Key Market Outlook(s) and Pick(s)

On Monday, I joined Brian Sozzi on Yahoo! Finance to discuss markets, the economy, outlook, Iran, rotation, the consumer, defensives, and a lot more. Thanks to Justin Oliver and Brian for having me on:

Video Length: 00:06:22

On Tuesday, I joined Sarah Al-Khaldi on Channel News Asia to discuss markets, the economy, outlook, rotation, the consumer, defensives, and a lot more. Thanks to Sarah and Marianne Star Inacay for having me on:

Video Length: 00:05:36

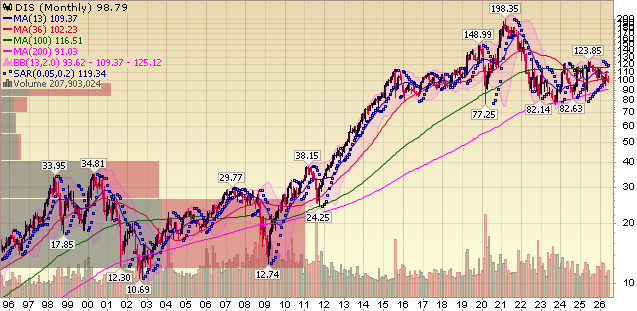

Disney Update

For newer readers, here’s a quick overview of the key drivers behind our thesis on Disney, once a media company with theme parks, now a theme park company with media along for the ride:

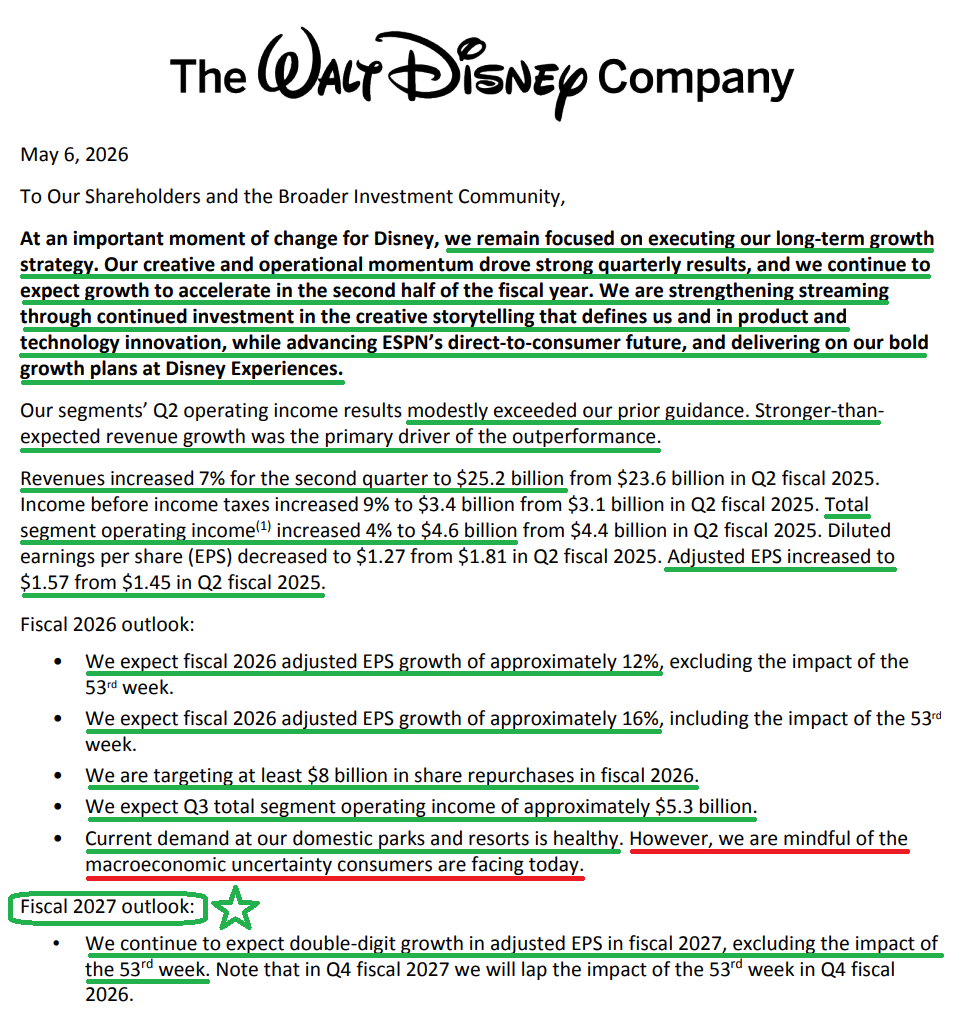

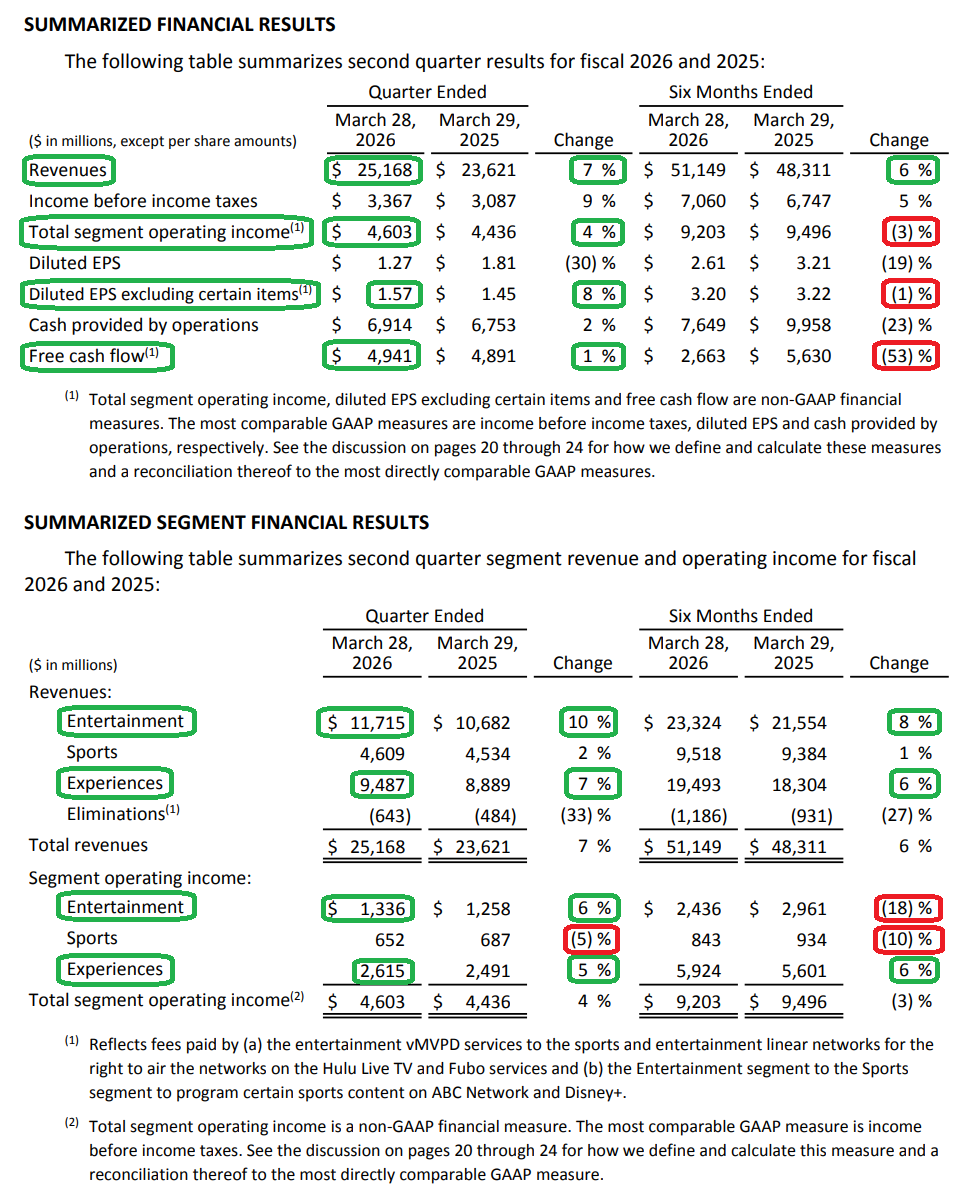

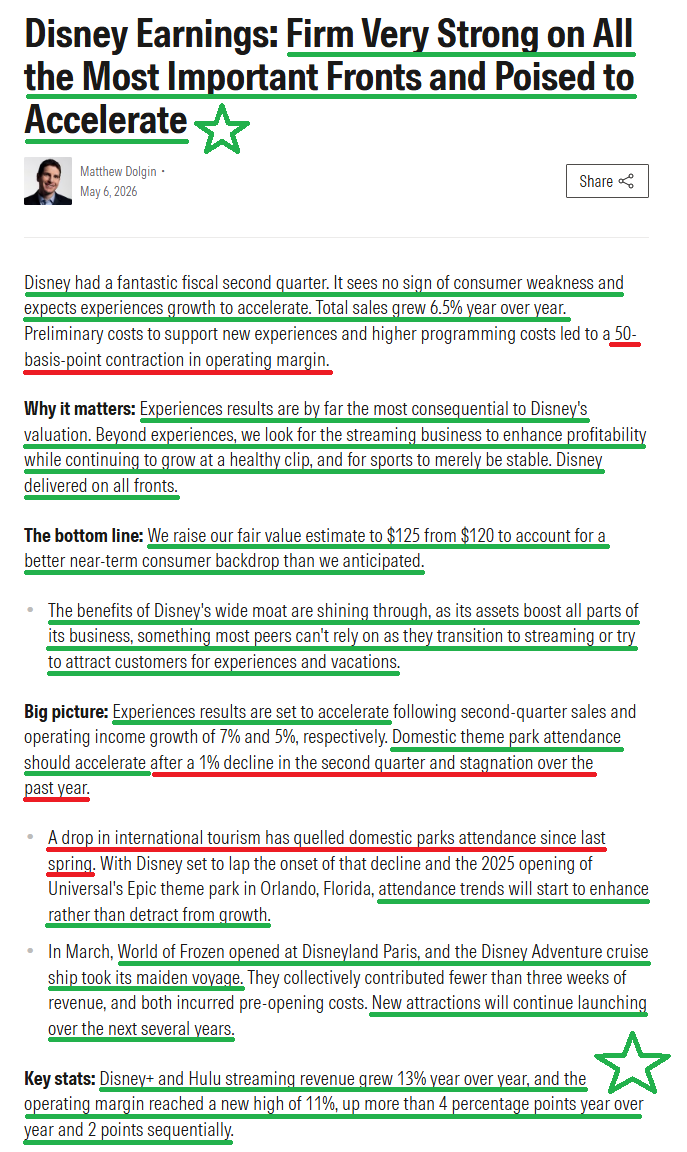

Disney delivered another fantastic quarter, with results checking every box that matters to the long-term investment case for the Mouse House. Revenue increased 7% Y/Y to $25.2B, while adjusted EPS rose 8% to $1.57, both ahead of expectations. Experiences delivered record revenue and operating income, Streaming reached a double-digit operating margin for the first time in company history as profits nearly doubled Y/Y, and management reiterated expectations for double-digit adjusted EPS growth in both fiscal 2026 and, even more importantly, fiscal 2027.

