Bank of America (BAC) Fund Manager Survey Update

On Tuesday, we put out a summary of the monthly Bank of America Global Fund Manager Survey. This month, they surveyed 181 institutional managers with ~$484B in AUM.

Here were the 5 key points:

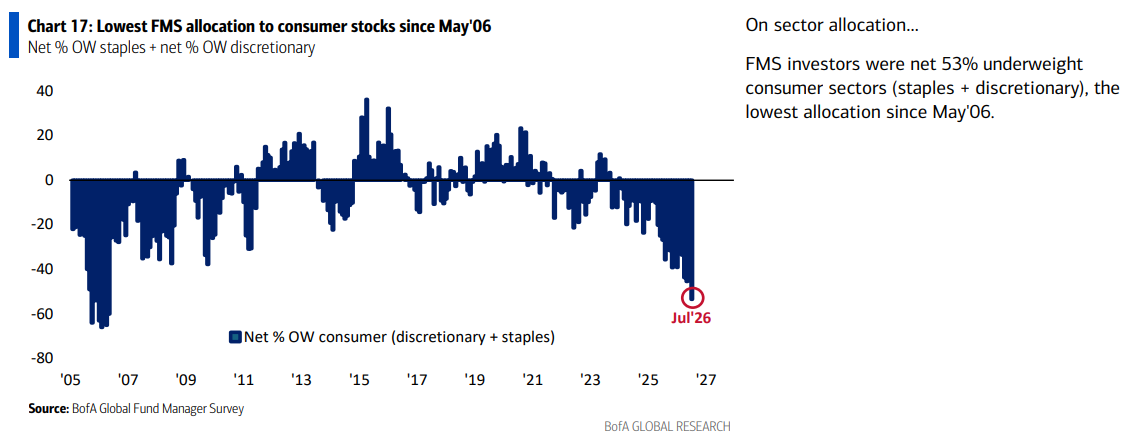

1) Fund managers are now net 53% underweight consumer sectors (staples + discretionary), the lowest allocation since May 2006. Staples took the brunt of it, sliding to a net 32% underweight from 21% last month, the most underweight since February 2014 and a full 2.0 standard deviations below its long-term average, while discretionary sits at a net 22% underweight, 0.9 standard deviations below its own. Both have been left for dead, and we continue to want exposure across the aisle, from HRL and EL in staples to VFC, ETSY, PZZA, and GOOS in discretionary. The conventional wisdom holds that these two are opposite sides of the same trade, that defense only works when offense doesn't, and vice versa. We see a scenario where both outperform together: household balance sheets are in the best shape in decades, unemployment sits at just 4.2%, retail sales continue to come in strong, and energy prices will make their way back down once the war premium wears off, as it always does.

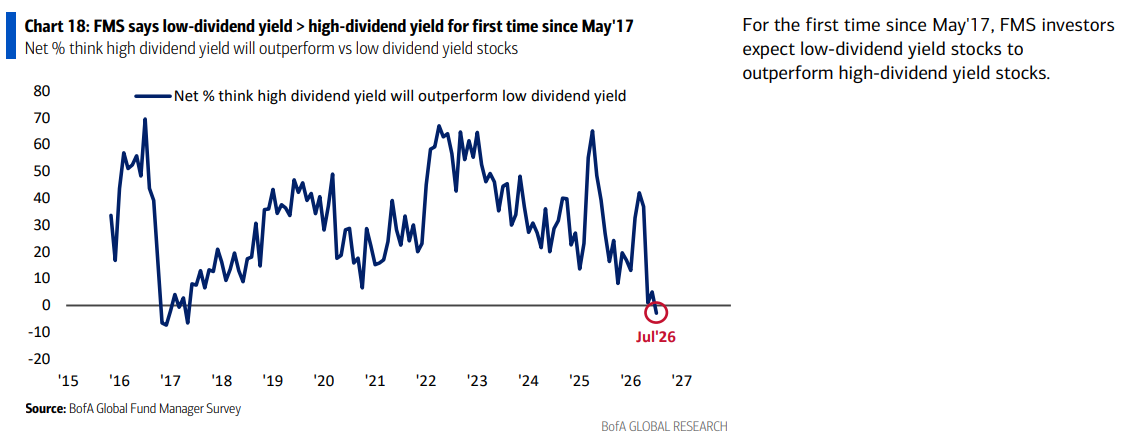

2) For the first time since May 2017, fund managers expect low-dividend-yield stocks to outperform high-dividend-yield stocks. This is ultimately a play on rates, and as they fall, the ~$7.95T parked in money market funds gets pushed off the sidelines in search of yield, with the dividend payers this survey just left for dead serving as the natural landing spot. This only reinforces our constructive view on the defensive, income-producing corners of the market.

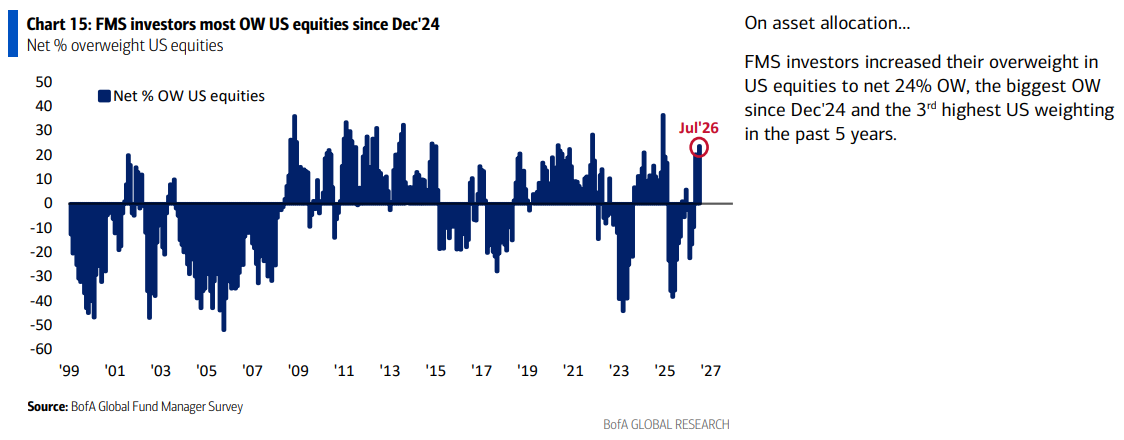

3) Fund managers lifted their US equity allocation to a net 24% overweight, the highest since December 2024 and the third-highest US weighting of the past five years, now sitting 1.4 standard deviations above its long-term average (meanwhile, they are the most underweight UK equities since August 2020). We remain constructive on the international versus US theme, coming off a record 15-year rolling stretch of US outperformance that is only in the early stages of unwinding.

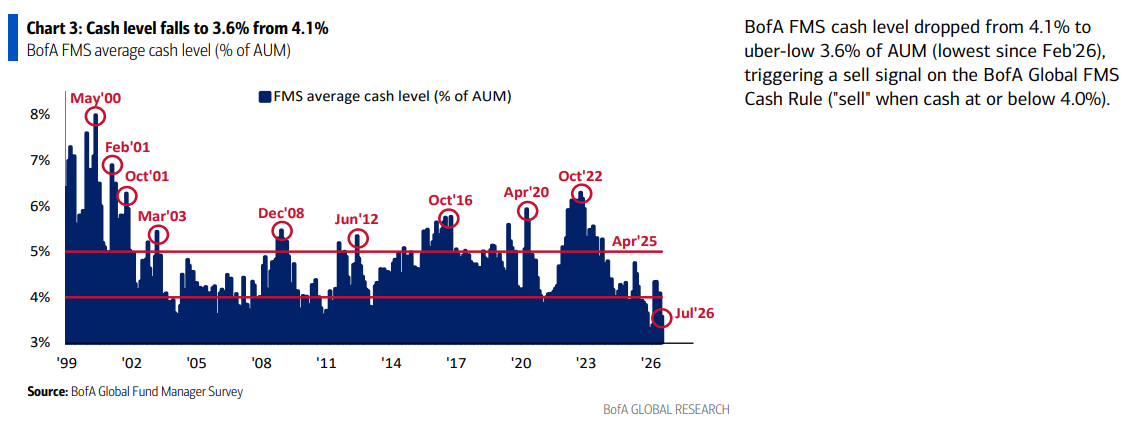

4) Fund managers' average cash level dropped from 4.1% to an uber-low 3.6% of AUM, the lowest since February 2026 and enough to trigger a sell signal on the BofA Global FMS Cash Rule, which flashes at or below 4.0%. Cash has fallen to 3.6% or lower in 16 instances since 2002, with stocks down an average of 1% over the following two weeks and 0.5% over the following month. Managers are now walking into late-summer, midterm-year volatility with no dry powder, which naturally begs the question: when everyone is all in, who is left to buy?

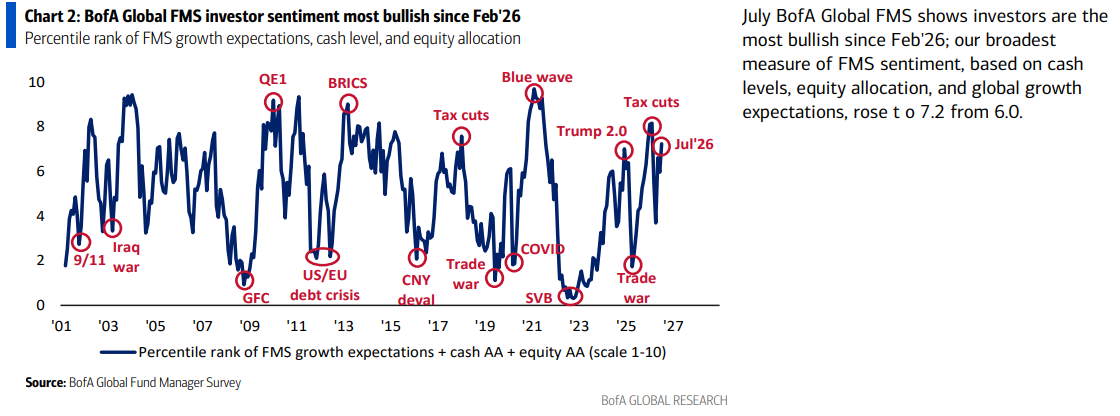

5) BofA's broadest sentiment gauge, built off cash levels, equity allocation, and global growth expectations, jumped to 7.2 from 6.0 in July, the most bullish reading since February 2026. Managers are leaning hard into a dovish Fed, with 83% saying there will be no hike before the November midterms and 41% now expecting an economic "boom" of above-trend growth and above-trend inflation, the highest reading since February 2022. Things are getting frothy, though still short of prior extremes. As we have said in the past, it is best to curb your enthusiasm and be selective here.

Comstock Resources (CRK) Update

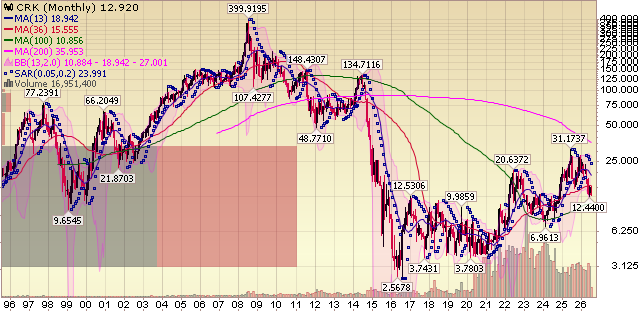

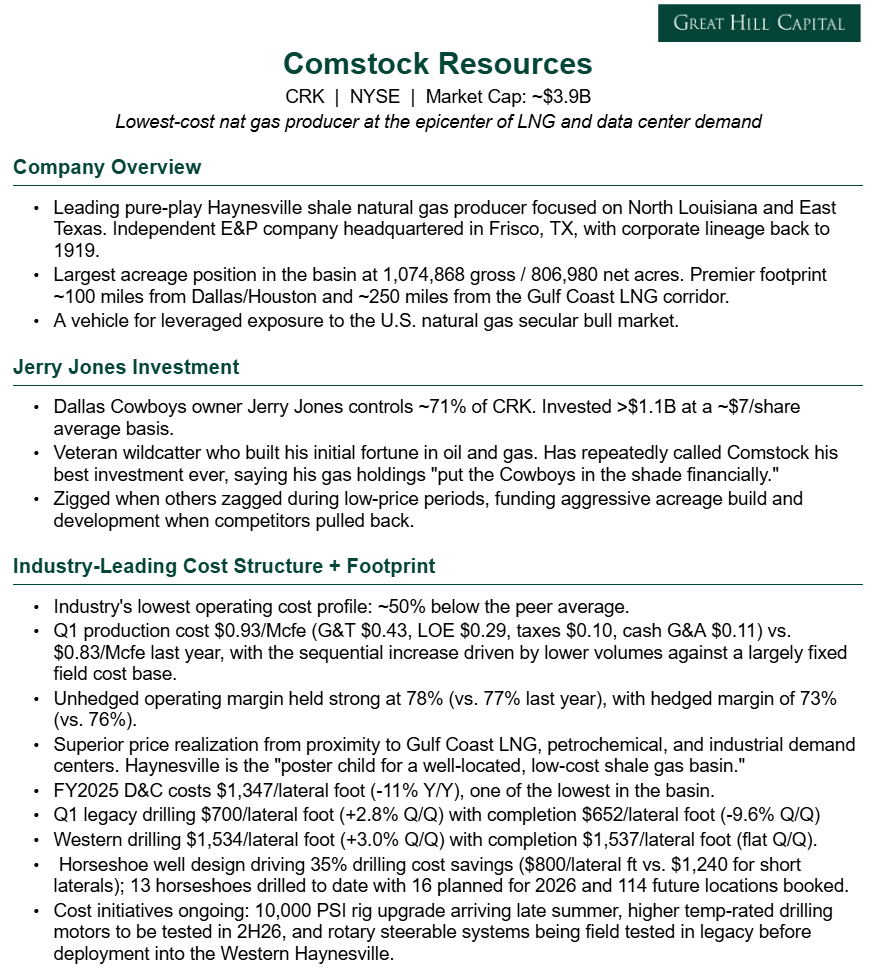

For newer readers, here's a quick overview of the key drivers behind our thesis on Comstock Resources, a natural gas producer that we believe offers one of the most attractive backdoor ways to play the AI and data center buildout at a reasonable valuation:

