Last week I noted the problems of sitting down with a blank screen and trying to figure out what to write. This week I have the opposite problem: I have well over 20 important research notes from various authorities about inflation, Federal Reserve policy, and interest rates. The challenge will be to summarize the most important points.

I think that we’re at the beginning of what might be called a “regime change.” We are moving from a world where disinflation was one of the primary drivers of economic policy to where the environment is biased towards inflation. Volcker began the lower-inflation and then disinflationary impulse, but globalization in particular and a number of forces in general made the inflationary environment benign. That is changing. Kevin Warsh inherits a completely different environment than any previous Fed chair, at least since Volcker. This week we had CPI, PPI and other corroborating data to lend credence to this thesis.

I’ve been writing about inflation more in recent months and quarters because inflation has become the major driver of the US macroeconomic landscape. I get that technology, AI, robotics, housing, labor and employment and a host of factors are all important. But inflation, at least in my mind, is the main factor that we should pay attention to. Rising inflation means rising interest rates, a more difficult housing and labor environment, problems for capital formation which we need for technology and other investments, and clear impacts on consumers and consumer spending.

This week, we take a deep dive into inflation and interest rates and at the end I talk about why I am buying gold for my grandkids.

CPI Head Fake?

After a .5% rise in headline CPI in May, it fell by .4% in June which was more than the anticipated drop of one tenth. The core rate too was under the estimate with no m/o/m change vs the estimate of up .2%. Versus last year, prices rose 3.5% headline and 2.6% core vs 4.2% and 2.9% respectively in May. Almost all the difference was in energy prices. That’s fine, except that energy prices have begun to rise again which will more or less erase that lower number next month. As I noted last week, energy markets responded well to the supply shock, but we are running through reserves and short-term adjustments rapidly. Notice below that the price of oil is back up to where it was 30 days ago.

Source: Oil Price Charts | Oilprice.com

From Peter Boockvar’s Substack:

"After the large run higher in the prior months, energy prices fell back by 5.7% in the month, though still up 15.7% y/o/y with gasoline prices in particular up by 27% y/o/y. Food prices grew by .2% m/o/m and 3% y/o/y. ‘Food at home’ prices were up by .2% m/o/m and 2.7% y/o/y. ‘Food away from home’ saw prices up .2% m/o/m and 3.4% y/o/y.

"Keeping a lid on the core rate was no change in services inflation ex energy m/o/m, though still up 3.2% y/o/y. Owners Equivalent Rent cooled a touch to a .2% rise m/o/m and by 3.3% y/o/y. ‘Rent of Primary Residence’ was up .1% m/o/m and 2.8% y/o/y, getting closer to reality. Medical care costs fell one tenth m/o/m and up just 2% y/o/y which is not close to the reality on the ground, particularly with health insurance. Explain this to me: health insurance costs fell 7.4% y/o/y and by .5% m/o/m. It’s because the BLS is measuring profit margins of health insurers rather than what policies are actually being priced at. Airline fares were little changed, up by .2% m/o/m, but after a big jump in the prior months. They are up 26.5% y/o/y. It’s still expensive to fix a car with ‘maintenance’ prices up by 1.1% in the month and by 7% y/o/y."

OER is starting to come down, which it should. OER has a significant lag effect on both the upside and downside. Rents and leases are decreasing and will eventually show up in the CPI.

That being said, the inflation environment is under pressure. Inflation in services is still the primary driver of overall inflation.