Throw into the mix one of the strongest film slates in years, a record investment pipeline across theme parks and cruises, and a raised $8B annual buyback authorization, and it’s difficult to poke many holes in the Disney story today.

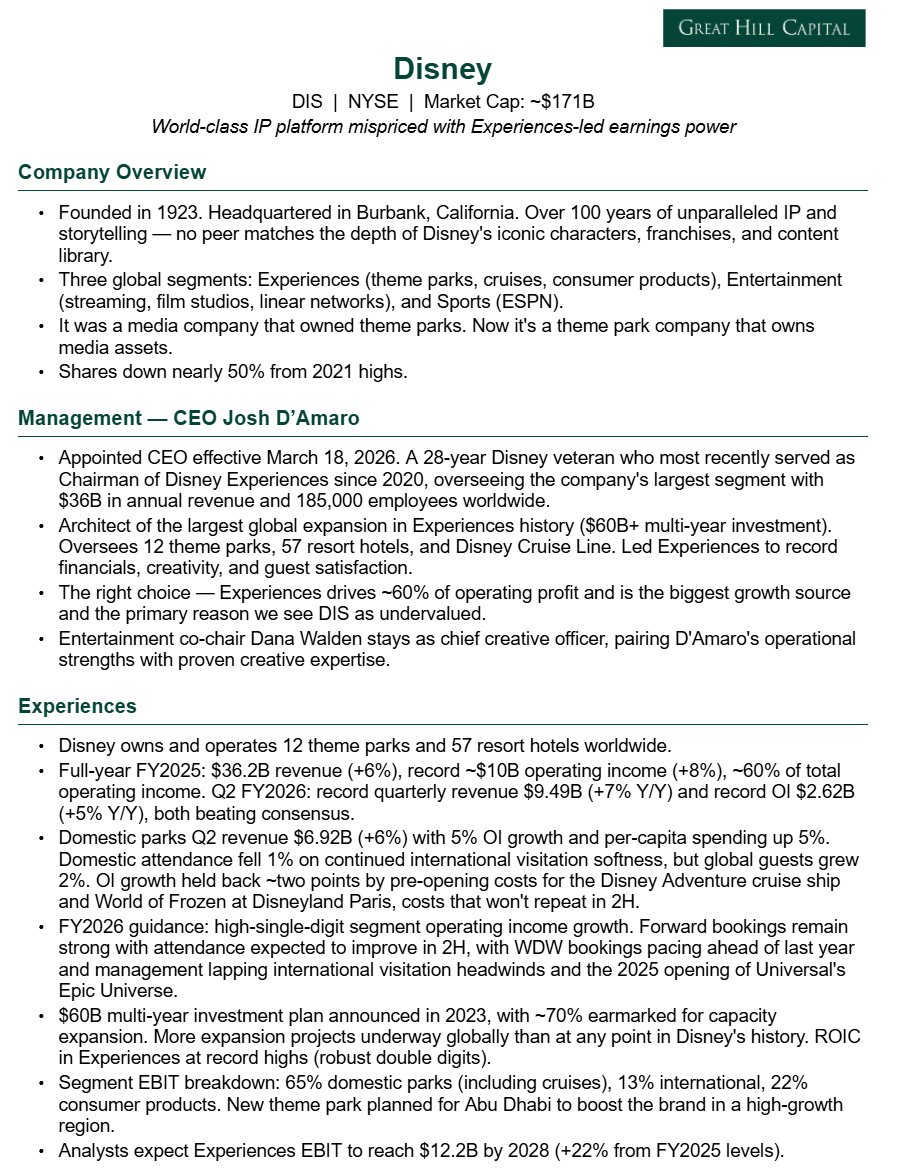

While the strong headline numbers were encouraging on their own, the bigger story of the quarter was that it marked the first under new CEO Josh D’Amaro. Investors got a clearer read on Disney’s strategy under new leadership, and in our view, it confirmed exactly why the Board made the right decision earlier this year.

Stepping back, this ties directly to the core driver behind our original DIS investment thesis. When we first built our position, we effectively underwrote Disney at a valuation where we were paying for Experiences alone, a segment generating close to $10B in annual operating income and supporting ~$80 per share of intrinsic value on a standalone basis. That left the rest of the business, including ESPN, Streaming, the film studio, and the linear networks, effectively as a free flier.

This is exactly why we’ve argued that the narrative around Disney being a media company that simply owns theme parks has been flipped on its head, with the company today looking far more like a theme park powerhouse that happens to own media assets. And if the theme parks, cruise business, and consumer products have become the economic engine of the company, then naming the executive who built that powerhouse is a no-brainer.

D’Amaro is a 28-year Disney veteran who spent the past six years leading Disney Experiences, the company’s largest and most profitable segment. During his tenure, Experiences grew into a $36B business accounting for 38% of company revenue while generating nearly $10B of operating income, or ~60% of Disney’s total. He also spearheaded the largest expansion in the segment’s history, laying out Disney’s $60B investment plan that continues to reshape the business today.

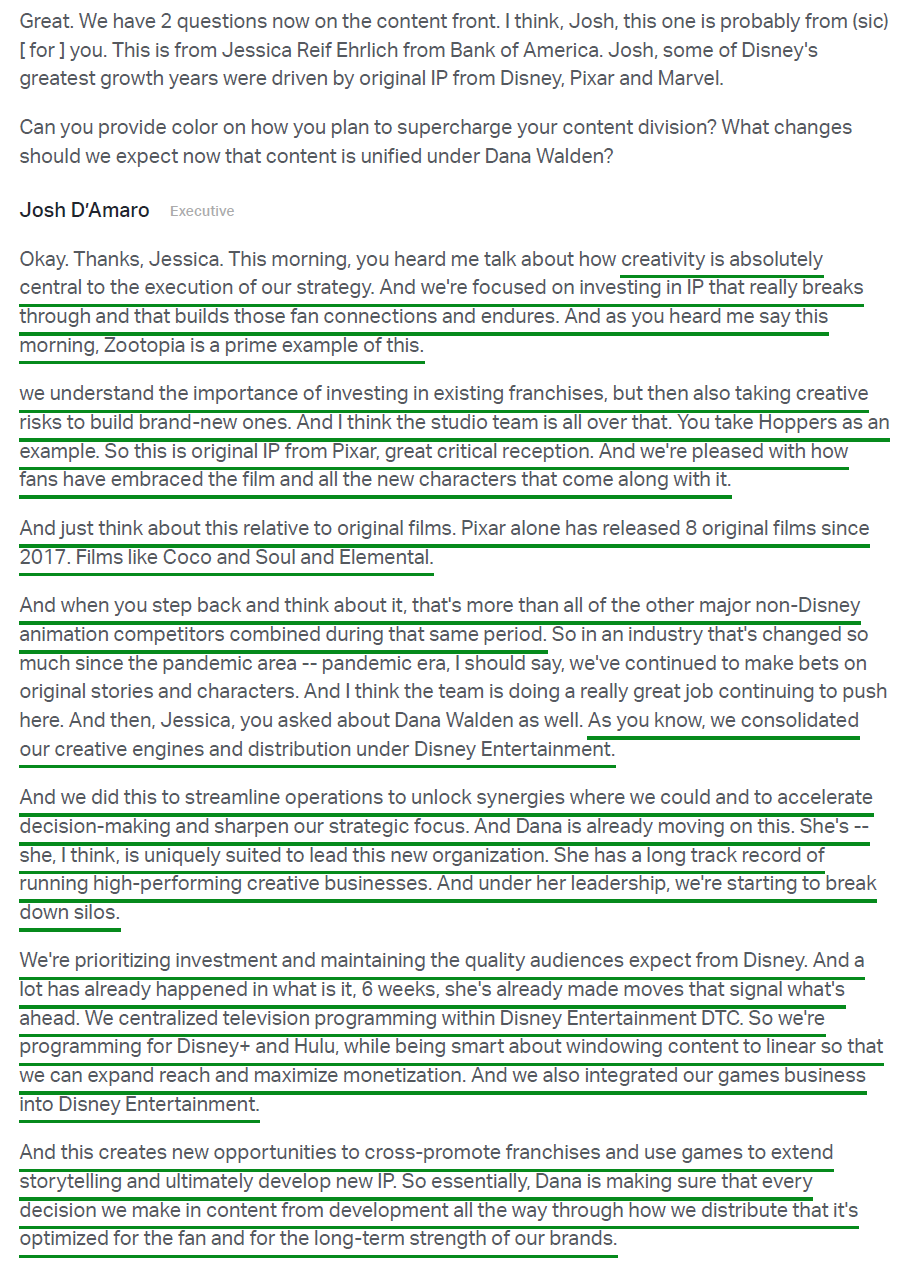

The only real question mark surrounding D’Amaro’s appointment centered on his lack of direct experience on the creative side of the business. Those concerns were largely addressed with the announcement that Dana Walden would remain at Disney in a newly elevated role as Chief Creative Officer, overseeing all of the company’s film and streaming content. We view the pairing as a best-of-both-worlds outcome for shareholders. D’Amaro brings decades of operational expertise and a strong command of the ins and outs of Disney’s parks, resorts, cruises, and consumer-facing businesses, while Walden continues to lead the creative engine responsible for the IP that powers the entire ecosystem. This is the blue-sky succession outcome that few thought was on the table.

In his inaugural earnings call, D’Amaro outlined three priorities that will guide Disney moving forward: investing in IP and creative excellence, deepening the direct relationship with consumers through Disney+ as the digital centerpiece, and using advanced technology as an accelerant across the business.

While these priorities may appear to be separate initiatives, they are deeply interconnected and all feed into the same engine: Disney’s flywheel.

The flywheel has always been Disney’s greatest competitive advantage, built around its irreplaceable, world-class IP at the center. Successful films extend far beyond the box office, creating characters and franchises that move seamlessly across streaming, consumer products, gaming, theme parks, cruises, and live experiences, allowing Disney to monetize the same IP across countless touchpoints. While this concept is not new for a company that has monetized IP this way for decades, D’Amaro’s strategy is focused on accelerating it.