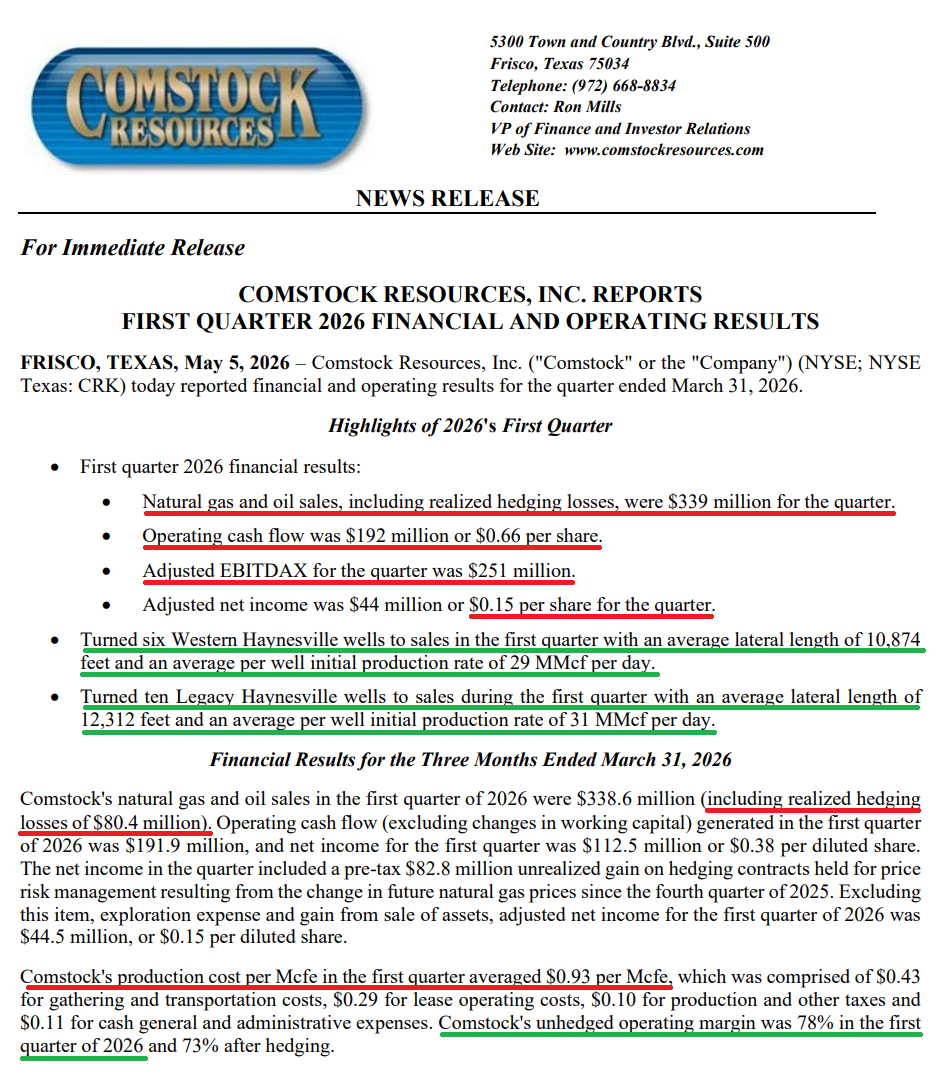

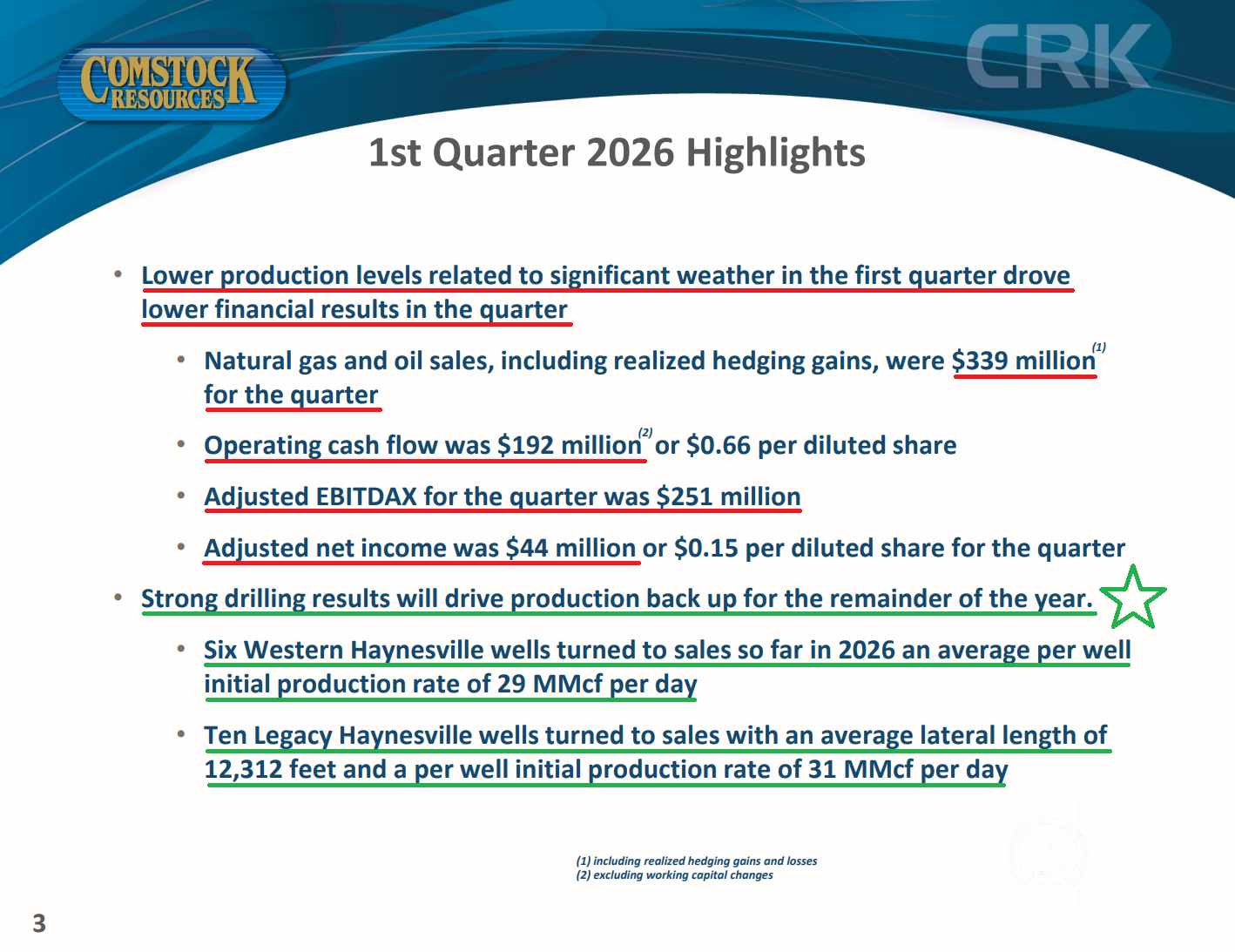

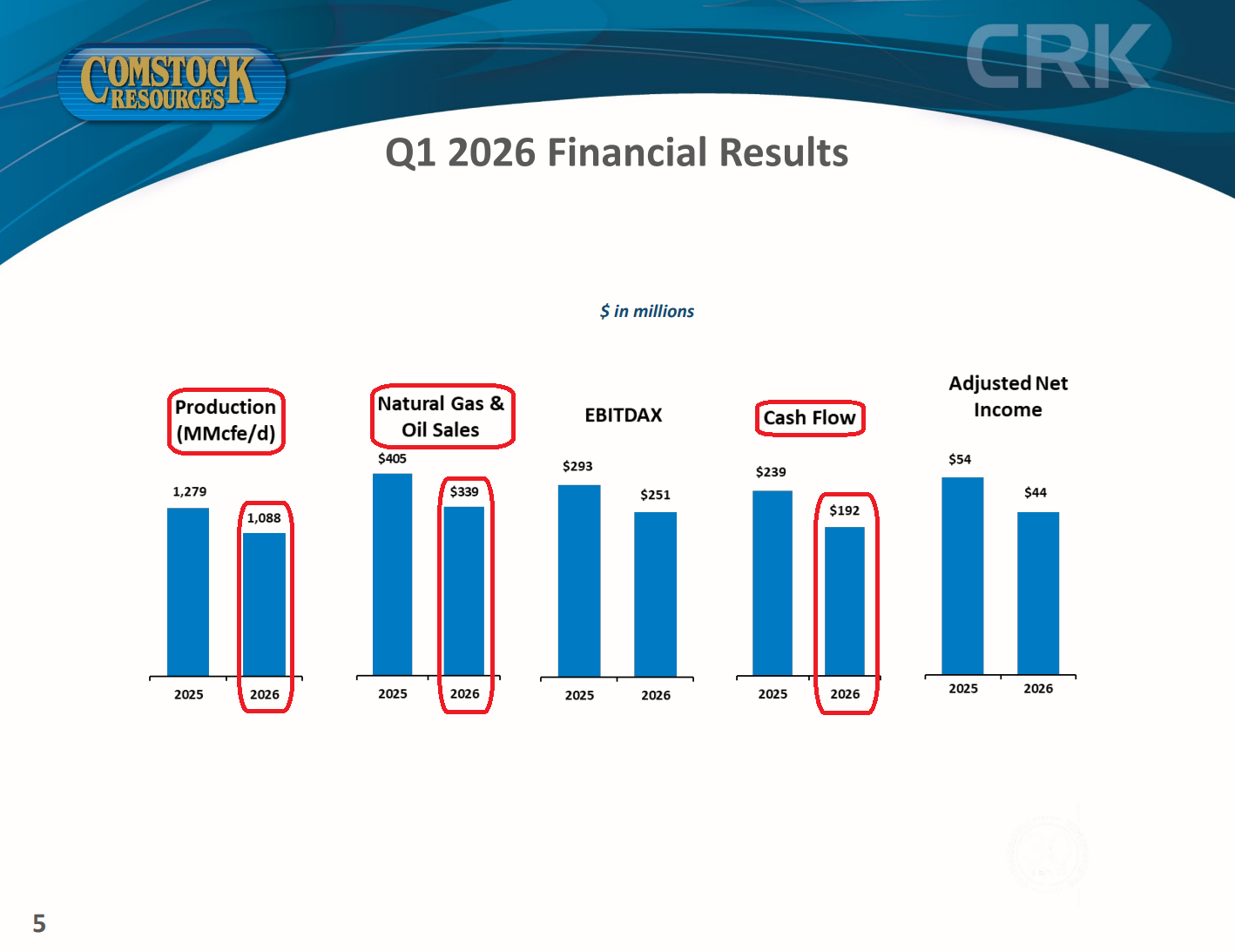

Comstock's first quarter delivered the two things a natural gas producer never wants to see in the same headline: production going down and capital spending going up. Volumes fell to 1,088 MMcfe/d, oil and gas sales declined 16% y/y to $339M, and the company spent $343M on drilling plus another $55M on midstream against just $192M of operating cash flow, driving free cash flow to a $206M deficit. There is no dressing that up. Those are ugly numbers, and while they made for ugly headlines, they told you very little about the underlying business.

That's because a brutal winter storm forced wells offline, shut down frac equipment, and made roads impassable, delaying completions by weeks. As a result, nearly every well Comstock turned to sales came online in the final days of March. In other words, the company incurred the cost of drilling and completing the wells but booked almost none of the associated production. Conventional accounting will call that a bad quarter, but it's really just a timing issue that reverses as the calendar turns.

We are not investors in single quarters, and this is precisely the sort of stretch that separates the people who OWN businesses from the people who RENT them. Management already has line of sight to production rebounding 13% to 15% sequentially, with strong momentum expected throughout the back half of the year. As CEO Jay Allison put it on the call, "I think we've turned the corner."

Even with volumes down, per-unit costs elevated as largely fixed expenses were spread across fewer units of production, and nearly every headwind blowing in the same direction, Comstock still produced natural gas at a cost ~43% below the peer average. That tells us the low-cost advantage that drew us to this name in the first place is as strong as ever.

Now for what actually mattered.

While the sell side spent its time picking apart a weather-driven quarter, two catalysts fundamentally reset what this company is worth, and neither received the attention they deserved.

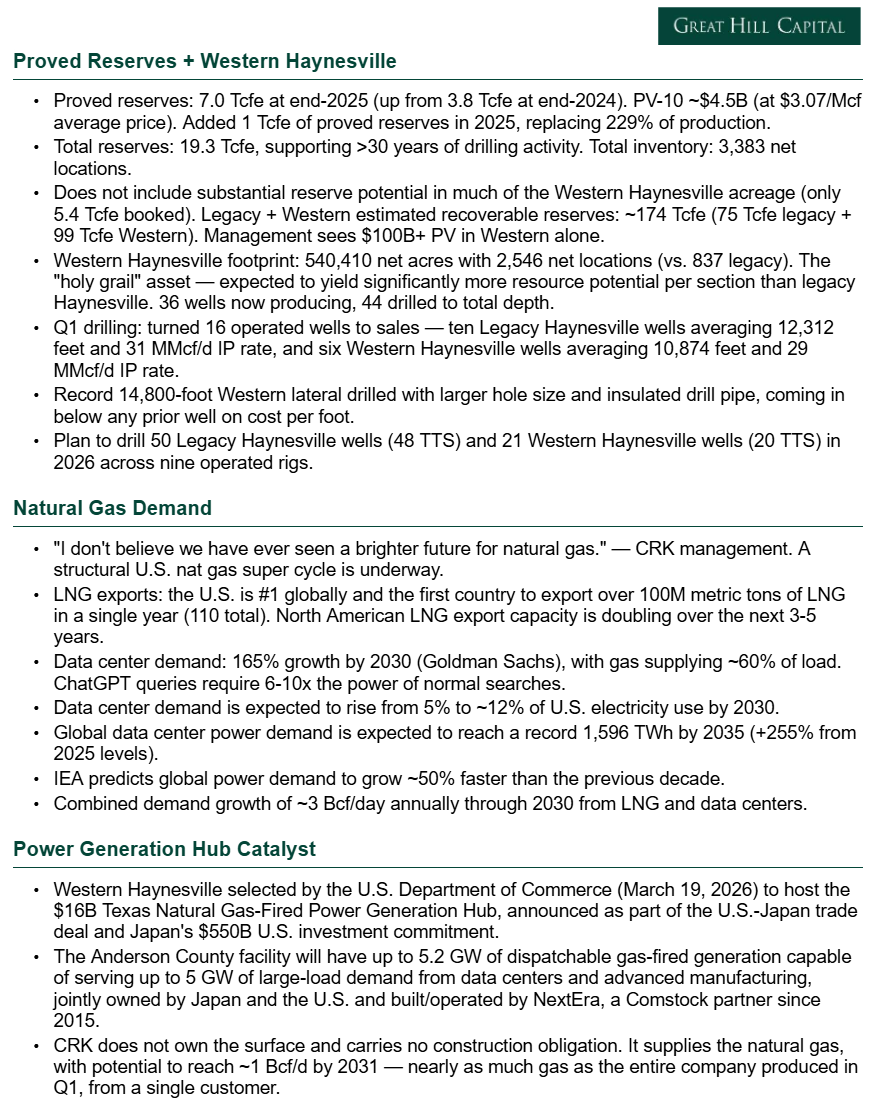

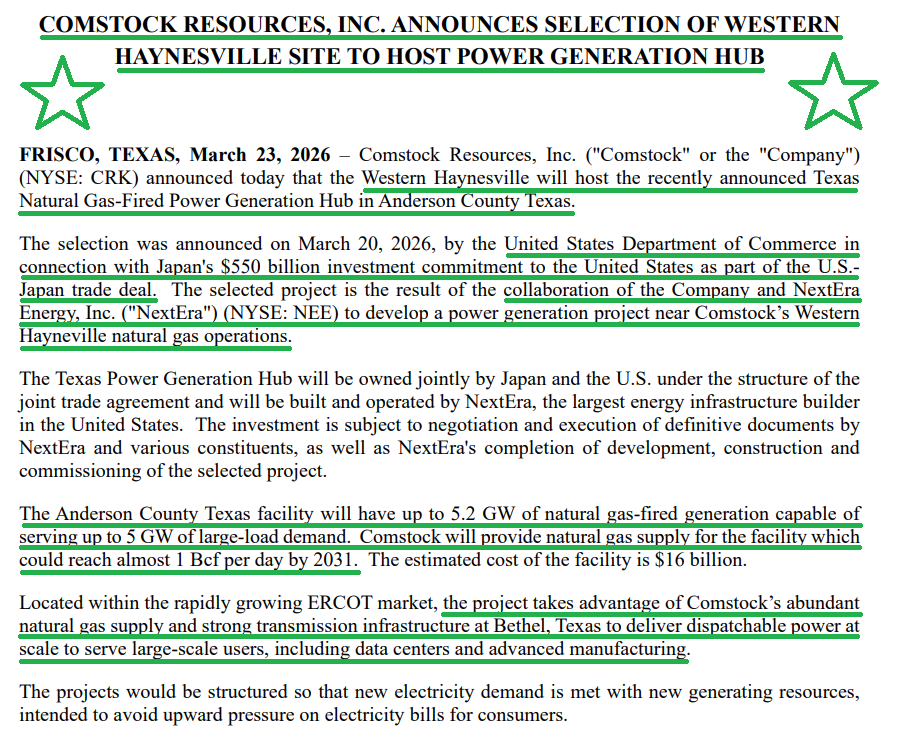

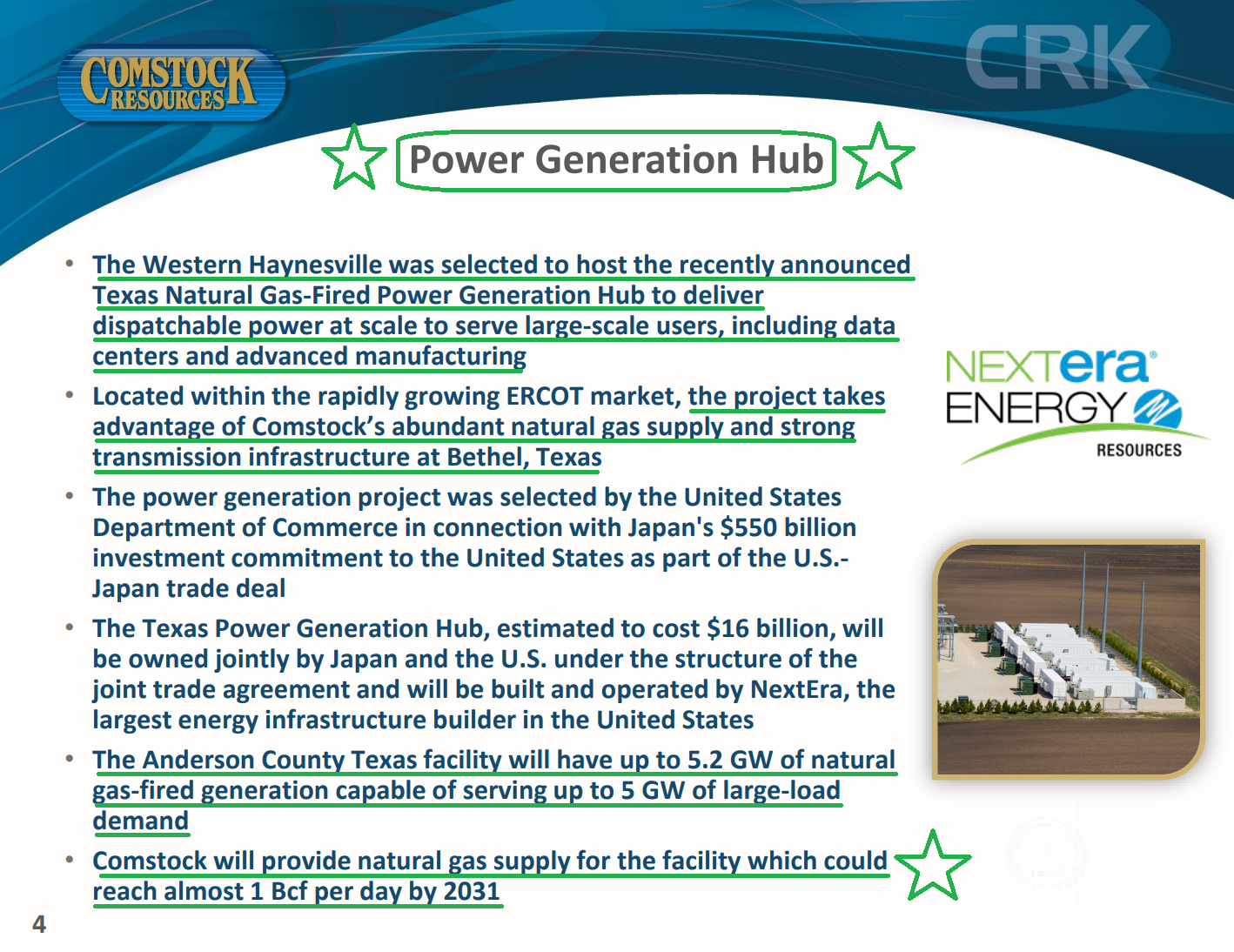

On March 19, the U.S. Department of Commerce selected Comstock's Western Haynesville to host the Texas Natural Gas-Fired Power Generation Hub, a $16B facility in Anderson County, Texas. The project will be built and operated by NextEra (NEE), the nation's largest energy infrastructure builder and a Comstock partner since 2015. Once complete, it will include 5.2 gigawatts of dispatchable gas-fired generation capable of serving 5 gigawatts of large-load demand from data centers and advanced manufacturing.

Comstock has what is arguably the best seat at the table, carrying no construction obligation, no surface ownership, and no capital at risk on the build. All it has to do is supply the gas, and those volumes could approach 1 Bcf/d by 2031. For context, Comstock produced ~1.1 Bcfe/d this quarter. In other words, the federal government just parked a customer in Comstock's backyard capable of absorbing nearly everything the company currently pulls out of the ground.

