This week is the final recap of the 2026 Strategic Investment Conference. I have always done summaries of the SIC afterwards, but I don’t think I’ve ever taken four weeks, let alone five weeks to cover it. And I feel we have only scratched the surface. There was just a lot of good content this year. And so much has happened since early May.

The three-week war in Iran is now 3.5 months, and there is zero consensus among people that I pay attention to as to when it will end. The Strait of Hormuz has been closed for weeks. As noted last week, Treasuries now come with an asterisk. China is building production capacity designed to permanently close the door on Western industry in thirty critical sectors. And the S&P 500 is up 17% in four weeks. If you find that paradoxical, you are paying attention. If you find it reassuring, you have not been paying attention. If you find it instructive, welcome to the world Ed Yardeni described at SIC.

Despite everything we have seen in the economic data, which can be confusing, the US consumer has refused to crack. My friend Dr. Ed Yardeni, whom I have known since '98, has the most compelling explanation I have heard for why. He came to SIC Day 4 with an upgraded S&P 500 target, a bullish earnings case, and an explanation for one of the most confounding data puzzles of the current cycle. He has been right more often than not over those decades, which is why I pay attention when he speaks. (For the record, he has been bullish for the entire last 15 years, and expects the bull market to continue through the rest of the decade. He has been more than right over that timeframe.) But on the consumer, here is the puzzle he laid out, and it is one I have been turning over myself:

In April alone, disposable personal income fell while consumer spending rose. The bears say that cannot last. Ed says they are measuring the wrong thing. Every permabear in the business has been pointing at that gap for two years and calling it a ticking clock. Yet Ed's answer is it is not a gap. To him, it is the G-shaped economy.

The G-Shaped Economy

The G stands for generational. Baby boomers, collectively sitting on $89 trillion in net worth (that is not a typo) are retiring in historic numbers. (Research shows that humans simply don’t understand the difference between a million, billion and trillion. There is an excellent Wall Street Journal piece on that.)

In 2025 alone, 1.85 million additional retired workers filed for Social Security for the first time. As they leave the workforce, they stop earning paychecks. That drags disposable income lower and depresses average hourly earnings. So, the income data looks weak. But consumption stays strong.

Ed explains it this way:

"What I see when I look around with the baby boomers is I see all my friends retiring... The boomers are doing absolutely great. If they're still working, they're making a lot of money in salaries. If they're retiring, they've got $89 trillion of net worth collectively. As they retire, guess what? They're not getting the paycheck anymore."

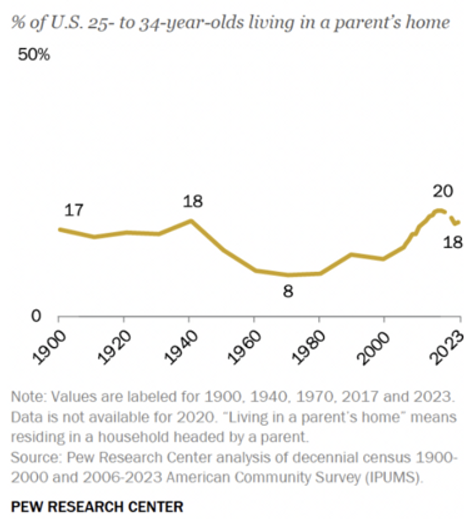

Nearly one in five adults ages 25 to 34 are living in a parent's home today, a number that bottomed at 8% in 1980 and has more than doubled since. We are back to levels not seen since before World War II. Not necessarily because they want to be there. In many cases, because they cannot afford not to be. An affordability crisis has squeezed younger generations, and the boomers are quietly filling the gap supporting their adult children. Helping with the grandchildren. Drawing down the $89 trillion.

Source: Pew Research Center

"How could consumption possibly exceed disposable income? Well, there's $89 trillion of net worth and all these kids who are facing an affordability crisis... It's not a good thing. I don't like seeing it. It would be much better if we didn't have an affordability crisis, but the way we're getting through it is I think the boomers are helping their kids."