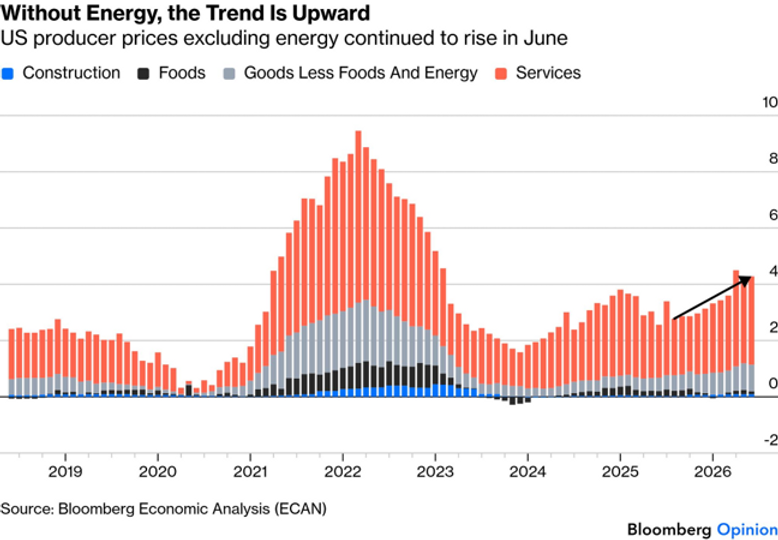

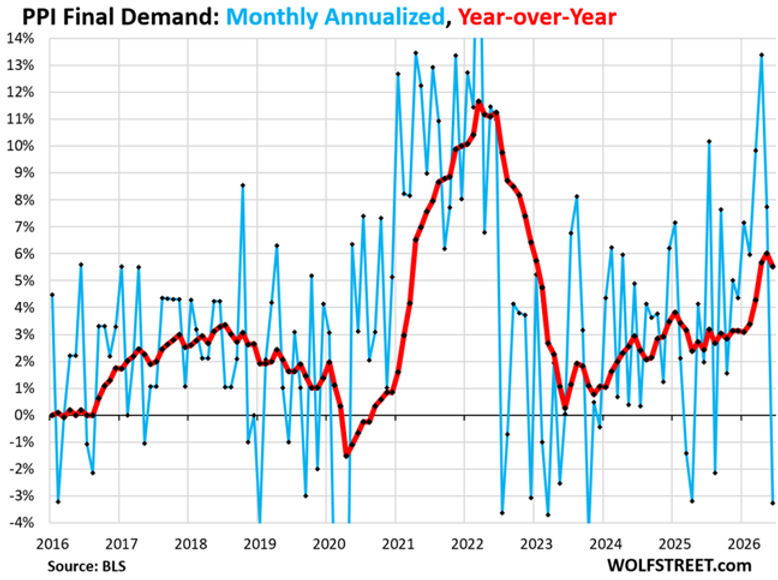

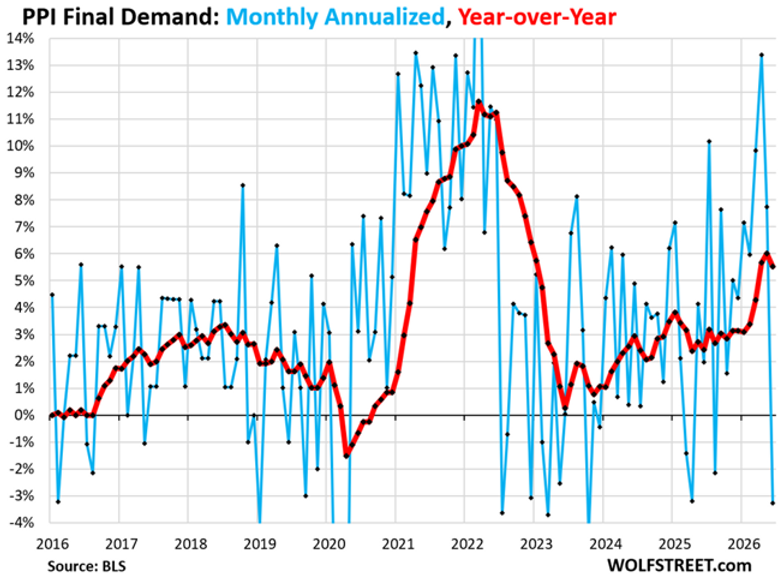

Pipeline Inflation

This week we also saw the Producer Price Inflation, which ex-energy was still high. From Wolf Richter:

“Year-over-year, the PPI rose by 5.5%, still a lot of inflation, but lower than the multi-year high in May (red). It has been zigzagging higher ever since the low point in mid-2023.”

Beyond the plunge in energy, producer-price inflation accelerated in June from May and year-over-year because inflation in services accelerated. Year-over-year, the services PPI accelerated to 4.6% (red line). That’s a lot of inflation in services. It has been zigzagging higher since the December 2023 low.

It gets complicated, but core goods in the PPI and CPI both saw increases in the 2% range, and without trying to be controversial, tariffs added at least 1% to the overall CPI. It is just arithmetic, not a political statement. Notwithstanding the tariff rebates, the tariffs have been enacted which basically continue to boost prices. This is not an argument against tariffs, although I could make one in a separate letter, but it gives an acknowledgment of their effects.

The End of Globalization’s Disinflationary Era

I wrote last month about Lacy Hunt’s truly remarkable (at least to me) change in his view on inflation and interest rates that he did in his presentation at the Strategic Investment Conference. He has been a bond bull since 1982 and has one of the best-performing bonds since that time under his management. He is now arguing that we are in a higher overall inflationary environment and that interest rates on the long end will likely rise.

