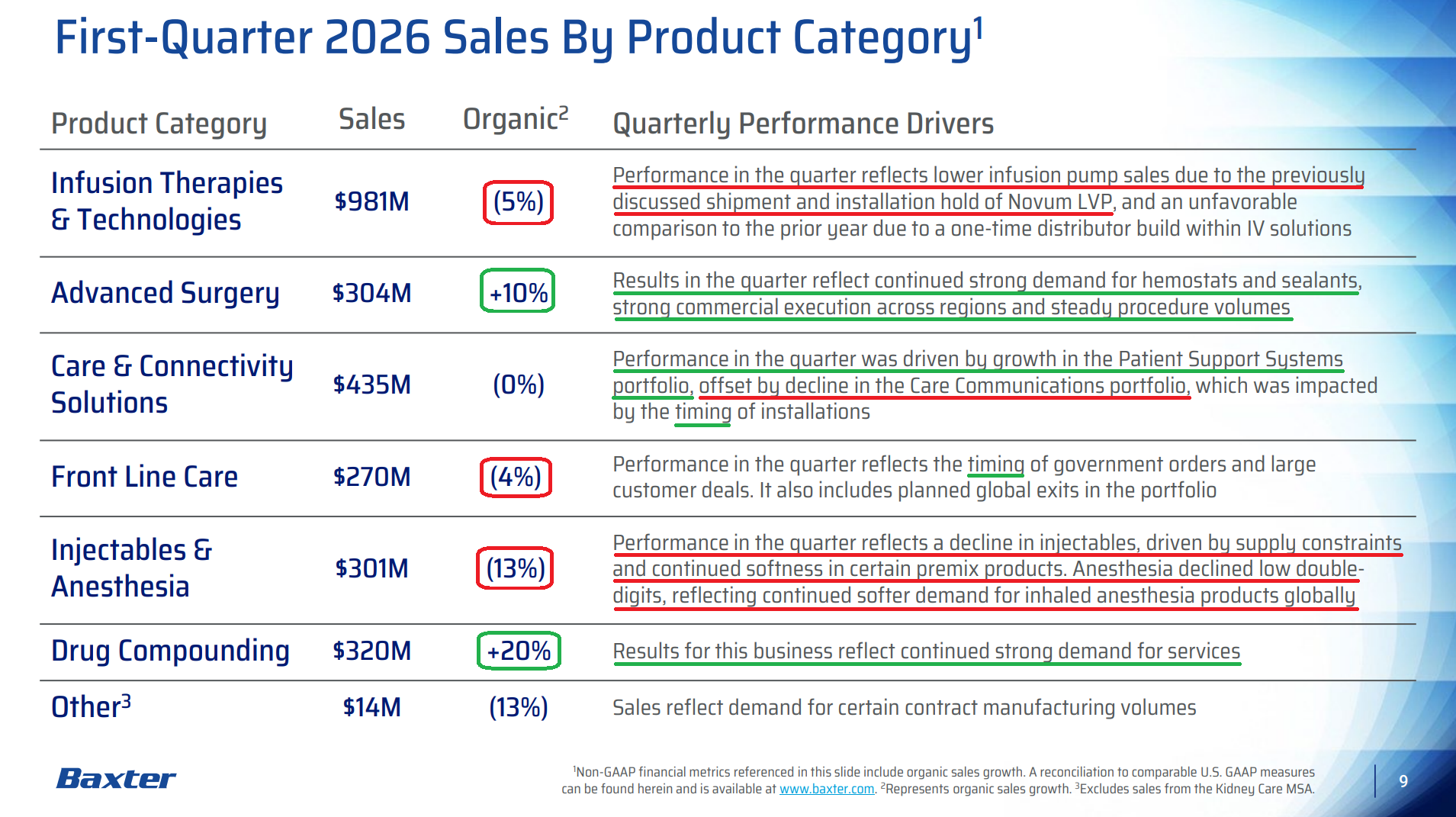

1) Revenue came in at $2.7B (+3% reported, -1% organic), beating consensus of $2.62B by ~$80M. International sales of $1.27B grew 12% reported and 3% organic, more than offsetting a 4% decline in U.S. sales to $1.44B. Adjusted EPS of $0.36 (-35% Y/Y) beat consensus of $0.31 by ~16%, with the year-over-year decline largely expected and driven by a ~$50M headwind from a prior-year timing shift in expense recognition, higher tariff costs, and lower manufacturing absorption.

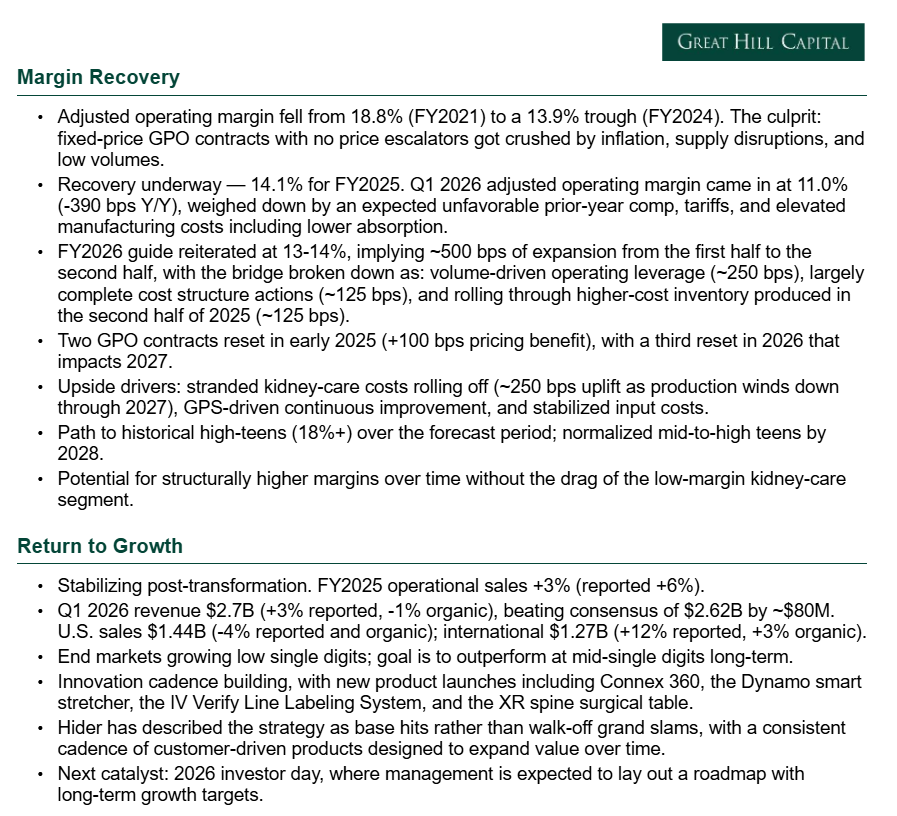

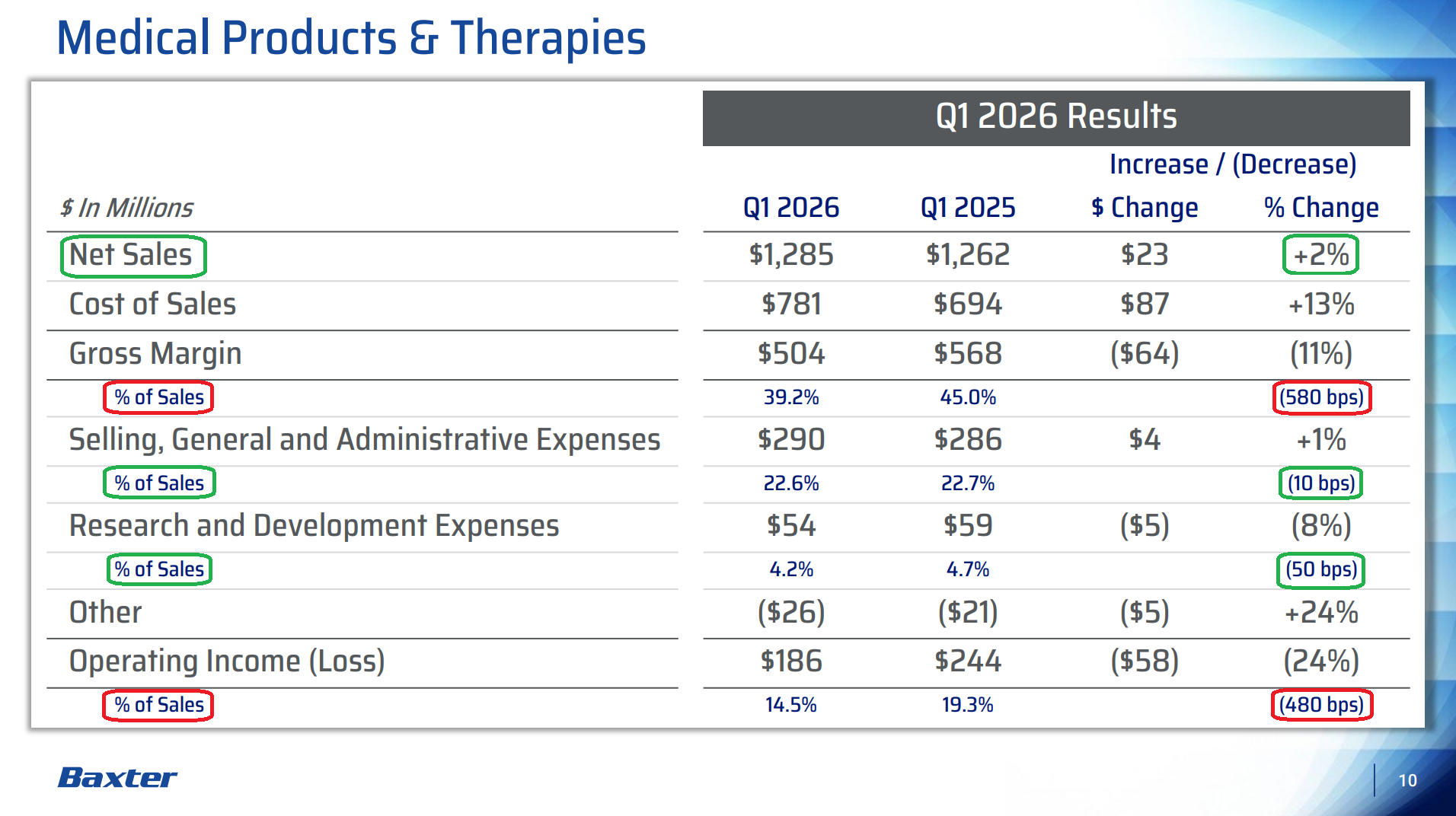

2) Adjusted operating margin came in at 11.0% (-390 bps), with adjusted operating income of $297M versus $392M in the prior year, beating consensus of $273.7M. The decline was driven by the same headwinds impacting EPS, including the prior-year cost reclassification, tariffs, and elevated manufacturing costs, including lower absorption. Management reiterated full-year adjusted operating margin guidance of 13% to 14% (vs FY25 14.1%), implying ~500 bps of expansion from the first half to the second half, driven by volume-related operating leverage (~250 bps), benefits from cost structure actions that are largely complete (~125 bps), and the rollover of higher-cost inventory produced in 2025 (~125 bps).

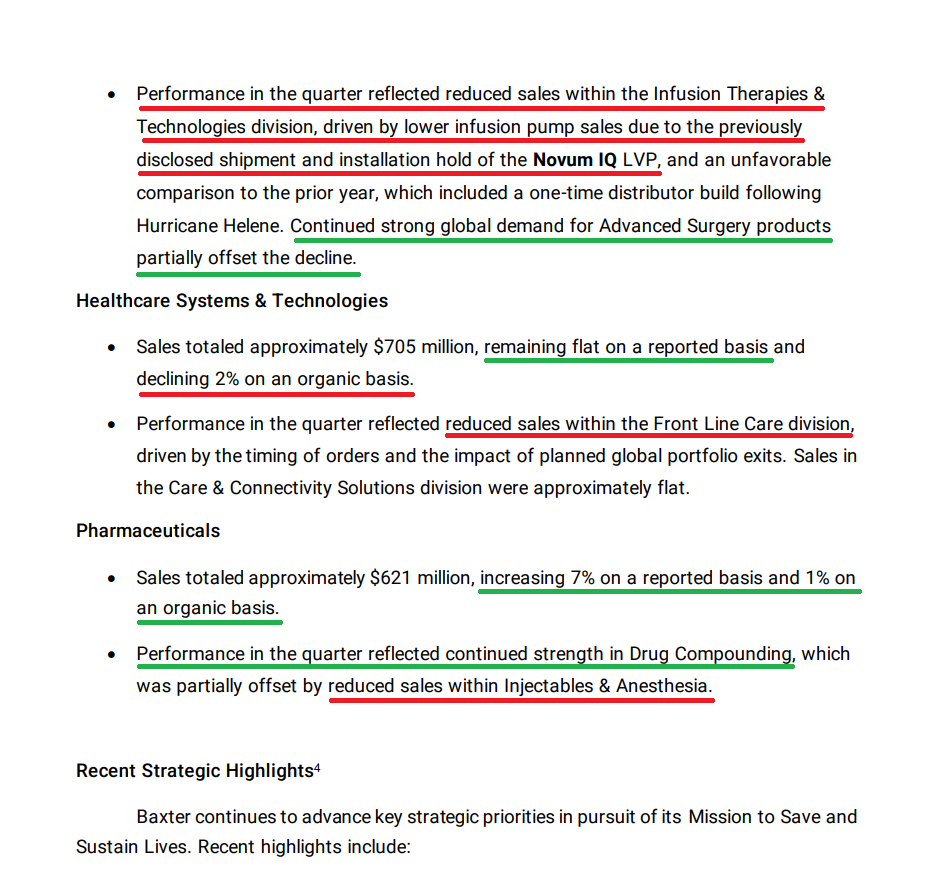

3) Advanced Surgery continues to build momentum and deliver strong results, with sales of $304M growing 10% organically, driven by sustained global demand for hemostats and sealants, solid commercial execution, and steady procedure volumes. Within the broader MPT segment, Advanced Surgery strength helped partially offset the -5% organic decline in Infusion Therapies & Technologies to $981M, which was pressured by Novum-related headwinds and a tough prior-year comp tied to a one-time post-Hurricane Helene distributor build in IV solutions. On IV solutions, management acknowledged that clinical practice changes have established a new demand baseline running ~10% to 15% below historical levels, and the company has taken steps to right-size its support footprint and align labor with current volumes.

4) The Novum IQ shipment and installation hold remains in place and is expected to continue for the full year, with hardware and software corrections still being finalized ahead of regulatory submissions. Management noted no material impact from customer returns in Q1, while maintaining the assumption of potential returns in full-year guidance out of prudence. The total pump portfolio, including Novum and Spectrum combined, represents less than 2% of sales, limiting overall exposure. Management continues to see strong customer interest in the Spectrum LVP pump and broader offerings, with pump revenue expected to grow in the back half as Spectrum fills the gap left by Novum.