This was not luck, and NextEra certainly did not select Comstock out of the kindness of its heart. A project of this scale requires abundant natural gas reserves, pipeline and transmission infrastructure already in the ground, and close proximity to the site itself. Very few operators in America check all three boxes because doing so requires years of investing ahead of a demand wave that has yet to arrive. That is exactly what Comstock did.

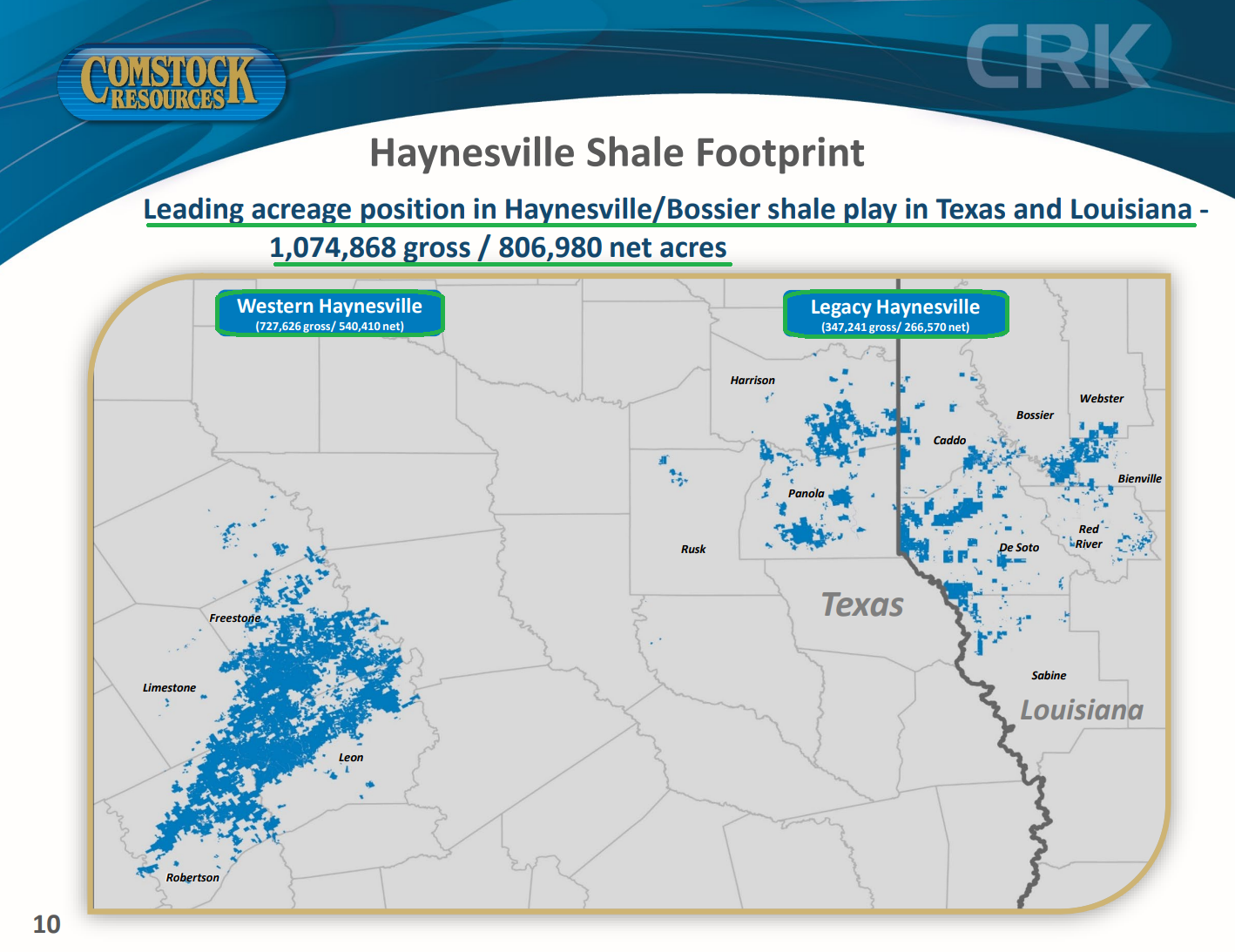

While much of the industry was hiding under its desk as natural gas was grinding sideways at inflation-adjusted lows, Comstock, backed by the deep pockets of veteran wildcatter and Dallas Cowboys owner Jerry Jones, was busy signing ~30,000 individual leases across what has since grown into more than 540,000 net acres in the Western Haynesville. Those assets sit squarely within the ERCOT (Electric Reliability Council of Texas) market, with transmission infrastructure already in the ground, ~100 miles from both Dallas and Houston, and ~250 miles from the Gulf Coast LNG corridor.

This is exactly what we mean when we talk about skating to where the puck is going, and this is what it looks like when the puck finally arrives.

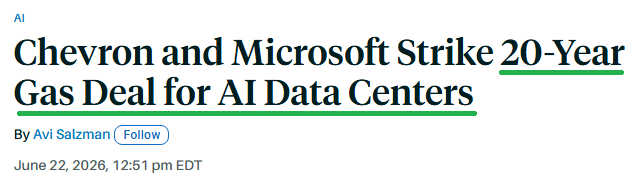

For the better part of a year, Comstock has been telling investors this moment was coming. Quarter after quarter, management discussed how large end users were increasingly looking to bypass the grid and work directly with producers through long-term supply agreements, noting that the phone had been ringing. The Power Generation Hub is the first tangible payoff from all that work, and we believe it is unlikely to be the last, because you only need to look at what Chevron (CVX) just did to see where this trend is headed.

Chevron signed a 20-year agreement to supply 2.67 gigawatts of power to Microsoft (MSFT) from new natural gas plants in West Texas, supporting a data center campus that will consume roughly as much power as two million homes while creating ~400 MMcf/d of incremental demand for Permian gas.

As the hyperscalers march toward a consensus $748B of capex commitments in 2026 (for now), up 80% Y/Y, the single biggest constraint standing in their way is access to reliable power. They are no longer waiting for the grid to solve the problem and are instead going directly to producers, locking in long-dated contracted volumes rather than relying on the spot market and hoping for the best.

This begs the question: Who owns more natural gas in the Western Haynesville and sits closer to this demand than Comstock Resources? Nobody does. With nearly 807,000 net acres positioned squarely between the Gulf Coast LNG terminals and the Texas data center buildout, additional agreements with Comstock’s name attached are a matter of when, not if.

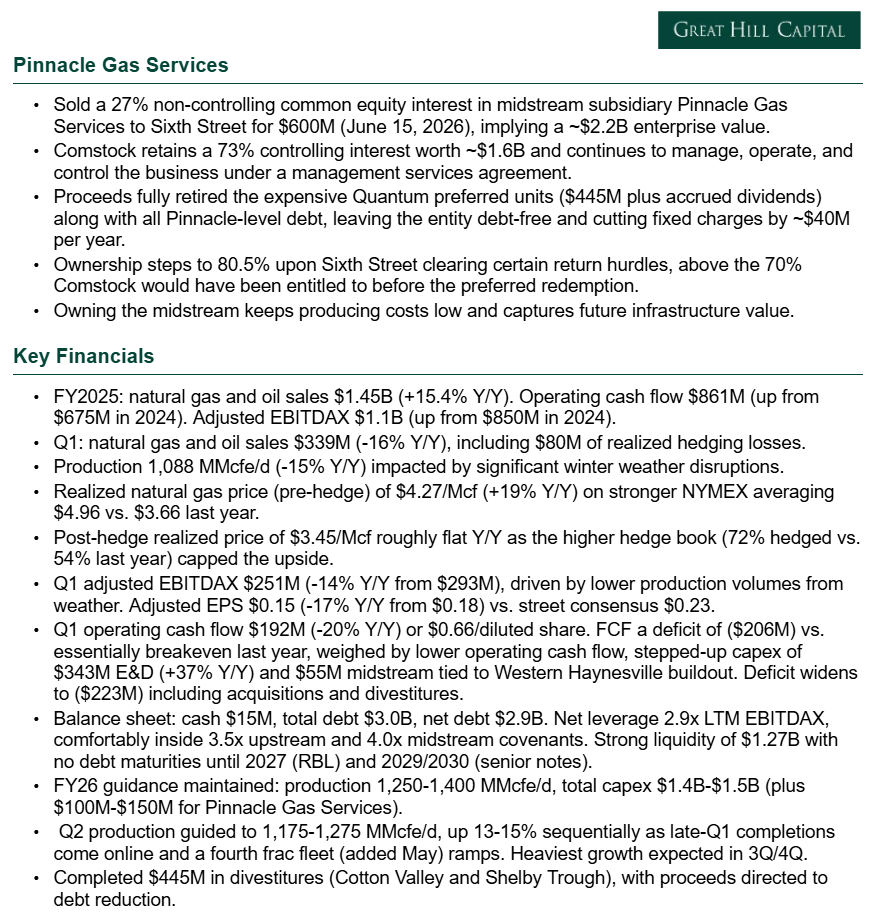

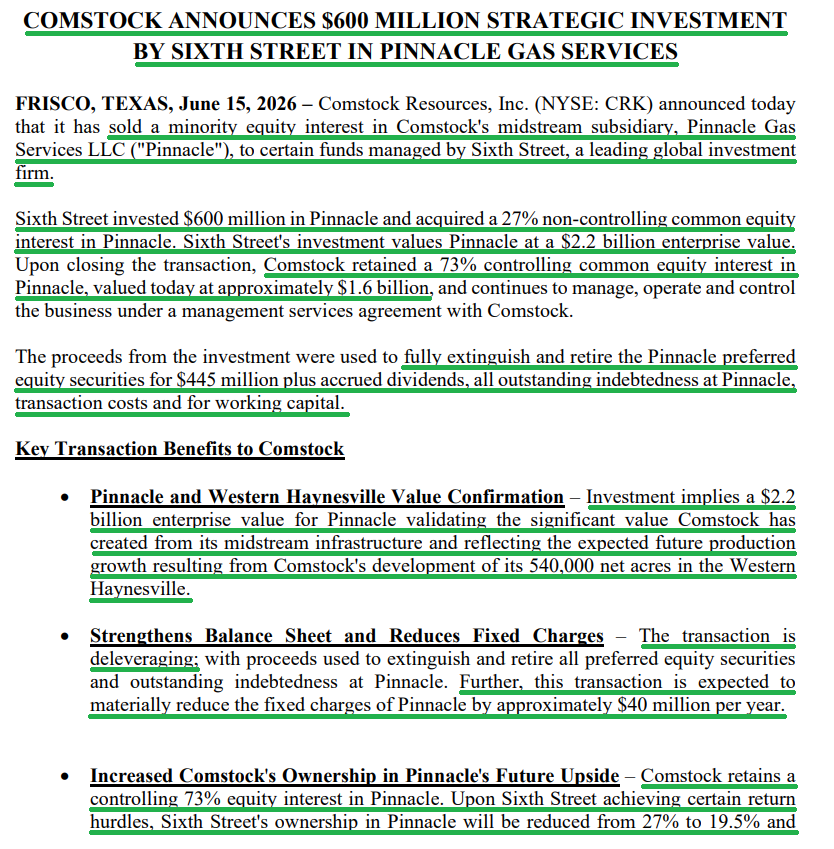

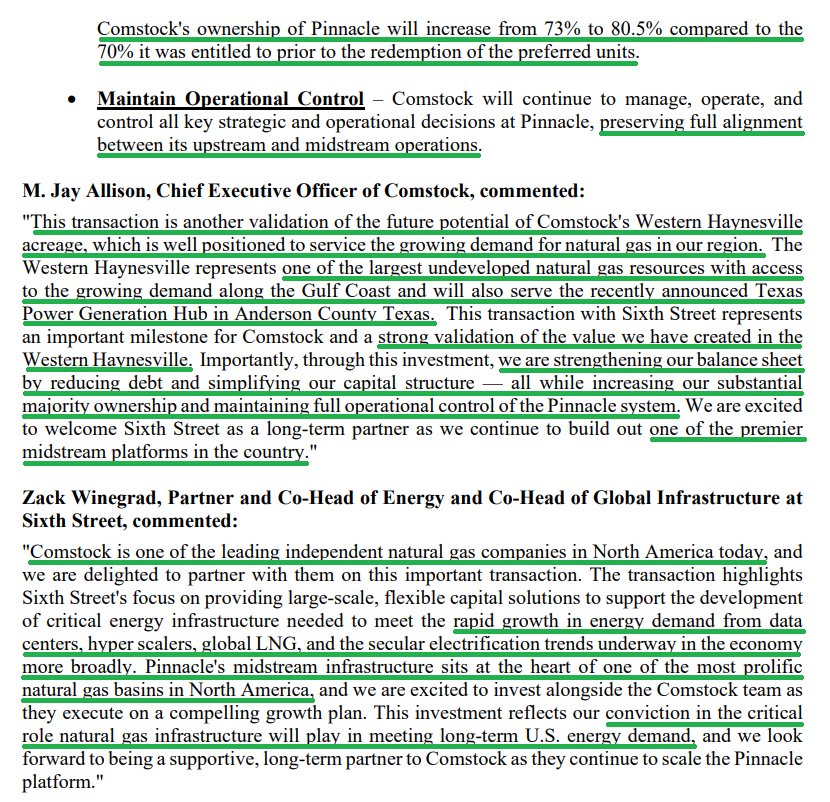

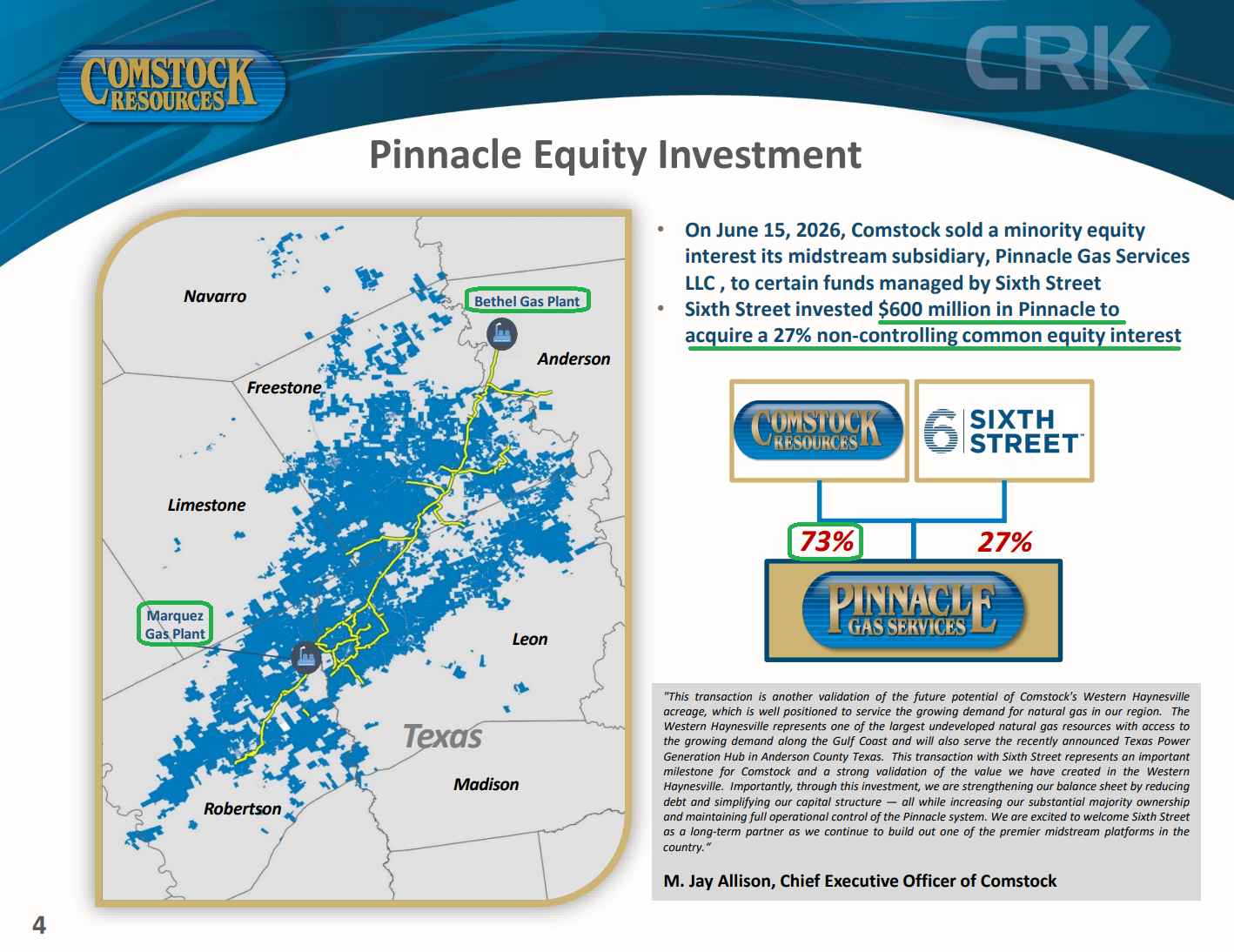

The second catalyst is one management flagged on the call and then delivered just six weeks later. During the call, management said the process of raising outside equity for Pinnacle Gas Services, Comstock’s controlled midstream subsidiary, was progressing well and nearing the finish line.