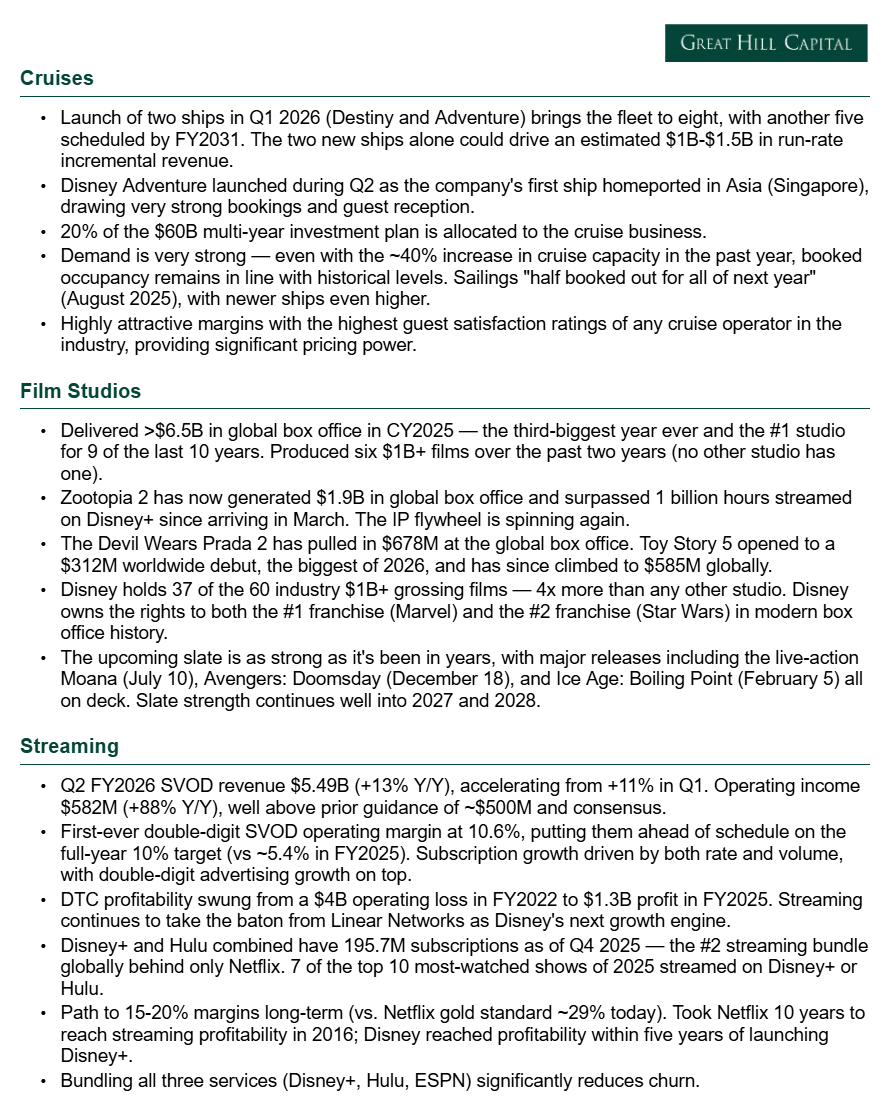

This starts with the studio, and fortunately there are already early signs that the process is well underway.

One of Bob Iger’s first major moves after returning as CEO in late 2022 was shifting Disney away from the volume-driven strategy that flooded the market with content during the streaming wars and back toward a focus on quality.

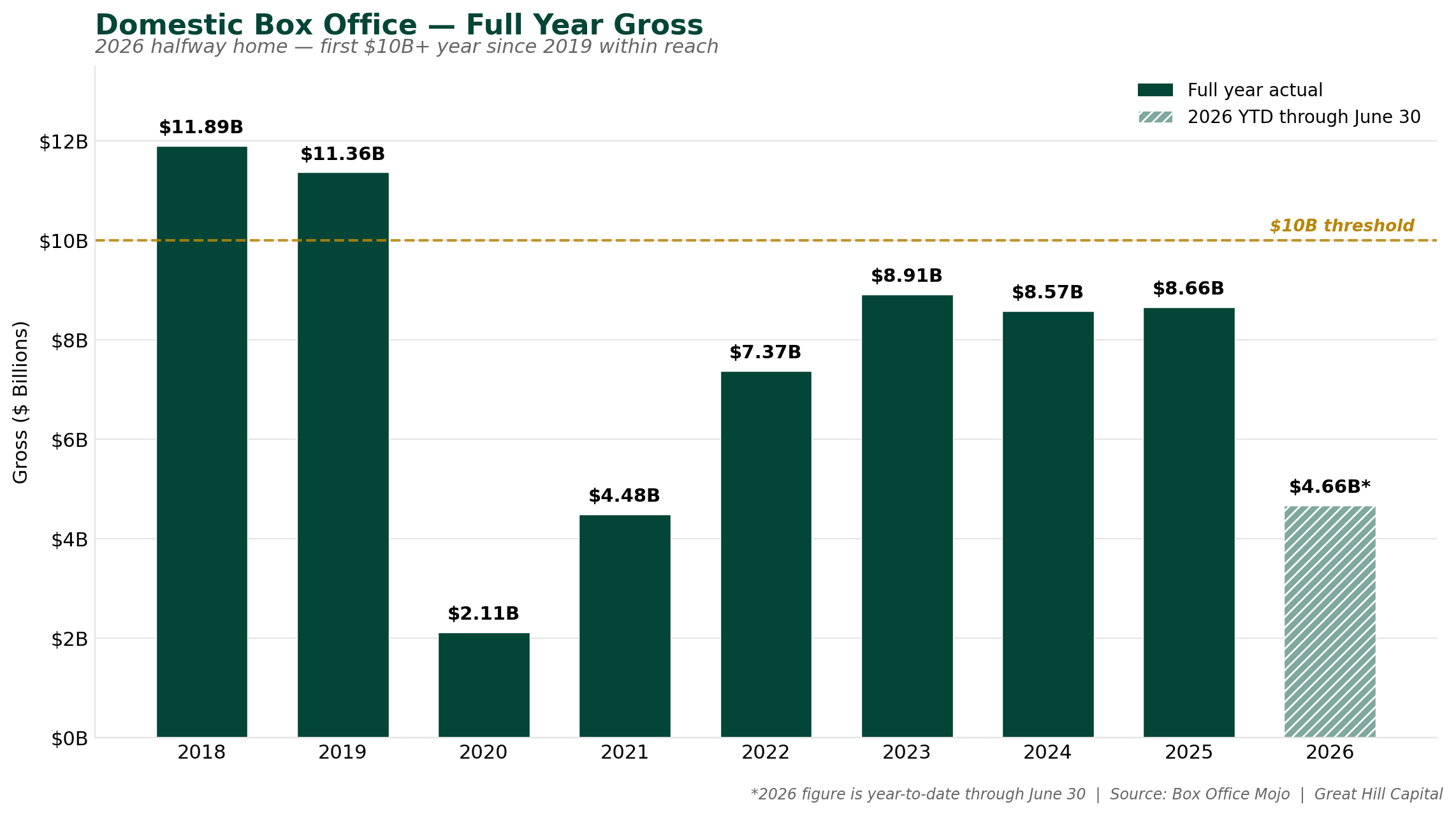

That pivot has already begun to pay off in spades. Disney produced six $1B+ films across 2024 and 2025, while no other studio produced a single one. Calendar 2025 alone generated more than $6.5B at the global box office, marking the third-largest year in company history and extending its run as the #1 studio in 9 of the last 10 years.

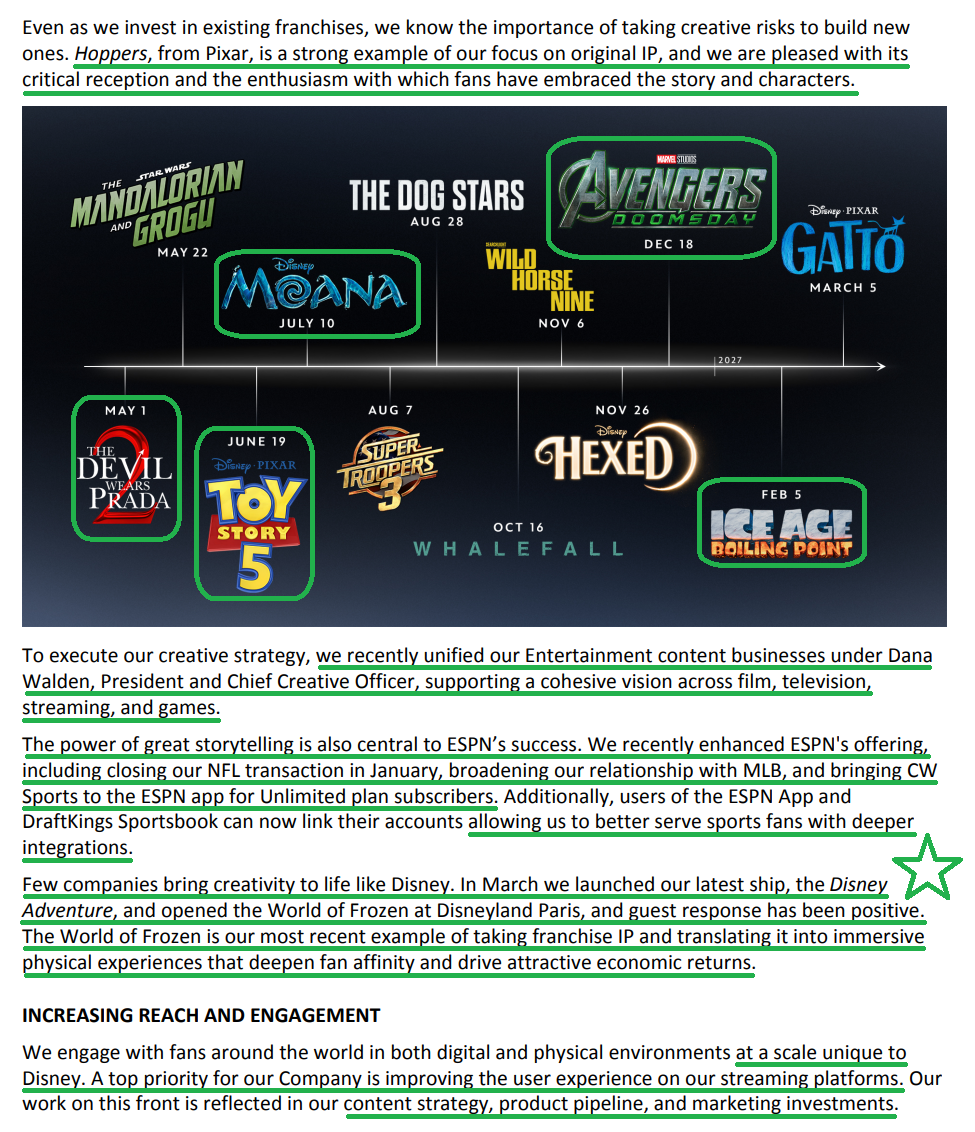

That momentum has carried into 2026. The Devil Wears Prada 2 has already generated ~$678M worldwide, while Toy Story 5 opened to the biggest debut of any film released this year ($312M) before climbing to nearly $600M globally in just two weeks, putting it well on pace to join the billion-dollar club.

