For decades, retirees were taught a simple formula for financial safety: reduce stock exposure, increase bonds and cash, and prioritize stability over growth. That approach worked remarkably well during one of the greatest disinflationary periods in modern financial history. From the early 1980s through 2020, inflation generally trended lower, interest rates steadily declined, and both stocks and bonds benefited from falling yields and abundant global growth.

Today, however, the investment environment may be changing in ways many retirees are not fully prepared for.

The greatest mistake many retired investors could make over the coming decade may not be taking too much risk. It may be becoming too conservative too early in retirement and allowing inflation to slowly erode purchasing power over time.

Retirement planning is no longer just about avoiding volatility. It is increasingly about protecting real wealth against a world of structurally higher inflation pressures, rising geopolitical instability, and changing global economic dynamics.

10-Year Treasury Yield Cycle

Source: Bloomberg

The Inflation Regime May Be Changing

Many investors forget how unusual the 1980–2020 period truly was. In 1981, the 10-year Treasury yield peaked above 15% as the Federal Reserve aggressively fought inflation. Over the next four decades, interest rates generally declined until the 10-year Treasury briefly fell below 1% during the COVID era in 2020.

That roughly 40-year decline in interest rates created a powerful tailwind for nearly all financial assets. Bonds appreciated as yields fell. Growth stocks thrived as lower rates boosted valuations. Globalization kept goods prices low. Cheap labor and efficient supply chains helped suppress inflation across developed economies.

But secular inflation cycles can last decades.

The inflationary period from the late 1940s through the early 1980s lasted roughly 30 years before inflation was finally broken by aggressive monetary tightening. Many investors today may be underestimating the possibility that the post-2020 environment represents the beginning of another prolonged inflationary cycle rather than a temporary spike.

Several structural forces support that possibility.

COVID-Era Stimulus Changed the Landscape

The COVID response unleashed one of the largest fiscal and monetary expansions in U.S. history. Congress approved trillions of dollars in stimulus spending, enhanced unemployment benefits, PPP loans, direct checks to households, infrastructure spending, and emergency support programs.

Estimates place total COVID-related fiscal support between roughly $4.5 trillion and $5.6 trillion.

At the same time, the Federal Reserve cut interest rates to near zero in March 2020 and kept them there until March 2022. The Fed’s balance sheet exploded higher as it purchased Treasury bonds and mortgage-backed securities to stabilize financial markets and support economic activity.

Fed Balance Sheet

Source: Bloomberg

While those policies successfully prevented a deep economic collapse, they also injected enormous liquidity into the global financial system.

Now, years later, inflation pressures appear to be evolving from cyclical to structural – and policymakers continue facing pressure to support growing government debt issuance and financial market stability.

Deglobalization and Protectionism Are Inflationary

One of the biggest shifts occurring globally is the reversal of decades of globalization.

For years, corporations optimized efficiency by moving manufacturing to lower-cost regions, building just-in-time inventory systems, and sourcing components globally. That system reduced costs and helped suppress inflation.

Today, countries are increasingly prioritizing supply-chain security over efficiency.

Tariffs, trade restrictions, industrial policy subsidies, export controls, reshoring initiatives, and geopolitical tensions are all contributing to higher structural costs. Companies are building redundant supply chains rather than purely efficient ones. Labor costs are rising as manufacturing returns to developed economies. Protectionism itself acts as a form of inflation because it increases production and distribution costs.

This matters enormously for retirees because inflation compounds over time.

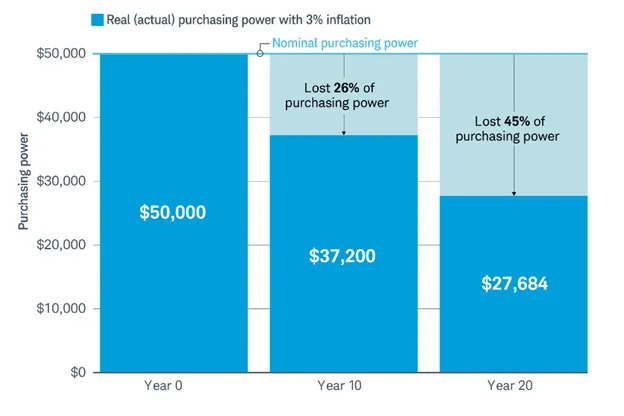

A retiree spending $100,000 annually today may need nearly double that amount in roughly 18 years if inflation averages around 4%. The image below from Schwab shows the loss of purchasing power from just 3% inflation over time.