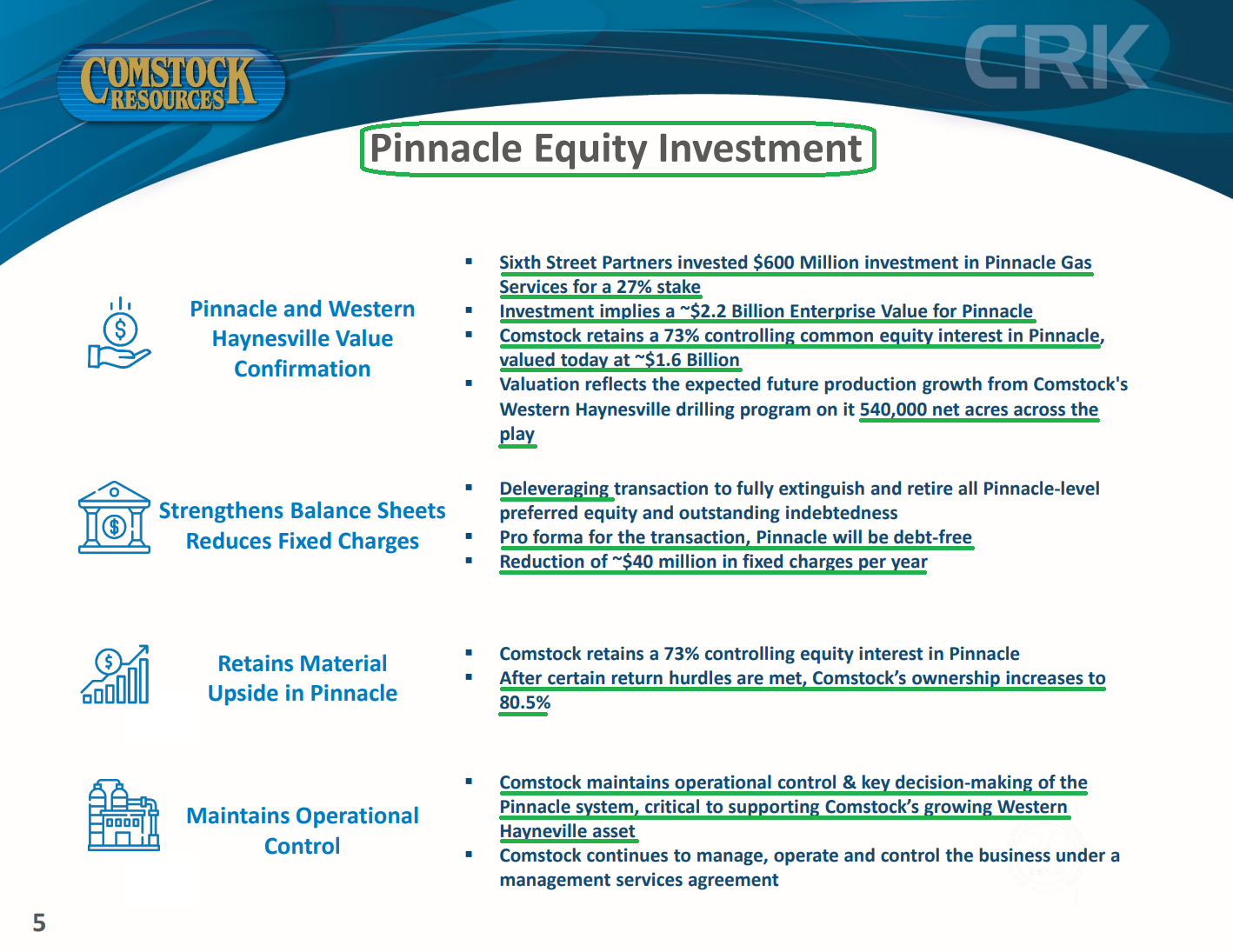

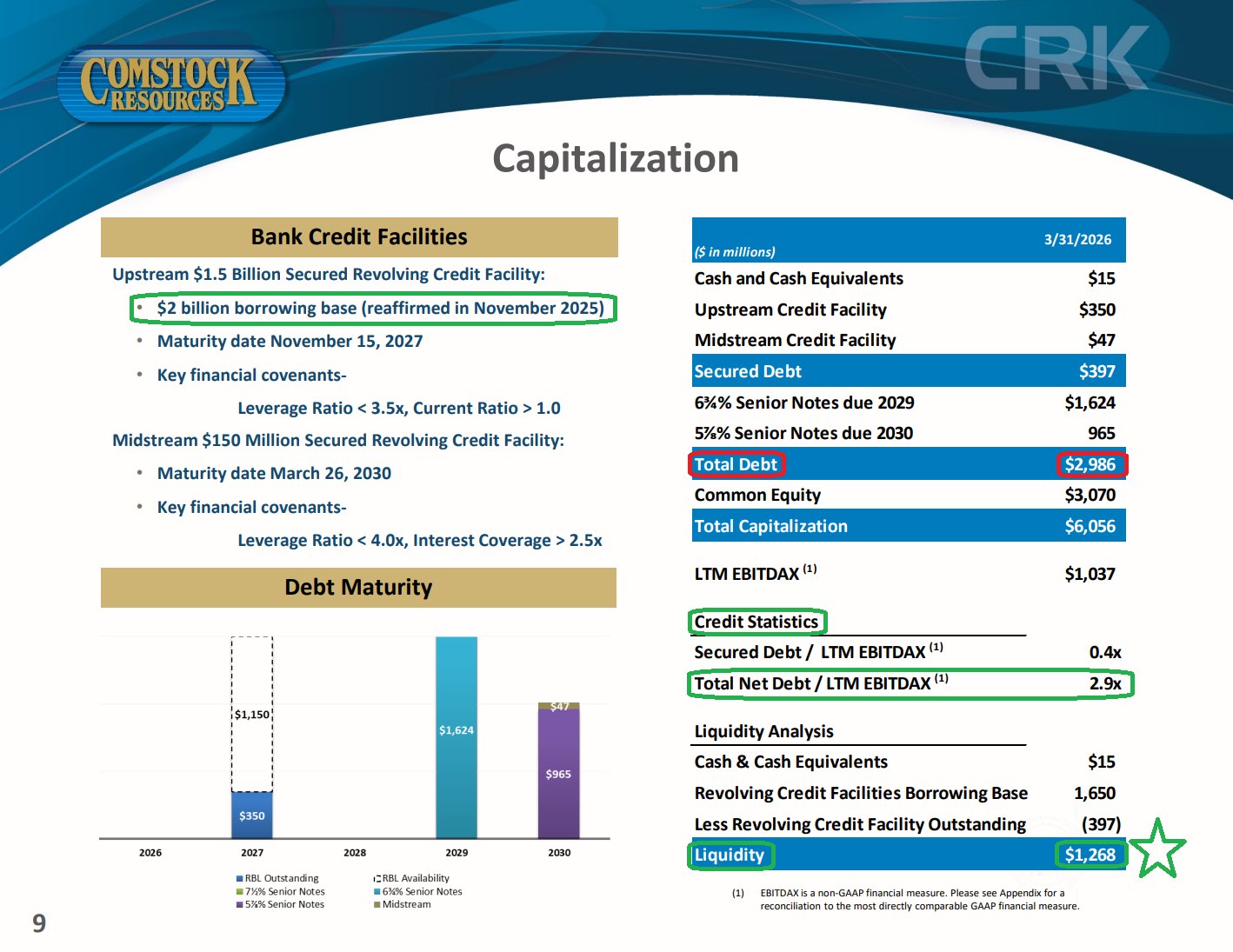

On June 15, they closed the transaction. Sixth Street invested $600M for a 27% non-controlling stake in Pinnacle, implying a $2.2B enterprise value for the midstream business.

From Comstock’s perspective, the transaction does everything you would want. Proceeds fully retire the expensive Quantum preferred units, which carried a 12% dividend on invested capital plus 80% of Pinnacle’s distributions until certain hurdles were met, at a cost of $445M plus accrued dividends. The transaction also eliminates all of Pinnacle’s outstanding debt, stripping ~$40M of annual fixed charges out of the structure in the process. Pinnacle emerges debt-free, Comstock retains a 73% controlling stake worth ~$1.6B, maintains full operational control, and ultimately steps back up to 80.5% ownership once Sixth Street clears its return hurdles.

Looking past the transaction details, the real headline is that an institutional investor managing >$135B just put real money behind a valuation that implies Comstock’s gathering and treating system, 246 miles of high-pressure pipeline, and two treating plants are worth $2.2B, all against a company with an entire market cap of only ~$3.8B. In other words, the pipes and treatment facilities alone are worth nearly 60% of the entire company.

The market, meanwhile, remains focused on storage reports, weather models, and geopolitical headlines, which is perfectly fine by us. Traders are welcome to have the quarter while we take the decade. We were more than happy to take advantage of the recent weakness, building positions for clients who came aboard after we initiated the investment and never had the opportunity to establish one, because the secular story has not changed one bit.

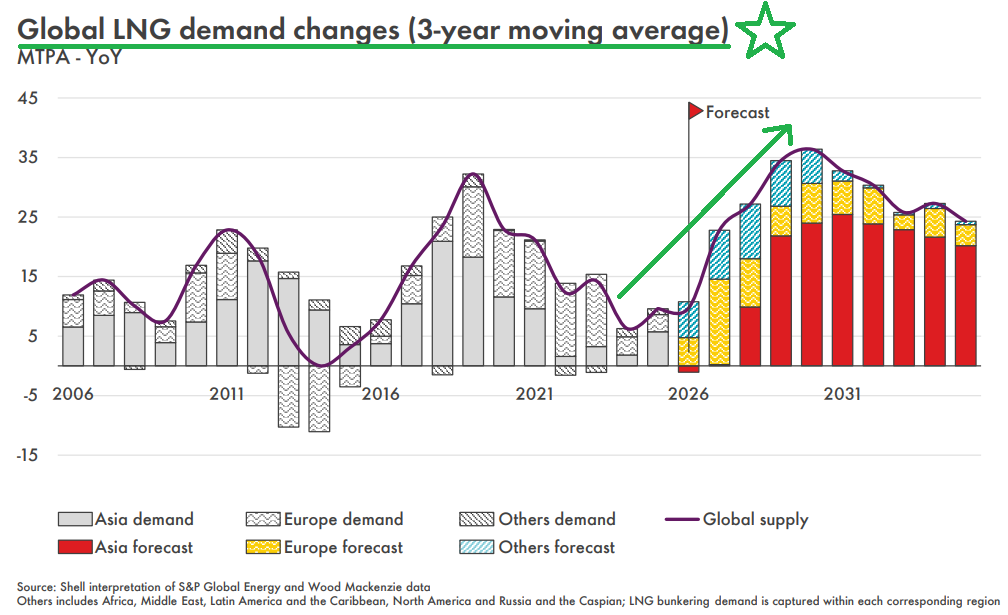

U.S. natural gas markets are structurally tightening as LNG exports accelerate and industrial demand builds along the Gulf Coast. The United States is already the world's largest LNG exporter, and shipments are expected to ~double by the end of the decade. Shell (SHEL)'s latest outlook projects global LNG demand increasing ~65% by 2050, approaching 700M tons annually compared to the 422M tons traded in 2025.

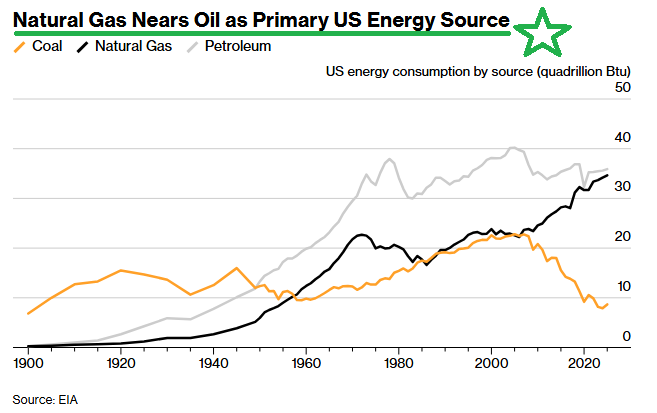

Then there is the milestone that says it all. Natural gas accounted for 36% of U.S. energy consumption in 2025, just shy of petroleum at 37%. By the end of the decade, natural gas is expected to surpass oil for the first time since 1950, when petroleum overtook coal.

Layer accelerating data center demand on top of the LNG export wave and you arrive at ~3 Bcf/d of incremental natural gas demand each year through 2030. At that point, the question stops being whether demand will materialize and starts being where all of that gas is going to come from. Comstock has positioned itself to be the answer.

The key point the market is missing: The entire world is busy trying to pick the winner of the AI era, debating which model, which chip, which hyperscaler, and which shiny object will come out on top next quarter. We would rather own the sure thing. Across the entire AI ecosystem, there is exactly one certainty: none of it runs without natural gas. Not the models, not the data centers, not a single query.

So we will happily own the industry’s lowest-cost producer, sitting on one of the best footprints in America, right alongside Jerry Jones, who controls ~71% of the company and sees more upside in his Comstock stake than in the most valuable sports franchise on the planet.

Now we’re cooking with gas.