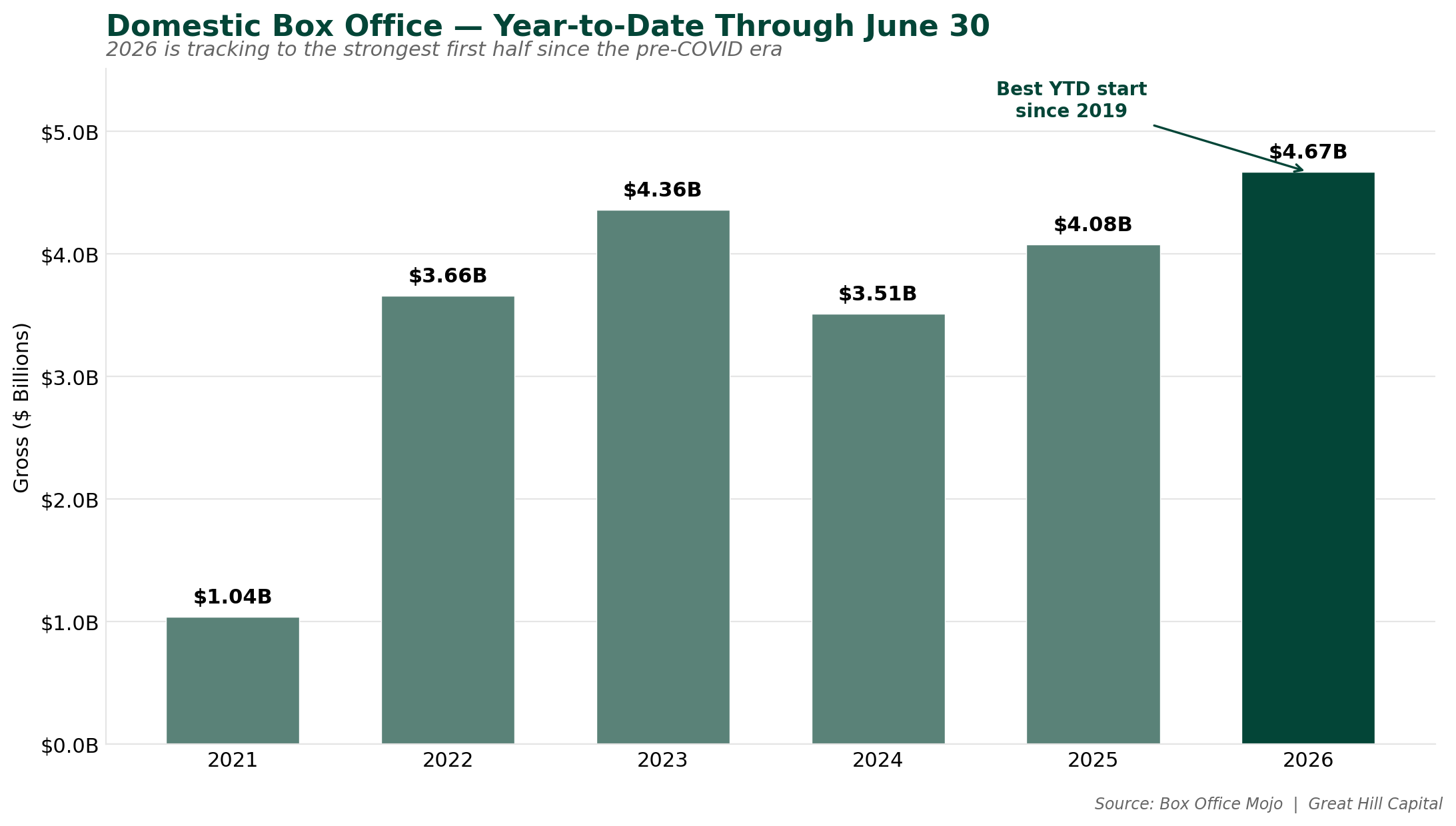

The timing of Disney’s studios finding their footing couldn’t be better. Domestic box office trends continue recovering toward pre-pandemic levels, with the industry enjoying its strongest first half since the pre-COVID era at $4.67B. If the second half delivers as many expect, 2026 will mark the first $10B domestic box office year since 2019, after six long years spent in the pain zone.

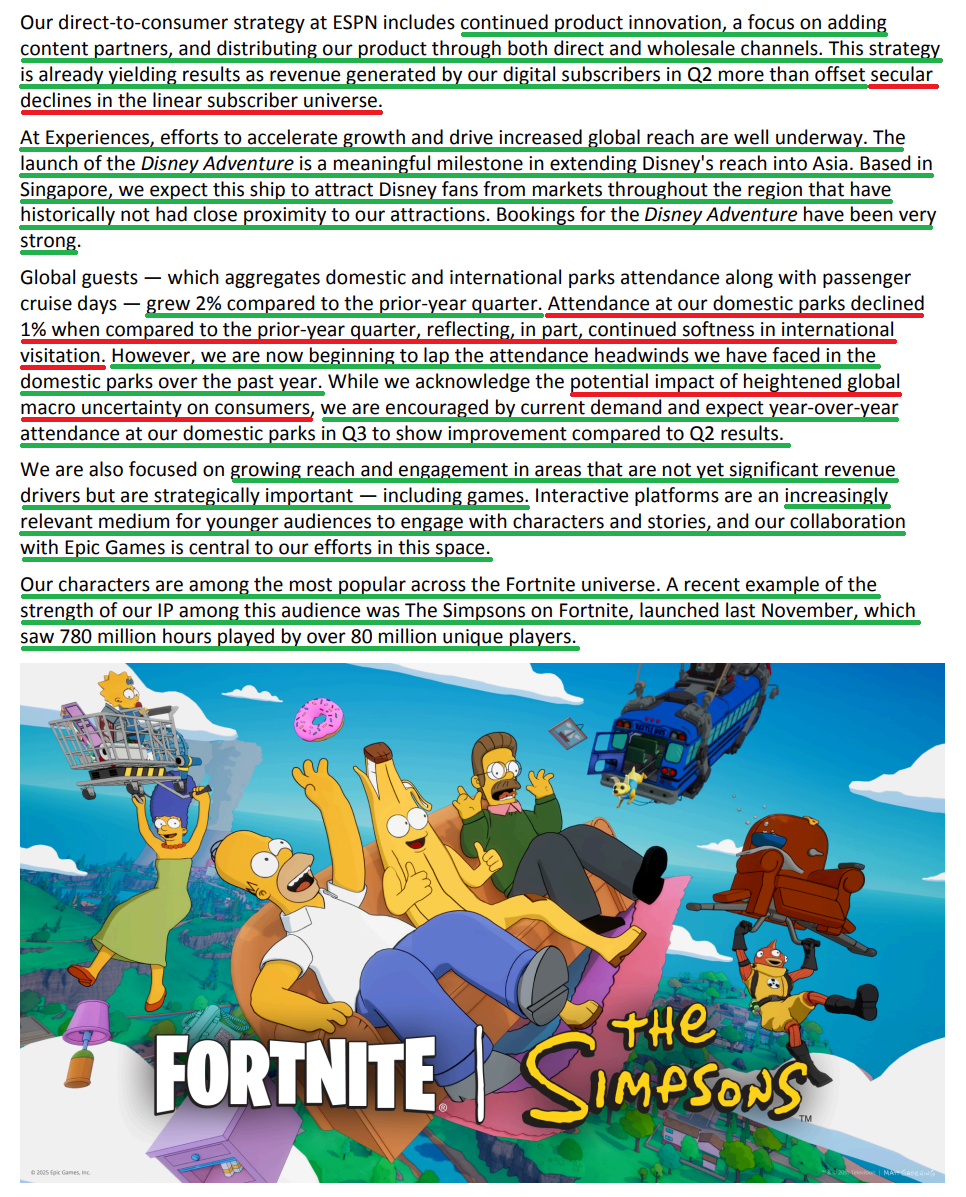

Disney is sitting in the driver’s seat of the recovery, and if the $10B mark is finally crossed in 2026, it will be due in large part to one of Disney’s deepest theatrical slates in years, headlined by the live-action Moana this July and Avengers: Doomsday in December, before a stacked 2027 lineup featuring new Ice Age, Star Wars, The Simpsons, and Frozen films.

While these box office hits may not always show up immediately as the largest contributor to financial results, they remain the most important long-term driver of the business. Where the film studio goes, Disney goes. Everything else, including streaming, consumer products, theme parks, and cruises, simply monetizes the IP created there.