Lacy Hunt has been essential reading for me on the plumbing of inflation and interest rates for decades, and their Q2 letter, “Capital Scarcity and the End of Globalization’s Disinflationary Era,” deserves your full attention.

He has now written in detail about that major shift in his thinking in his latest quarterly update that I think you should read at least once, if not three or four times. It took me a while to absorb. I’m going to try to give you a summary:

Their thesis is blunt: the disinflationary machine that ran from 1990 to 2020 is breaking down. They write that the “long run equilibrium range” for inflation “is migrating from roughly 1.5–3.5% toward 3.5–4.5%, with a significant risk of episodes of inflation above 5%.” Let that sink in.

What powered three decades of low inflation? Cheap global labor, integrated supply chains, and falling capital costs pushed the aggregate supply curve outward. Debt could expand without triggering inflation because money velocity kept falling — M2 velocity dropped from 2.2 in 1997 to just 1.1 during the pandemic — and that dormant liquidity, paired with expanding global capacity, absorbed everything the Fed threw at the system.

That machine is now in reverse. Tariffs, friendshoring, and the shift from “just-in-time” to “just-in-case” production are, in their words, “structurally raises costs across manufacturing, logistics, and inventory management.” Labor is turning scarce rather than abundant, and since service-sector inflation is fundamentally wage-driven, that scarcity flows straight into prices.

Then there’s the capital problem. Net national saving has collapsed from a 6.8% historical average to near zero, just as AI, the power grid, and reindustrialization demand enormous investment. Something has to give: foreign financing, higher real rates, or crowded-out investment.

And the Fed in the past did not help. I still maintain that Jerome Powell was the worst Fed chair since Arthur Burns. He created this inflation surge.

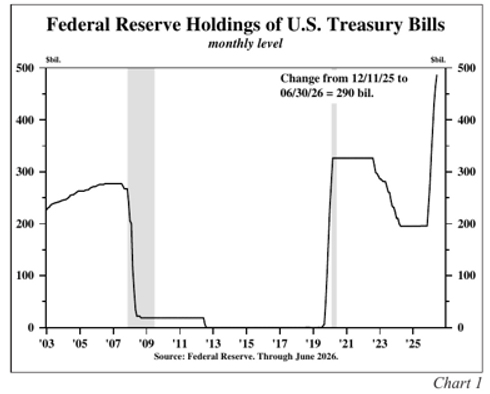

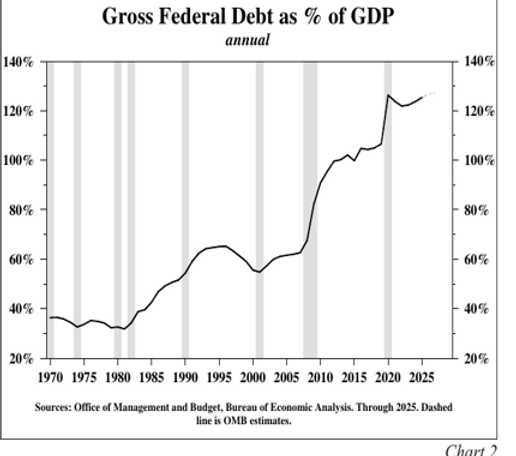

New Chairman Kevin Warsh inherited a $290 billion Treasury-bill buying spree (Chart 1) that reignited deposit and loan growth — ODL grew at an 8.9% annualized rate, well above its 5.7% ten-year trend.

(Important Sidebar: “ODL” represents funds held by banks that are not demand deposits or time deposits. These liabilities can include things like savings deposits, certificates of deposit, and other types of accounts. When banks hold these types of deposits, they have more funds available for lending and investment activities. This is because of the impact of ODL on the velocity of money in an economy. And Powell juiced it.)

Meanwhile, gross federal debt is closing in on 125% of GDP (Chart 2), which brings to mind Niall Ferguson’s Law: great powers decline once debt-service costs exceed military spending.

Lacy’s bottom line: absent a recession or genuine monetary restraint, both inflation and long bond yields trend higher — just less smoothly than markets are used to. I wouldn’t bet against them.