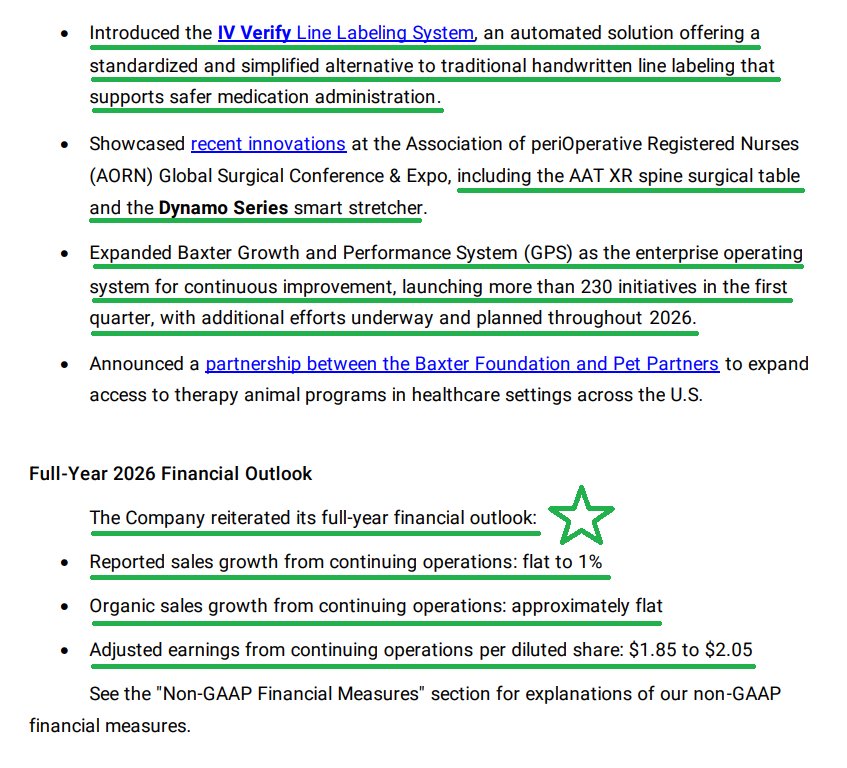

5) Adjusted R&D spending totaled $124M (4.6% of sales) in Q1, down from $138M (5.3% of sales) in the prior year, though Q1 is not reflective of the expected run-rate going forward, with targeted investment across divisions remaining a priority. New product momentum is building, with strong customer response and order growth from the Dynamo smart stretcher, continued traction from Connex 360, and two additional launches in the quarter, including the IV Verify Line Labeling System and the XR spine surgical table. Hider has been clear that innovation at Baxter will be measured and deliberate, describing the strategy as base hits rather than walk-off grand slams, with a consistent cadence of customer-driven products designed to expand value and drive growth over time.

6) Free cash flow came in at $76M in Q1, a strong improvement from the ($221M) outflow in the prior-year period, even with capex increasing to $137M from $122M a year ago. The improvement was driven by early progress in working capital efficiency and continued disciplined execution. Free cash flow is expected to remain back-half weighted, consistent with 2025’s pattern, with BAX continuing to expect improvement from FY25’s $438M base as it works back toward its historical ~80% cash conversion rate.

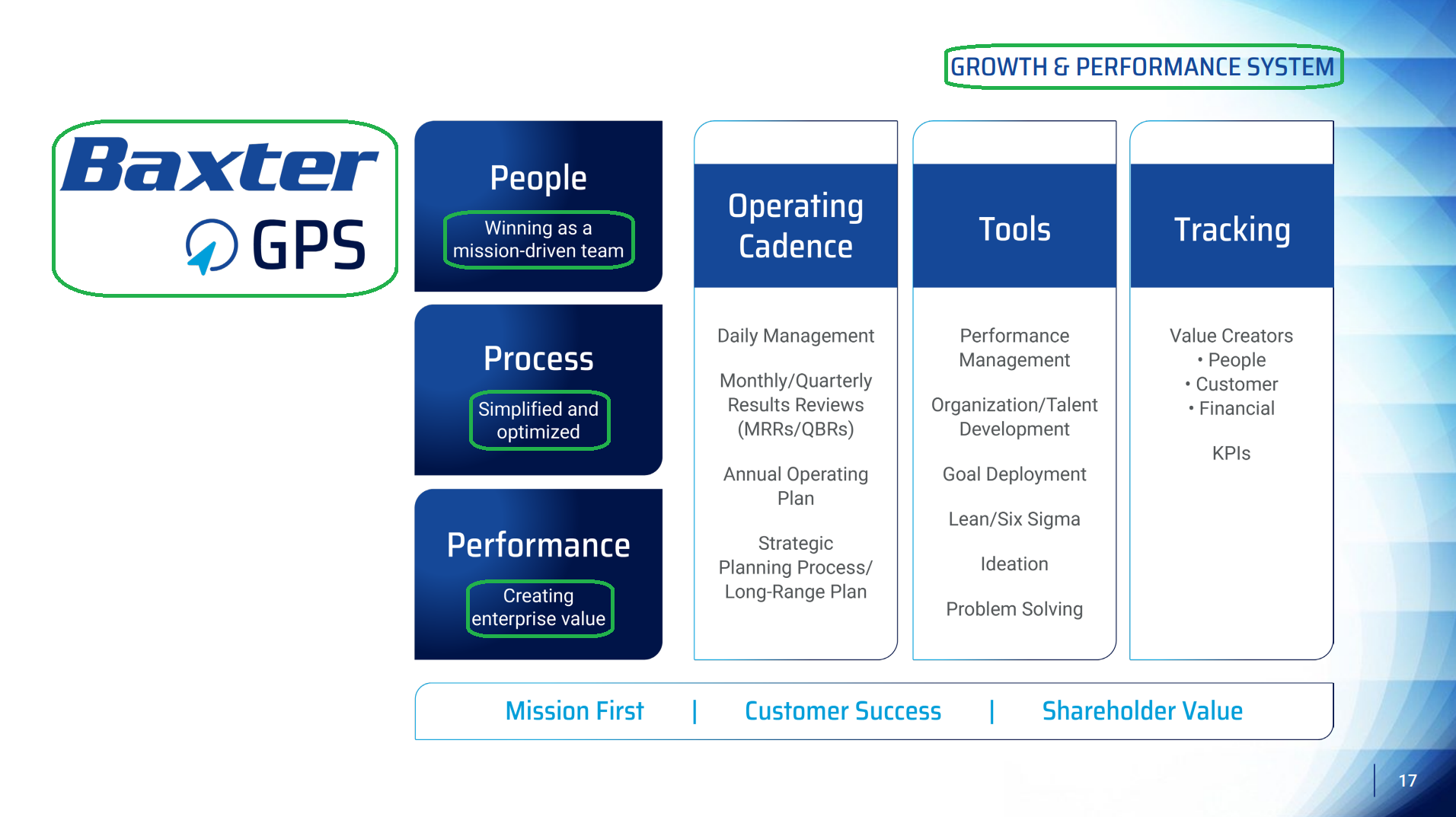

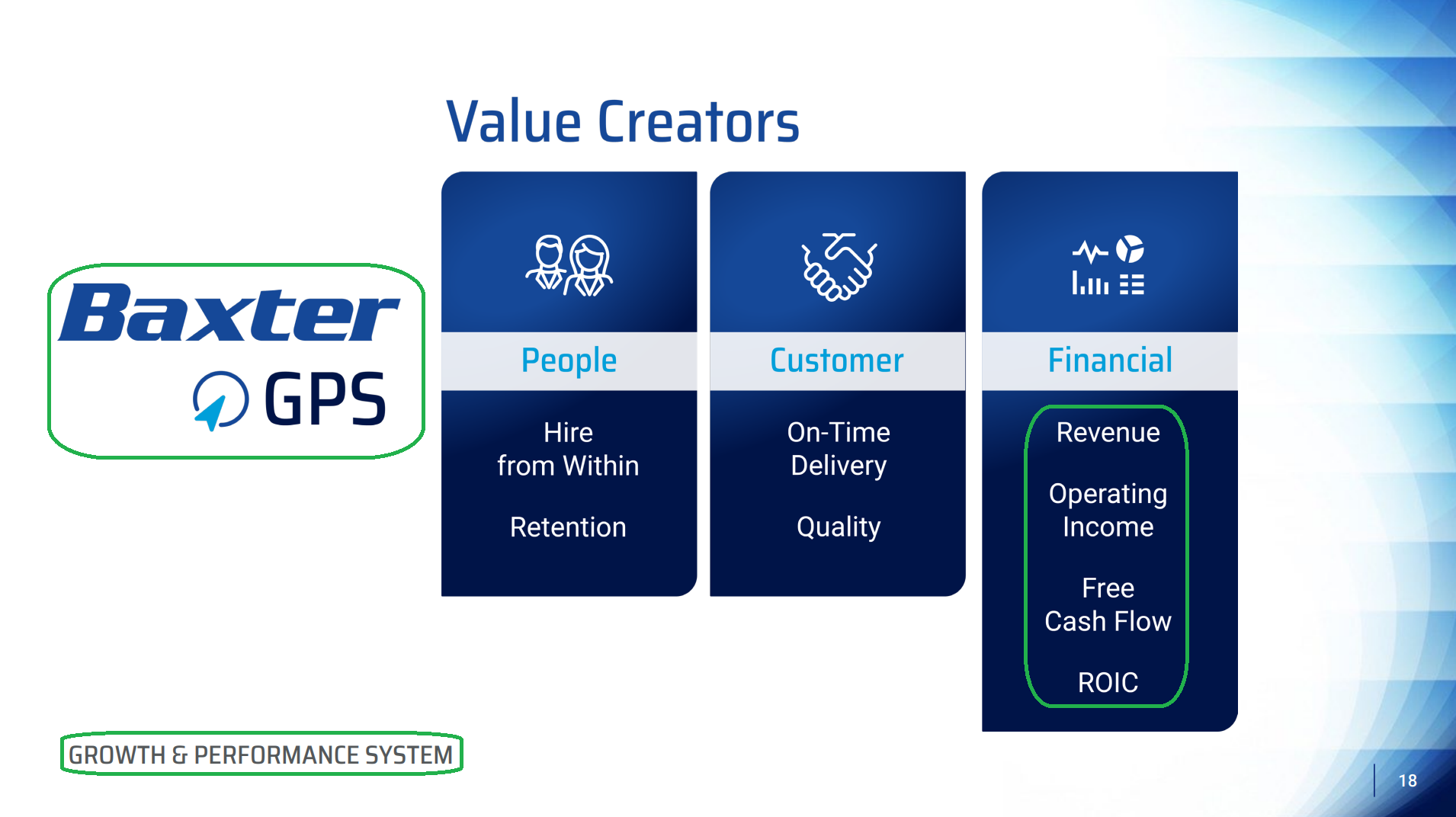

7) Baxter GPS continued to build traction in Q1, with more than 230 continuous improvement initiatives launched in the quarter. Management emphasized this is not a one-time program, with GPS positioned as the permanent operating system for the enterprise, including reduced management layers, P&L responsibility pushed directly to segment leaders, and rigorous KPI frameworks embedded throughout the organization.

8) Management addressed concerns over exposure to Middle East conflict, noting that Middle East revenue represents less than 2% of total sales and that fuel cost exposure has been cut by more than half following the Kidney Care divestiture, leaving overall commodity sensitivity more manageable than in prior years. Memory chip supply has seen no material shortages or disruptions to date, with dual sourcing and disciplined supplier engagement serving as active countermeasures. Management acknowledged BAX is not immune to macro pressures, but noted that if oil stays at current levels, the impact on 2026 is expected to be manageable and non-material.

9) Deleveraging remains the top near-term capital allocation priority, with management targeting ~3x net leverage by year-end 2026 while remaining committed to maintaining an investment-grade credit rating. Once the leverage target is reached, the framework opens up to strategic tuck-in M&A and opportunistic share repurchases.