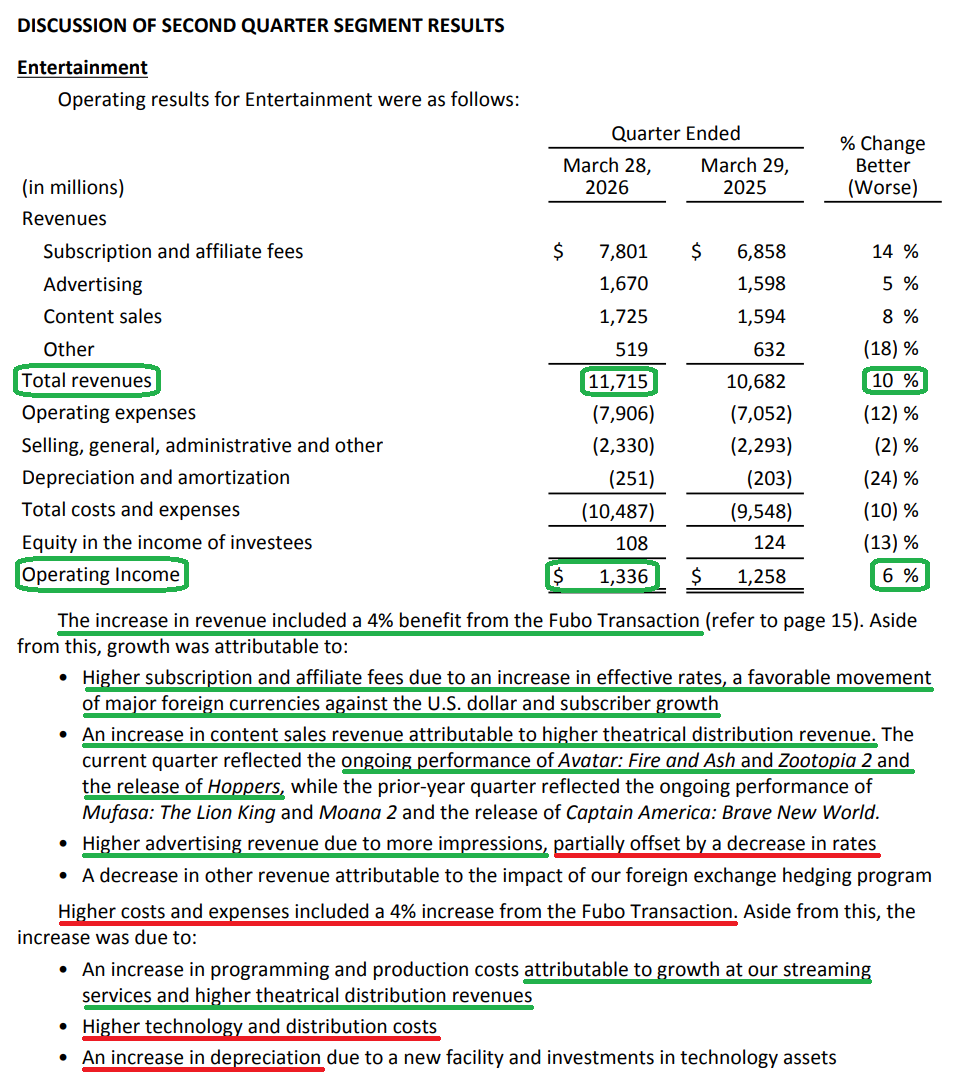

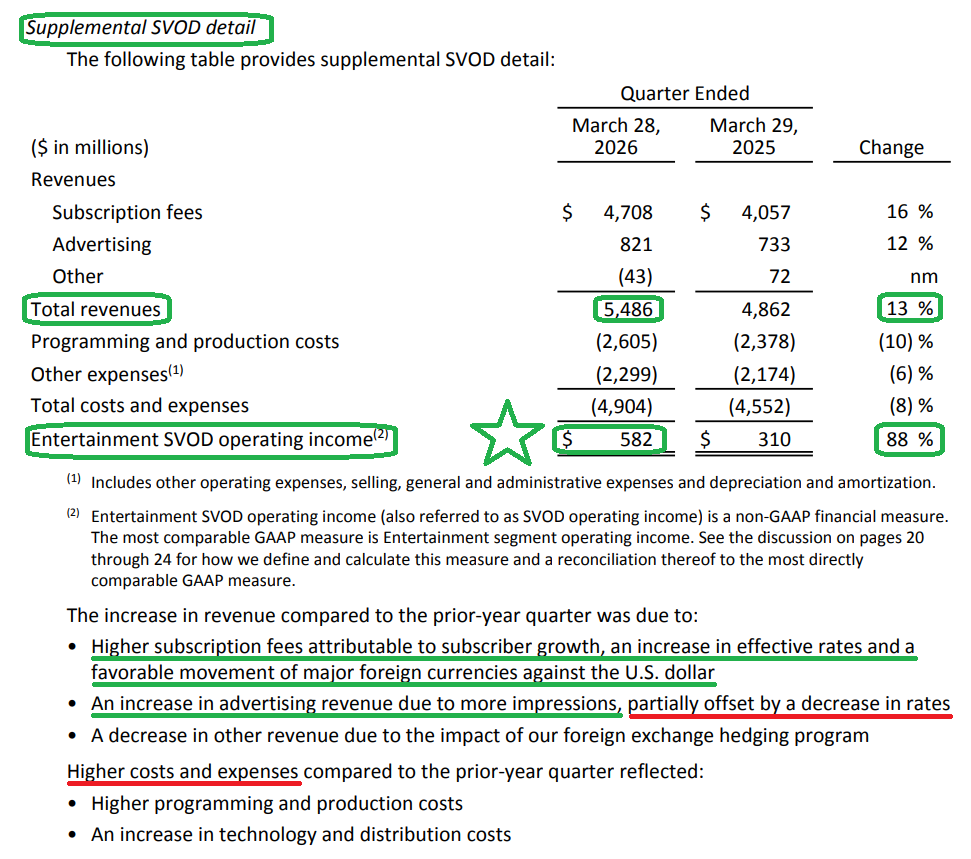

The most immediate and direct beneficiary of Disney making great movies is Streaming, where every successful theatrical release creates another reason for consumers to subscribe, stay engaged, and remain within Disney’s ecosystem. More hits mean more sign-ups, the key driver behind continued top-line growth of 13% Y/Y, accelerating from 11% in Q1.

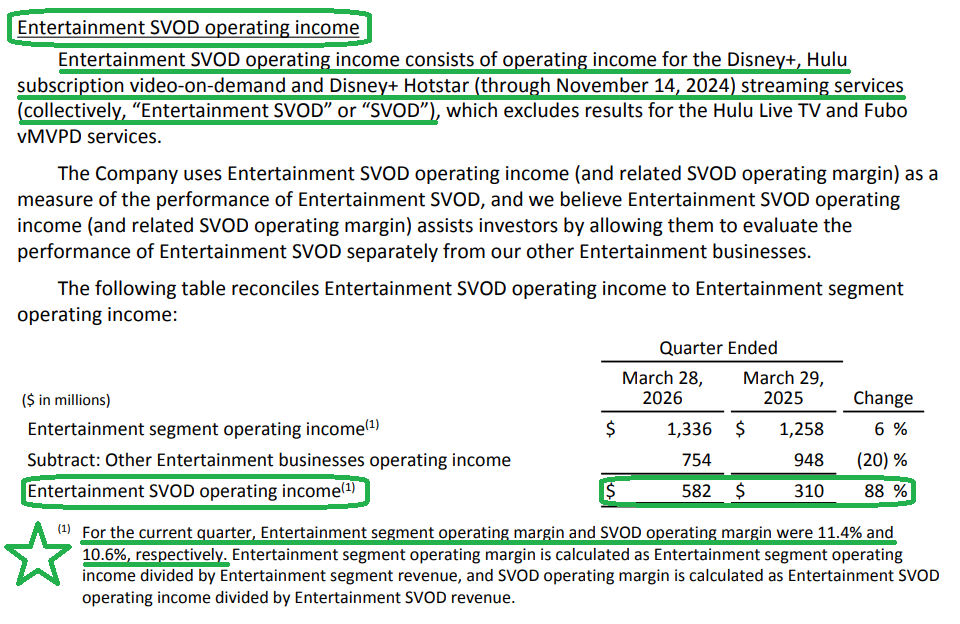

More importantly, just a few years removed from incinerating ~$4B in cash annually, DTC is steadily emerging as one of Disney’s fastest-growing profit centers as it continues taking the baton from Linear Networks. Operating income nearly doubled this quarter, jumping 88% to $582M, and for the first time in company history, Disney+ and Hulu crossed the double-digit operating margin threshold, reaching 10.6%.

While this marks a major milestone for the streaming business and comes ahead of schedule, it is still very early innings with plenty of room for margins to move higher over time. Netflix, which took nearly a decade to reach profitability in 2016, remains the industry’s gold standard with operating margins just below 30%. Disney still has plenty of levers to pull as the platform continues to mature, with recent initiatives including the bundling of Disney+, Hulu, and ESPN, the integrated Disney+ and Hulu experience, and product enhancements such as personalized recommendations, browse previews, and the recently launched Verts feature, all designed to reduce churn, deepen engagement, and expand margins over time. Closing even part of the margin gap with Netflix carries massive implications for Disney’s long-term earnings power and, ultimately, the stock.

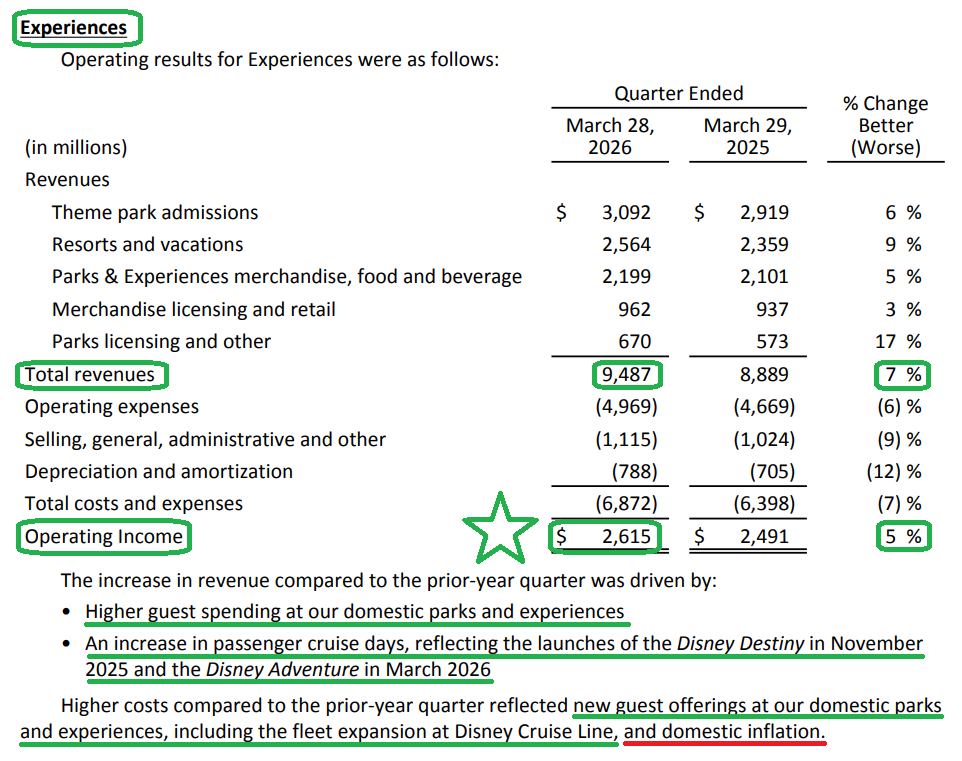

If Streaming is the future growth engine, Experiences remains the financial foundation that made the transition possible. The segment is the core $10B+ profit driver generating the cash flow that allowed Disney to invest aggressively in its direct-to-consumer transition without compromising the balance sheet. In many ways, the parks, resorts, cruises, and consumer products businesses bought Disney the time it needed to build a world-class streaming platform while navigating the melting ice cube that is linear TV.

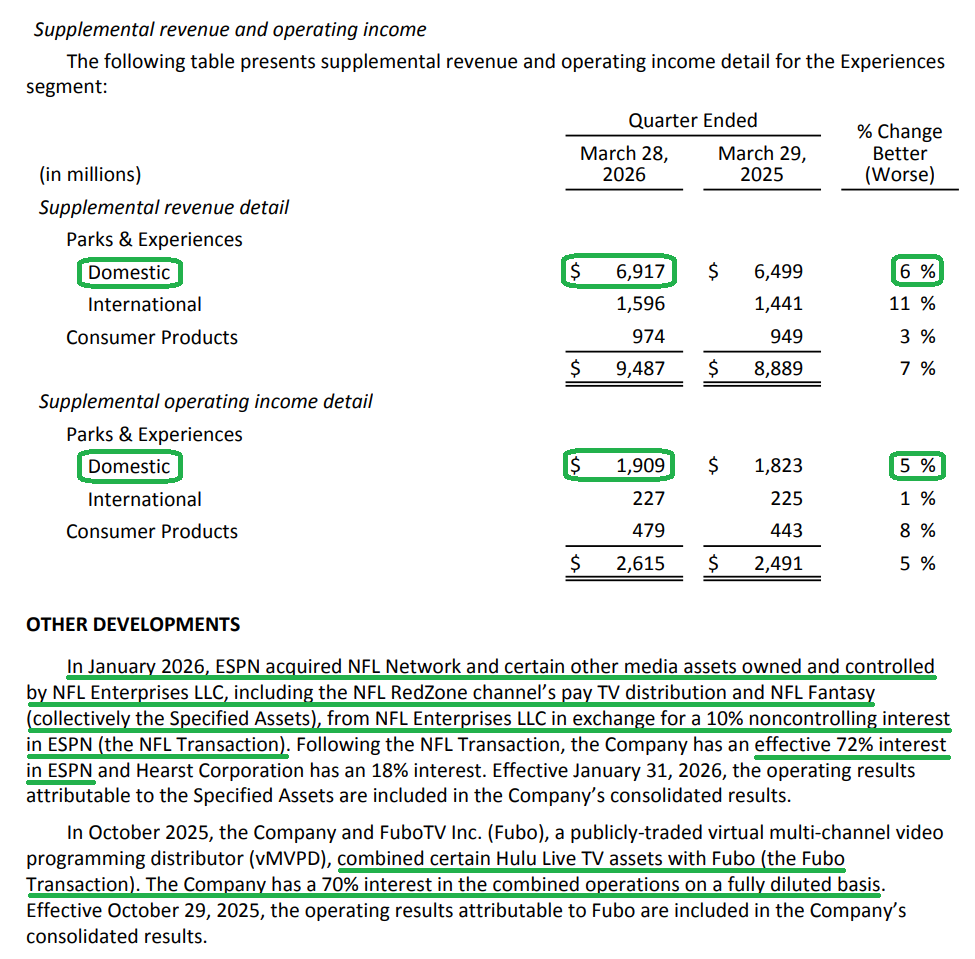

That foundation once again delivered this quarter, generating record revenue of $9.49B (+7% Y/Y) and record operating income of $2.62B (+5% Y/Y), despite temporary headwinds from softer international visitation and non-recurring pre-opening costs tied to new attractions and cruise capacity. For all the concerns surrounding the consumer, management continues to see little evidence of weakness. Forward bookings remain strong, domestic guest spending continues to increase, and attendance is expected to improve throughout the back half of the year as comps become more favorable.