Q1 Earnings Breakdown

10 Key Points

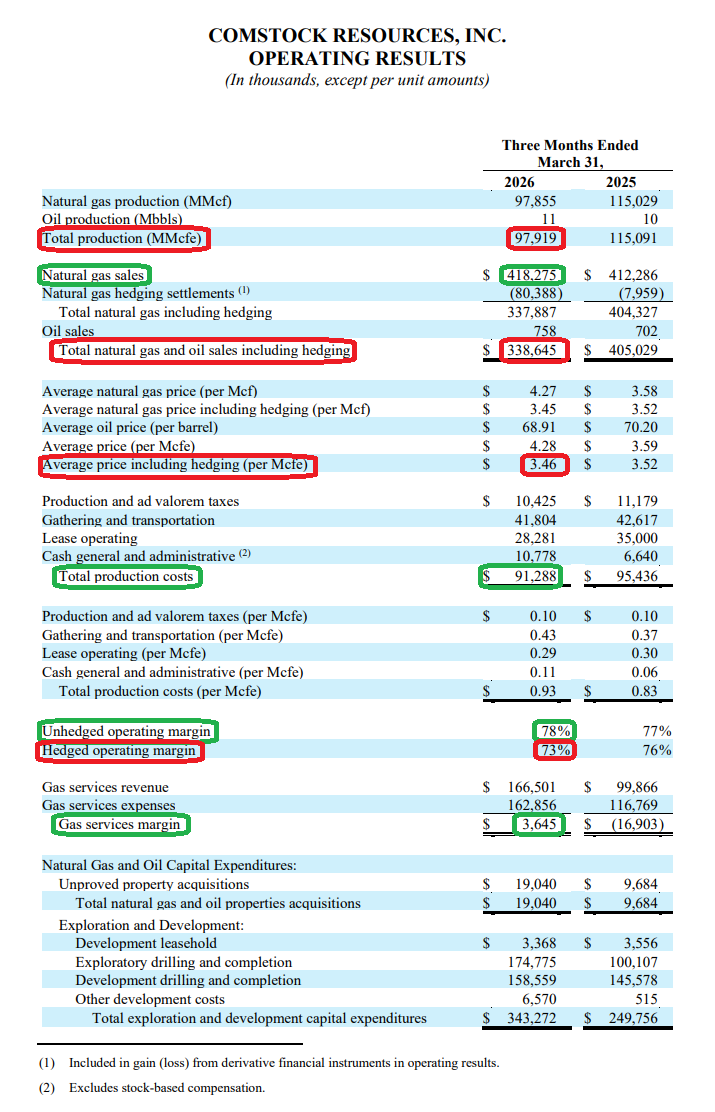

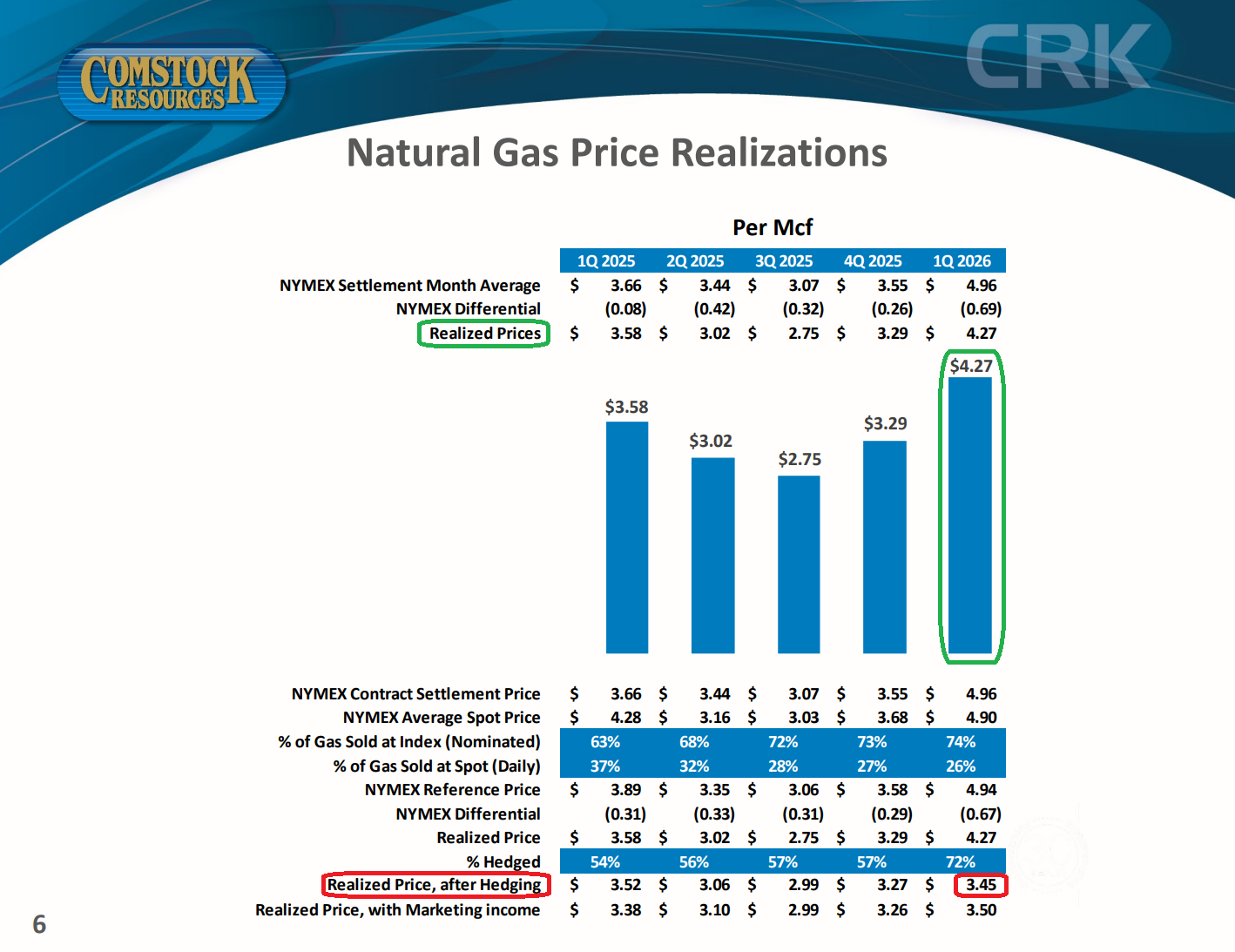

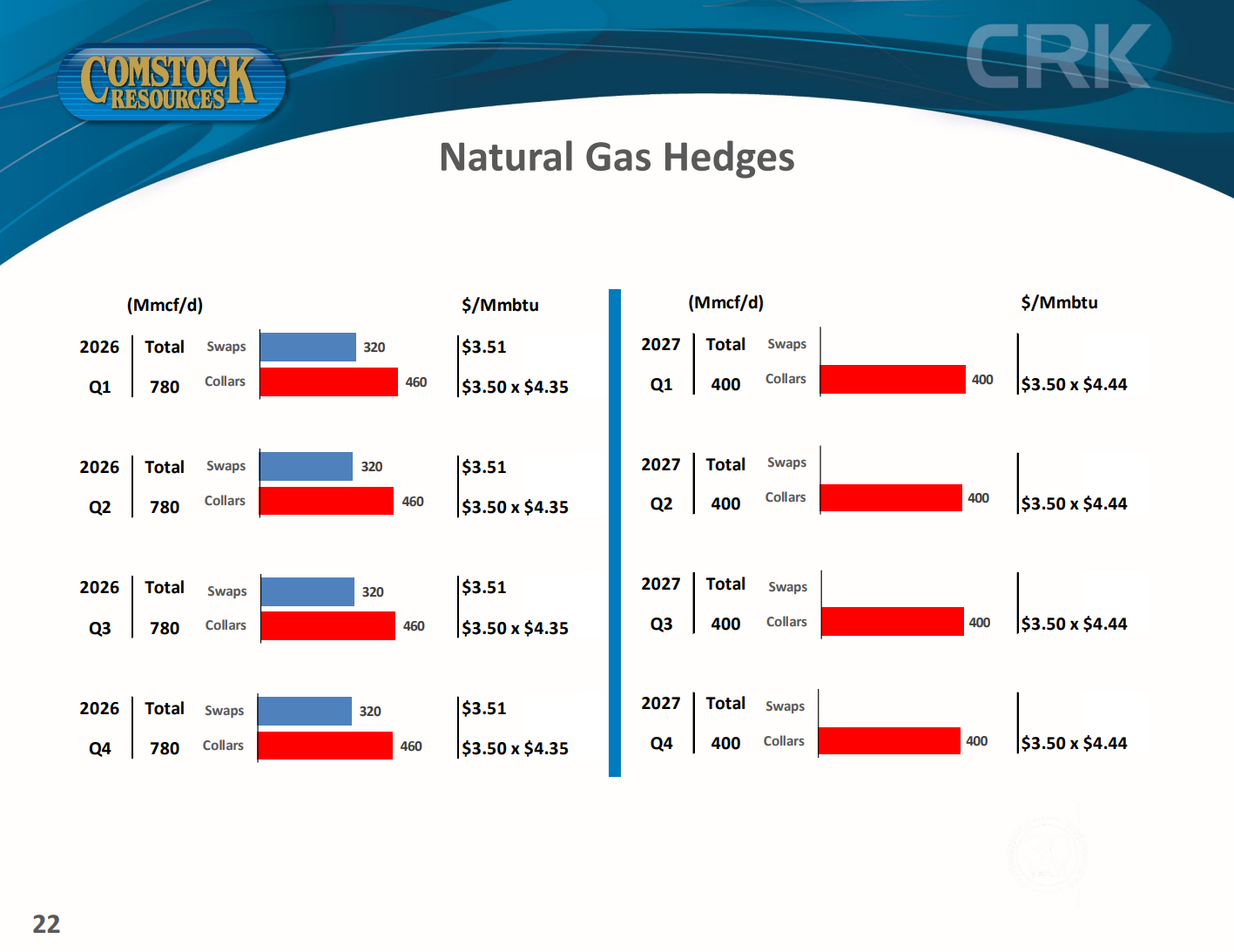

1) Natural gas and oil sales totaled $338.6M in Q1 (-16.4% Y/Y), including $80.4M of realized hedging losses. Production averaged 1,088 MMcfe/d (-14.9% Y/Y), landing within the 1,075 to 1,150 MMcfe/d guidance range but ~2% below the midpoint, as significant winter weather forced shut-ins and pushed several well completions into the following quarter. Before hedging, the realized gas price was $4.27/Mcf (+19.3% Y/Y), tracking a NYMEX settlement average of $4.96 versus $3.66 last year. After hedging, however, the realized price came in at $3.45/Mcf (-2.0% Y/Y), as a materially larger hedge book (72% hedged vs. 54%) capped the upside. Third-party marketing added another $0.05/Mcf, lifting the all-in realized price to $3.50/Mcf.

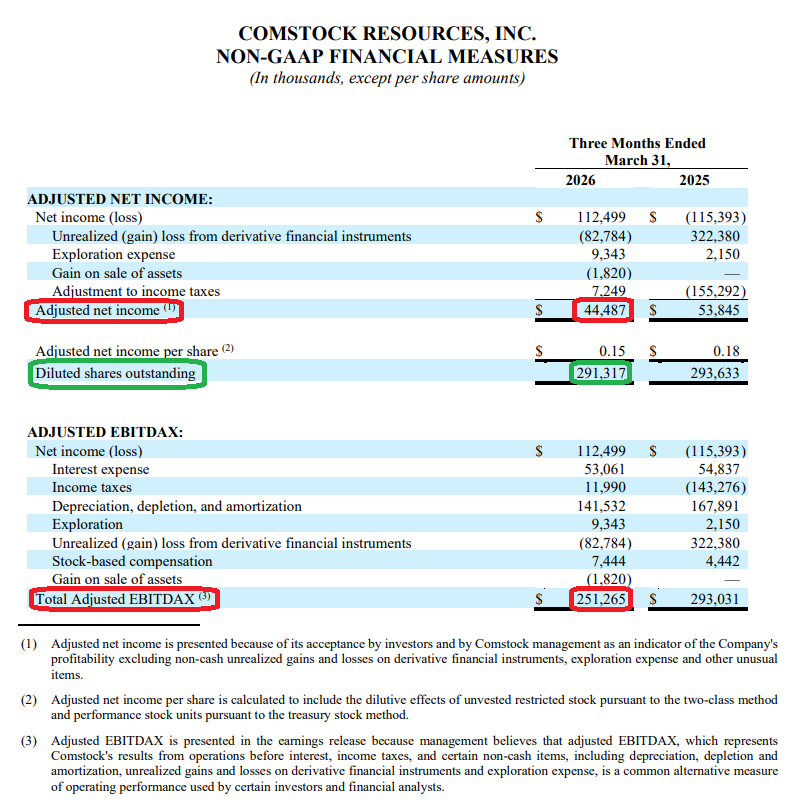

2) Adjusted net income totaled $44.5M in the first quarter, down 17.4% Y/Y from $53.8M. On a per share basis, adjusted EPS came in at $0.15 (-16.7% Y/Y from $0.18), below Street consensus of $0.23.

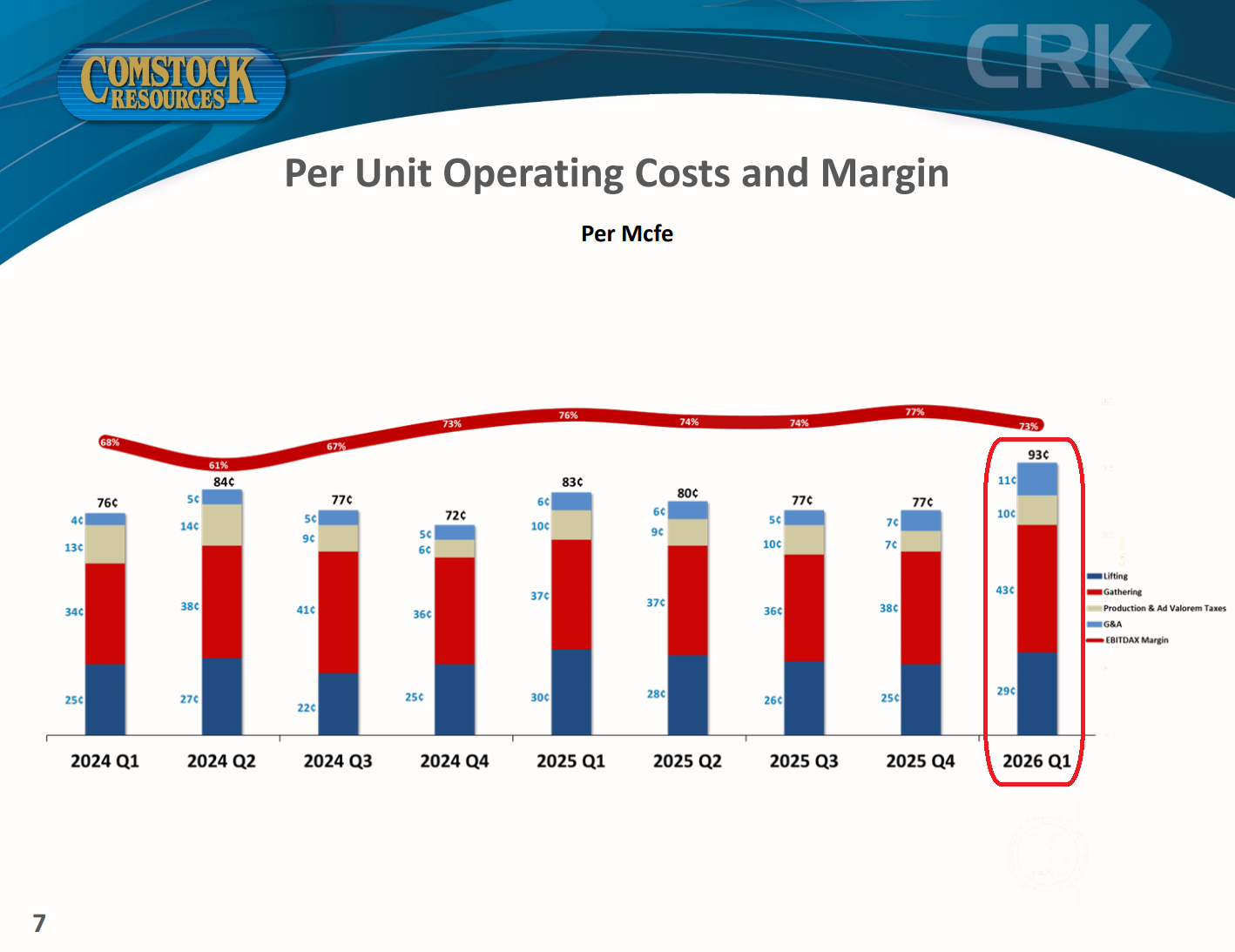

3) Adjusted EBITDAX was $251.3M (-14.2% Y/Y from $293.0M), reflecting lower production volumes against a largely fixed field cost base. Production costs averaged $0.93/Mcfe versus $0.83 last year and $0.77 in Q4, consisting of $0.43 for gathering and transportation, $0.29 for lease operating expenses, $0.10 for production and ad valorem taxes, and $0.11 for cash G&A. Within the $0.16 sequential increase, lifting costs and cash G&A each rose $0.04 on lower production levels, production and ad valorem taxes increased $0.03 on higher gas prices, and gathering costs increased $0.05 due to prior period adjustments. Unhedged operating margin improved to 78% (+100 bps Y/Y, +100 bps Q/Q), while hedged operating margin came in at 73% (-300 bps Y/Y, -400 bps Q/Q). Even with the quarter's cost headwinds, Comstock's cost structure remains ~43% below the peer average.