Think about what that means in practice. When your 28-year-old is living rent-free and you are covering their bills, that money does not disappear. It flows straight into consumption. The boomer's balance sheet becomes the younger generation's spending power.

This is not a consumption bubble. It is an intergenerational wealth transfer that standard economic models miss because they measure income, not assets. The K-shaped economy that everyone describes is real but incomplete. The G-shaped economy explains why the consumer keeps surprising to the upside even as the income data looks grim. The bears have been right about the income numbers for two years. They have been wrong about the conclusion.

Ed is right. This is a natural outcome of the baby boom and the extraordinary economic times we’ve been privileged to live in. It’s not just that baby boomers are retiring. When they actually do retire, their income goes away and obviously is not in the BLS statistics on income. That is not a bad outcome as it is precisely what the boomers have planned. They saved, paid into Social Security and pensions, and now they are living on whatever wealth they accumulate.

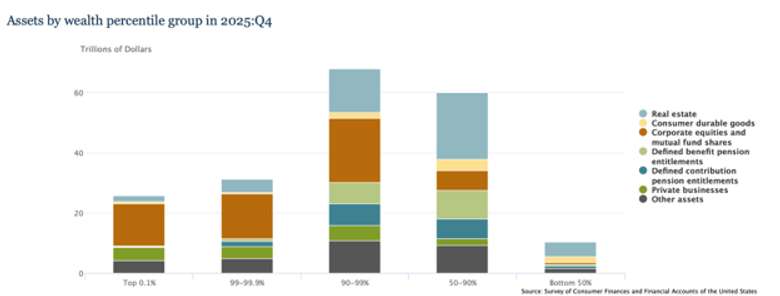

However, the wealth doing the work of keeping consumer spending up is not evenly distributed. It sits overwhelmingly with older Americans who spent four decades benefiting from rising home prices, rising stock prices, and falling interest rates. The bottom 50% of Americans hold almost nothing by comparison. That gap may be the single most important reason the consumer has remained stronger than the income data suggests.

The bottom 50% of Americans hold roughly $9 trillion in assets. The top 10% hold well over $100 trillion. That is a canyon sized gap.

Source: Board of Governors of the Federal Reserve System

The gap is real. But it is not permanent. Boomers are not immortal. A portfolio is not a paycheck. When the wealth transfer slows, as it eventually must, the consumption engine that has been confounding the bears for two years loses its fuel. Ed is not saying the consumer is permanently fine. He is saying the consumer is fine for longer than the income data suggests.

Ed also noted something important about earnings breadth. More than 85% of S&P 500 companies are currently seeing forward earnings rise on a year-over-year basis. The market has broadened significantly, and earnings are on track for 23 to 24% growth this year, a number you usually only see coming out of a recession. That kind of breadth, sustained through a hot war and a closed strait, is either a sign of remarkable resilience or a market that has simply stopped paying attention to risk. Ed thinks the former.

SpaceX

I hope he is right. But there is a caveat. Unless you are living under a rock, you are aware that SpaceX went public yesterday, and Anthropic and OpenAI will shortly follow at trillion-dollar valuations. From Friday’s Dividend Cafe, courtesy of David Bahnsen (edited):

“S&P 500 index investors, or just people who own most of the mega-cap, Mag-7, big tech names, there is pretty much exposure to a lot of this IPO mania whether you like it or not, and whether the indexes you own include them or not. Not only do names like Nvidia, Meta, Microsoft, Google, and Amazon all have massive cap table positions in a bunch of these mega AI names, but it turns out an unfathomable amount of the "earnings growth" of the index last quarter was just these companies marking up the value of these private AI names that they own. $69.2 billion of "profits" were "other income" from just THREE companies (Google, Nvidia, Amazon). This accounts for a staggering 12% earnings growth year-over-year, making the "operating earnings" growth far, far more understandable (though still quite robust, it should be said).”