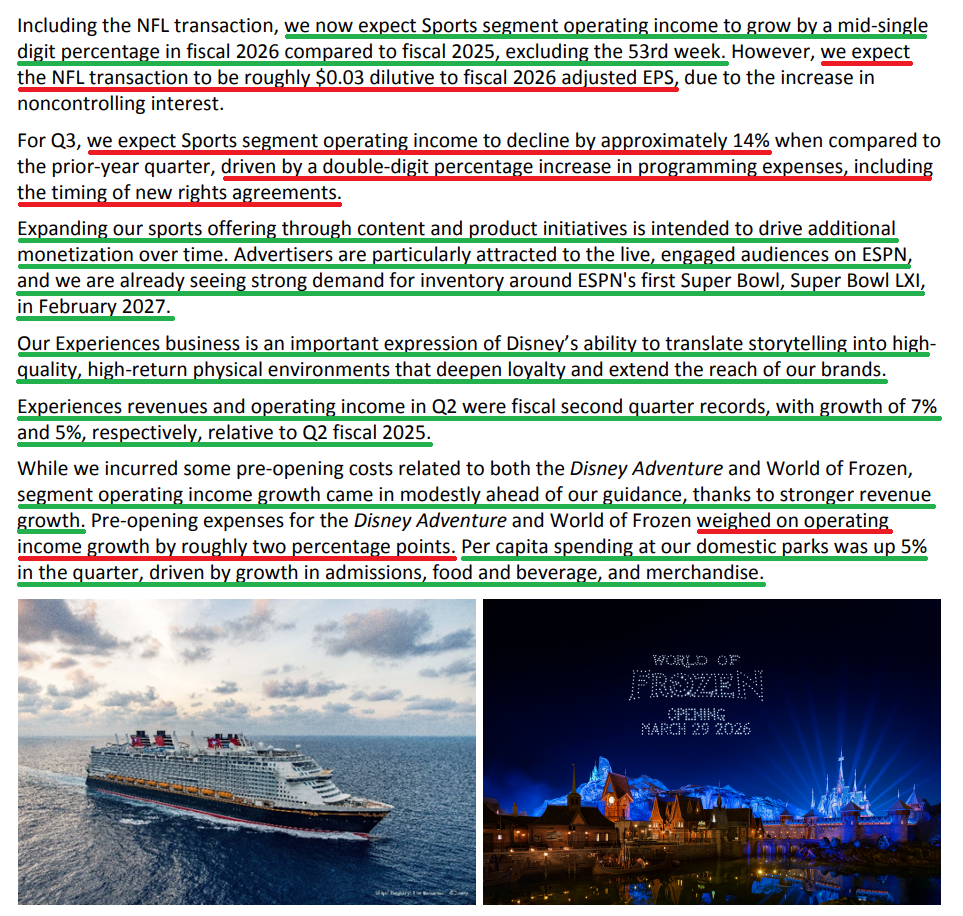

Not only did management brush aside fears of a slowing consumer, they expect growth to accelerate from here. A big reason why is Disney’s $60B expansion plan, with more projects currently under development around the globe than at any point in the company’s history, providing a long runway for attendance and guest spending growth for years to come. A key focus of that expansion is Disney Cruise Line, with the fleet expected to grow from eight ships today to thirteen by 2031. Even after expanding cruise capacity by ~40% over the past year, booked occupancy remains in line with historical levels, supporting management’s view that demand continues to outpace how quickly the company can put new ships in the water, a good problem to have.

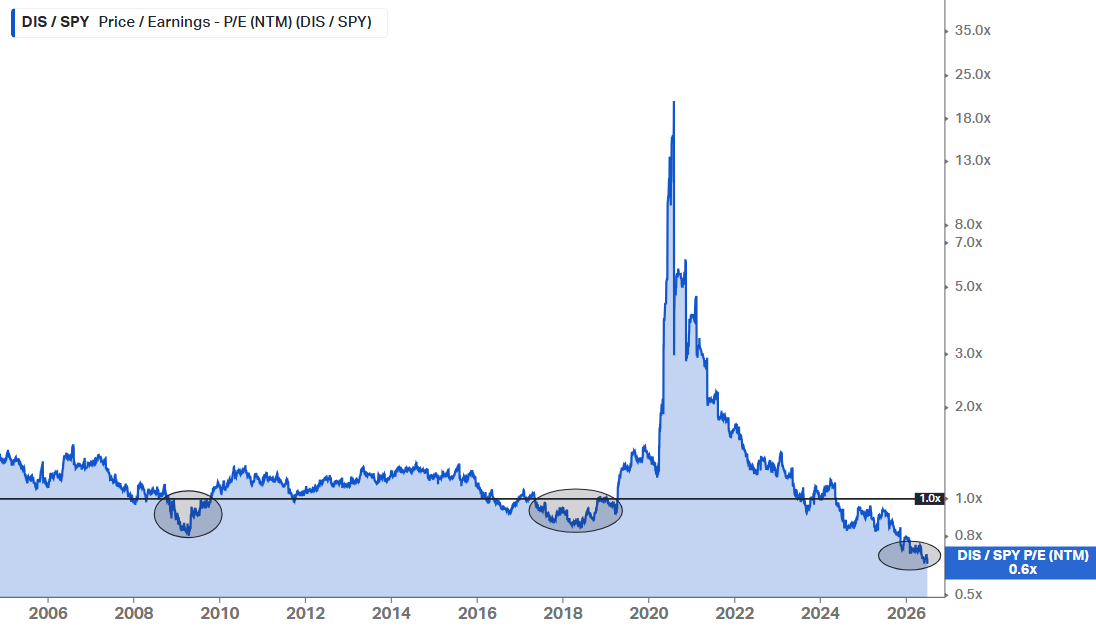

Yet despite the strength across virtually every part of the business, the market continues to yawn. Shares currently trade at ~13x forward earnings, roughly half the company’s historical average of ~26x, and more in line with run-of-the-mill cruise operators like Carnival and Norwegian than a high-quality, double-digit earnings compounder.

In fact, at just 0.6x the S&P 500 multiple, this is the cheapest relative valuation to the market we have seen in nearly three decades. Opportunities to buy Disney at a discount to the market have been few and far between, served up in only two other recent periods: the GFC and the 2018 Fox acquisition. In both cases, the discount was short-lived before snapping back to a historic premium.

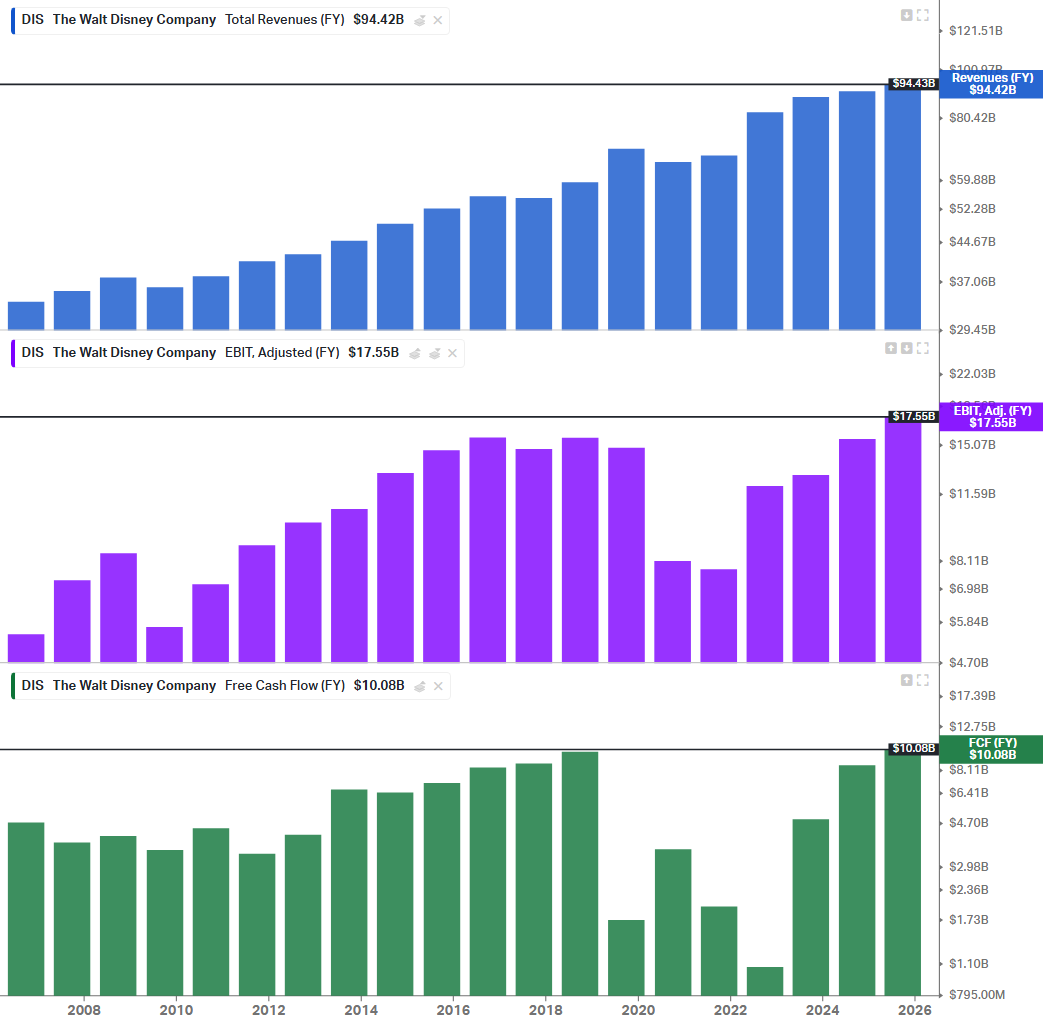

The valuation becomes even harder to justify when viewed through the lens that matters most: fundamentals. Based on this year’s consensus expectations, Disney has grown revenue by ~94%, earnings by ~33%, and free cash flow by ~42% since the stock last traded around these levels more than a decade ago. Today, revenue, operating profit, and free cash flow all sit at record highs, yet the stock has gone essentially nowhere.

Just as you’d expect from a shareholder-friendly management team, Disney is leaning into this dislocation between price and intrinsic value, stepping on the buyback pedal with repurchases now expected to total at least $8B this year, or ~4.7% of the current market cap, while continuing to pay a healthy ~1.6% dividend.

Ultimately, we don’t believe closing the gap between price and value requires another dramatic turnaround story, transformational acquisition, sweeping restructuring, or complete reinvention of the business. It simply needs consistent execution.

Much of the uncertainty that clouded Disney over the past several years stemmed from questions surrounding leadership, streaming profitability, and the future of its traditional media assets. One by one, those questions are being answered.

A few more quarters of disciplined execution under Josh D’Amaro will go a long way toward allowing investors to finally look beyond the uncertainty of the past and put to rest any lingering discount tied to the failed Chapek succession. When that happens, the market’s weighing machine will begin recognizing what the fundamentals already suggest: Disney remains one of the highest-quality collections of assets in the world, with world-class IP, the industry’s premier theme parks, a rapidly growing cruise business, an increasingly profitable streaming platform, and the leading sports media brand, all supporting what we believe is a high-quality, double-digit earnings compounder.

Based on what we’ve seen so far, we believe Disney has found the right director for what could become its best sequel yet.