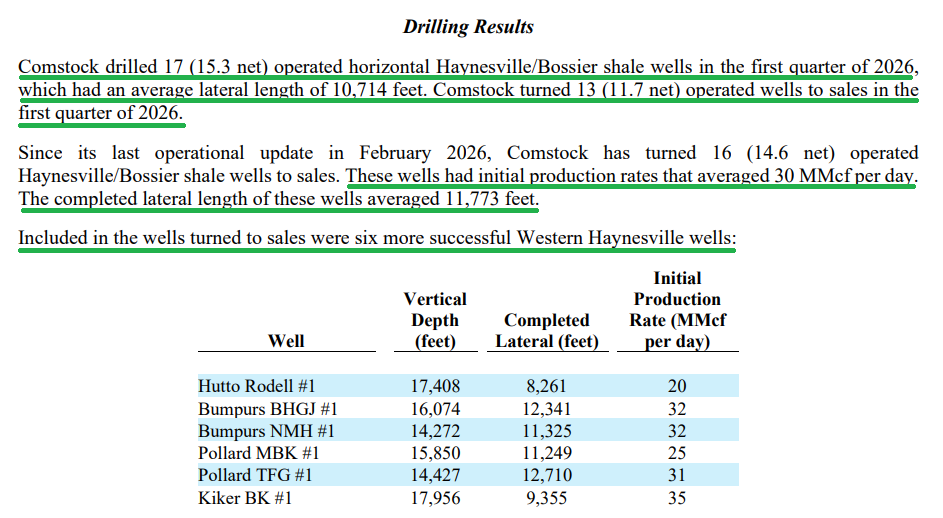

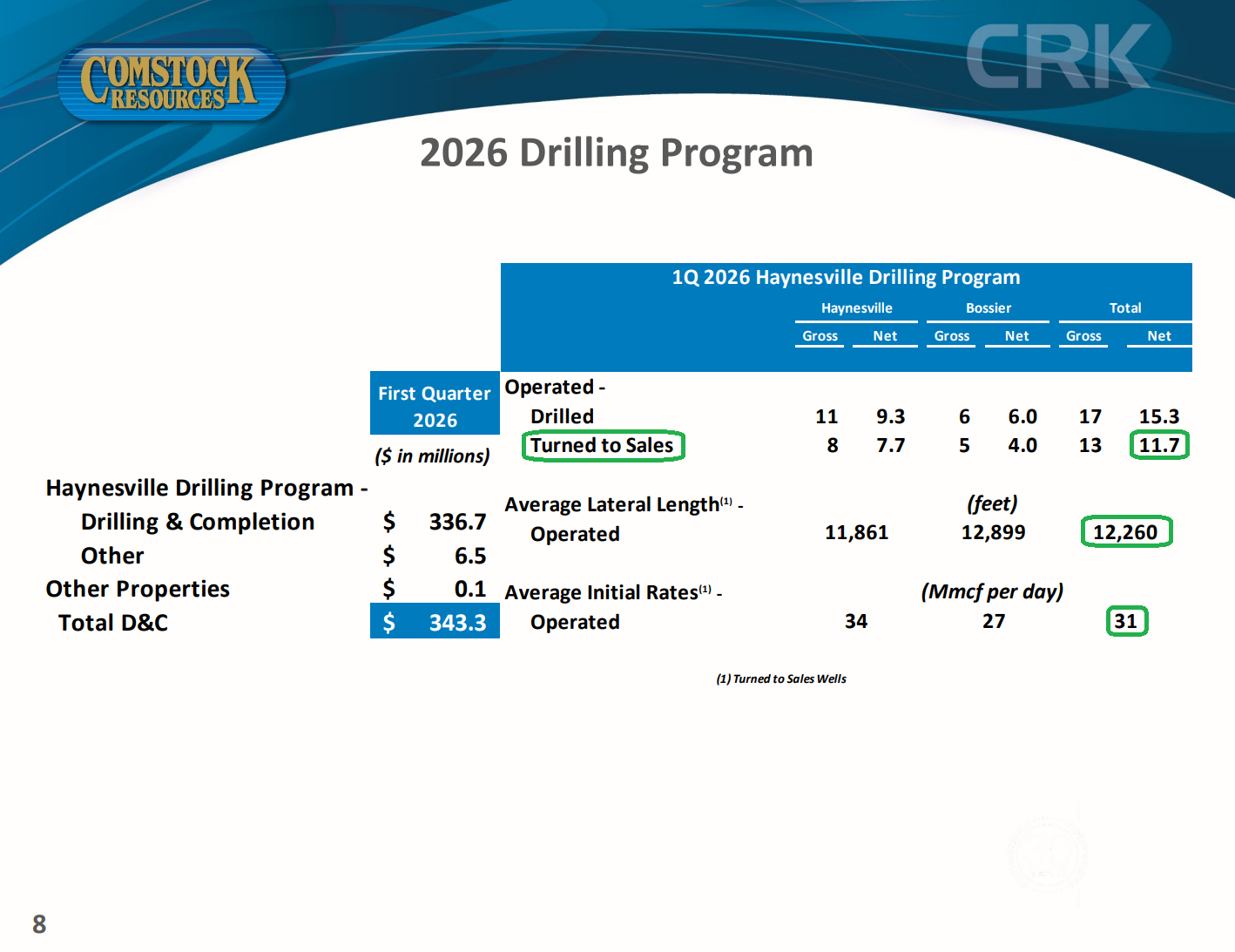

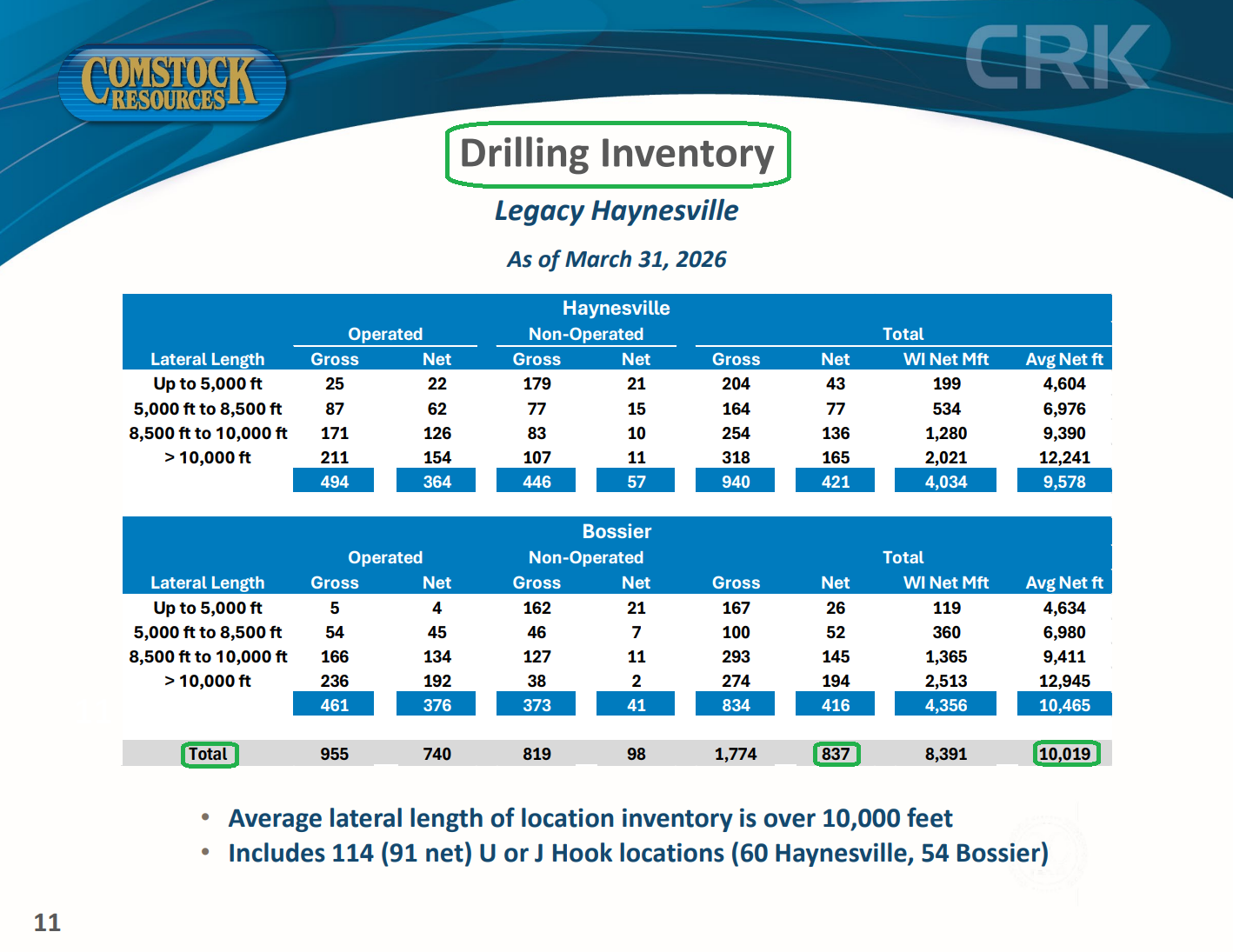

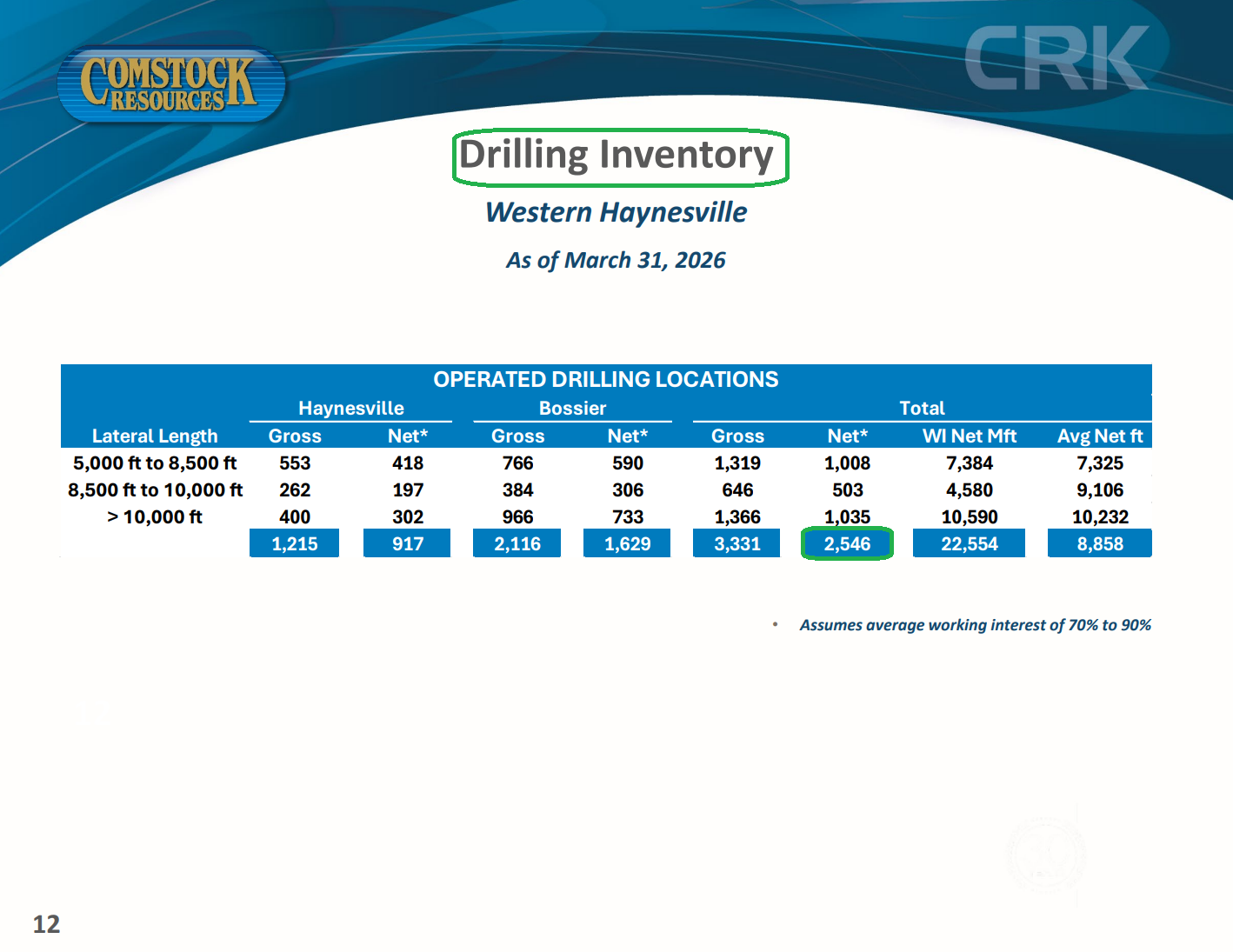

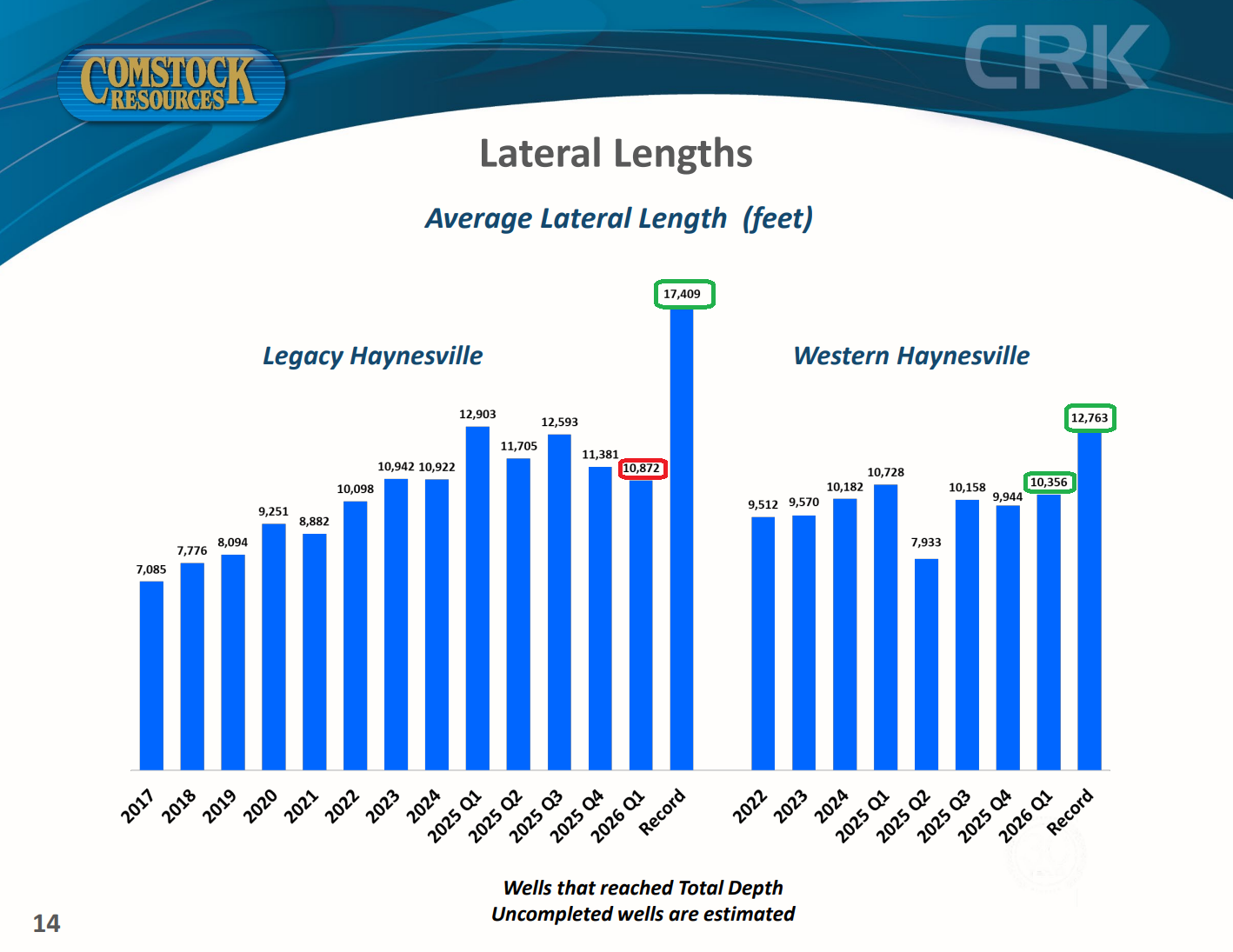

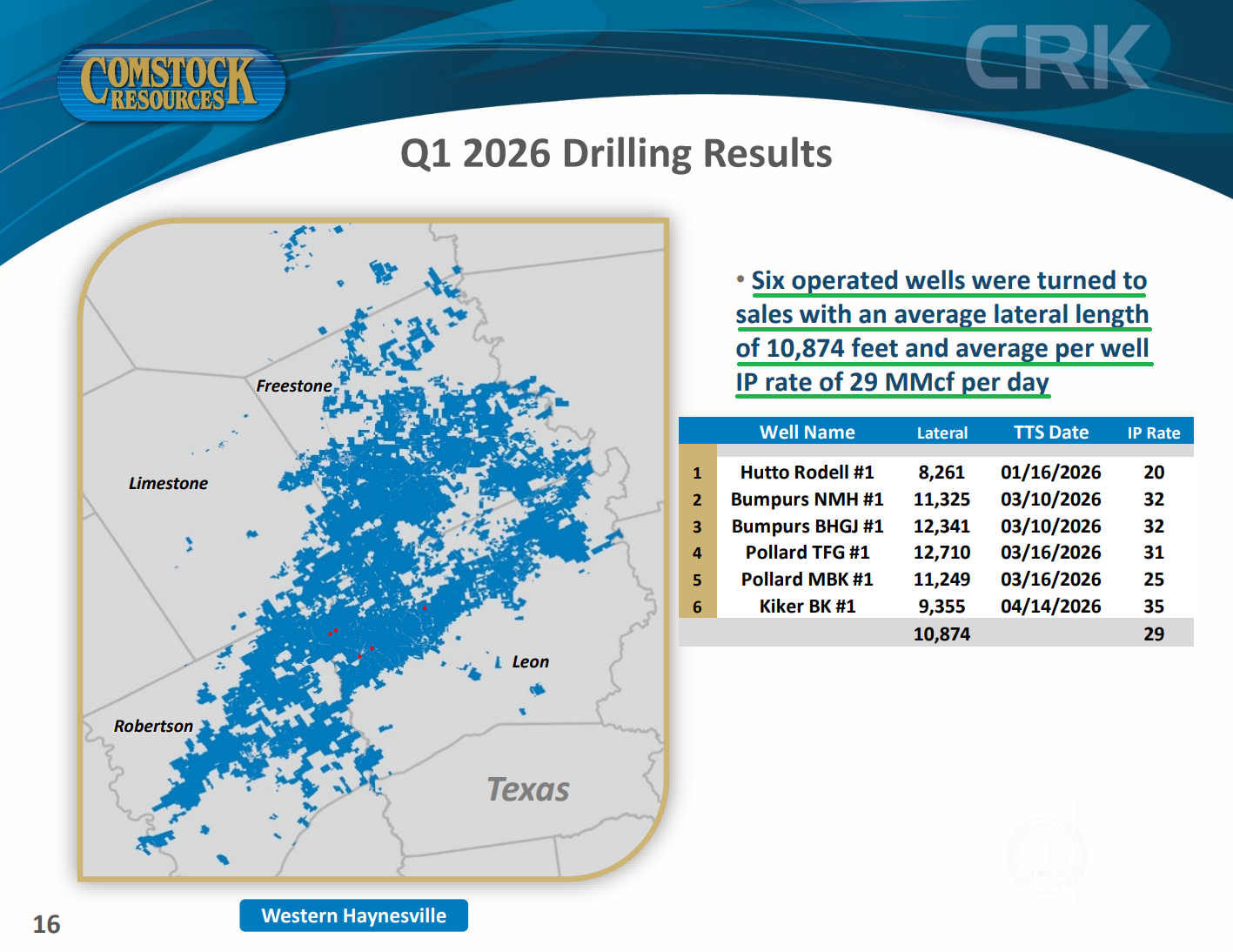

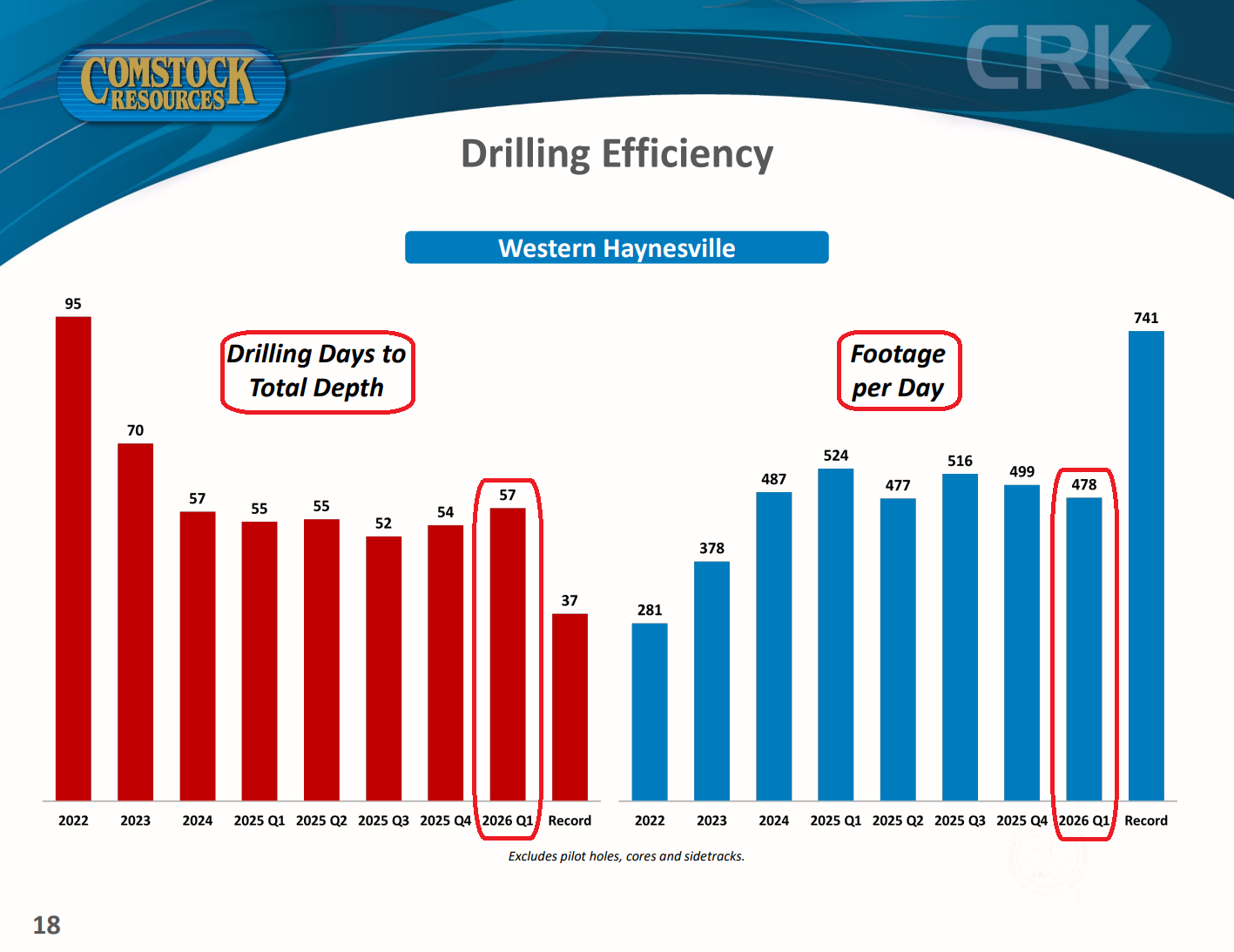

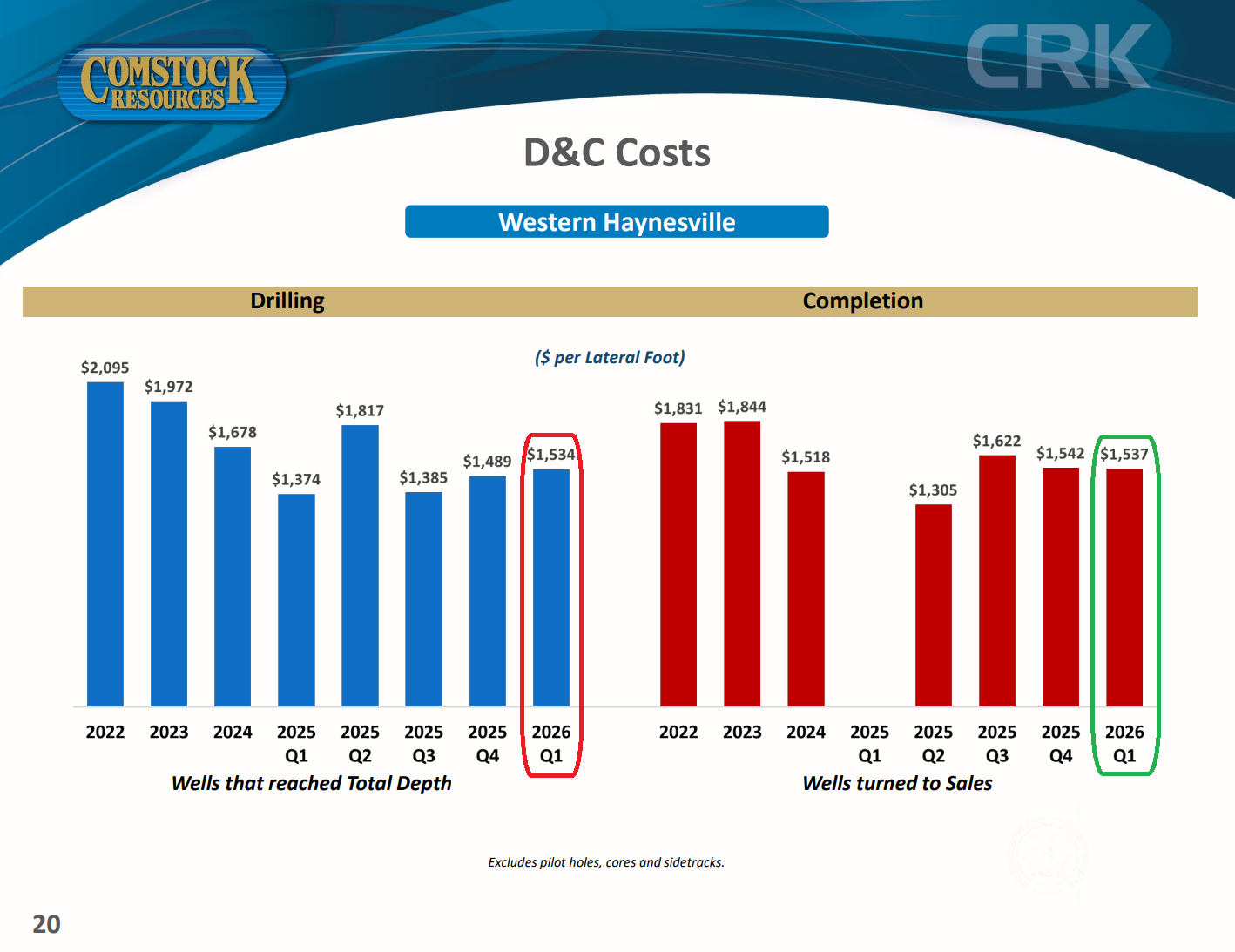

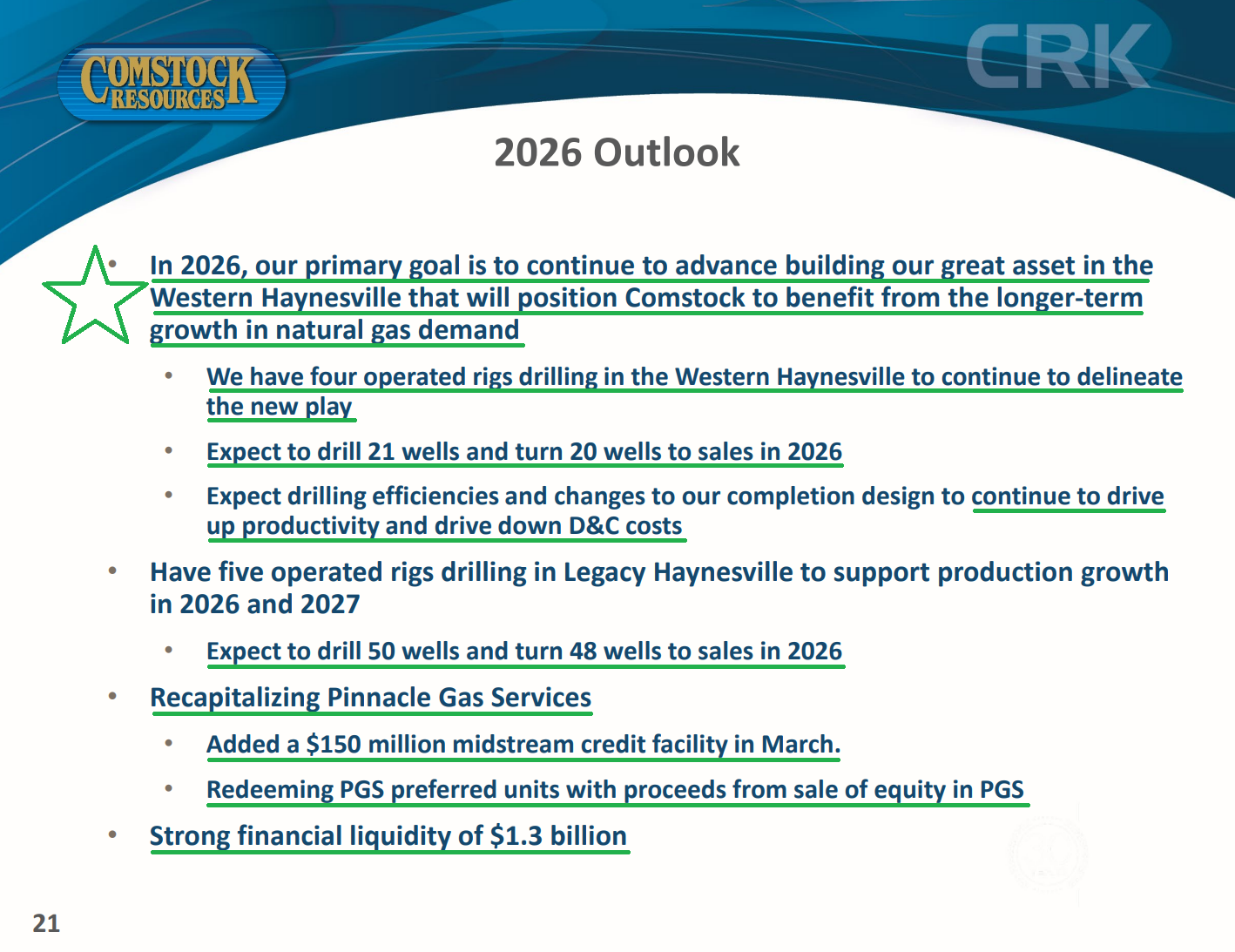

4) The "holy grail" Western Haynesville footprint has grown to 540,410 net acres with 3,331 gross and 2,546 net operated locations at an average working interest of ~76% and an average net lateral length of 8,858 feet. Comstock turned six wells to sales during the quarter with an average lateral length of 10,874 feet and a 29 MMcf/d IP rate, bringing the play to 36 producing wells and 44 drilled to total depth. Drilling performance stepped back, with days to total depth rising to 57 (+5.6% Q/Q, +3.6% Y/Y) and footage per day falling to 478 (-4.2% Q/Q, -8.8% Y/Y), while drilling costs increased to $1,534/lateral foot (+3.0% Q/Q, +11.6% Y/Y) and completion costs remained essentially flat at $1,537/lateral foot (-0.3% Q/Q). Management remains focused on lowering costs, having drilled a record 14,800-foot lateral with a larger hole size and insulated drill pipe that achieved the company's lowest cost per foot to date. A 10,000 PSI rig upgrade is expected by late summer, with higher temperature-rated motors set for testing later this year. Four operated rigs are active across the acreage, with 21 wells expected to be drilled and 20 turned to sales in 2026, and management continues to expect the play to yield significantly more resource per section than the legacy Haynesville.