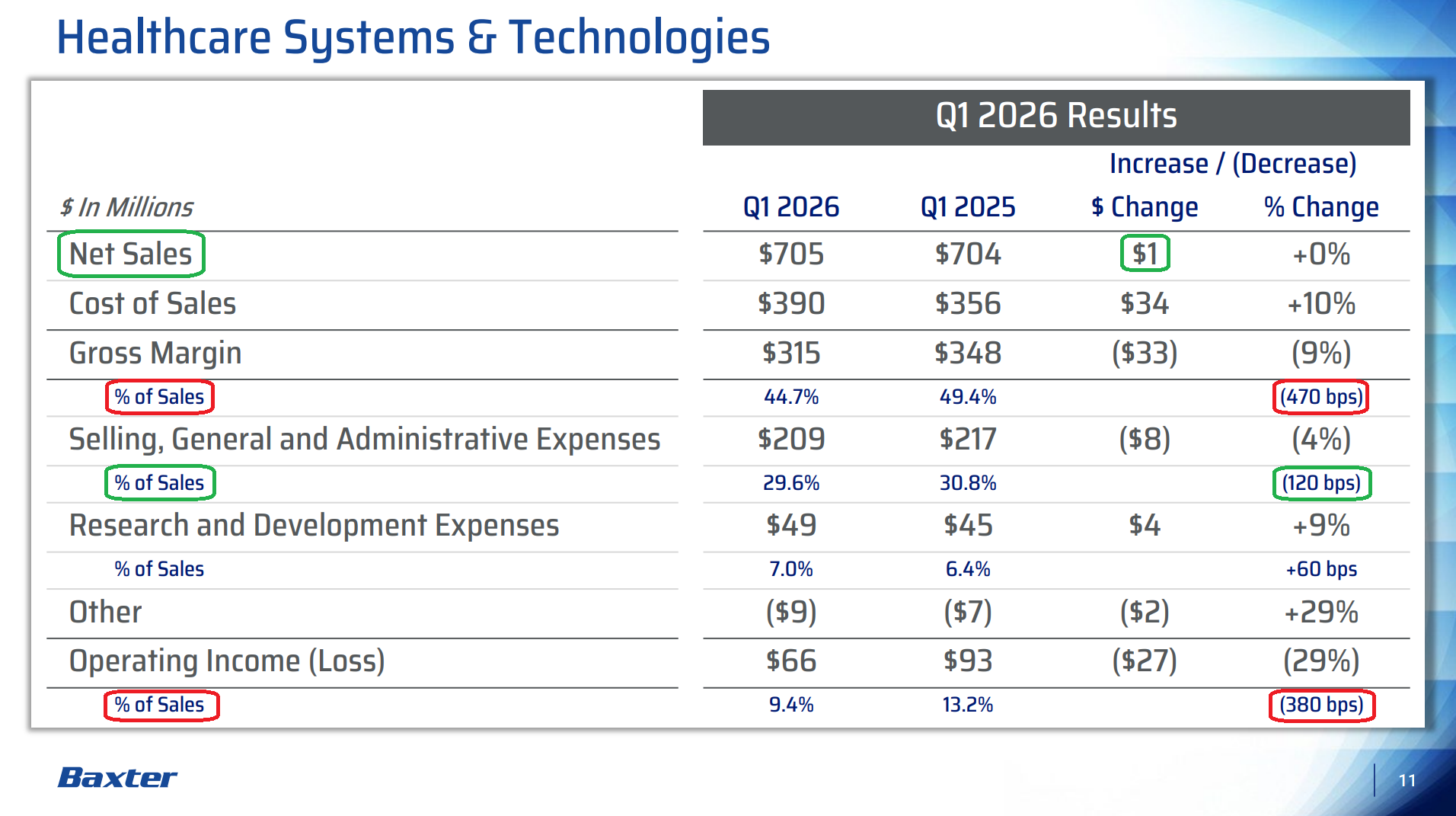

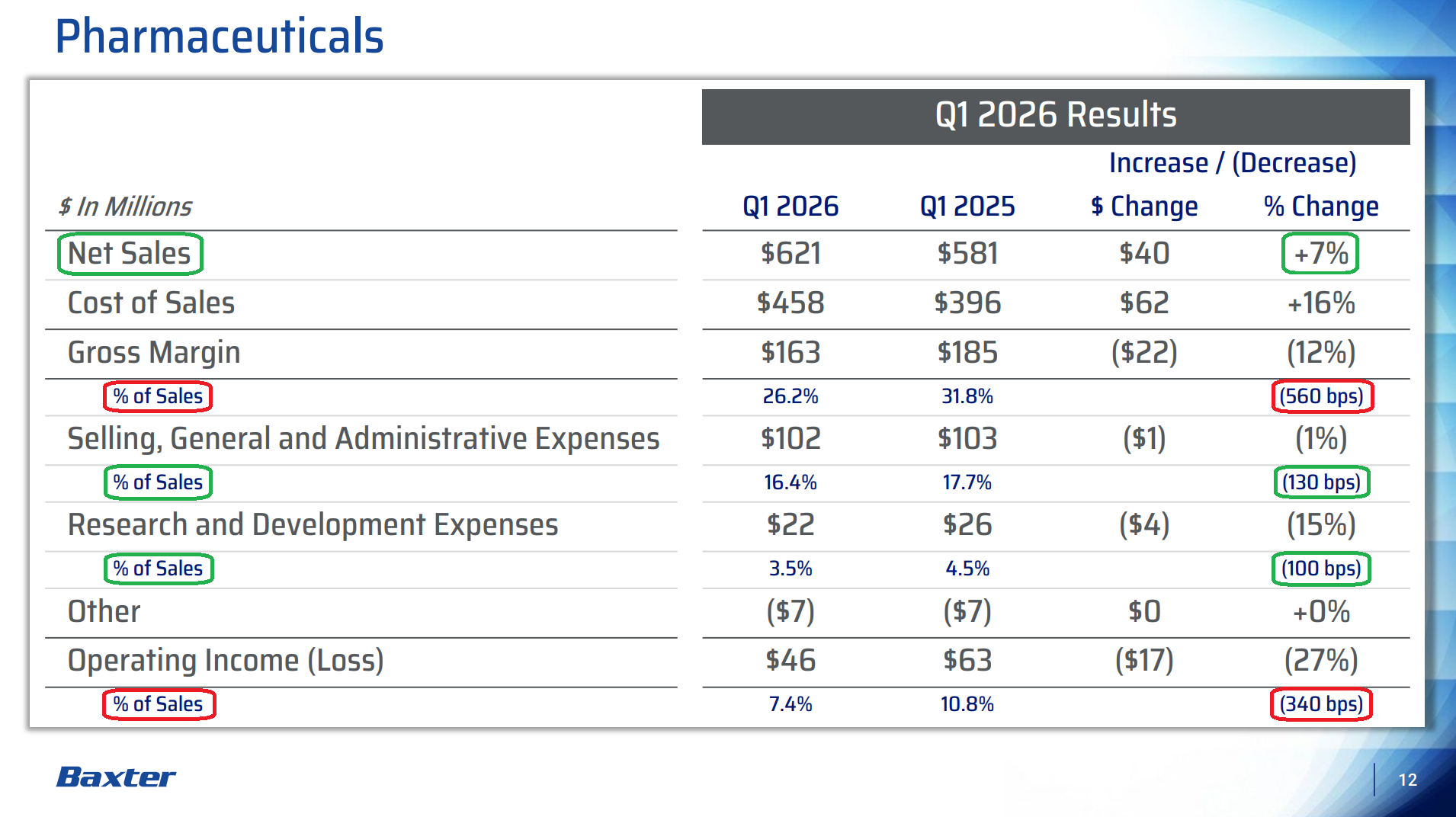

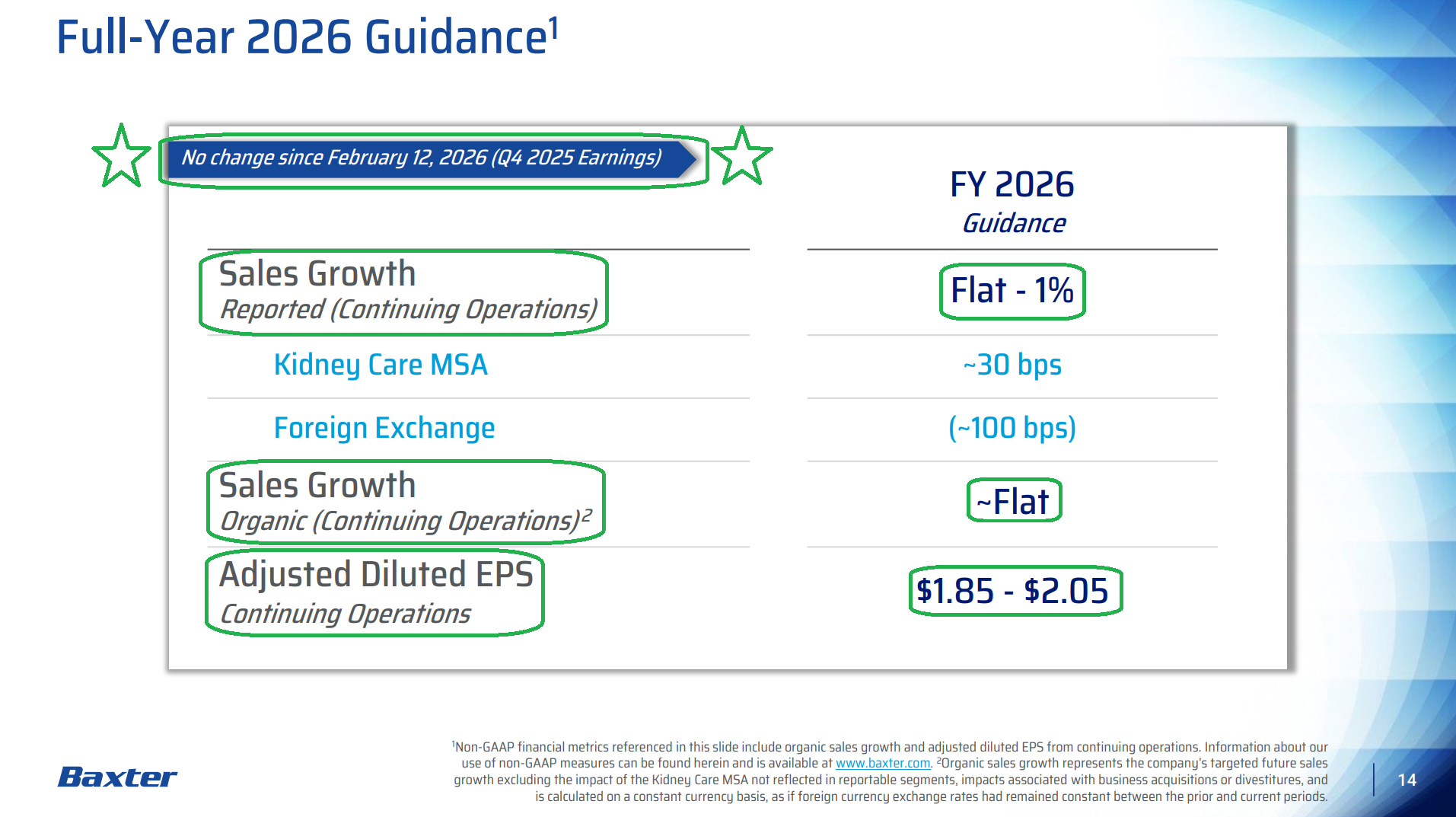

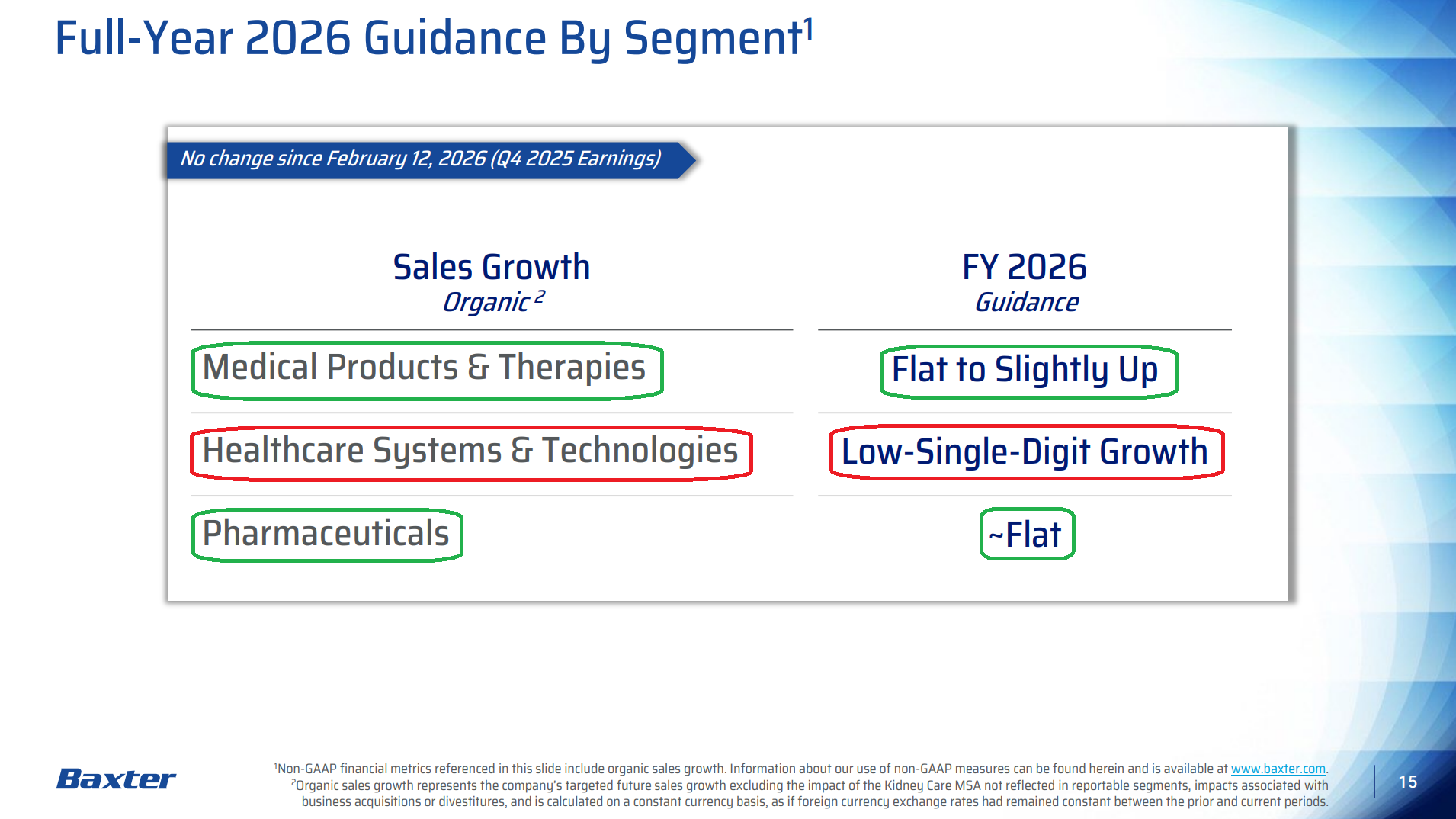

10) Management reiterated all components of its full-year 2026 guidance, with reported sales growth of flat to +1%, organic sales ~flat, and adjusted EPS of $1.85 to $2.05 (vs. consensus of $1.91). By segment, MPT is expected to be flat to slightly up, HST low-single-digit growth, and Pharmaceuticals roughly flat. Management also provided early color on 2027, expecting modest sales and earnings growth as TSA headwinds roll off and cost structure improvements compound.

