Next month I will begin my 27th year of writing this letter. The way I write, how I come up with topics, when I write have all changed over time. But one thing is consistent: when I sit down to write there is a blank screen. Some weeks topics are obvious. Some weeks I scramble as the fear of a blank screen forces me to just start writing. On a few occasions those are my better pieces. Often, well, let’s just say that those letters will make the top of the list.

This week a number of articles caught my attention. The only thing that ties them together is their impact on the US and global economy. Economic anomalies: things we were not looking for but show up and force us to pay attention. Today in the summer heat, let’s take a look at a few of them.

People As Policy

The new Federal Reserve Chairman Kevin Warsh announced at the beginning of his term that he would create 5 taskforces to deal with various topics:

Communications: Warsh is clearly on record as not being in favor of the forward guidance to the extent that it developed under Bernanke, Yellen and Powell. He did not offer a dot plot in his first meeting. He wants a complete rethink.

Balance sheet policy: Warsh would like to reduce the balance sheet and shorten the duration of his portfolio.

Improving data: we all know that the data the Federal Reserve gets from the BLS and other government agencies is outdated and the methodologies are suspect in a modern era. Should the Fed collect its own data or work with the government agencies to improve their methodology? I have talked about this in the past and there are ways to do this but it is not simply tinkering around the edges of data collection. There needs to be wholesale changes and modernization.

Productivity and jobs: arguably this (employment) is one of the assignments that Congress has given to the Fed but the linkage between monetary policy and jobs is not clear.

The most important task force? In my mind it is the one on inflation. Warsh wants to revisit how the Federal Reserve understands and responds to the drivers of inflation.

When I first read about the Task Forces, I was admittedly a little skeptical. Another blue-ribbon committee making suggestions that will be thrown into the mind-numbing bureaucratic maw, chewed up and “processed” and passed through the system ending up as the same old… stuff.

Please note: I am a huge fan of Kevin Warsh. He is clearly changing the culture at the Federal Reserve. This is the regime change that not many people are talking about. But as we have found, regime changes are more difficult than simply saying the words.

Then Thursday I looked at the people that he appointed to the taskforces. The one that stood out to me immediately was his task force on inflation:

Greg Mankiw, professor of economics, Harvard University; former chairman, Council of Economic Advisers

Thomas Sargent, professor of economics, New York University; Nobel laureate

William White, senior fellow, C.D. Howe Institute; former economic adviser, Bank for International Settlements

Thomas Sargent and Bill White (who is no stranger to my readers and to attendees at the Strategic Investment Conference) are hell on inflation. Bill White, when he was the Chief Economist at the Bank of International Settlements, consistently fought with central banks and governments over inflation. Nobel laureate Tom Sargent is one of the true conservative Nobel laureates and whose research reinforces the points about inflation and fiscal policy, along with a number of other topics. I know both of these gentlemen. Greg Mankiw is a well-known conservative economist at Harvard.

His task force on productivity and jobs? Marc Andreessen (Andreessen Horowitz) and Asha Sharma, executive vice president and XBOX CEO, Microsoft Corp. (MSFT) The one academic, Charles I. Jones, professor of economics, Stanford University, is currently on leave at Anthropic. Three very serious thinkers to understand the impact of AI on jobs and productivity as well as normal business practice. All-Star team.

I do not want to go into the weeds on each task force, but they are all of the same cloth. People with deep understanding of their topics and aware of the need for dramatic change in directions. Clearly Warsh has been planning this for a very long time.

Warsh in his speeches and publications has been very clear that he expects things to change at the Federal Reserve. The people he has appointed to these task forces simply double down on that expectation.

This is a potential major sea change in central bank policy. It is coming at us at the same time as the Japanese central bank is also making changes. The yen is continuing to weaken (finally). The Japanese central bank could raise rates more, which would give strength to the yen but that also has consequences. If the BOJ buys bonds, that will be seen by the market as quantitative easing and inflationary.

What they have elected to do this week is to “encourage” Japanese pension funds to sell foreign government bonds (read US) and buy Japanese bonds. That would both support their bond market, increase the value of the yen and not be a shock to their stock market. Just one fund alone has almost $2 trillion in assets. It is conveniently controlled by the Bank of Japan. What do you do when the boss encourages you to do something? And if you’re an independent Japanese pension fund, when your central bank comes to you making suggestions, what do you do?

This will complicate Chairman Warsh’s life as he needs more buying of US treasuries, not less. This will not happen overnight, but it will be a direction that will work its way through US yields, even if on the margin.