Source: https://www.schwab.com/how-to-invest/investing-basics

That means retirees still need growth in retirement. Simply preserving account balances is not enough. Purchasing power must also be preserved.

Three Major Inflationary Forces Emerging in 2026

Several real-world developments in 2026 are reinforcing inflation concerns.

1. Energy and Commodity Inflation From the Strait of Hormuz

The ongoing disruptions and closure risks surrounding the Strait of Hormuz have created renewed pressure on global energy markets. Roughly one-fifth of the world’s oil supply moves through this region, making it one of the most important energy chokepoints in the world.

Higher oil prices affect far more than gasoline.

Energy is embedded in transportation, shipping, fertilizer production, plastics, chemicals, industrial manufacturing, and agriculture. Rising energy costs eventually work their way through the broader economy and contribute to higher consumer prices.

2. AI Infrastructure Is Driving Massive Energy Demand

Artificial intelligence is becoming another inflationary force, particularly through energy consumption.

Modern AI chips and hyperscale data centers require enormous amounts of electricity. Utilities across the United States are already seeing surging demand projections as cloud providers and technology companies race to expand AI infrastructure.

Data centers are expected to consume a dramatically larger share of U.S. electricity usage over the coming decade. That increased demand is putting upward pressure on electricity generation, grid investment, natural gas demand, and long-term infrastructure spending.

The AI boom is not only reshaping technology. It is also reshaping energy markets.

3. Memory Prices Are Rising Sharply

Another underappreciated inflationary pressure is occurring inside the semiconductor supply chain itself.

High-bandwidth memory, DRAM, NAND flash, and advanced storage components are experiencing rising demand due to AI servers and accelerated computing systems. As supply tightens and demand surges, memory pricing has risen significantly.

This creates a ripple effect across technology hardware pricing and capital expenditure budgets.

Ironically, this has also created another risk for retirees: concentration risk.

The Hidden Risk of Becoming Too Conservative

Many retirees understandably seek safety after decades of saving and investing. Watching portfolio balances fluctuate during retirement can create anxiety, especially when withdrawals are occurring simultaneously.

But there is a major difference between reducing risk and eliminating growth.

An investor who moves 70% or 80% of their portfolio into bonds and cash at the beginning of a secular inflation cycle could face significant long-term problems. While account values may appear stable, the real value of those dollars may steadily decline.

This is especially true if inflation remains persistently above bond yields.

Fixed-income investments perform best during falling inflation and declining interest rates. But during inflationary environments, long-duration bonds can struggle badly because rising rates reduce bond prices while inflation simultaneously erodes purchasing power.

Retirees who become excessively conservative may unintentionally create another form of risk: longevity risk. The risk that their portfolio no longer grows fast enough to sustain future spending needs.

At the same time, retirees must balance inflation risk against sequence-of-returns risk, where large market declines early in retirement can permanently impair long-term portfolio sustainability if withdrawals occur during periods of volatility.

For retirees today, the challenge is balancing stability with inflation protection.

The Danger of Chasing What Is Hot

In today’s market, AI infrastructure and memory-related stocks have become some of the market’s strongest-performing investments. Semiconductor and memory companies are attracting enormous investor enthusiasm as AI spending accelerates globally.

But retirees need to be careful not to become overly concentrated in the hottest areas of the market simply because they are outperforming.

At times, it can feel like the AI and memory trade is sucking the oxygen out of every other investment category. Momentum can become intoxicating. Investors begin believing only one theme matters.

History suggests otherwise.

Every market cycle eventually rotates leadership. Even transformative technologies experience periods of excessive valuation, volatility, and mean reversion.

Retirees should avoid confusing a strong investment theme with the need for portfolio concentration.

The goal in retirement is not maximizing upside at all costs. The goal is building sustainable long-term financial resilience.

Diversification Is Still the Best Defense

One of the most effective ways retirees can manage inflation and uncertainty is through diversification across asset classes with different economic sensitivities.

Because different investments respond differently to inflation, recessions, rising rates, economic growth, and geopolitical shocks, diversification is one strategy which may help mitigate risk across market environments – though results will vary.