Earnings Call Highlights

Morningstar (MORN) Analyst Note

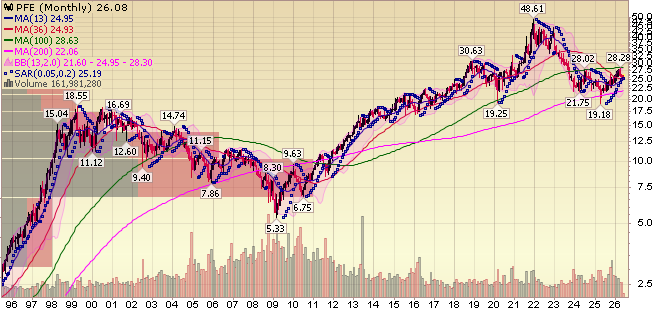

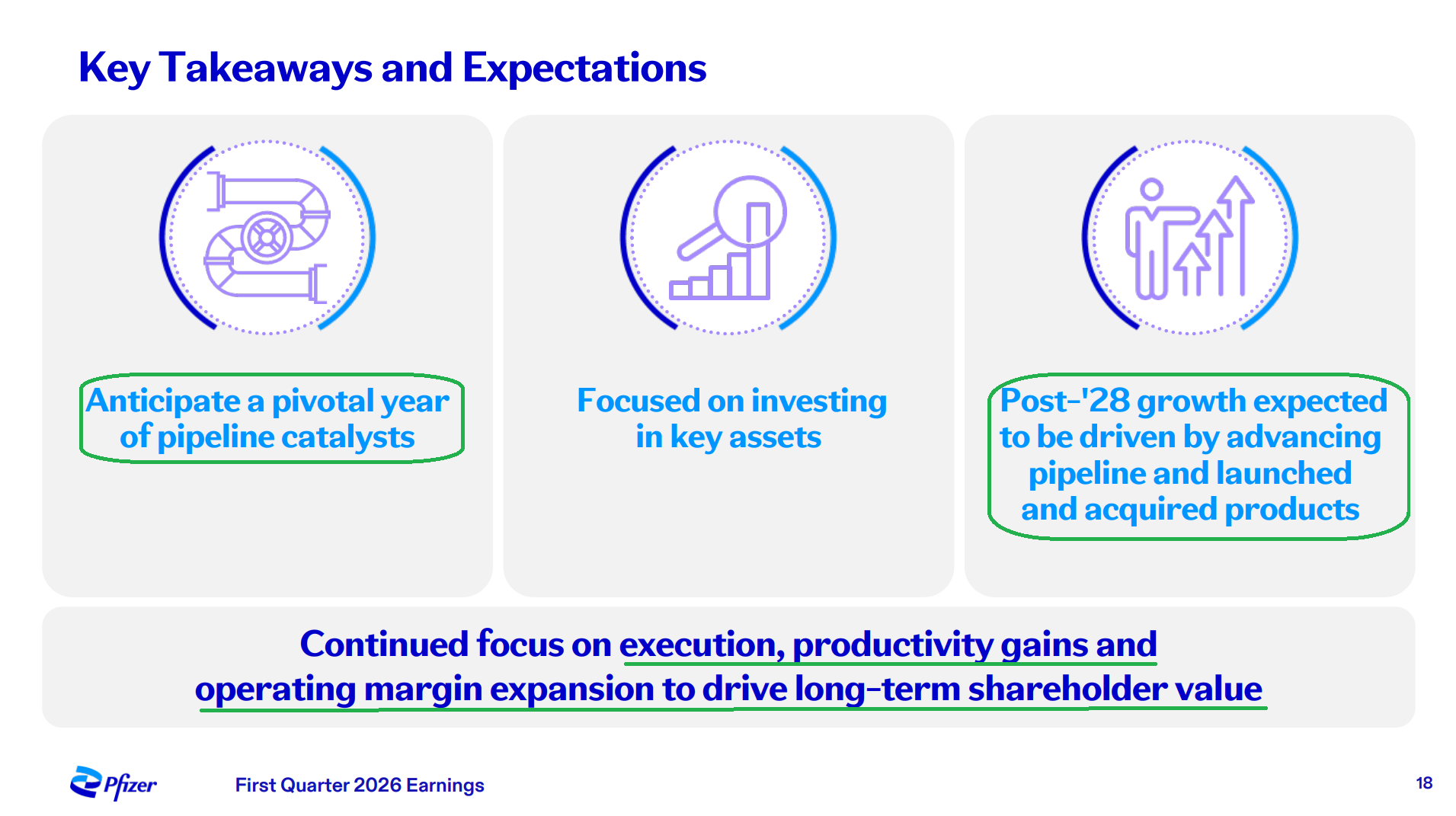

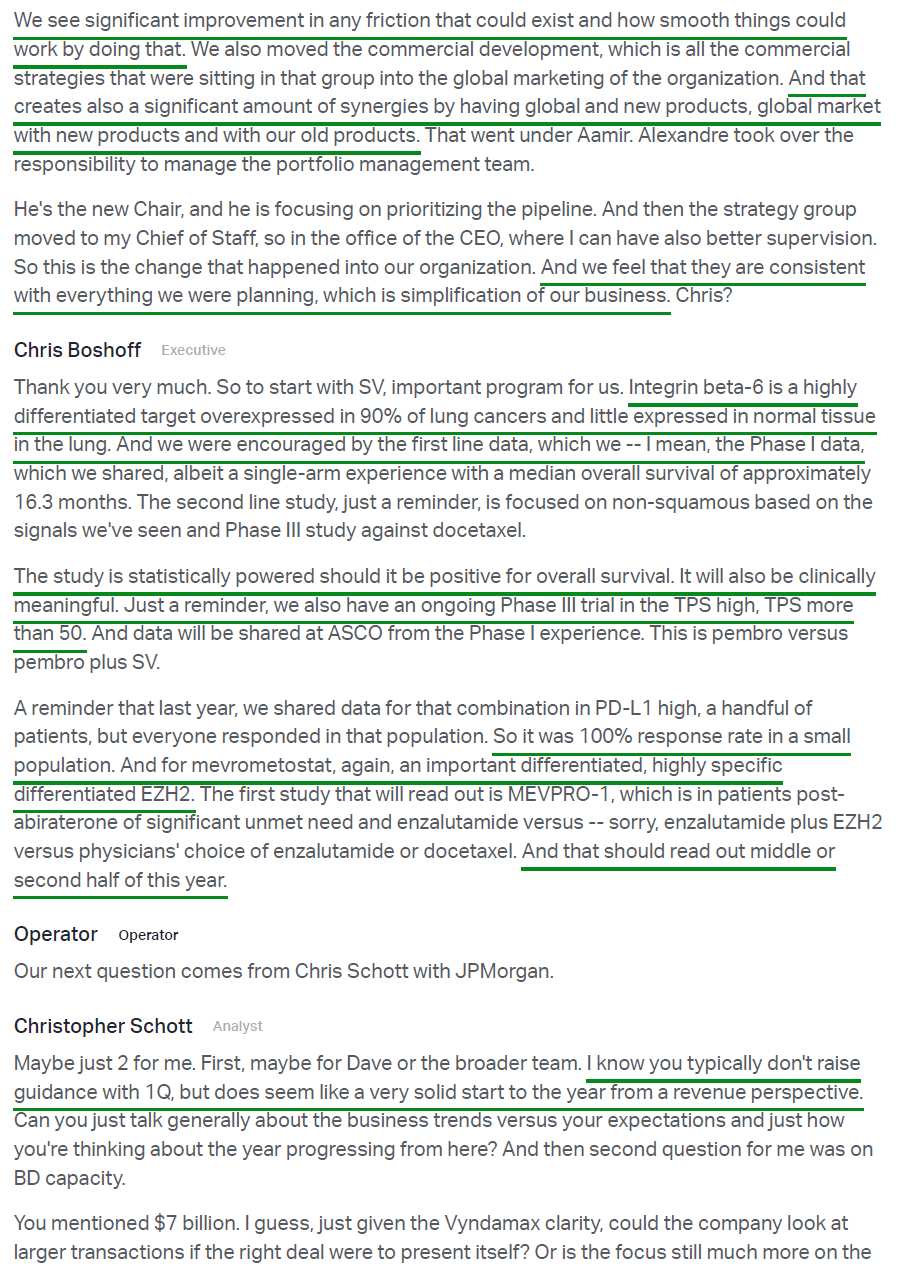

Pfizer (PFE) Update

For newer readers, here’s a quick overview of our thesis on Pfizer, a 176-year pharma giant navigating a post-COVID earnings reset, where disciplined cost management and a pipeline built around oncology and obesity are laying the groundwork for a post-LOE recovery:

Q1 Earnings Breakdown

10 Key Points

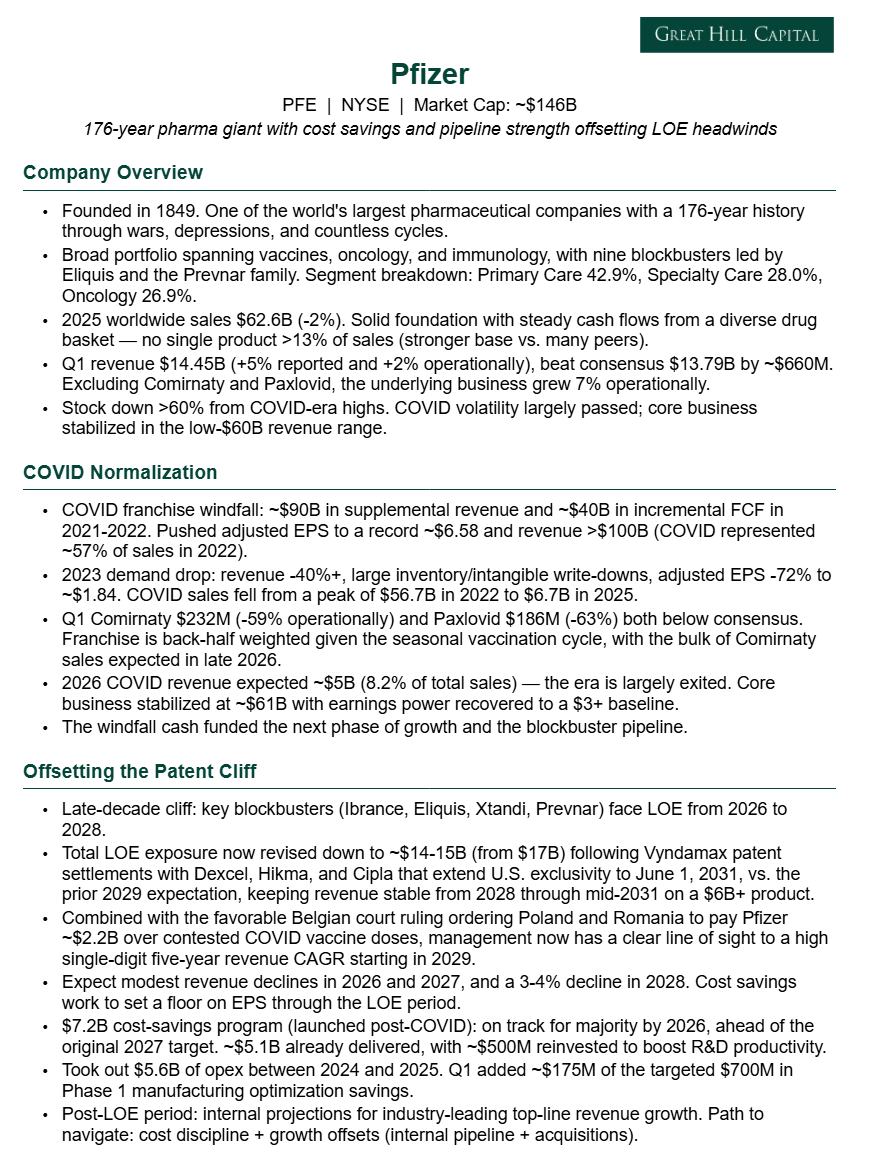

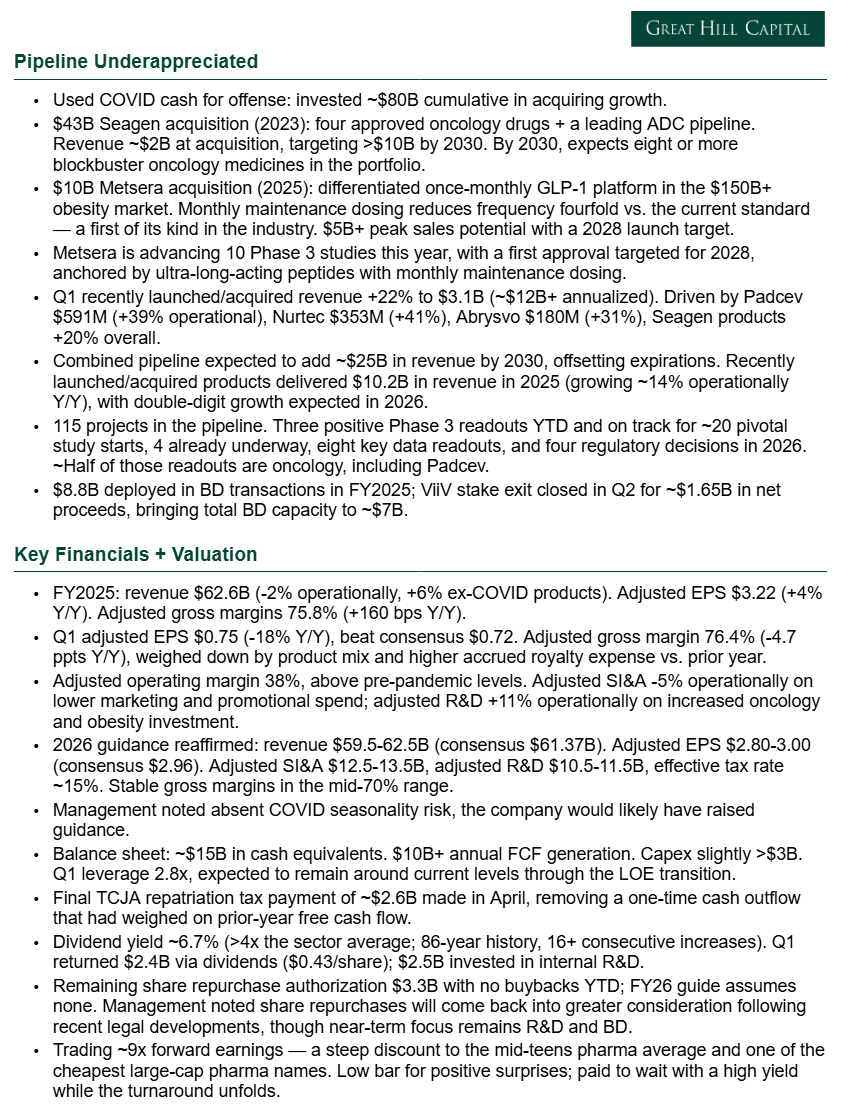

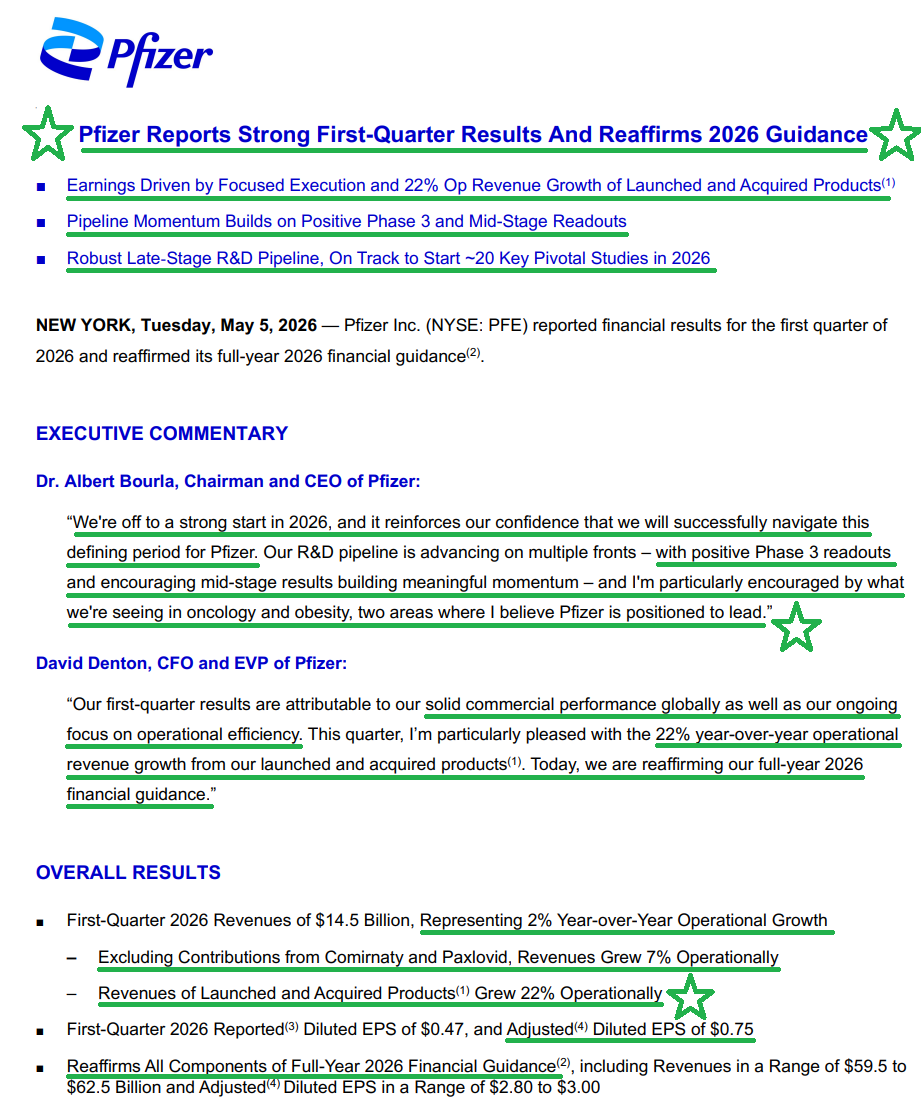

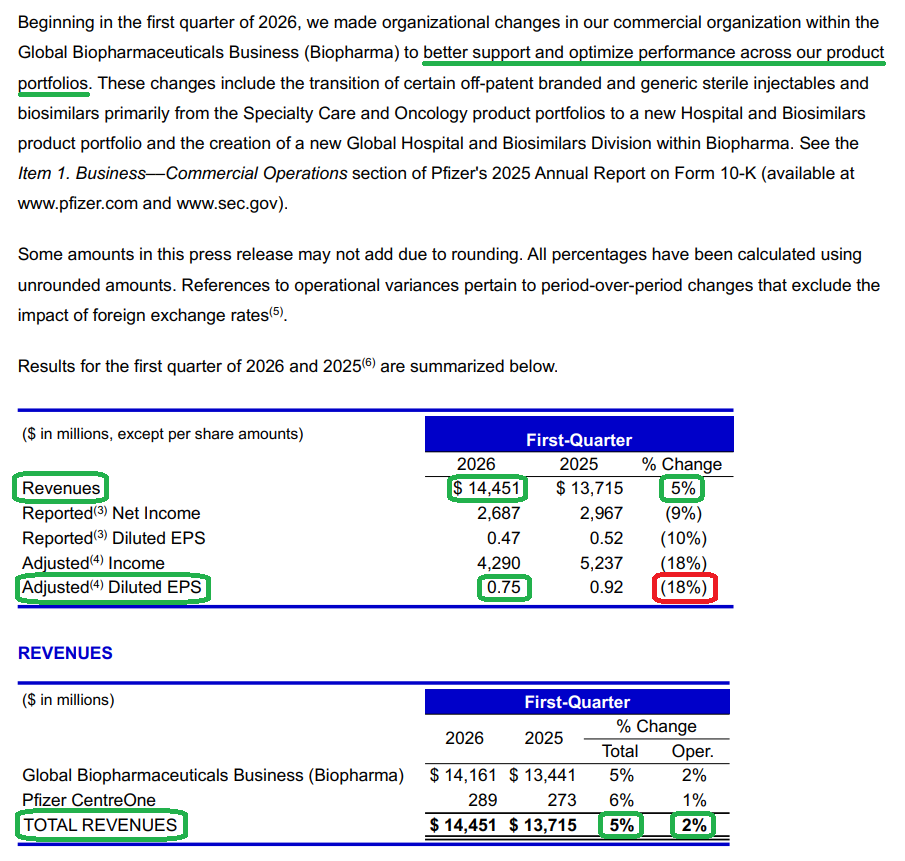

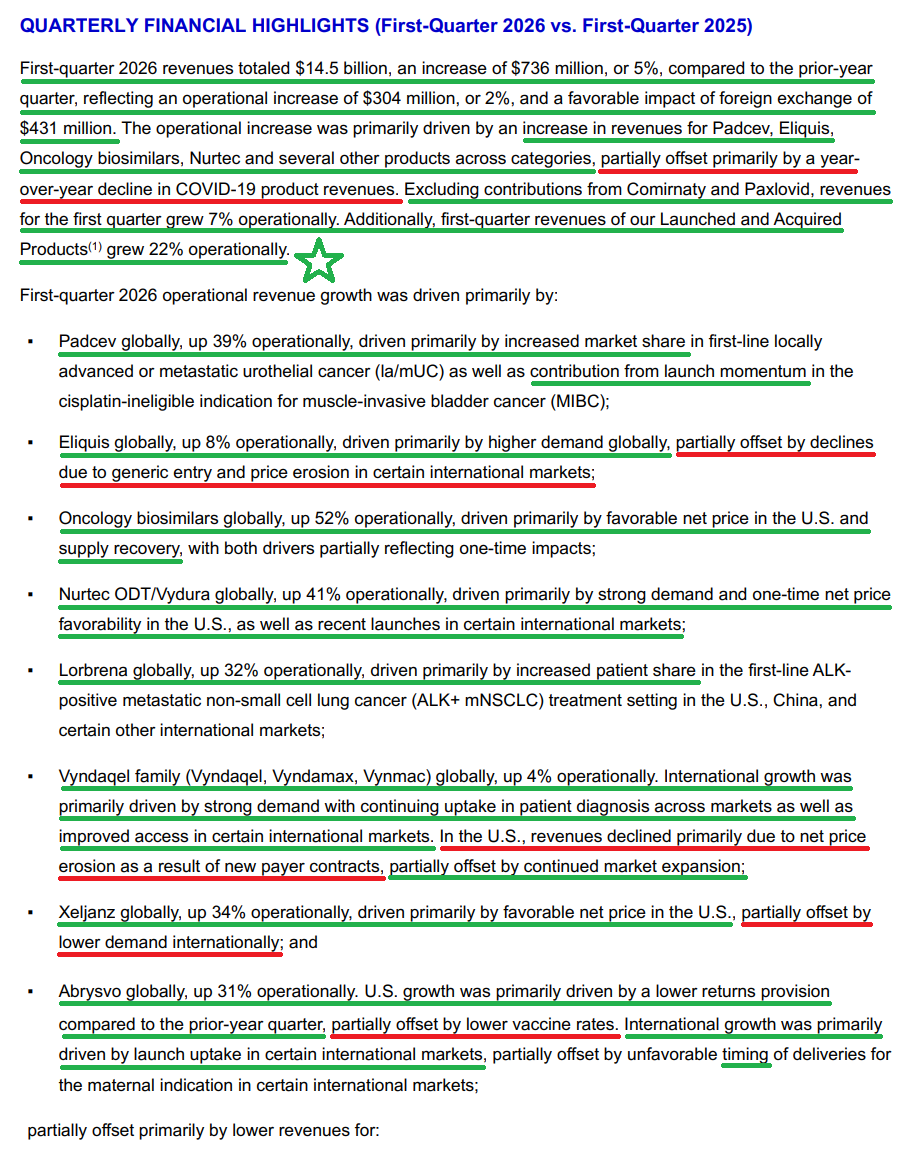

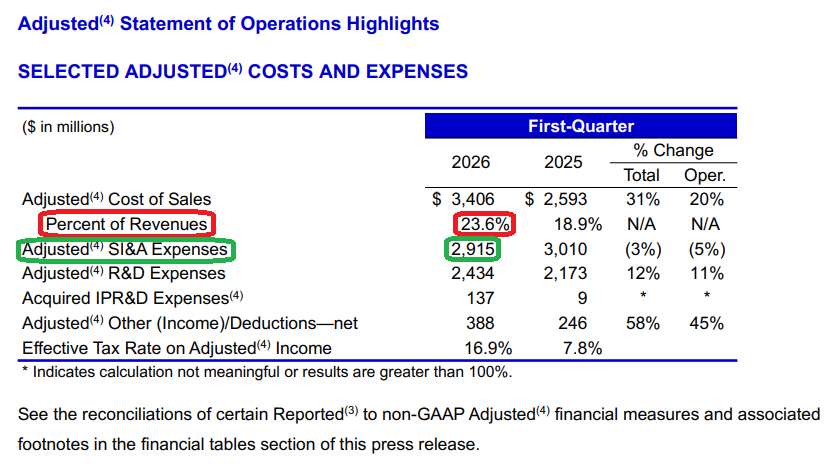

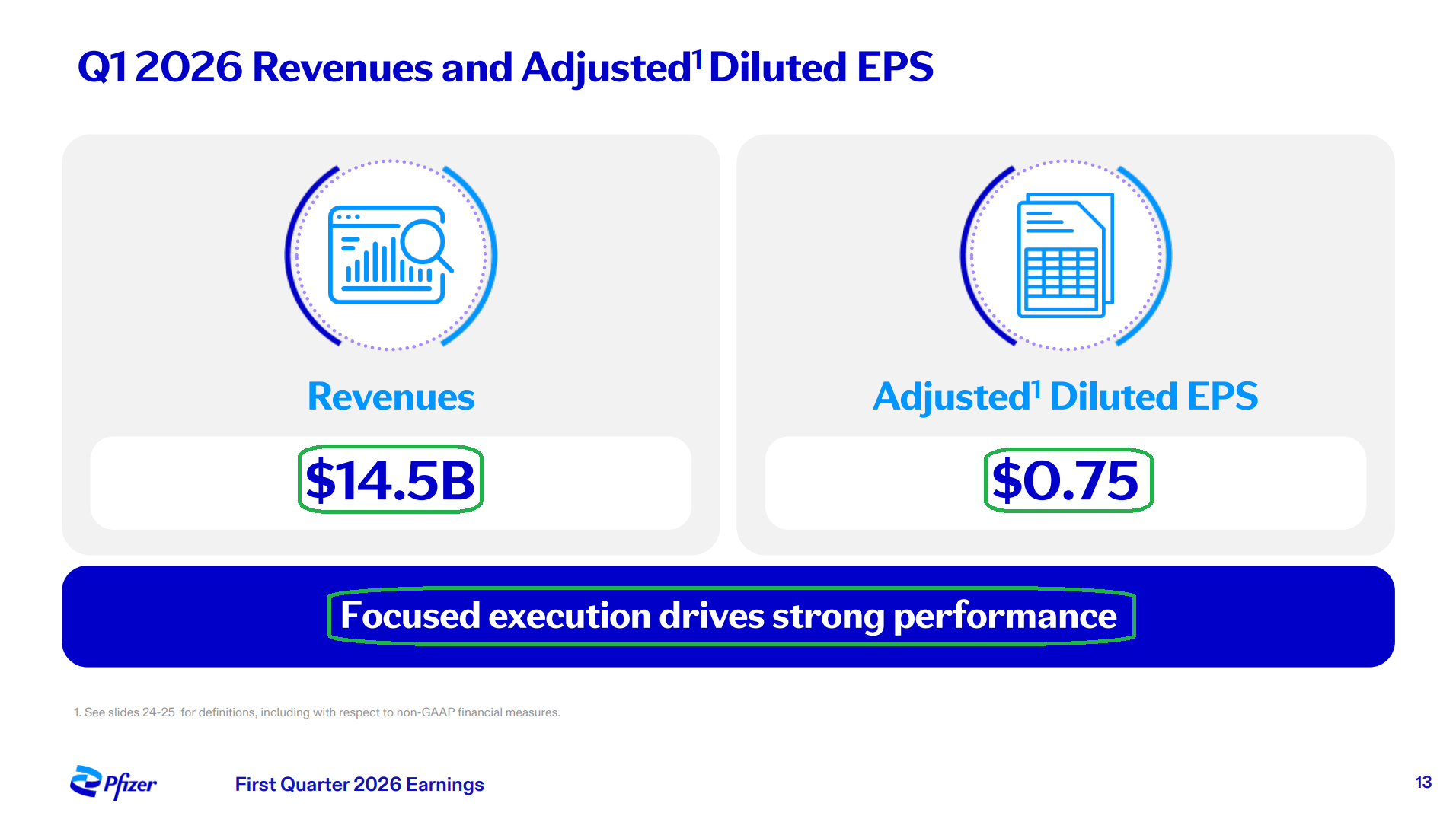

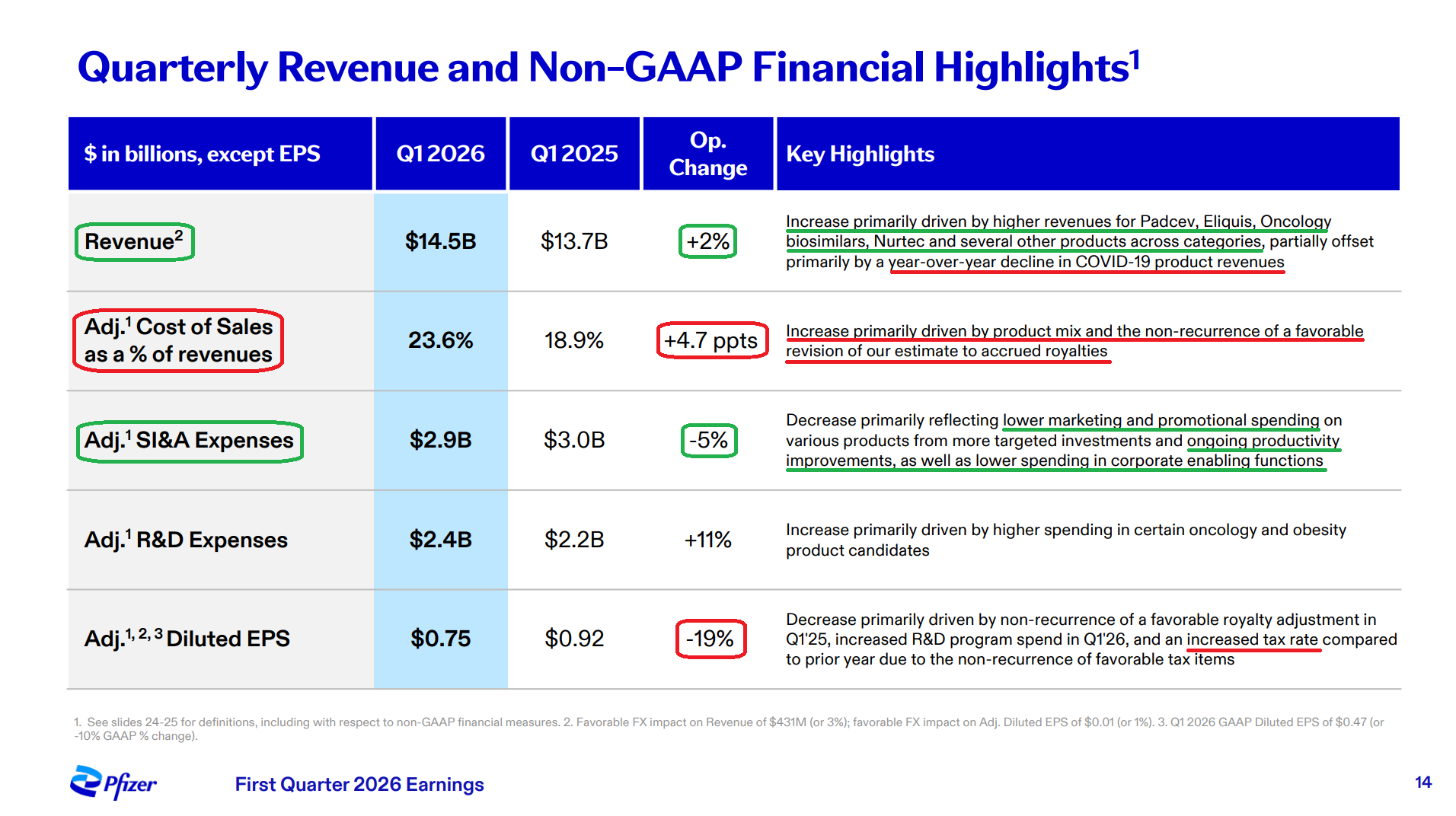

1) Pfizer posted Q1 revenue of $14.5B (+5% reported, +2% operational), ahead of consensus estimates of $13.8B. Excluding Comirnaty and Paxlovid (COVID franchise), the underlying business delivered 7% operational revenue growth, driven by solid commercial execution across key brands and continued momentum in recently launched and acquired products. Adjusted diluted EPS of $0.75 beat estimates of $0.72, -18% Y/Y due to the non-recurrence of a favorable royalty adjustment in Q1 2025, higher R&D spend, and a higher tax rate.