Sidebar: David Bahnsen wrote about the SpaceX IPO this week from the perspective of having been an early investor with some of his clients in a private vehicle. Would he sell the day? What should you do? You can find out at this Dividend Cafe. If you are not subscribing to Dividend Cafe you should be.

(Sidebar: My personal thoughts on SpaceX? I am a huge fan but will likely not buy any shares for my retirement accounts. [Full disclosure: I have a private investment in a different startup space company.] Except, what I think I will do a year from now is create a small “trust fund” for my grandkids where they get some amount of SpaceX which they can’t touch for 20 years. More than just transferring a little wealth, it will have them looking at markets and dreaming and maybe about accumulating stocks on their own. And learning that investing is a long-term game and not some trading vehicle.)

Final Panel

The final panel at SIC covered a lot of ground. Tyler Cowen’s core argument was straightforward: if AI delivers even modest productivity gains, many of the fiscal and demographic problems that dominate today's headlines become manageable rather than catastrophic. Not solved. Manageable. He said 2.5% growth, not utopian, just modestly better than recent trends, could let the United States squeeze through its debt problem without a crisis.

However, I am less certain. David Bahnsen and I wrestled with the Japanification scenario (something we’ve been doing in our private conversations for a very long time), whether excessive debt simply suppresses growth indefinitely without triggering the apocalypse the bears have been predicting. Japan has been running at 200%+ debt to GDP for decades. Everything works. Nothing grows. (Sound familiar?) Is that our future? Tyler thinks American innovation and immigration make us categorically different from Japan. I actually agree with this point, but the timing is the issue. Our best companies are genuinely extraordinary. Our capital markets have no peer. And we continue to attract the world's most ambitious people in ways that Japan simply cannot.

David made the distinction more precisely than I could. America has managed roughly 1.8% real growth since the financial crisis, barely over half our historical average, but still dramatically better than Japan's near zero. The reason, he argued, is exactly what Tyler said, better companies, a better banking system, and an economy that continues to attract the world's best immigrants. Those competitive advantages are real. But at the same time, they are also not guaranteed to persist indefinitely under a debt load that keeps rising.

I think he may well be right. Debt is future consumption brought forward. If that debt was used to pay Social Security, Medicare and other government expenditures, it is still being borrowed from the future. Over time, the portion of expenditures that are debt keep increasing to what we suspect will be untenable, without creating inflation. Japan’s demographic structure is deeply deflationary. It is not unreasonable to think that Japan might need a loose monetary policy to overcome that deflationary bias. And as we all know the Japanese GDP has been flat or negative for the last 20 years, they have also seen their per capita GDP grow. Are they the template for future low population growth countries, or are they the exception? For what it’s worth, as long as the US still has people wanting to emigrate, we will not be a low population growth country ever. Unless we choose to be which would be simply irrational, at least from an economic standpoint.

David Bahnsen closed the final panel with the cleanest investment answer to a messy conversation. AI may lift growth, debt may suppress it, Washington may drift, geopolitics may shock supply chains, and the obvious themes may still be terrible investments if the risk-reward is wrong.

"Disruption is inevitable. It is the norm. We've been living in disruption for the entirety of all of our lives, regardless of what generation we're in. And disruption will continue to be the case, but my belief is that investment results largely do not come from betting right on what disruptions come and when and to what margin and what companies. Investment success comes from aligning your portfolio with the right set of risk-reward trade-offs."

And then:

"I strongly recommend people invest within what they can and do know and not what they can't and don't know. And unfortunately, this is a lesson that many people have to learn the hard way."

On sectors, the panel was more specific than most final panel investment conversations tend to be. Energy emerged repeatedly throughout the discussion (and the conference!), as a hedge against geopolitical disruption, as a beneficiary of AI infrastructure demand, and as one of the few sectors where valuation still appears attractive. Biotech and longevity were where I personally have conviction.

We are closer than most people realize to therapies that could dramatically extend both health span and longevity. At the time of this writing, four people have had their Parkinson's disease completely reversed through a single therapy, at a cost of over a million dollars per treatment. (The cost will come down. It always does. There is research that suggests the price could drop by more than 90%.) And when it does, the demand for what comes next will be unlike anything the healthcare system has ever seen.