Q2 Earnings Breakdown

10 Key Points

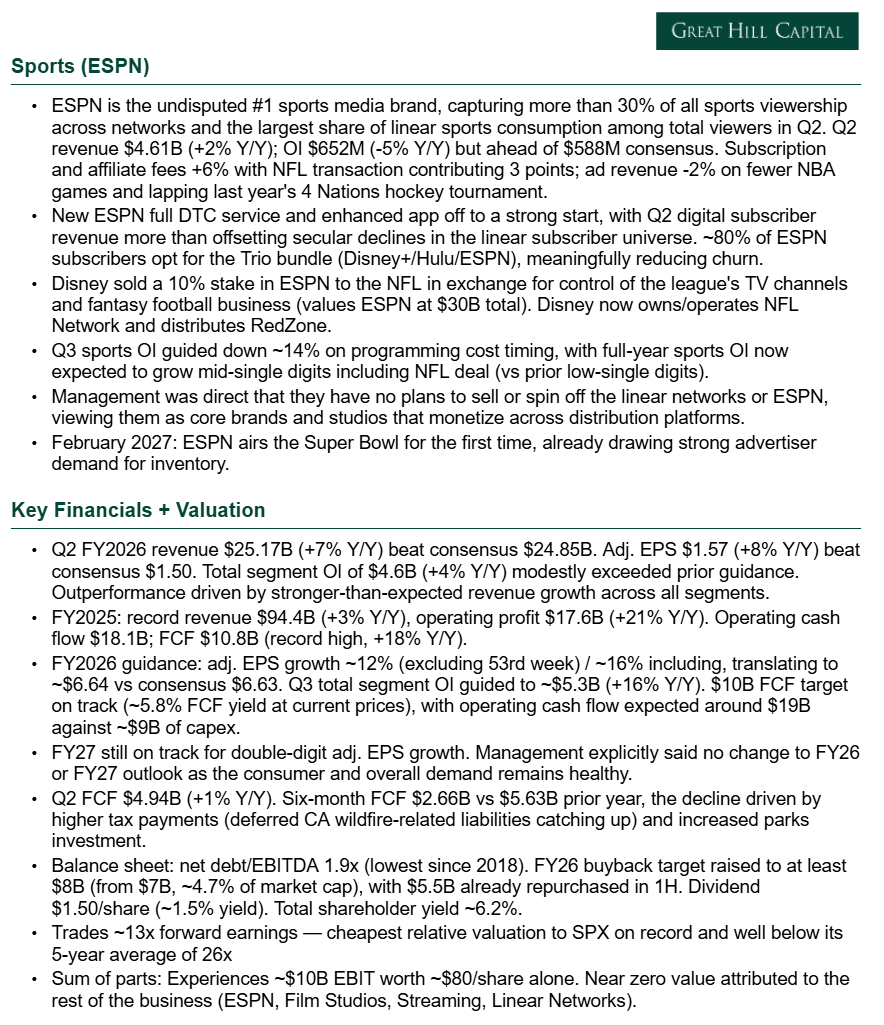

1) Revenue came in at $25.17B (+7% Y/Y), beating consensus expectations of $24.85B, with the outperformance driven by stronger-than-expected revenue growth across all three segments. Total segment operating income of $4.6B (+4% Y/Y) modestly exceeded management’s prior guidance, while operating margins came in at 18.3% versus 18.8% in the prior year period. Adjusted EPS of $1.57 (+8% Y/Y) also topped consensus estimates of $1.50.

2) Streaming continues to take the baton from Linear Networks as Disney’s next growth engine, with Disney+ and Hulu SVOD revenue accelerating to $5.49B (+13% Y/Y) from +11% growth in Q1, while operating income jumped 88% Y/Y to $582M, well ahead of prior guidance of approximately $500M. Most importantly, the segment delivered its first-ever double-digit operating margin at 10.6%, expanding ~420 bps Y/Y and ~220 bps sequentially, putting Disney ahead of schedule on its full-year 10% margin target. Subscription fees grew 16% Y/Y to $4.71B, driven by both pricing and subscriber growth, including the benefit of new international wholesale agreements, while advertising revenue increased 12% Y/Y to $821M. Management continues to focus on reducing churn and improving engagement through initiatives including the integrated Disney+ and Hulu experience and new product enhancements such as the recently launched Verts feature, designed to drive daily interaction, and the video browse initiative, which allows subscribers to preview content while browsing.

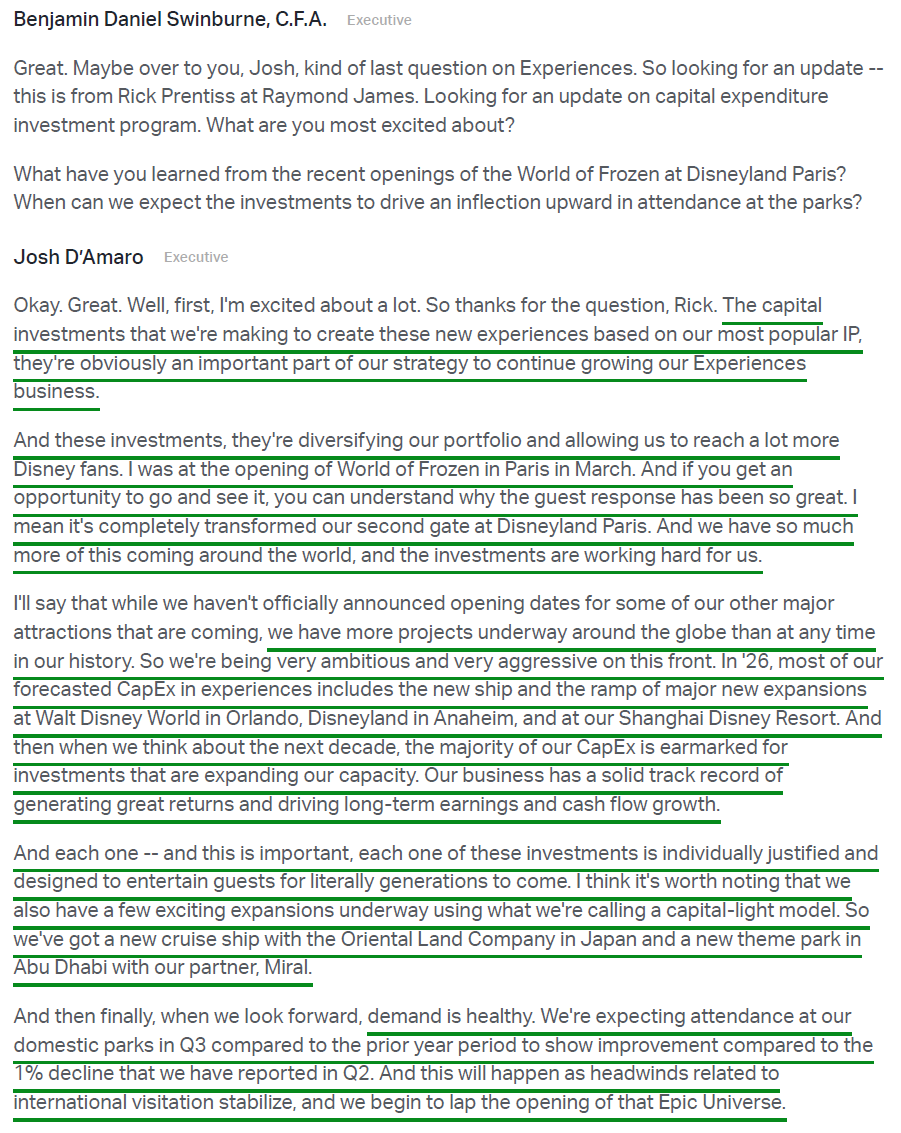

3) Disney’s Experiences segment delivered another record quarter with revenue of $9.49B (+7% Y/Y) and operating income of $2.62B (+5% Y/Y), both ahead of expectations. Domestic parks generated $6.92B (+6%) in revenue as per-capita spending increased 5%, more than offsetting a 1% decline in attendance caused by softer international visitation. Global guests, which aggregate domestic and international park attendance along with passenger cruise days, grew 2% Y/Y. Operating income growth was held back by roughly 2 percentage points due to pre-opening costs for the Disney Adventure and World of Frozen at Disneyland Paris, neither of which will recur in the back half of the year. Management expects domestic park attendance growth to improve in Q3 as the company laps both the international visitation headwinds and the 2025 opening of Universal’s Epic Universe, with forward bookings described as “very encouraging” and Walt Disney World bookings pacing ahead of last year.

4) Disney’s cruise expansion continues to pay off, with the Disney Adventure launching during the quarter as the company’s first ship homeported in Asia, generating very strong bookings and guest reception. Management continues to target fleet expansion from 8 ships today to 13 by 2031, and even with an ~40% increase in cruise capacity over the past year, booked occupancy remains in line with the prior year. Cruises are shaping up to be a meaningful contributor to Experiences growth for years to come, and while management doesn’t break out the business separately, they continue to highlight its highly attractive margins and the highest guest satisfaction scores across the company, translating directly into significant pricing power.