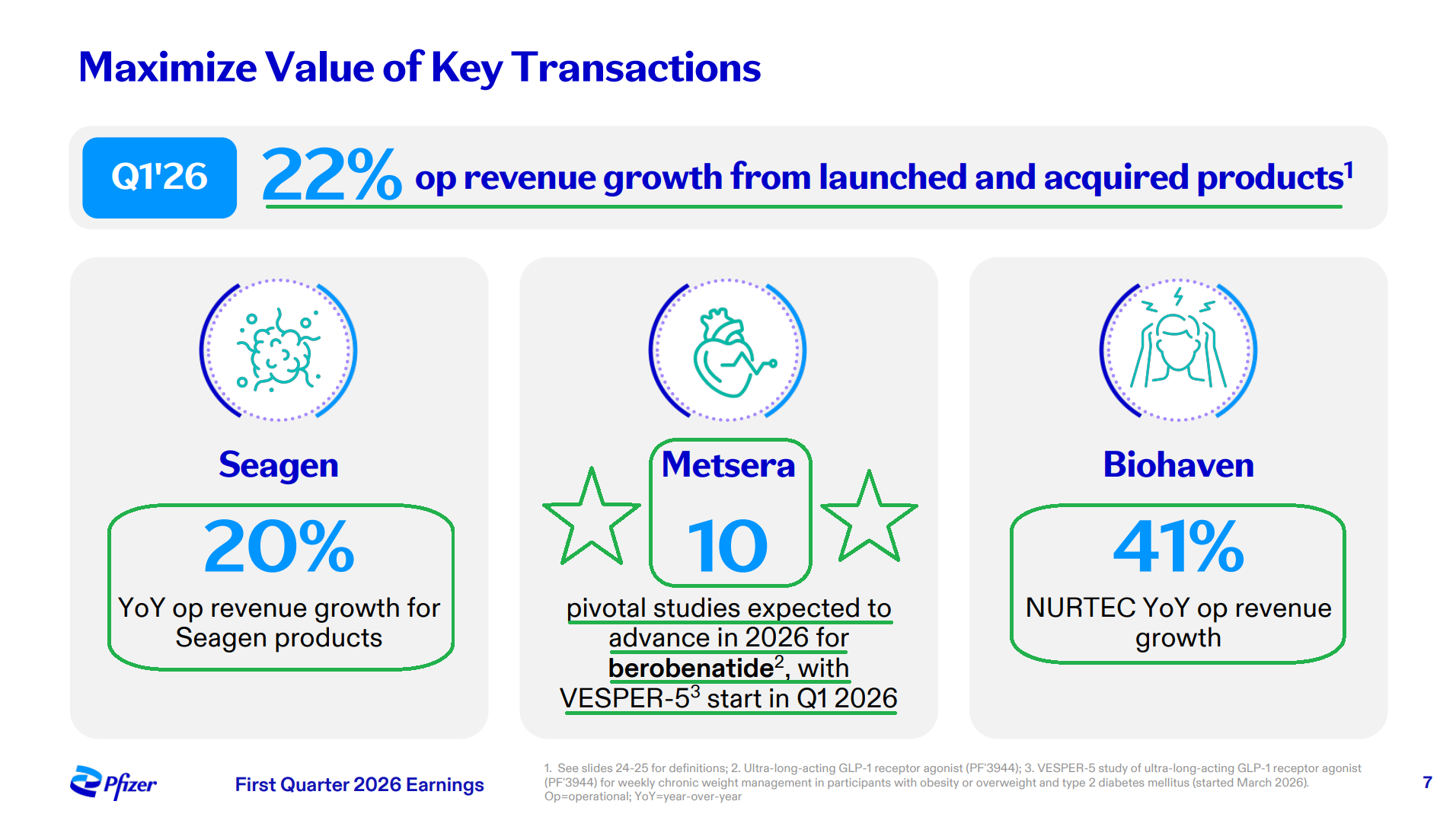

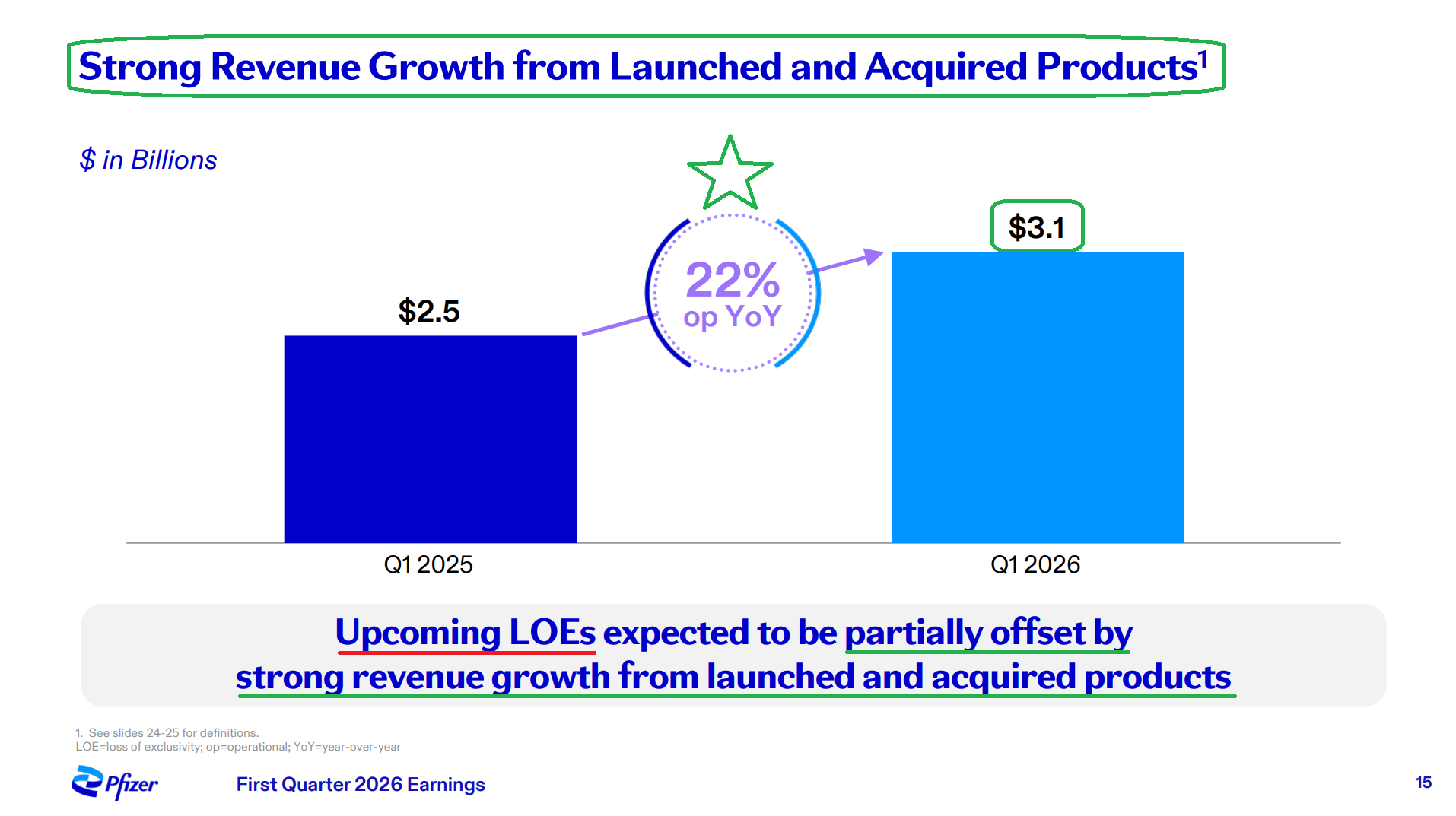

2) Recently launched and acquired products remained the key growth driver, delivering $3.1B in Q1 revenue (+22% operational Y/Y vs. $2.5B in Q1 2025) and remaining on pace to exceed $12B on an annualized basis. Padcev (bladder cancer) led the way with $591M (+39% operational), well ahead of the $528M consensus estimate, driven by strong market share gains. Nurtec (migraine) grew 41% operationally to $353M on strong demand and one-time net price favorability in the U.S., while Seagen (oncology) products posted 20% operational revenue growth and Abrysvo (RSV vaccine) grew 31% to $180M. Continued scaling of these newer growth drivers, alongside ongoing cost management, serves as a key offset to upcoming LOE headwinds.

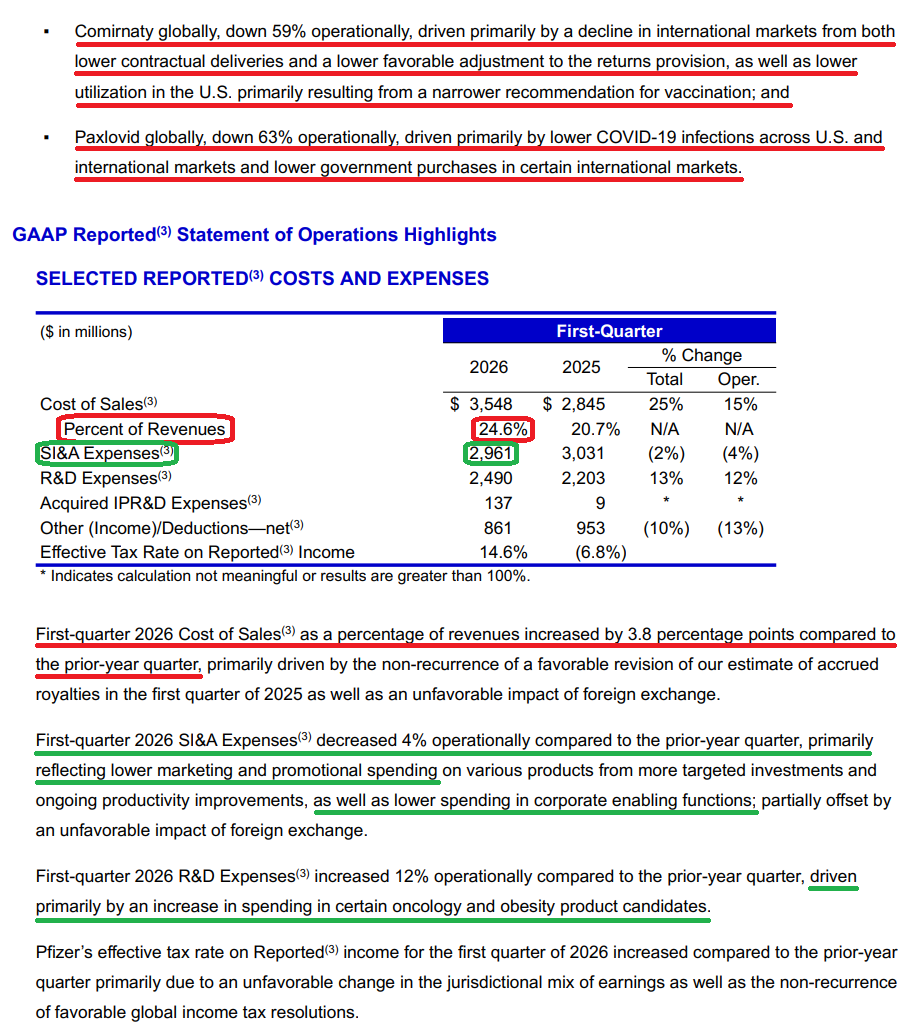

3) Adjusted gross margin came in at 76.4% (-4.7 ppts Y/Y vs. 81.1%), driven by product mix and the non-recurrence of a favorable royalty estimate revision in Q1 2025. Adjusted SI&A expenses declined 5% operationally to $2.9B on lower marketing and promotional spending and ongoing productivity improvements, while adjusted R&D expenses rose 11% operationally to $2.4B, driven by increased investment in oncology and obesity candidates. Adjusted operating margin came in at 38%, above pre-pandemic levels and reflective of the cost discipline running through the P&L.

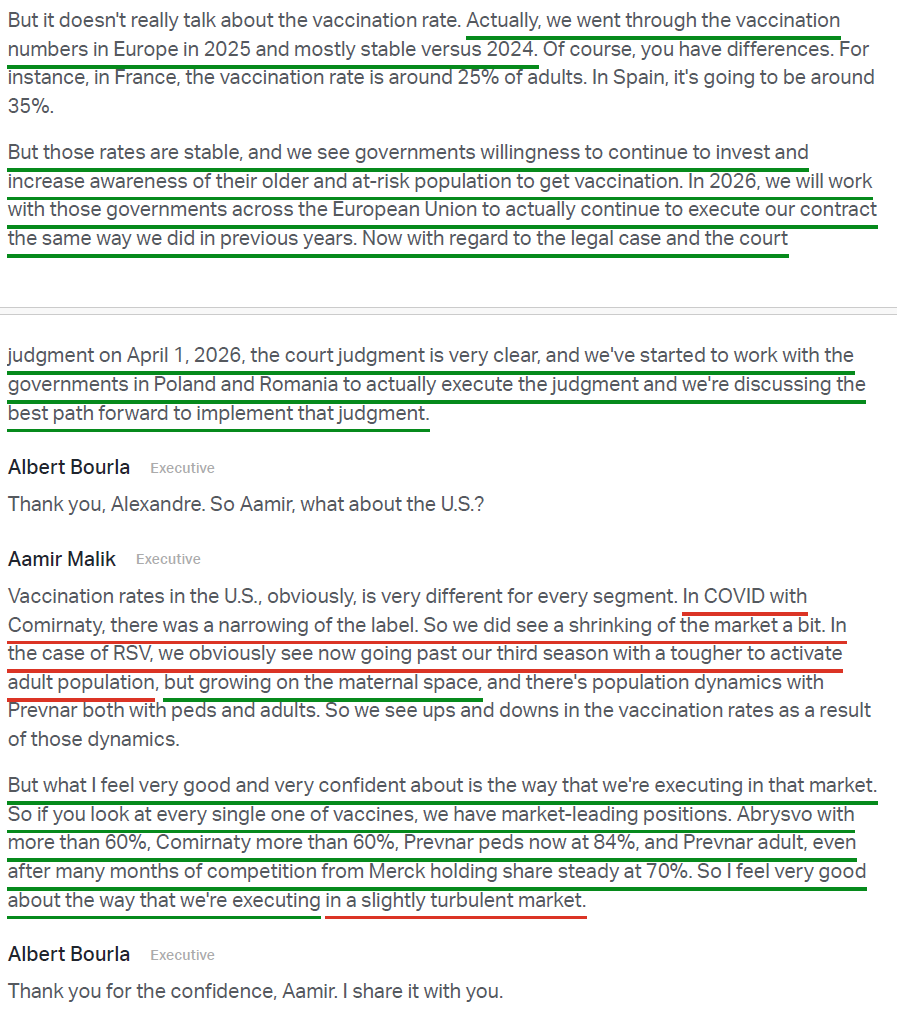

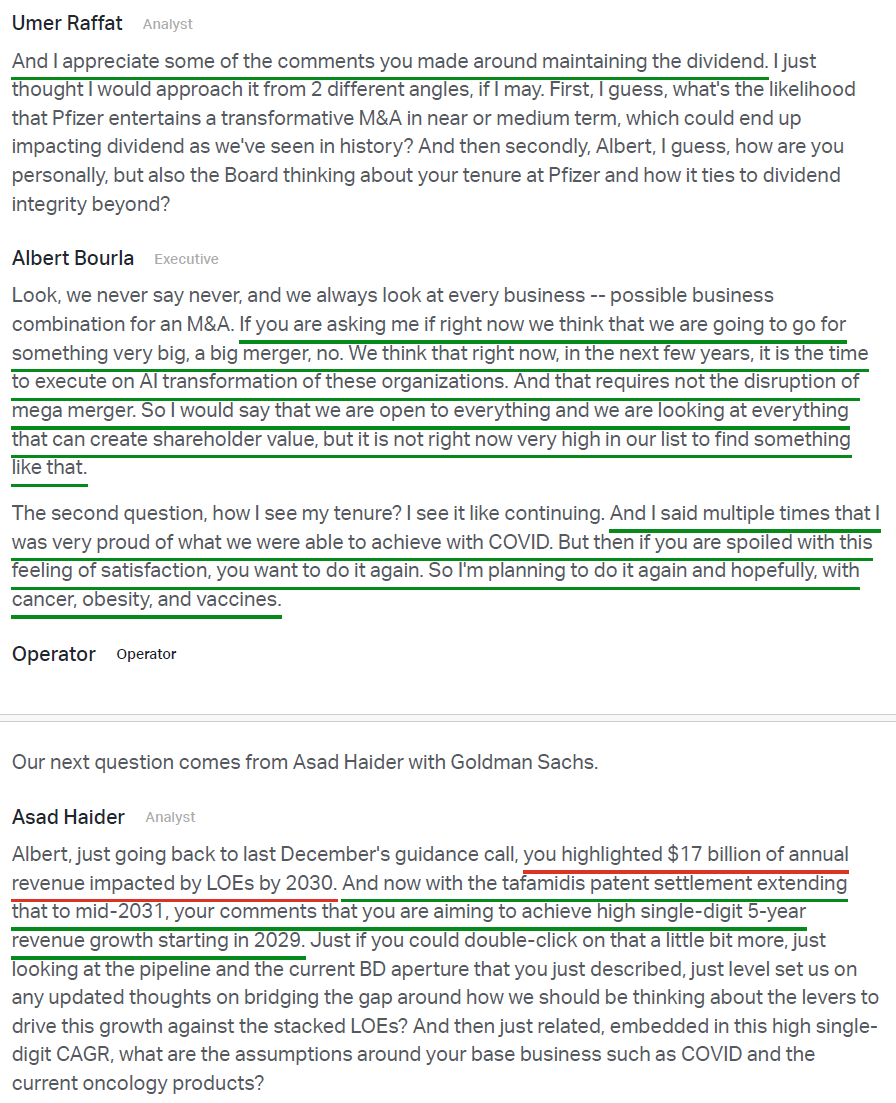

4) Two significant legal developments during the quarter materially improved Pfizer’s post-2028 growth profile, giving management confidence to target a high single-digit revenue CAGR over the five-year period beginning in 2029. Pfizer entered into settlement agreements with Dexcel Pharma, Hikma (HKMPF), and Cipla, extending the effective U.S. patent expiry for Vyndamax (~$6.3B in worldwide sales last year) to June 1, 2031. This pushes anticipated generic entry out by ~2.5 years and reduces the previously cited $17B LOE headwind through 2030 to $14B to $15B. Separately, a Belgian court ruled that Poland and Romania must pay Pfizer ~$2.2B in a dispute over contested COVID vaccine doses, which management characterized as a positive for future EPS and cash flow.