People are policy and the people that Kevin Warsh has put on the committees should send a big signal to the markets. It should also send the same signal to Congress, but they will ignore it until there is a fiscal crisis. Hopefully by the time we have a crisis, Warsh has his team and policies in place to be able to force Congress to deal with their own fiscal dysfunction. It will take a great deal of fortitude and courage, but I believe he is the man for the job.

Market Response to the Oil Shock

As you might imagine, I get a wide variety of publications sent to me. I recently ran across an article from Scott Lincicome of The Dispatch. I found myself nodding along, as he described the same internal reflection that I have had recently. I found myself being very pessimistic about the Strait of Hormuz being closed. I am on record in numerous places of being long-term bullish on the price of oil and especially gas. Part of that was the simple fact that the consumption of energy (coal at first) and then oil has gone from the lower left to the upper right on the graphs for over 200 years. With the exceptions of recessions, the demand for oil and gas has been steadily increasing year-over-year. While developed nations are becoming more efficient, developing nations aspire to the same energy usage that we in the West have, and thus demand more oil and gas.

And that logic held up until recently. I really thought by this time (assuming Iran had not capitulated, which they obviously didn’t) the price of oil would be far higher and the shocks would be throughout the economy.

So what happened? Yes, the price of oil and gas has risen, but not as much as I thought it would. It seems that free markets respond the way they’re supposed to. I have used the line many times: the cure for high prices is high prices. High prices will reduce demand and increase production of whatever commodity or service we are talking about. It’s not instantaneous, but it happens over time.

I was skeptical that production could increase and wondered where it would finally come from. Clearly something is happening.

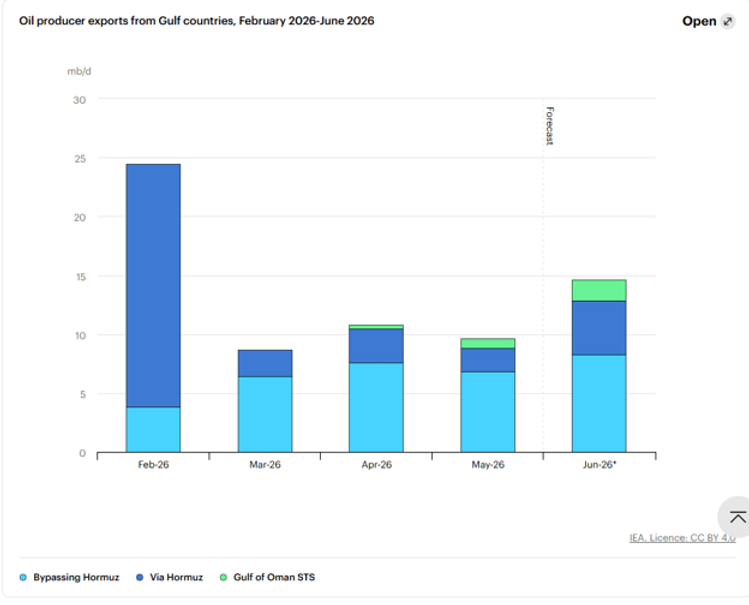

The International Energy Agency just released a report that gives us insight into what really happened.

Oil consumption in the world was a little over 104 million barrels per day in the fourth quarter 2025. (IEA) The closing of the Strait of Hormuz cut out 10 million barrels per day or 10% of world production. Yes, we had reserves and so forth but the math was fairly straightforward: when the world ran through reserves, unless the Strait was open, the price will go through the roof. The roof being $140 or more.

But then a strange thing happened on the way to the forum. The markets actually worked. The IEA report identifies three major reasons why we didn’t see oil prices in the stratosphere.

There were large releases from private storage. Governments opened their emergency stockpiles. That added 3.8 million barrels a day to the global supply so far.

Second, oil producers responded to the shock with crude output and sales that avoided the conflict zone. Saudi Arabia and the United Arab Emirates, for example, utilized alternative transportation routes—like the Saudis’ East-West pipeline—to bypass the strait and boost non-Hormuz oil exports by several million barrels per day.

Source: IEA

Refiners in the U.S. and Africa also boosted output and exports, especially for jet fuel to Europe—avoiding the dire consequences that many airline analysts predicted.

Simple demand destruction. The IEA estimates that demand will be 5 million barrels per day lower than was predicted in January. China is a big part of that, with their demand dropping by 4 million barrels per day.

As Scott noted, there were other smaller contributors. There was a lot of oil smuggling from Iran and Russia. Both nations had “shadow fleets” already in place smuggling large amounts of oil against sanctions. Clearly that has to stop.

“Most notably, the Trump administration waived the Jones Act for an unprecedented 150 days, thus boosting U.S. energy supplies (and security) by allowing foreign-flagged vessels to move American-made crude, refined products, and fertilizer between U.S. ports. So far, the waiver has allowed tens of millions of barrels and dozens of voyages that would’ve been banned by law in nonwaiver times.”