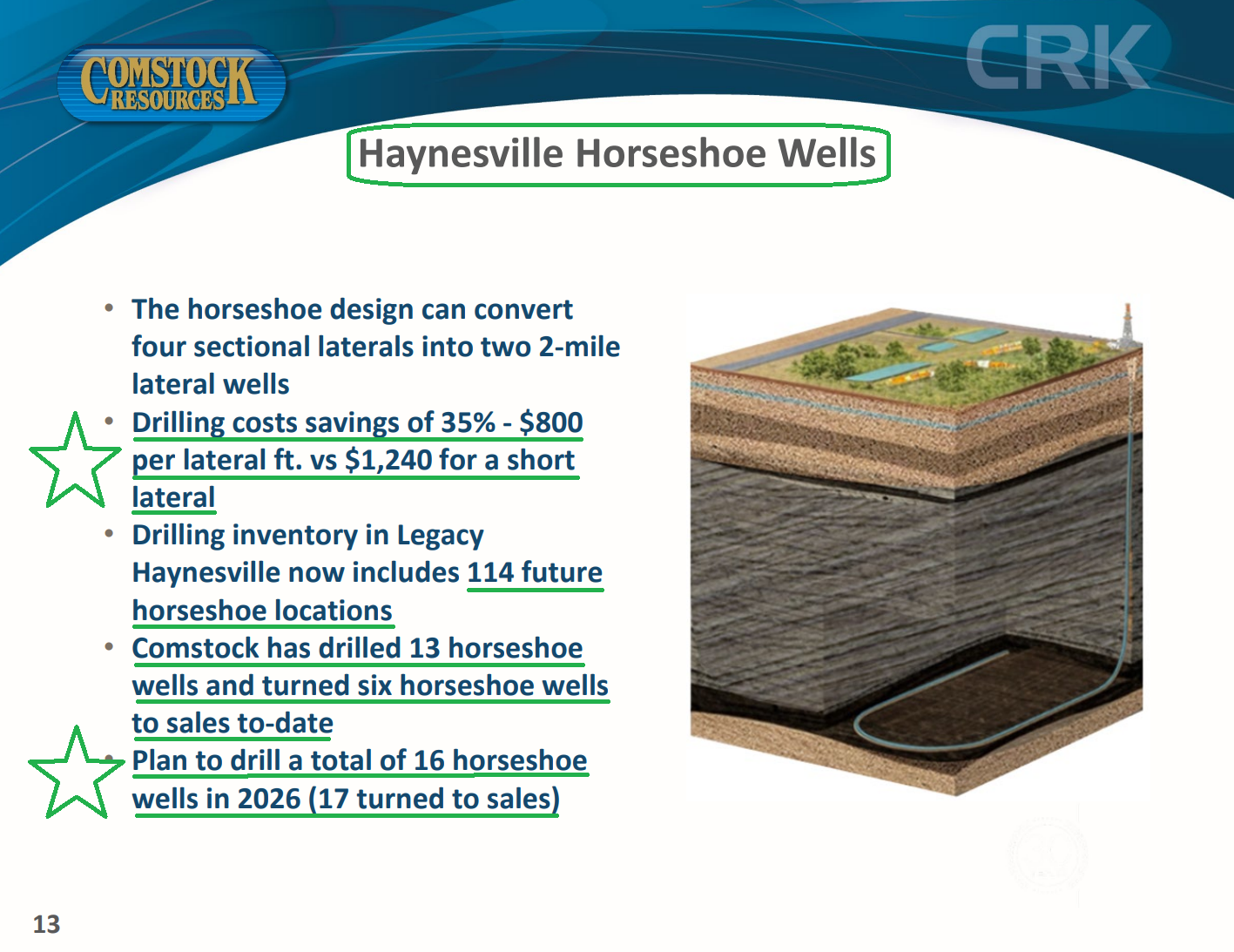

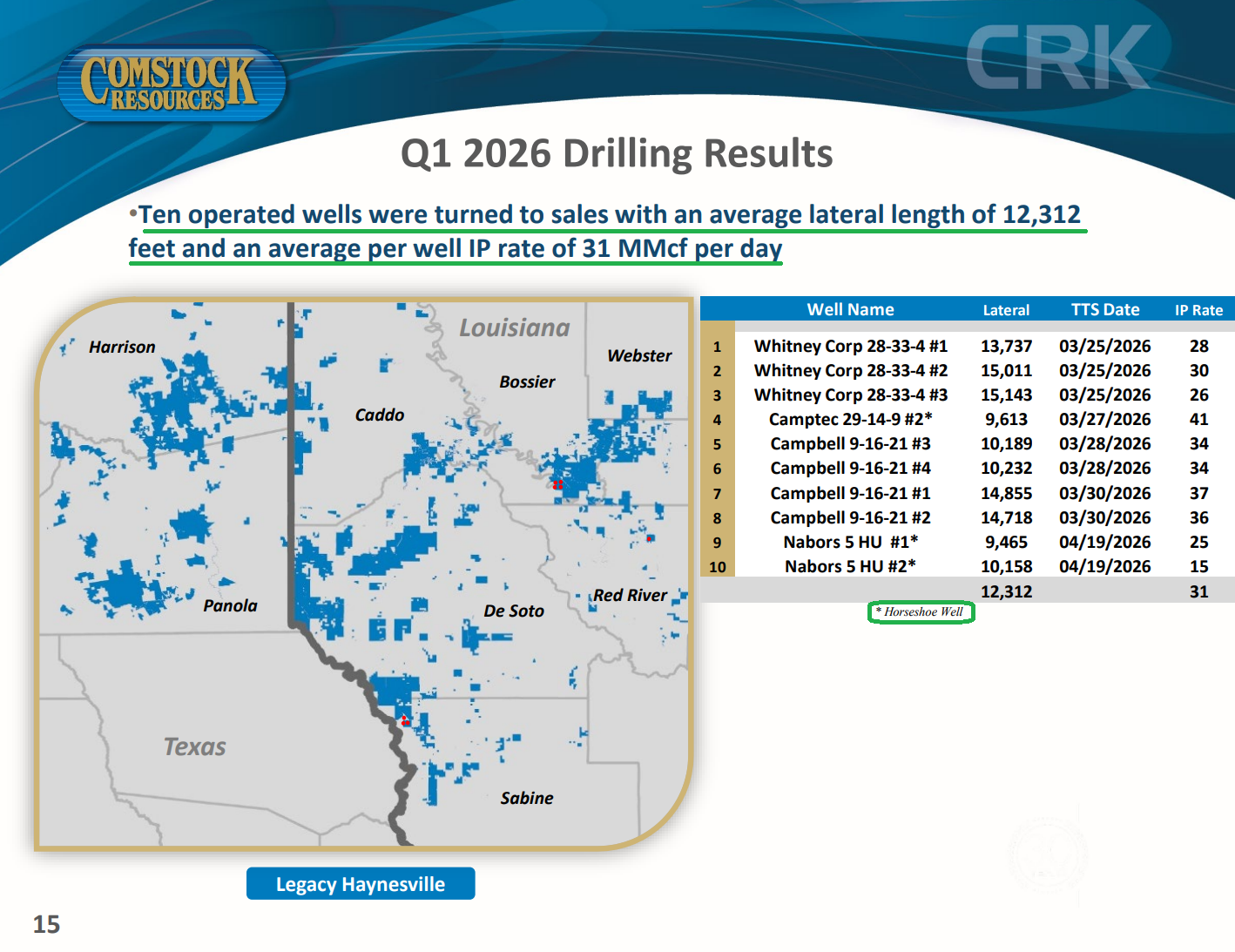

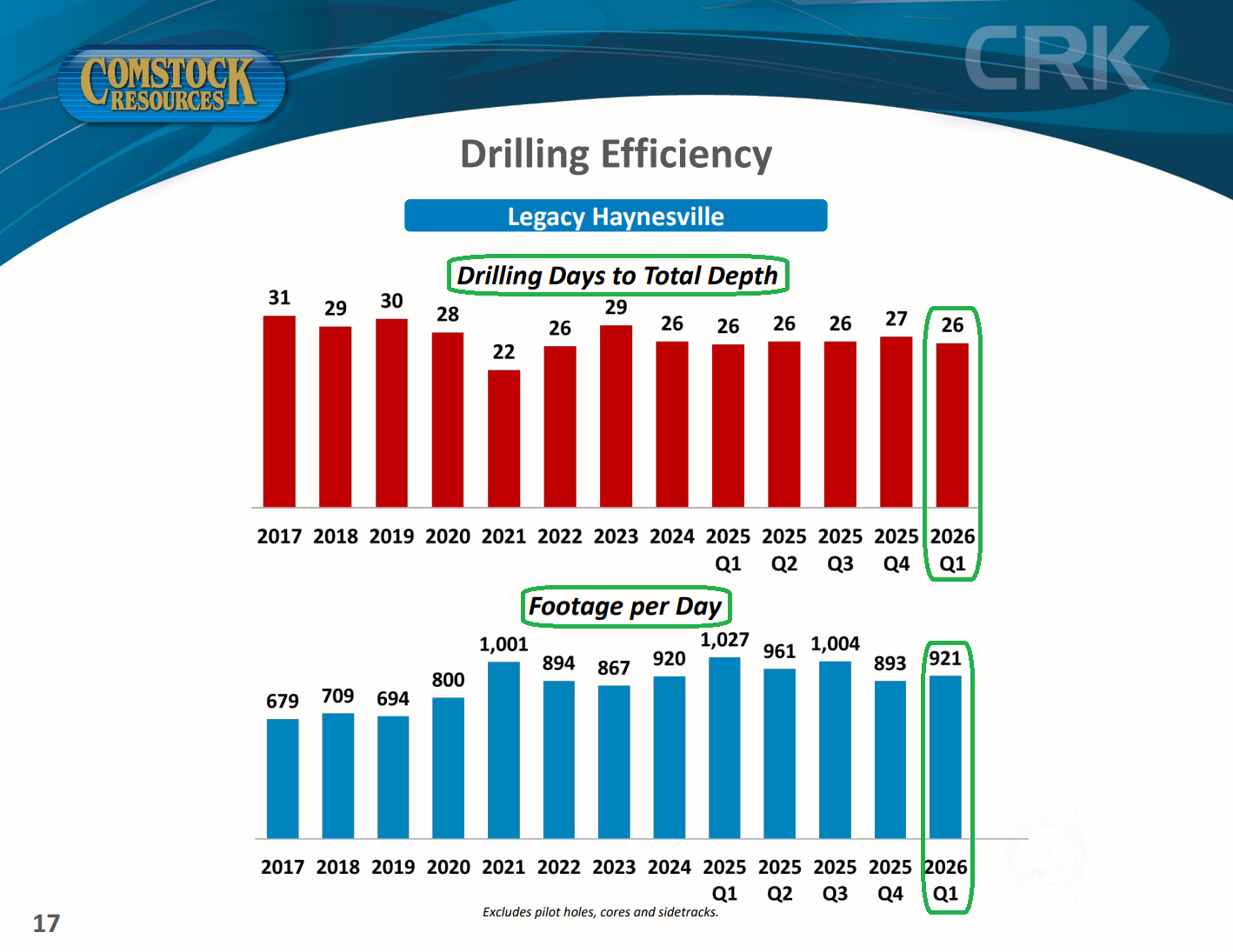

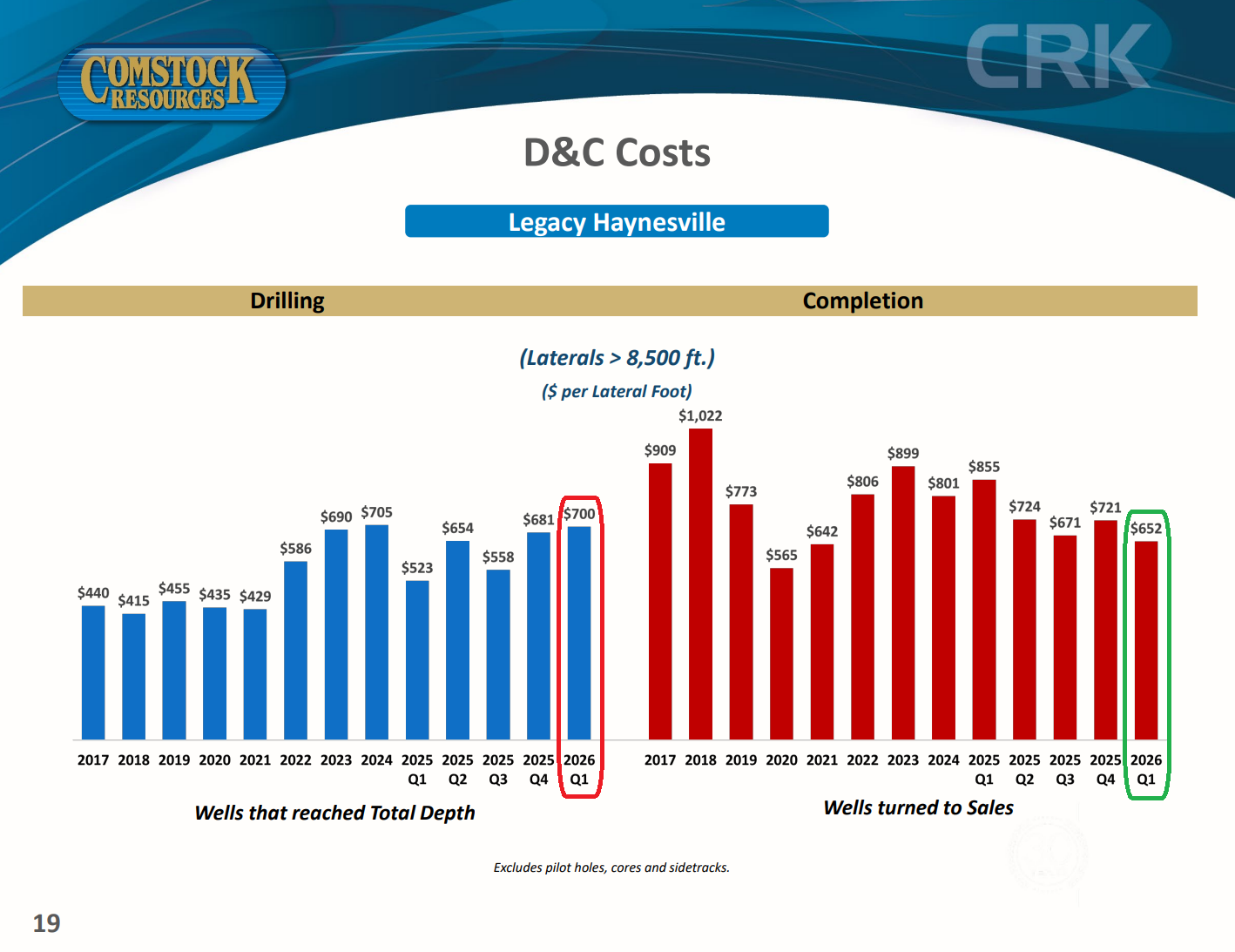

5) Comstock turned 10 operated legacy wells to sales during the quarter with an average lateral length of 12,312 feet and an average IP rate of 31 MMcf/d, across a footprint spanning 266,570 net acres with 837 net locations and an average net lateral length of 10,019 feet. Drilling efficiency improved, with days to total depth falling to 26 (-3.7% Q/Q) and footage per day rising to 921 (+3.1% Q/Q, -10.3% Y/Y). On the cost side, drilling costs increased to $700/lateral foot (+2.8% Q/Q, +33.8% Y/Y) on shorter average laterals, more horseshoe wells, and additional casing strings in East Texas, while completion costs fell to $652/lateral foot (-9.6% Q/Q, -23.7% Y/Y) on lower horsepower and better frac efficiency. The horseshoe program continues to deliver ~35% drilling cost savings ($800/lateral foot vs. $1,240 for short laterals), with 114 future locations booked, 13 drilled to date, and 16 planned in 2026. Five of Comstock's nine rigs are working the legacy acreage, where management expects to drill 50 wells and turn 48 to sales this year.

6) On March 19, the U.S. Department of Commerce selected the Western Haynesville to host the Texas Natural Gas-Fired Power Generation Hub, a ~$16B facility in Anderson County, Texas, tied to Japan's $550B U.S. investment commitment under the U.S.-Japan trade deal. The project will be jointly owned by Japan and the U.S. and built and operated by NextEra, a Comstock partner since 2015. The facility will feature up to 5.2 GW of dispatchable gas-fired generation, capable of serving up to 5 GW of large-load demand from data centers and advanced manufacturing. Comstock does not own the surface rights and bears none of the construction obligation but will supply the natural gas, with volumes potentially reaching ~1 Bcf/d by 2031.

7) On June 15, weeks after the quarter closed, Comstock sold a 27% non-controlling common equity interest in its midstream subsidiary, Pinnacle Gas Services, to Sixth Street for $600M, implying a ~$2.2B enterprise value for Pinnacle. Comstock retains a 73% controlling interest worth ~$1.6B and continues to manage, operate, and control all key strategic and operational decisions under a management services agreement. The proceeds fully extinguished the expensive Quantum preferred units ($445M plus accrued dividends), along with all Pinnacle-level debt, leaving the midstream entity debt-free and reducing fixed charges by ~$40M per year. Should Sixth Street clear certain return hurdles, its stake steps down to 19.5% and Comstock's rises to 80.5%, above the 70% it would have been entitled to before the preferred redemption.

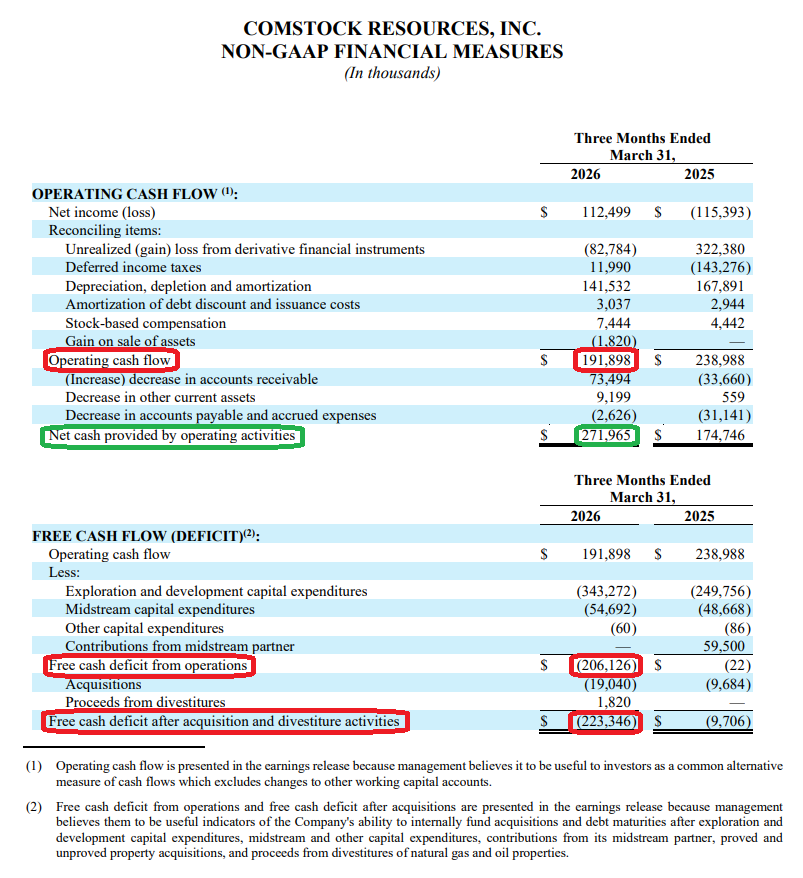

8) Operating cash flow was $191.9M, or $0.66 per diluted share (-19.7% Y/Y from $239.0M), reflecting lower production and EBITDAX during the quarter. Free cash flow swung to a $206.1M deficit from operations versus essentially breakeven in the prior year period, as lower cash generation coincided with a stepped-up capital program that included $343.3M of exploration and development spending (+37.4% Y/Y) and $54.7M of midstream capex tied to the Western Haynesville buildout. Including acquisitions and divestitures, the free cash flow deficit widened to $223.3M. Management has guided to an outspend of $400M to $450M for the year, depending on gas prices, with Pinnacle's capital intensity expected to step down once its second treating plant comes online this summer.

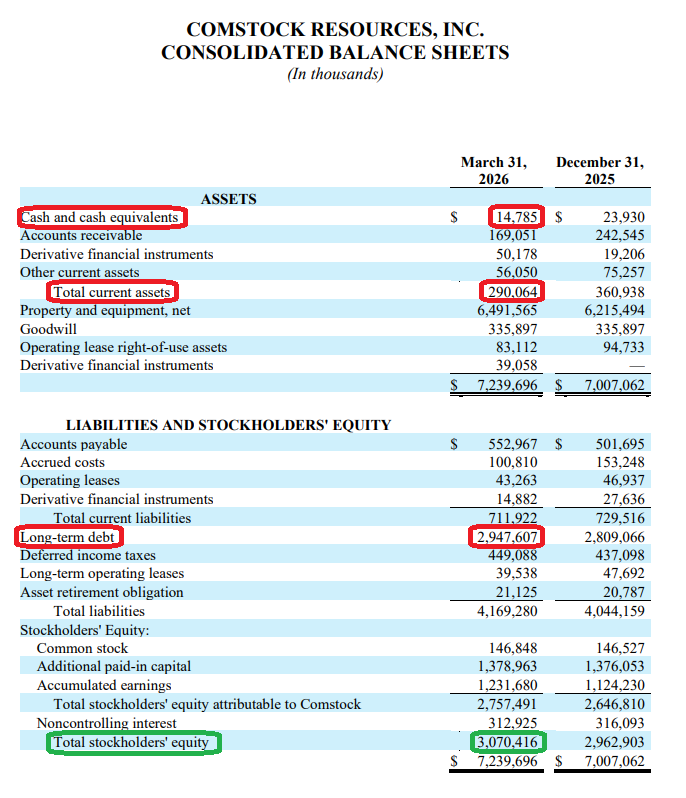

9) Comstock ended the quarter with $14.8M of cash and $2.99B of total debt, comprised of $350M drawn on the upstream revolver, $47M on the new midstream facility, $1.62B of 6.75% senior notes due 2029, and $965M of 5.875% senior notes due 2030. Net leverage stood at 2.9x LTM EBITDAX, comfortably within the 3.5x upstream and 4.0x midstream covenants, with $1.27B of liquidity and no maturities until the revolver comes due in November 2027. The $150M secured midstream revolver added for Pinnacle in March carries no recourse to the upstream credit structure.

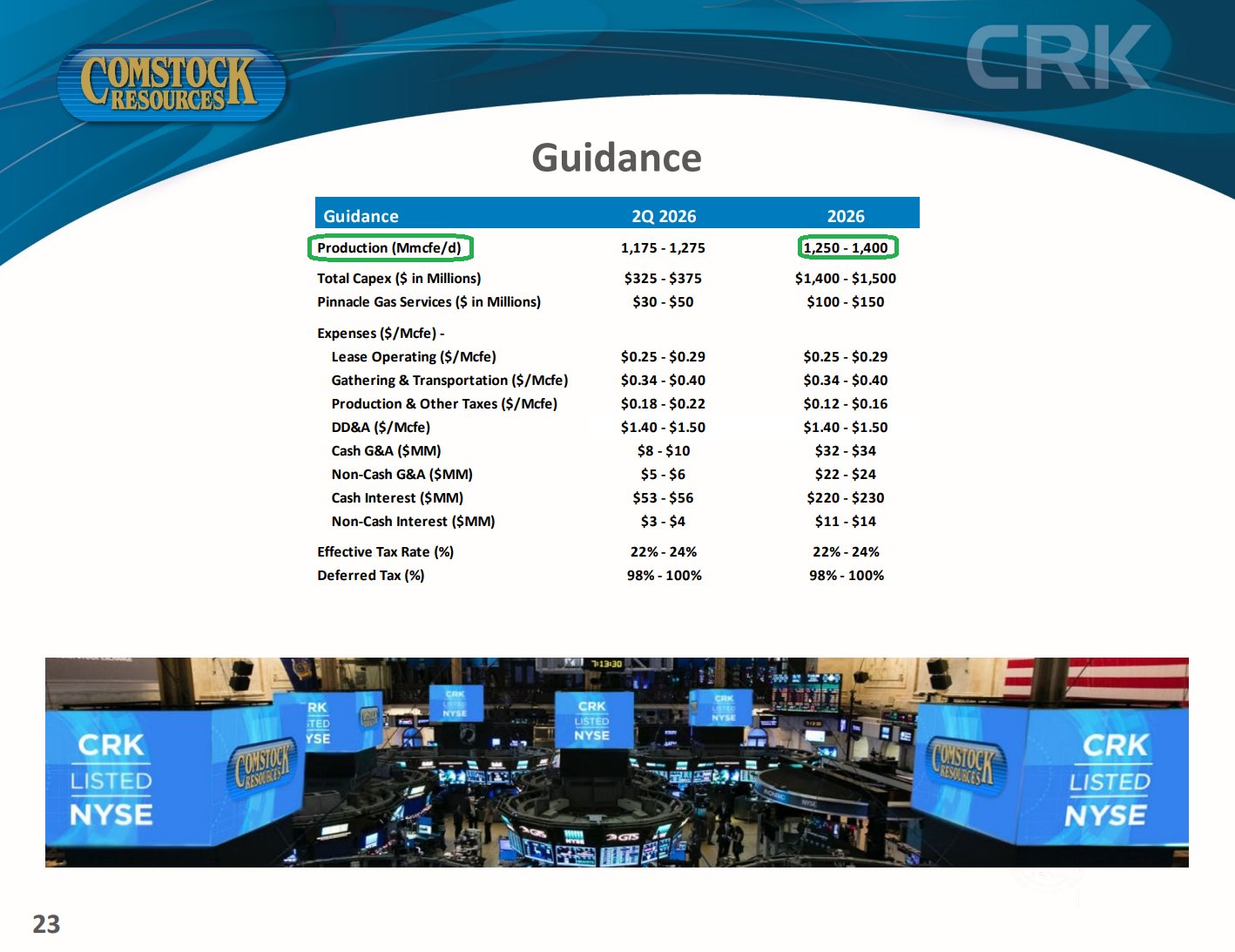

10) Management maintained full-year 2026 production guidance of 1,250 to 1,400 MMcfe/d and total capex of $1.4B to $1.5B, plus $100M to $150M for Pinnacle. Second quarter production is guided to 1,175 to 1,275 MMcfe/d, representing a 13% to 15% sequential increase as the wells completed late in Q1 come online and a fourth frac fleet, added in May, ramps up. Referencing the production shortfall and elevated capex that defined the quarter, Allison put it simply: "I think we've turned the corner."

Earnings Call Highlights

General Market

The CNN “Fear and Greed Index” ticked up to 48 this week from 44 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

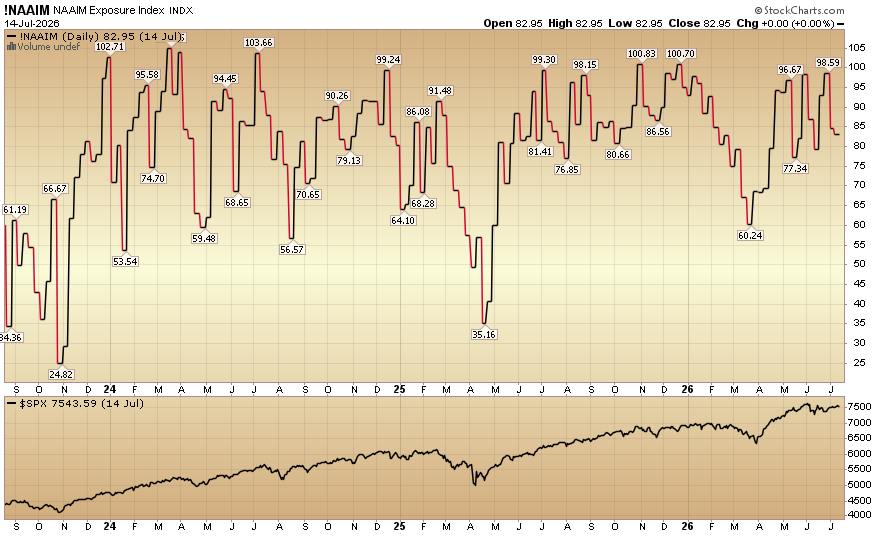

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) ticked down to 82.95% equity exposure this week from 84.69% last week.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Congratulations to all of the new clients that came in during the second quarter (Q2), and to those existing clients who upsized their contributions to their accounts.

Our opening for smaller accounts ($1.5M+) is now officially closed. Thank you to everyone who took advantage of the opportunity.

Larger accounts $5–10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms

Comments

Log in or sign up to join the conversation.