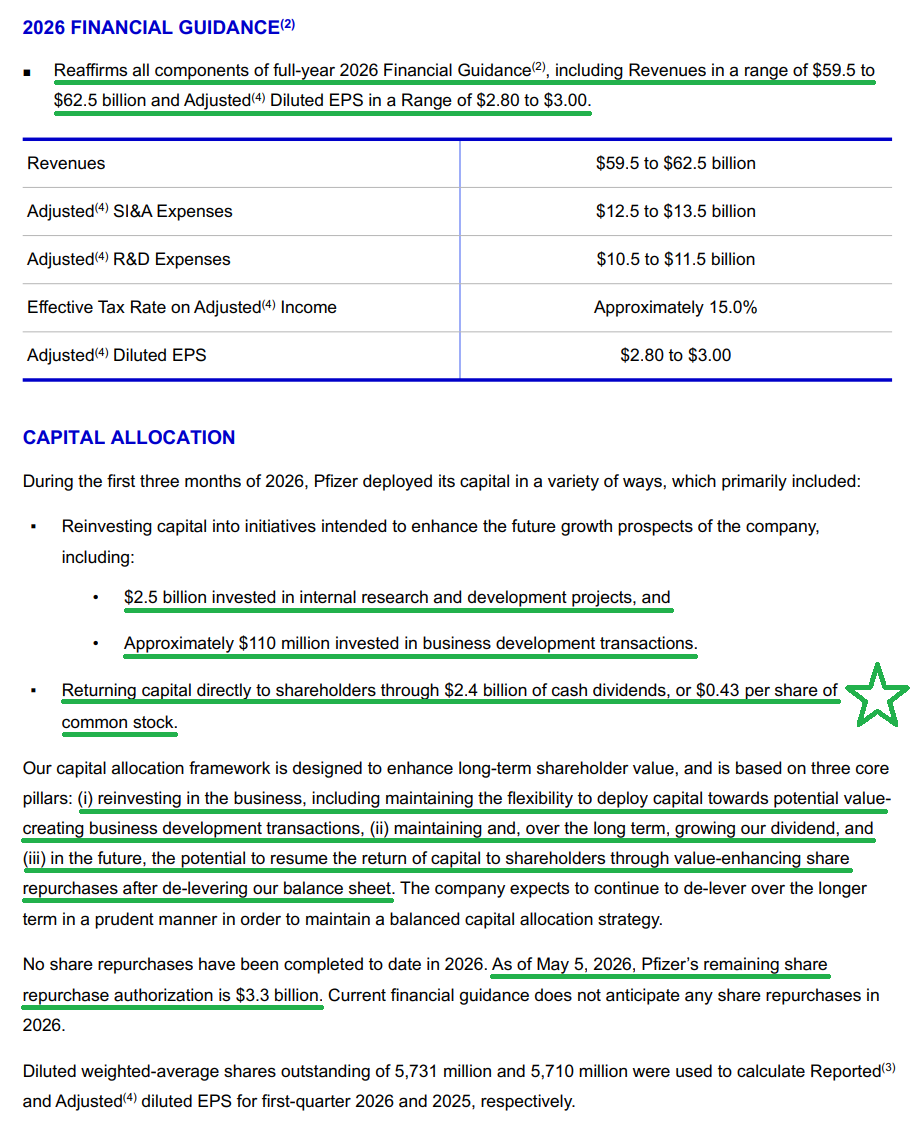

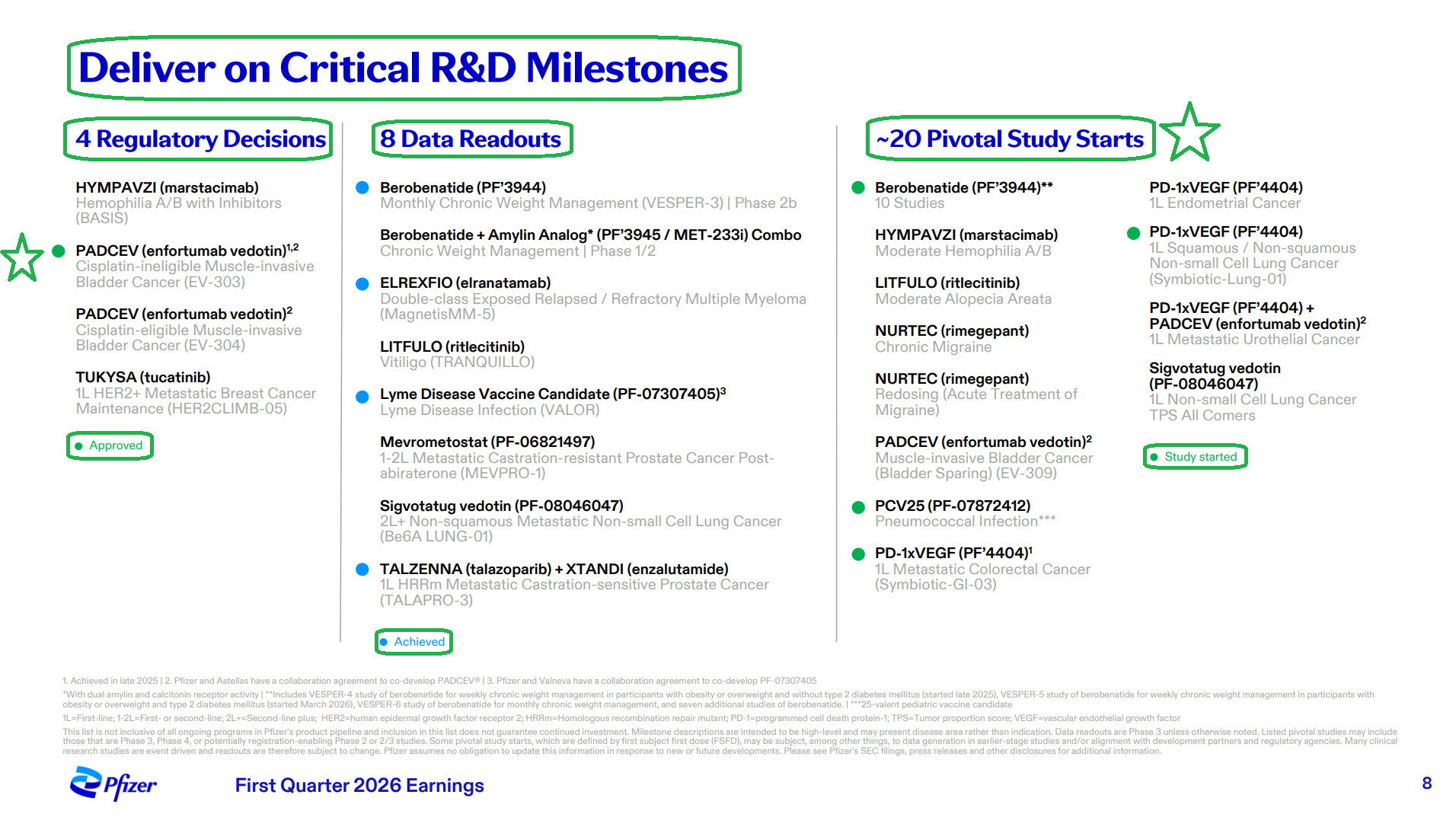

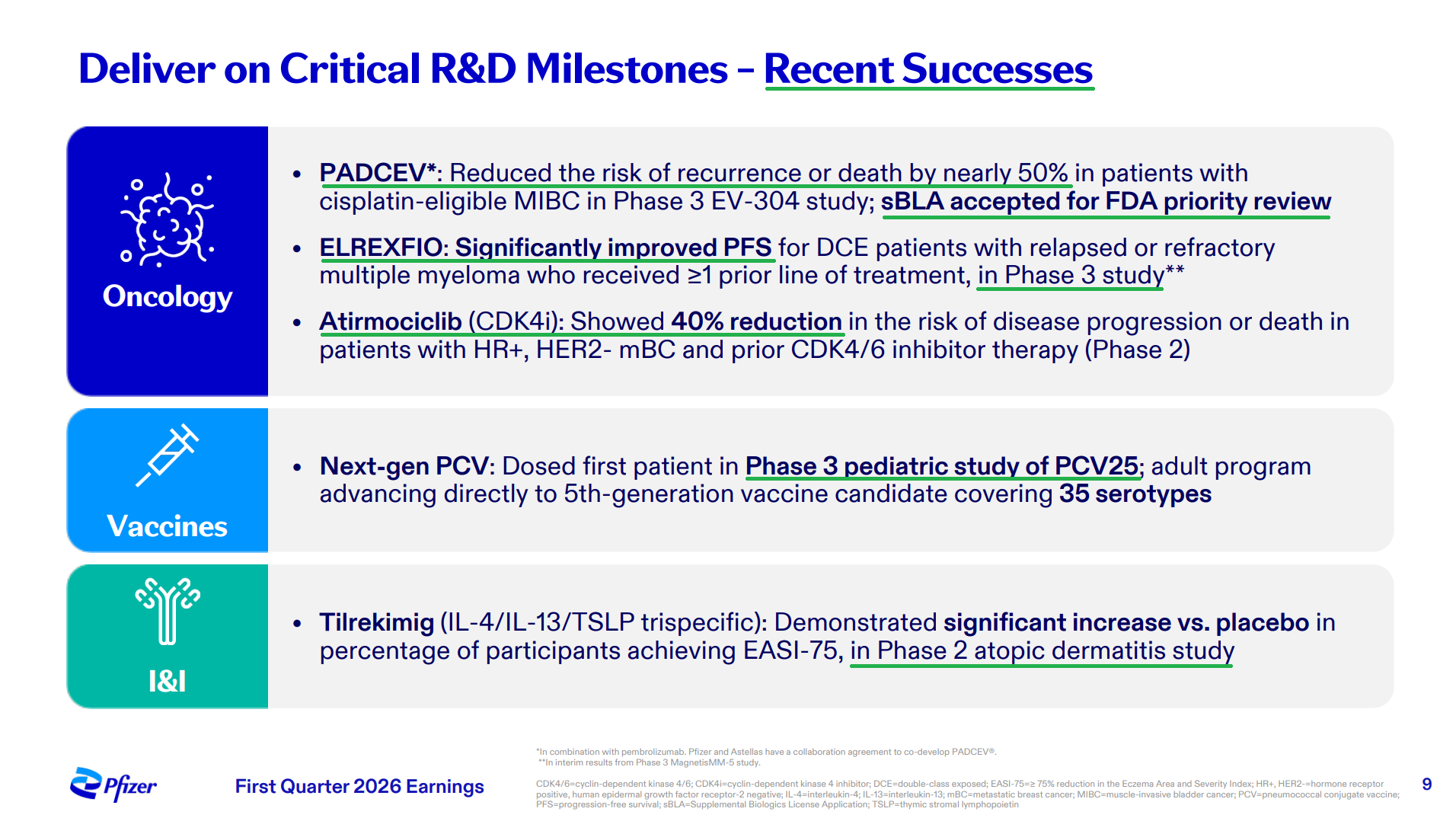

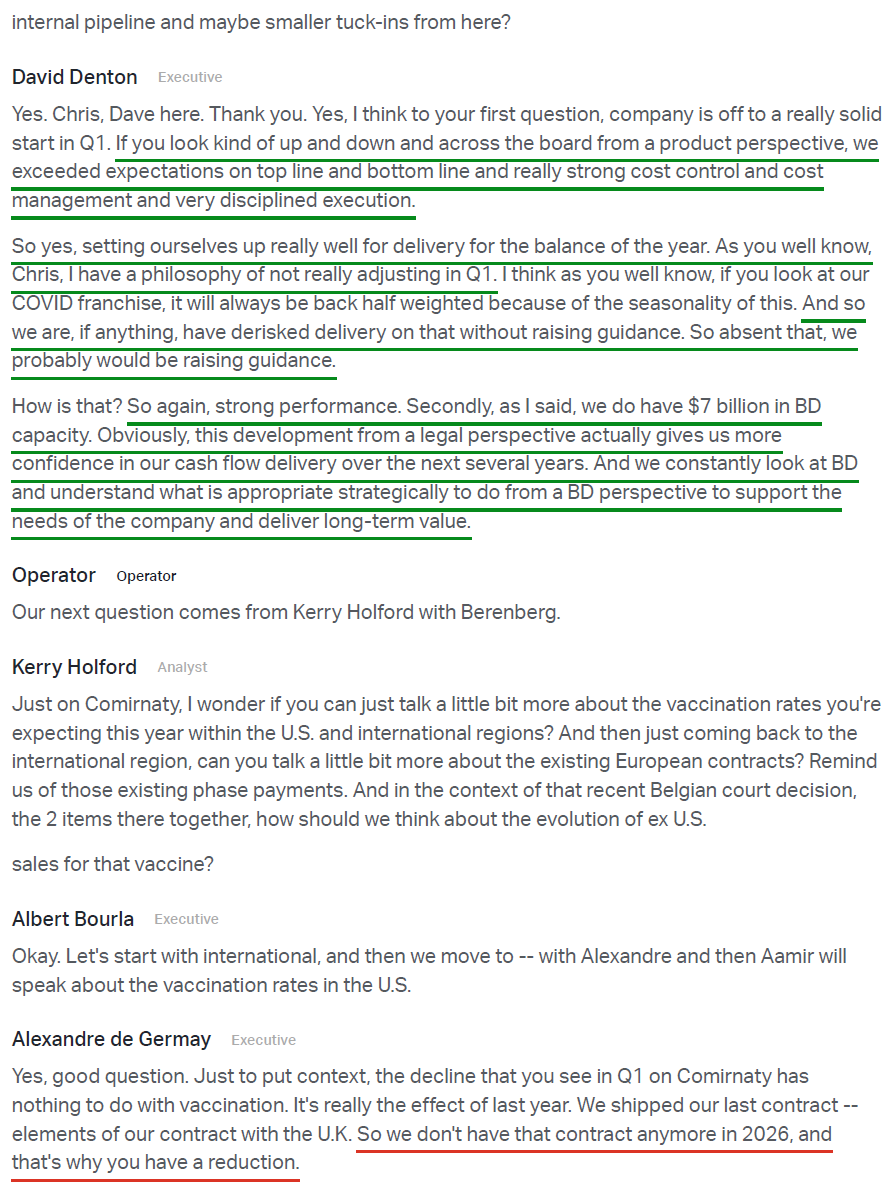

5) Pfizer invested $2.5B in internal R&D during Q1 and remains on track for ~20 pivotal study starts in 2026, with four already underway. The quarter produced three positive Phase 3 readouts across oncology, with roughly half of the eight key data readouts expected this year coming from that category. On the obesity front, Pfizer is advancing 10 Phase 3 studies for berobenatide (the GLP-1 asset acquired via Metsera) in 2026, targeting a first approval in 2028 from a portfolio of ultra-long-acting peptides with the potential for competitive efficacy and tolerability, alongside a differentiated monthly maintenance dosing schedule. BD capacity now stands at ~$7B following ~$1.65B in net proceeds from the completed sale of Pfizer’s ViiV Healthcare stake, though management was clear that a large transformative deal is not on the agenda, with the current focus squarely on executing the internal pipeline.