Source: Cato Institute

“Few, if any, of these adjustments were costless—trade-offs always exist—and the market remains fragile. But even with the conflict still percolating, the doomsday scenario that many smart, nonpartisan eggheads predicted simply never materialized.

“And the reason is textbook stuff: A massive supply shock triggered a dramatic increase in prices that was based on the expectation of reduced future supplies. Those high prices signaled to the rest of the world to supply more—by pump, export, or stockpile—and/or consume less. And, because crude oil is an easily transportable commodity traded on a global market that’s relatively transparent and free (and, thanks to liberalizing moves like Trump’s Jones Act waiver, made even freer after the shock hit), prices remained well below what most experts predicted based on an educated—but static—view of existing supply and demand patterns.”

Source: Cato Institute

The same thing is happening in other scarce commodities such as fertilizers, helium and sulfur. Markets adapted. It wasn’t plain or pretty, but the world is not ending. It is against the instinct of most politicians to trust the markets; this episode should at least give policymakers pause before they enact price controls or try to manipulate the market.

By the way, the president has the ability to waive the Jones Act for a period of time. The Jones Act might’ve been useful in 1920, but it is a drag on the national economy today. I can tell you that in Puerto Rico it contributes to higher costs. Clearly, the market responded by producing more oil because of the removal of the constraints of the Jones Act. Maybe Congress should just consider at least scrapping it for energy markets, if not for everything?

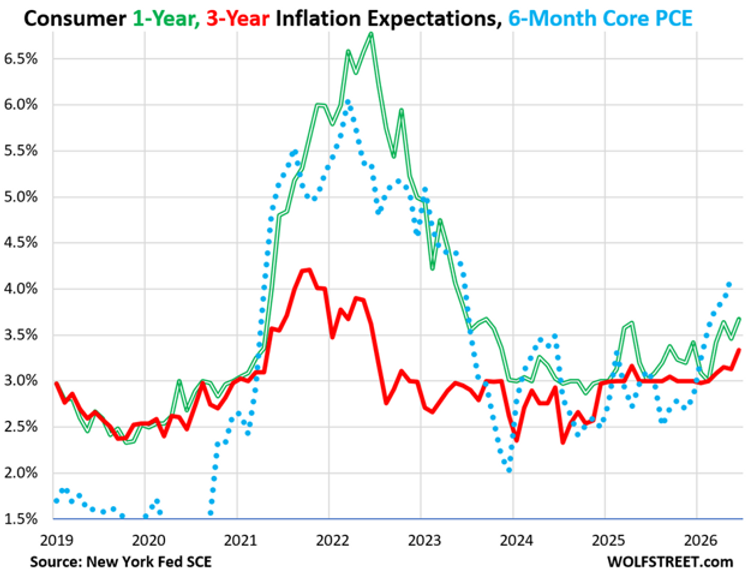

Core Inflation Expectations Are Not Well Anchored

In the past, the Fed preferred to look at inflation as measured by PCE. “Core” PCE was the Fed’s benchmark. And core PCE has been rising since the middle of 2025. Recently, part of that has been energy prices but not as much as you might think, as it is still working its way through the system. But recent core PCE was 3.47% and the Fed projects 3.3% for June. Well above the 2% target. The six-month core PCE is at 4.1%, which more accurately reflects the recent energy price increases and is the worst in three years.

Consumer expectations have been rising as well. Wolf Richter at Wolf Street offers this chart:

Source: Wolf Street

“Consumers’ median inflation expectations for one year from now rose to 3.67%, the highest since September 2023, when they were on the way down (green double line).

“Inflation expectations for three years from now rose to 3.34%, the highest since Jun 2022 (red line). These “medium-term inflation expectations,” as they’re called in the Fed’s communications, had been “well anchored in all of 2025, but at 3.0%, which is not near the Fed’s inflation target of 2.0%. And this year they became unanchored off this 3.0% line and in June rose to 3.34%, the highest in four years.”

The Fed wants to keep inflation expectations “anchored.” This makes sense as high inflation expectations means that consumers will adjust their spending as well as ask for higher wages, and businesses will start increasing prices in anticipation of higher inflation.

Obviously, the Fed wants to anchor inflation at their 2% target. The previous three Federal Reserve chairs were all focused on consumer expectations. It remains to be seen what this chairman will do. I think that if he continues to focus on bringing inflation down that he believes expectations will follow.

Kevin Warsh, borrowing a phrase from The Blues Brothers, believes he is on a mission from God to bring inflation below 2%. It will not happen this year but over time? Absolutely.

Comments

Log in or sign up to join the conversation.