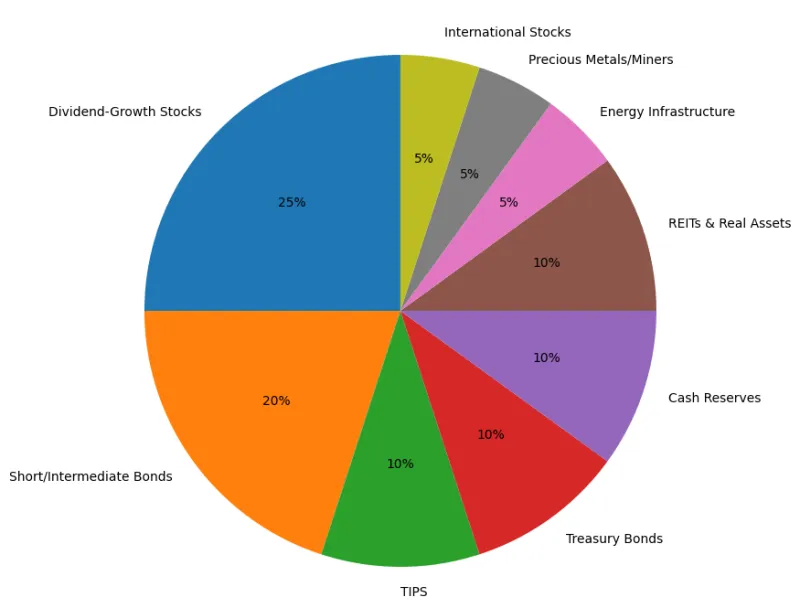

A balanced retirement portfolio may include:

Blue-chip dividend-growing stocks

Short- and intermediate-term bonds

Treasury Inflation-Protected Securities (TIPS)

Floating-rate bonds

Cash reserves

Real assets and infrastructure exposure

Precious metals or precious metal miners

International diversification

No single investment solves every economic environment perfectly. The objective is creating balance rather than relying entirely on one outcome. The goal is not maximizing returns through concentration, but creating a diversified allocation capable of generating income, participating in long-term growth, and helping preserve purchasing power during inflationary environments.

Illustrative Conservative Allocation

Actual portfolio allocations will vary based on client risk tolerance, goals and timeframe.

Dividend Growth Stocks Can Help Offset Inflation

I believe one particularly important strategy for retirees during inflationary periods is owning high-quality companies with long histories of increasing dividends.

Unlike fixed-income investments that pay static coupons, dividend-growing companies may raise their payouts over time as revenues and earnings increase.

Businesses with strong balance sheets, pricing power, durable cash flow, and recession resilience can help retirees maintain income growth even as living costs rise.

This becomes especially valuable in a higher-inflation world because rising dividends may partially offset the declining purchasing power caused by inflation.

Blue-chip dividend growers also provide exposure to productive assets rather than idle capital sitting in cash.

Smarter Bond Positioning for Inflation

This does not mean retirees should abandon bonds altogether. Bonds still play an important role in portfolio stability and income generation.

But bond construction matters far more during inflationary periods.

Laddered Bond Portfolios

A bond ladder spreads maturities across multiple years rather than concentrating all holdings into long-duration bonds. As bonds mature, proceeds can be reinvested at prevailing interest rates.

This helps reduce interest-rate risk while improving flexibility during rising-rate environments.

Floating-Rate Bonds

Floating-rate bonds adjust coupon payments based on prevailing short-term interest rates. As rates rise, income payments rise as well.

This can help reduce the damage inflation and rising rates inflict on traditional fixed-rate bonds.

Treasury Inflation-Protected Securities (TIPS)

TIPS are specifically designed to help protect purchasing power. Their principal value adjusts with inflation, helping investors maintain real value over time.

While TIPS are not perfect and can still fluctuate in price, they may provide an important hedge during persistent inflationary periods.

Precious Metals Still Have a Role

Precious metals can still serve an important role in diversified retirement portfolios, particularly during periods of geopolitical instability, currency debasement concerns, or inflation shocks.

But retirees should avoid overconcentration.

Physical gold itself does not generate income, dividends, or cash flow. For retirees needing income, precious metal mining companies may offer an alternative because many miners generate free cash flow and pay dividends while still benefiting from higher gold prices.

Again, balance matters more than extremes.

Tax Diversification Matters in Retirement

Many conservative retirees rely too heavily on bond interest for retirement income without realizing that most bond income is taxed as ordinary income at both the federal and state level. While Treasury bond interest is exempt from state income taxes, it is still taxable federally, and municipal bond interest may still be subject to state taxes if the bonds are issued outside the investor’s home state.

In contrast, qualified dividends from many blue-chip stocks receive preferential tax treatment and are generally taxed at 0%, 15%, or 20% federally depending on income levels, which can create a significantly better after-tax outcome for many investors.