Labor Market Inflation

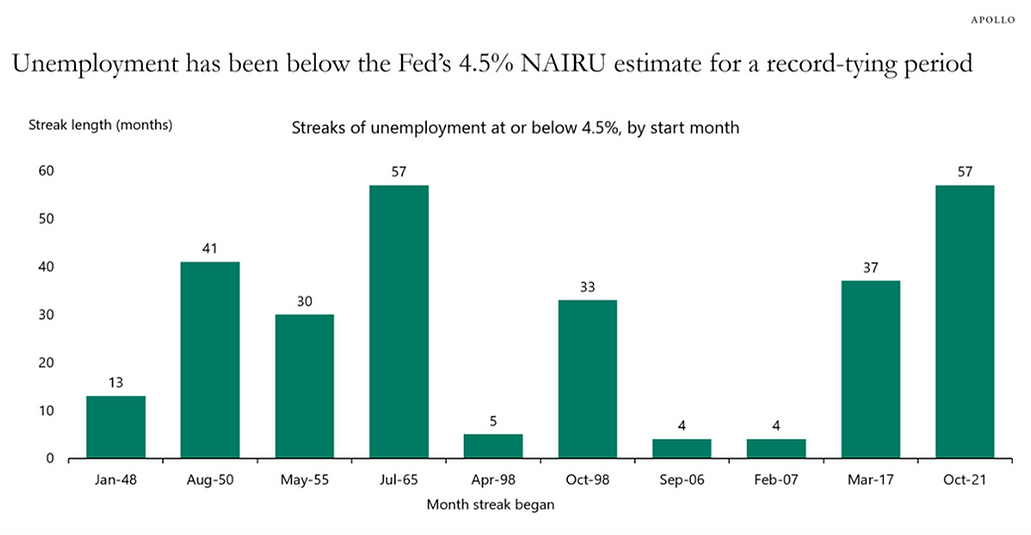

Torsten Slok, the chief economist at Apollo (and a favorite read) argues that the labor market explains why inflation won’t go away.

“With the Fed estimating the non-accelerating inflation rate of unemployment (NAIRU) at below 4.5%, and unemployment having stayed at or below that level for 57 months, tied for the longest such streak on record, the labor market has been operating in excess-demand territory for an unusually long time. That persistent tightness is a key reason inflation has remained elevated: when unemployment runs below NAIRU, wages and prices face sustained upward pressure.

“The chart below puts this streak in historical context. Prior episodes of sub-4.5% unemployment were typically far shorter. The current one is one of the longest on record, which helps explain why the ongoing inflation overshoot since 2021 has been so stubborn.

“The bottom line is that a strong economy is the reason why inflation has been high, and only by keeping rates higher for longer can the Fed cool inflation down towards the FOMC’s 2% inflation target.”

Sources: US Bureau of Labor Statistics, Apollo Chief Economist The Daily Spark | Macro and Market Insights | Apollo Global Management

Is AI Inflationary or Deflationary?

The short, but not necessarily helpful, answer is yes. But the real answer depends on your timeframe.

Ed Yardeni has hit on one of 2026’s more interesting monetary puzzles, and it’s worth unpacking. Summarizing his weekly long essay:

When Kevin Warsh sat for his confirmation hearing, he sold senators — and markets — on a dovish story: AI would be “structurally disinflationary,” much like the internet was, freeing the Fed to cut rates. Six months later, that story has flipped completely. AI did not turn out to be the Fed’s excuse to ease. It became the reason to stay hawkish.

The June FOMC minutes tell the tale. Officials pinned part of the inflation pickup on “the surge in demand related to the AI buildout,” with core-goods inflation partly reflecting “AI-related price pressures” and “ongoing strong demand for AI infrastructure” keeping upward pressure on technology and electricity prices. The trouble is timing: productivity gains are expected to “lag the ongoing boost of AI adoption on demand,” so the disinflationary payoff “would likely take time to materialize.”

New York Fed President John Williams put it plainly: AI-driven demand is now his “primary inflation concern,” and if it keeps inflation above his baseline, “monetary policy would need to respond.” Governor Michael Barr thinks AI will push up the neutral rate and is “unlikely to be a reason for lowering policy rates.” St. Louis Fed’s Musalem is the most hawkish of the bunch, arguing the Fed should “lean against demand and inflation pressures today” rather than wait on productivity gains that haven’t shown up yet.

Yardeni agrees with the hawks, for now. Computer-software CPI jumped 14.5% year-over-year in May, the fastest since that series began in 1977. Electronic-component PPI is up 26.9%. Electricity inflation hit 5.9%. Meanwhile the AI buildout is soaking up capital just as Baby Boomer retirements and tighter immigration shrink the pool of savings — exactly the recipe for a higher neutral rate.