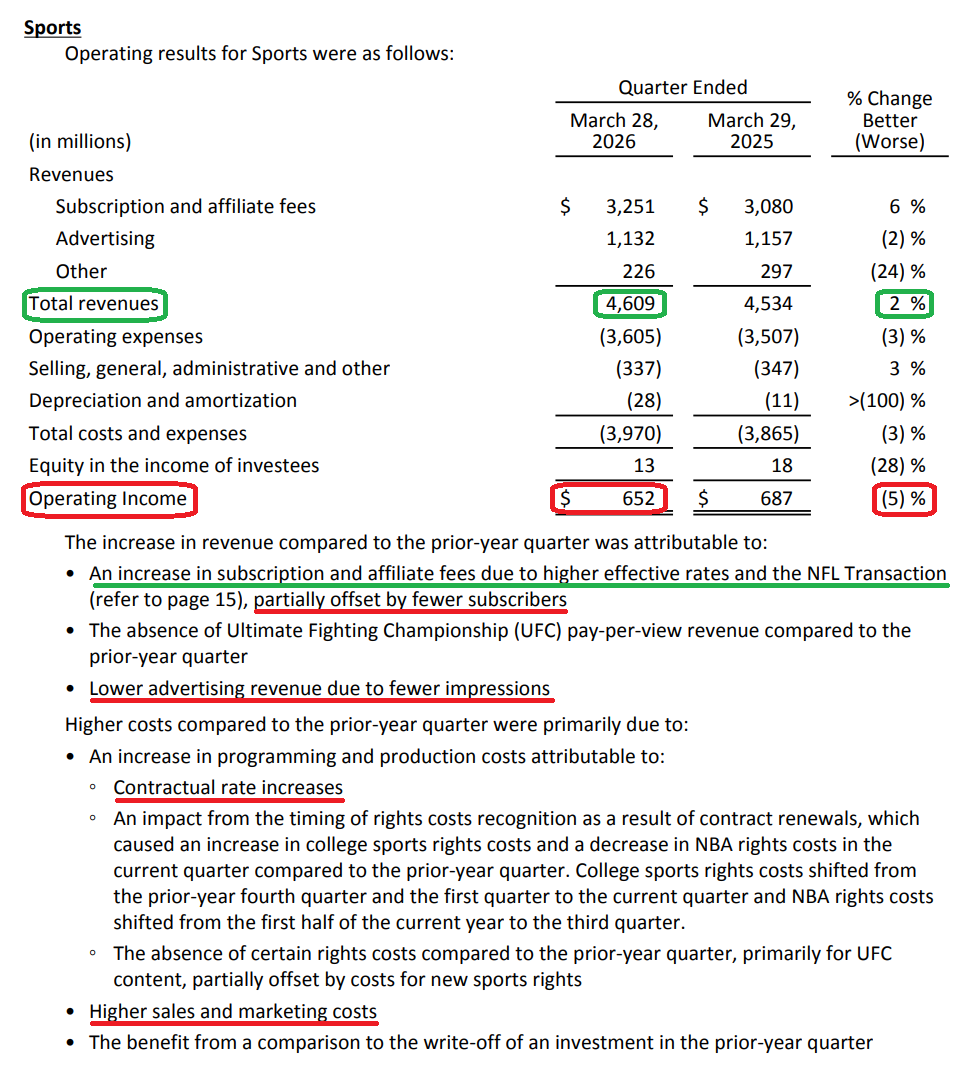

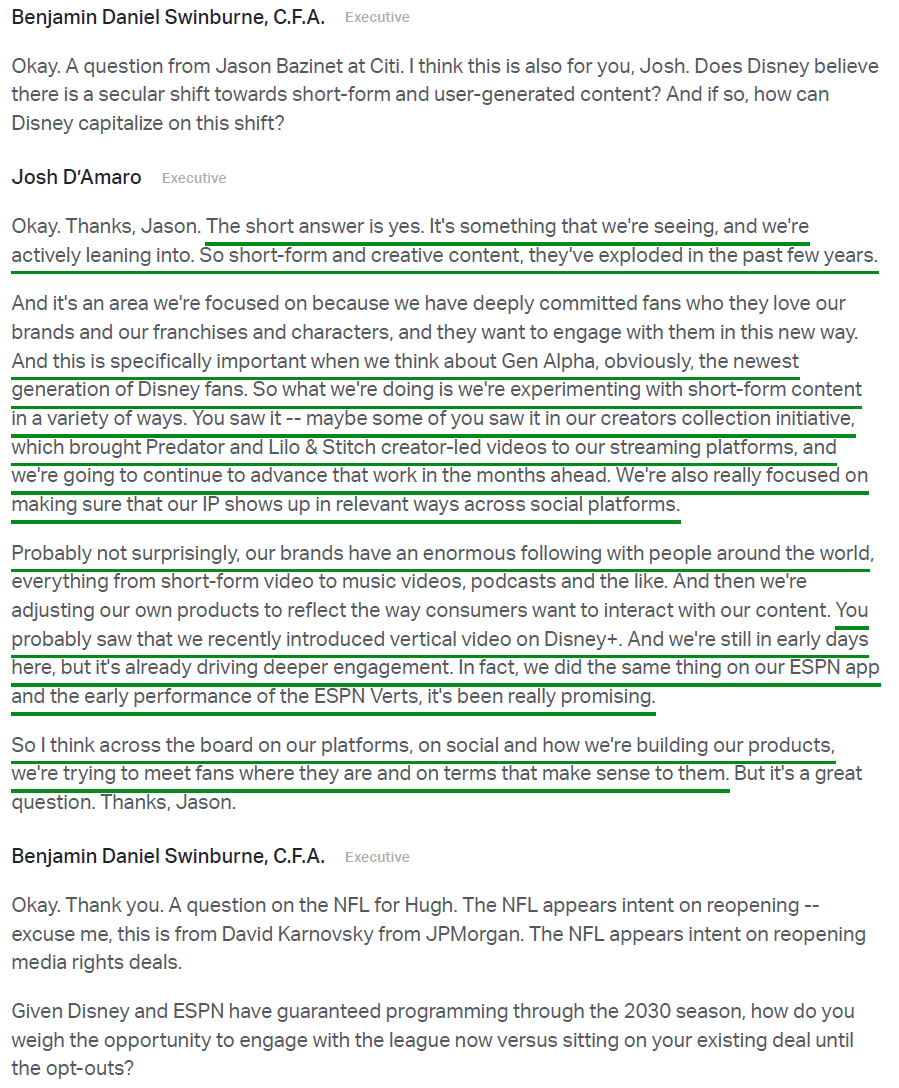

5) Sports revenue increased 2% Y/Y to $4.61B (vs. $4.59B consensus), driven by 6% growth in subscription and affiliate fees, with the NFL transaction contributing 3 percentage points, partially offset by a 2% decline in advertising revenue due to fewer NBA games and the lapping of last year’s 4 Nations hockey tournament. Despite the top-line growth, segment operating income declined 5% Y/Y to $652M, though well ahead of the $588M consensus estimate, as higher programming and rights costs, including timing-related shifts in NBA and college sports rights recognition, weighed on profitability. Q3 Sports operating income is guided down ~14% on continued programming cost timing, but full-year Sports operating income is now expected to grow by mid-single digits, including the NFL deal, up from prior low-single-digit guidance. ESPN remains the #1 sports media brand in the U.S. and captured the largest share of linear sports consumption among total viewers during the quarter, with ESPN’s first-ever Super Bowl broadcast in February 2027 already drawing strong advertiser demand. Most importantly, while still early following the launch of ESPN Unlimited less than a year ago, the direct-to-consumer strategy continues to gain traction, with digital subscriber revenue in Q2 more than offsetting secular declines in the linear subscriber universe.

6) Disney’s film slate continues to fire on all cylinders, with management highlighting excitement around the upcoming releases of The Devil Wears Prada 2 and Toy Story 5 on the earnings call, both of which have since delivered. The Devil Wears Prada 2 has now generated $678M at the global box office, while Toy Story 5 opened to $312M worldwide, marking the biggest movie debut of 2026, and has since grown to $594M globally. Beyond the box office, these releases continue to fuel Disney’s content flywheel across streaming, consumer products, and Experiences, with Zootopia 2 serving as a prime example after generating $1.9B at the global box office and surpassing 1 billion hours streamed on Disney+ since arriving on the service in March. Looking ahead, the upcoming slate is as strong as it has been in years, with major releases including the live-action Moana (July 10), Avengers: Doomsday (December 18), and Ice Age: Boiling Point (February 5) all on deck.

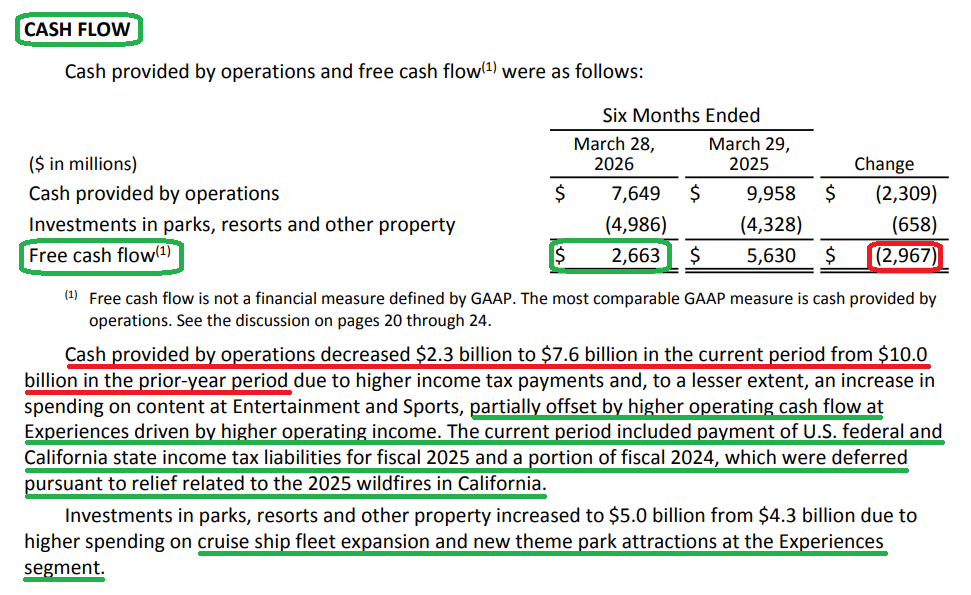

7) Operating cash flow remained strong, with Q2 cash from operations of $6.91B (+2% Y/Y) and year-to-date operating cash flow of $7.65B versus $9.96B in the prior year period. Free cash flow totaled $4.94B (+1% Y/Y) for the quarter, while year-to-date free cash flow came in at $2.66B versus $5.63B last year. The year-over-year decline was driven primarily by higher tax payments related to previously deferred California wildfire relief liabilities catching up, along with increased investment across the Experiences segment. For FY26, management continues to expect operating cash flow of ~$19B and free cash flow of ~$10B, translating to a 5.8% free cash flow yield at current prices.

8) Capex during the quarter totaled $1.97B, bringing year-to-date spending to $4.99B (+15% Y/Y) and keeping the company on track for ~$9B in FY26. The bulk of that investment is earmarked for cruise fleet expansion and new attractions across Walt Disney World, Disneyland, and Shanghai Disney Resort, with more projects underway around the globe than at any point in Disney’s history. Disney also continues to pursue additional capital-light expansion opportunities, including a new cruise ship partnership in Japan and the Disneyland Abu Dhabi resort alongside partner Miral. Most importantly, returns on invested capital within the Experiences segment remain highly attractive and continue to lead the company across all segments.

9) Management raised its full-year share repurchase target to at least $8B, up from $7B previously, representing ~4.7% of the company’s current market cap. Disney has already repurchased $5.5B of stock during the first half of the fiscal year, and when combined with its $1.50 annual dividend (~1.6% yield), total shareholder yield now stands at ~6.3%.

10) Management reiterated confidence in its full-year outlook, continuing to expect ~12% adjusted EPS growth for fiscal 2026 excluding the 53rd week, or ~16% including it, while maintaining expectations for double-digit adjusted EPS growth in fiscal 2027. Despite ongoing macro uncertainty, management stated that demand across its domestic parks and resorts remains healthy, with no meaningful changes in consumer behavior observed thus far and attendance trends expected to improve during the second half of the year.

Earnings Call Highlights

Morningstar Analyst Note

General Market

The CNN “Fear and Greed Index” ticked up to 30 this week from 28 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

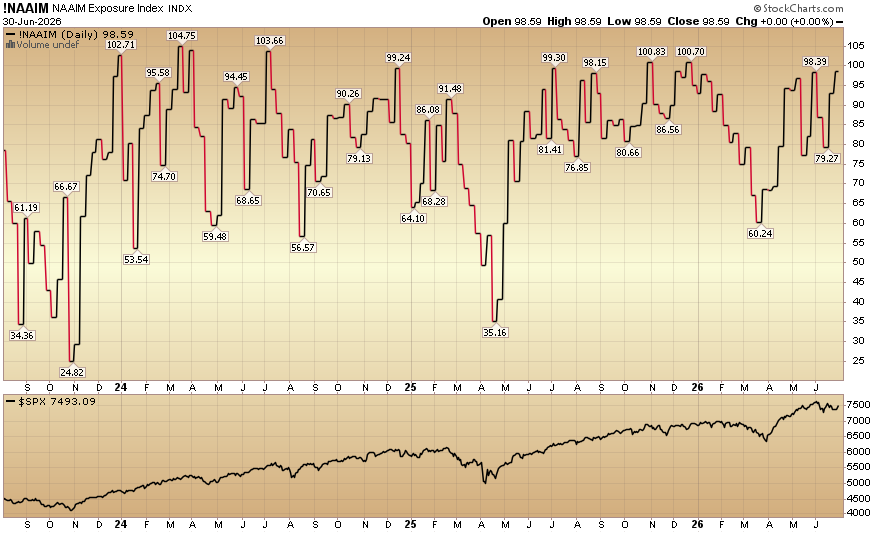

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) ticked up to 98.59% equity exposure this week from 79.27% last week.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Comments

Log in or sign up to join the conversation.