Diversifying retirement income sources can improve both tax efficiency and inflation protection. Rather than relying too heavily on taxable bond income, retirees may benefit from combining income streams with different tax treatments and inflation sensitivities, including:

Qualified dividend-paying stocks, which may receive favorable federal tax rates of 0%, 15%, or 20%

Treasury bonds, which are exempt from state income tax

Municipal bonds, which may be exempt from federal and state taxes

TIPS and floating-rate bonds that may adjust better to rising inflation and rates

Dividend-growing blue-chip stocks with pricing power

Rental income and REITs that may benefit from rising property values and rents

Mid-stream pipeline and energy infrastructure income

Social Security benefits with cost-of-living adjustments (COLAs)

Annuities with inflation-adjustment riders

Roth IRA withdrawals for tax-free income flexibility

By diversifying income sources, retirees may improve after-tax cash flow, reduce concentration risk, and better preserve purchasing power during inflationary periods.

This approach not only improves flexibility for managing taxes and retirement cash flow, but also helps protect purchasing power during inflationary periods. Dividend-growing companies, for example, may increase payouts over time, while fixed bond payments remain static. The goal is not avoiding bonds altogether, but creating diversified income streams that balance stability, tax efficiency, and long-term inflation protection.

Diversification Means More Than Simply Owning Many Investments

One of the biggest misconceptions in retirement investing is that diversification simply means owning a large number of positions. In reality, true diversification comes from owning asset classes that behave differently from one another across varying economic environments.

A portfolio holding 30 technology stocks may appear diversified on the surface, but if all 30 positions are highly correlated and respond similarly to rising interest rates, economic slowdowns, or valuation compression, the portfolio may still carry significant concentration risk. The same applies to retirees who own multiple bond funds that all have similar duration exposure or multiple precious metal holdings that rise and fall together.

Effective diversification focuses on combining investments with lower correlations to one another. Correlation measures how similarly assets move over time. Assets with high positive correlations tend to move together, while assets with lower or even negative correlations can help offset volatility during difficult market periods.

For example, dividend-paying blue-chip stocks, short-duration bonds, TIPS, floating-rate bonds, precious metals, infrastructure investments, utilities, energy exposure, cash reserves, and select international holdings may all respond differently to inflation, recessions, geopolitical events, and interest-rate changes. By blending multiple asset classes together, retirees may improve portfolio stability without relying entirely on one investment theme or economic outcome.

This is where professional portfolio analytics can become extremely valuable. A financial advisor using modern portfolio analysis tools can evaluate not just performance, but also how investments interact with one another inside the portfolio. Advisors can review metrics such as standard deviation, correlation coefficients, drawdown history, income generation, concentration exposure, and overall risk-adjusted returns.

In many cases, retirees unknowingly take more risk than they realize because their investments are overly concentrated in assets driven by the same economic forces. A portfolio may appear diversified simply because it contains multiple mutual funds or ETFs, while still remaining heavily exposed to rising interest rates, inflation shocks, equity market corrections, or specific sectors such as technology. For example, an investor may own five different large-cap mutual funds, yet all five funds could have significant overlap, with 30–40% of each fund concentrated in the same handful of mega-cap technology stocks. Layering multiple funds together can create the illusion of diversification when, in reality, the portfolio may still be highly concentrated in a narrow group of industries or market themes.

Through portfolio analysis and rebalancing, an advisor can help reorganize investments to improve efficiency — seeking to reduce unnecessary volatility while still maintaining sufficient growth and income potential. The goal is not necessarily maximizing raw returns, but improving risk-adjusted returns over time by building a portfolio designed to better withstand multiple market environments.

For retirees especially, diversification should not be viewed as a defensive compromise. It should be viewed as a strategic framework for balancing growth, income, inflation protection, and long-term financial sustainability.

Conclusion: The New Retirement Reality

The retirement environment ahead may look very different from the one retirees experienced over the past 40 years.

The combination of higher fiscal spending, deglobalization, protectionism, energy insecurity, AI-driven electricity demand, supply-chain restructuring, and geopolitical instability may create a structurally more inflationary world than many investors became accustomed to between 1980 and 2020.

That means retirees may need to rethink what “safe” investing actually means.

Too much conservatism can become dangerous.

The greatest risk for many retirees may not be short-term volatility, but the long-term erosion of purchasing power.

Too much concentration can also become dangerous.

The most resilient retirement portfolios will likely be those that maintain diversification, preserve flexibility, generate growing income streams, and continue participating in long-term economic growth while still managing downside risk.

Retirement investing is no longer simply about avoiding volatility. It is about preserving purchasing power in a changing world.

Comments

Log in or sign up to join the conversation.