But here’s their real thesis, and it’s the more interesting one: this is a sequencing problem, not a permanent one. Once AI adoption widens, productivity growth should turn disinflationary — and it’s already bending unit labor costs lower, up just 0.5% year-over-year in the first quarter, the slowest pace since 2019.

Kevin Warsh on Inflation

Kevin Warsh had his first Humphrey Hawkins presentation to the Senate this week, and we need to cover a few highlights. (H/T to Rene Aninao)

In his prepared testimony, he said this of note, “The members of our committee have no tolerance for persistently elevated inflation. And we share a resolute commitment to restoring price stability.”

"If we get policy right — and we will — the inflation surge of the last five years will be a thing of the past." (As Peter noted, the level of government spending is a key factor in inflation, and with a budget deficit at 5.6% of GDP, it makes it tough to get back to 2% sustainably.)

The Chairman then stated he was “doubling down” on the 2% inflation target — a general concept he’s been publicly critical of in the past — and here it’s worth reminding market participants that the Federal Reserve targets “the annual change in PCE” [read: headline, not “3mo super core” or any of these other silly dovish “cherry-picked” metrics]

Though maybe most stunningly and most importantly, the Chairman stated that “unfortunately, after 63 months of prices above target,” it is “our job and my commitment to take sticky prices and un-stick them” [see exchange here].

To add to the list of Federal Reserve governors and presidents who are commenting on inflation mentioned above by Yardeni, Federal Reserve governor Chris Waller said in his speech this week, “Sternly staring at inflation until it melts before our withering gaze is not an option.” More and more of the Fed members are turning hawkish. If and when Warsh wants to raise rates, I believe he will have the backing of the majority of the members.

Taken in total, we are in an environment where interest rates are going to be higher than many would like. Warsh sees his job as getting inflation back below 2%. For all the reasons above, this will be more difficult than it was in the past. That means that rates will be higher for longer and that it will take more hard work to bring inflation down.

The market is pricing in a ~90% probability that there will be at least one rate hike by the end of the year. I am having a running conversation with friends who are knowledgeable on both the policy front and on Kevin Warsh’s views. My belief is that raising rates in front of the midterm election is just not proper Federal Reserve etiquette. But there is reason to believe that the Chairman is more focused on containing inflation than being “proper.” While I don’t think (and the market basically agrees) there will be a rate hike at the July Fed meeting, if we get hot inflation numbers in August and September, he may elect to move in October before the December meeting.

In any event, I think market participants will eventually come to understand, if they don’t already, that Chairman Warsh is completely independent of the Trump administration. He is a fierce proponent of Federal Reserve independence.

Yes, I get the problems of higher interest rates on the housing market in particular and other side effects in general. But if inflation is increasing the price of housing, even if the Fed were to cut rates and long-term rates were to fall, bond market investors will want higher yields to compensate for inflation. The best way to bring interest rates and especially mortgage rates down is to reduce inflation below 2%. As we have seen above, that is not going to be easy. Over time, I expect that fed funds rates will come down but only after inflation is coming down. That is certainly not going to happen in the next six months.

But if we see an end of the war in Iran (thus energy prices falling) as well as Owner’s Equivalent Rent (OER) finally showing up in lower housing inflation, we might see a situation in the coming year where the Fed has room to cut. But that is not happening this year.

Gold and Grandkids

Roughly 13 years ago, we did a promotion for the Hard Asset Alliance which gave investors a way to conveniently buy and store gold offshore. Basically, your gold is held in a vault in Zürich, London, Perth, Singapore or New York. There was quite a positive response. The company has changed names (now GBI Direct), but the proposition is basically the same. You can store your gold, and can have it delivered to you when and where you want it. You pay a small annual storage fee. The company has roughly 200,000 customers.

While I have my personal gold in a bank vault, they also let me do something unique. I opened an account for each of my grandchildren, starting in 2014, and still buy $100 a month in gold for their accounts. I realized this week that I have new grandkids that I do not have in that program. I asked my assistant Tammi to figure out how to add accounts and I was curious as to how much the accounts have grown. It turns out the initial grandkids are all well over $30,000 and the others have their share, depending on when they started. None of them know about it.

Whether for yourselves or your kids and grandchildren, GBI Direct is a convenient way to own gold, especially if you’re purchasing small quantities each month. If this is of interest to you, you can find out more at GBI Direct. And don’t tell my kids!

Comments

Log in or sign up to join the conversation.