6) The COVID franchise continued its expected structural decline, with Comirnaty revenue of $232M falling 59% operationally and coming in well below consensus of ~$446M, driven by lower international contractual deliveries and narrower U.S. vaccination recommendations, though Pfizer retained >60% market share in the category. Paxlovid declined 62% to $186M, also missing the ~$248M estimate, due to lower infection rates across U.S. and international markets. Management reiterated that sustained low COVID infection levels will weigh on Paxlovid utilization in the near term and that the majority of Comirnaty sales are expected in the back half of the year, consistent with vaccination season timing.

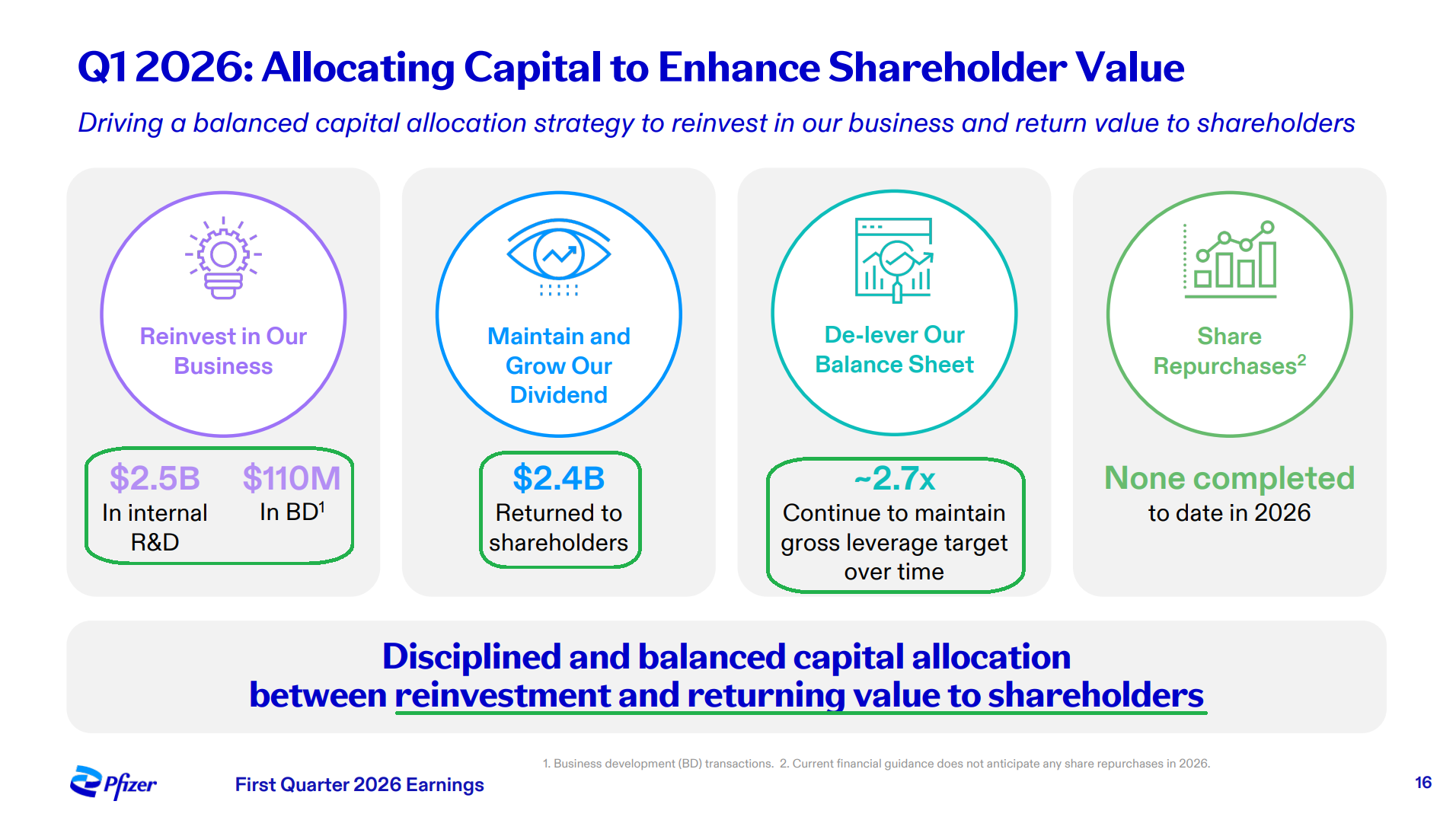

7) Pfizer returned $2.4B to shareholders through its quarterly dividend of $0.43 per share in Q1 (forward yield ~6.7%), with management reaffirming its commitment to maintaining and, over time, growing the dividend. No share repurchases were completed in Q1, and none are included in 2026 guidance. However, following favorable legal developments during the quarter, management noted that improved cash flow visibility and confidence have brought share repurchases back into consideration, with Pfizer retaining $3.3B in remaining repurchase authorization.

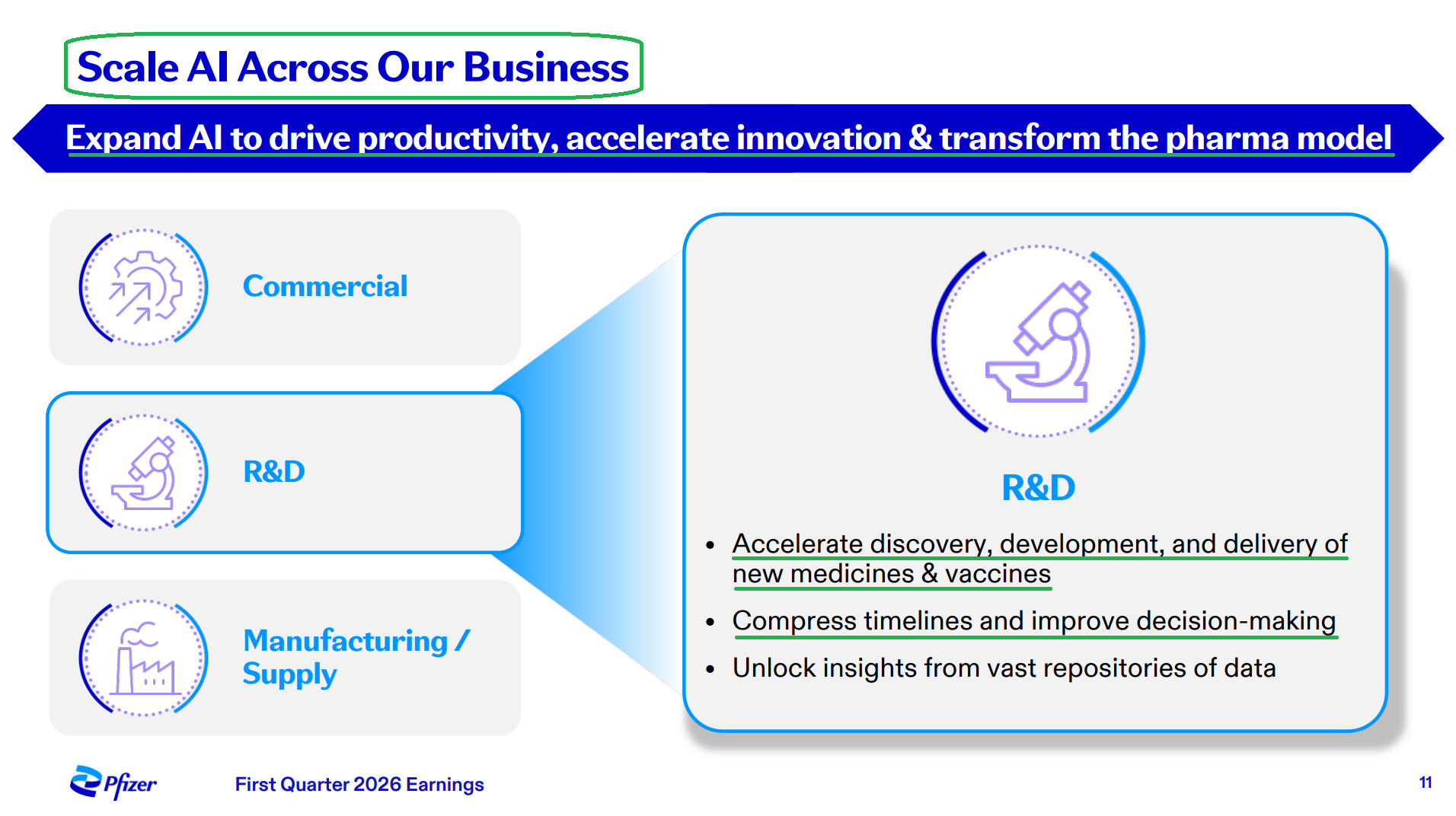

8) Pfizer remains on track to deliver the majority of its $7.2B in cumulative net cost savings by year-end 2026, with ~$700M expected from Phase 1 of its manufacturing optimization program this year alone, ~$175M of which was realized in Q1. Management noted it will continue identifying opportunities to further enhance efficiencies while prioritizing investments that support future growth. Pfizer also highlighted embedding AI across the organization as a key strategic priority, with management viewing its proprietary data repositories as a structural advantage in accelerating drug discovery and development, compressing timelines, and driving productivity across the pipeline.

9) Gross leverage ended Q1 at ~2.8x, with management guiding leverage to remain around current levels or modestly higher through the LOE transition period. Operating cash flow came in at $2.6B in Q1, and the final TCJA repatriation tax payment of ~$2.6B was made in April, removing a prior drag on free cash flow. Capital expenditures are expected to be slightly above $3B for the full year, and with the bulk of restructuring cash payments now behind the company, free cash flow generation is expected to improve going forward.

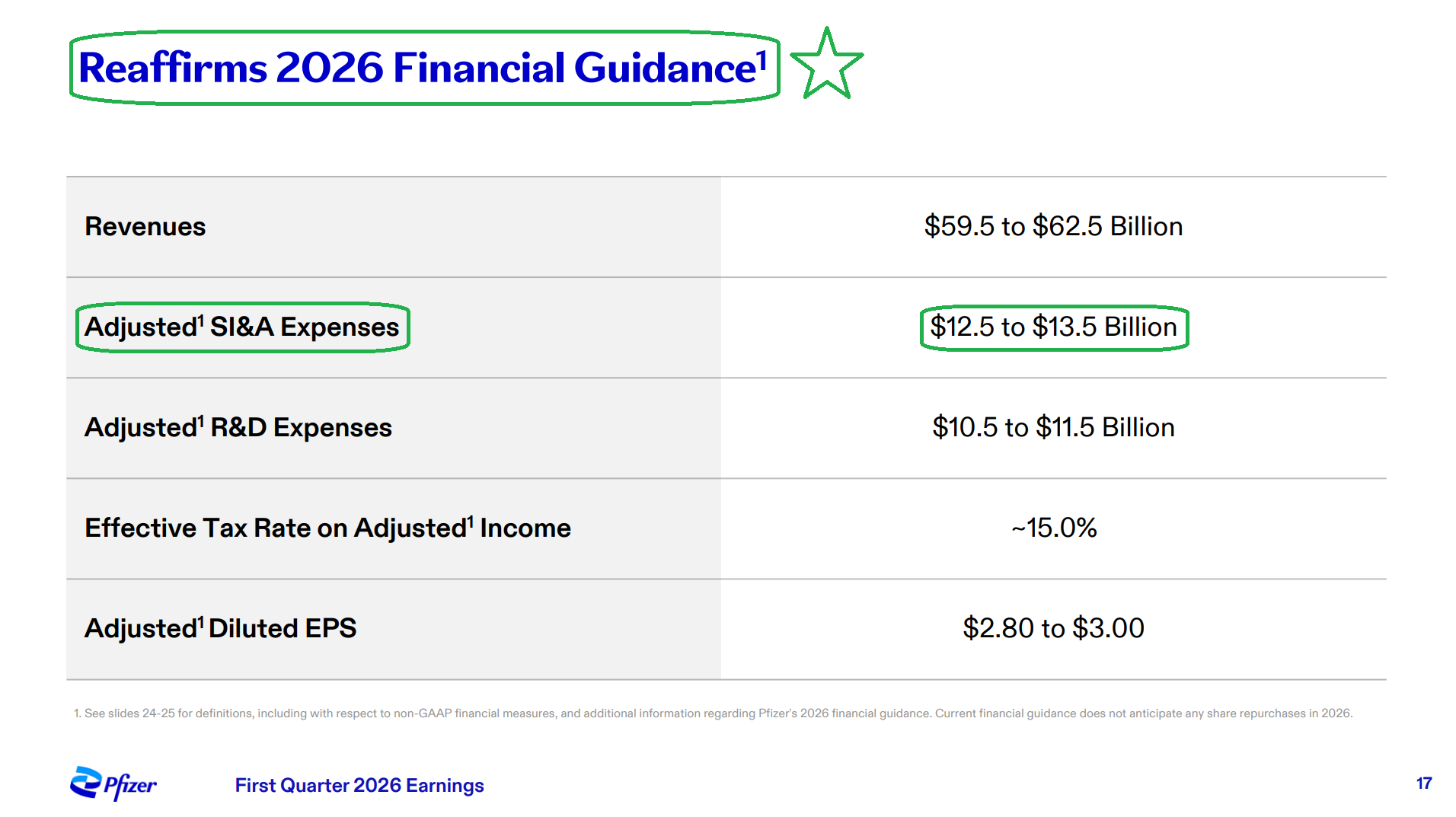

10) Management reaffirmed all components of FY26 guidance, including revenue of $59.5B to $62.5B (consensus $61.37B), adjusted diluted EPS of $2.80 to $3.00 (consensus $2.96), adjusted R&D of $10.5B to $11.5B, adjusted SI&A of $12.5B to $13.5B, and an effective tax rate on adjusted income of ~15%. Management noted that, absent the back-half COVID weighting, it likely would have raised guidance, with COVID seasonality effectively de-risking delivery of the existing range.

Earnings Call Highlights

Morningstar Analyst Note

General Market

The CNN “Fear and Greed Index” ticked down to 34 this week from 57 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) was unchanged at 98.39% equity exposure this week.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms

Comments

Log in or sign up to join the conversation.