Mining and rare earths came up as a theme everyone agreed was directionally correct and practically difficult. The gap between identifying the opportunity and finding the right company to own it is wide. And mining is a long-term process.

Bruce Mehlman added the structural context for why Washington will not be providing clear policy direction anytime soon. Change in Washington requires one of three things: a crisis, a movement, or persistent incremental evolution.

"Often, policymakers ignore things until something breaks... Number two are movements... Finally, there's what happens more often than not, which is people see a problem and they make incremental improvements over time."

What I took away from the final panel is that nothing is going to change without a crisis in any significant way. There is just too damn much inertia and you’ve got two disparate sides that are becoming increasingly hostile. I stand by that. The crisis I believe is coming will eventually manifest in the bond market. Not this year. Possibly not next year. But the arithmetic is the arithmetic. Tyler may be right that AI saves us from the worst of it. Bahnsen may be right that we Japanify rather than collapse. Mehlman may be right that change comes more slowly than either the optimists or pessimists expect.

But if none of us knows exactly how this resolves, the more useful question is how we navigate through it. David Bahnsen gave the clearest answer I heard at the entire conference: identifying the disruption and identifying the winners are not the same exercise. A Wall Street Journal column that landed in my inbox this week illustrates exactly why.

Sidebar: The Global Crossing Lesson

A friend sent me a column from the Wall Street Journal this week by Andy Kessler. The timing could not be more relevant. We are about to see three of the largest IPOs in the history of the capital markets arrive within months of each other.

In 1997, Global Crossing laid undersea fiber optic cable and projected enormous revenues based on prevailing T-1 line pricing. The spreadsheets flashed green. The stock hit $55 billion in market value. Then AT&T and MCI laid their own cables, prices dropped more than 90%, and Global Crossing went bankrupt. (The CEO paid $60 million for a home in Bel Air. Heady times.)

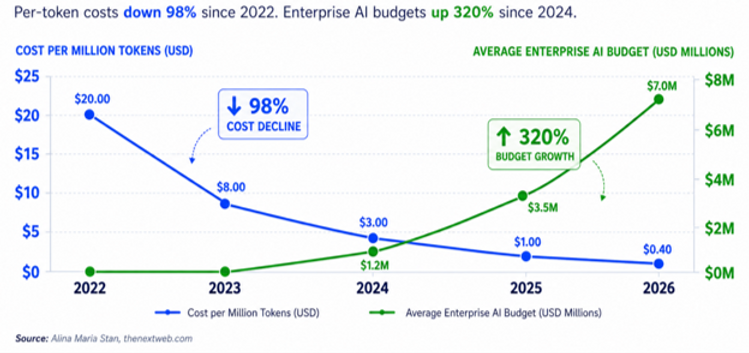

Kessler's point: AI token prices have already dropped 90% since ChatGPT launched. They will likely drop another 90%, possibly 99%, over the next five years. DeepSeek recently cut prices on its open-source model by 75%. Running certain benchmarks, OpenAI costs 12 times as much as DeepSeek. Anthropic costs 19 times as much.

And yet, even as token prices collapsed 98%, enterprise AI bills are up 320%.

Source: Alina Maria Stan

Uber blew through its entire 2026 AI coding budget by April. Microsoft revoked its developers' Claude Code licenses six months after enabling them. One company ran up a $500 million bill in a single month. Prices are falling. Consumption is exploding. The bills are going up anyway.

The internet happened. The demand was absolutely real. Global Crossing went bankrupt anyway. Getting the theme right and making money on the theme are two different things. People made multi-generational riches and went broke on the exact same internet thesis. Just saying.

With that caveat, the overall theme of the conference was surprisingly positive. As I’ve noted in previous letters, there were some serious negatives, but the general advice was to stay conservative and diversified, and be focused on specifics and not broad-based indexes in your own personal portfolios.

Comments

Log in or sign up to join the conversation.