TACO Tuesday?

Financial markets are oscillating in a narrow, uneasy range as traders sized up the countdown to Donald Trump’s Iran deadline, with tentative ceasefire optics offering brief relief but never fully offsetting the lingering risk of escalation.

Brent crude gave back early gains to hover just below $110 a barrel, reflecting a market still trading on access risk rather than outright disruption, as volatility held firm into Tuesday's 8 p.m. Eastern cutoff. US equity index futures clawed back initial losses to sit largely unchanged, a signal of positioning restraint rather than conviction.

Across Asia, equities leaned cautiously higher, with the MSCI Asia Pacific Index up 0.7%, led by South Korea as technology names carried the tape. Stocks perceived as insulated from the Middle East fallout outperformed, with Samsung Electronics (SSNLF) gaining 1.5% after reporting a sharp profit surge, reinforcing the market’s selective bid for earnings resilience amid geopolitical noise.

On Monday, the tape drifted through the long weekend vacuum with Europe offline and liquidity stretched thin, yet the market refused to fracture. Instead, it leaned into the absurdity of it all, balancing between relief and risk as if both outcomes were already partially priced. Stocks, bonds, and crude all edged higher, not on conviction but on the absence of panic, while gold and the dollar stood motionless, waiting for a signal that never quite arrived. It had the feel of a market trading shadows rather than substance, where every headline is both credible and dismissible at the same time.

TACO Tuesday again? Turmoil returns or troubles terminated? For now, the rhetoric has tightened, the threats sharpened, and yet the market is not capitulating, conditioned by repetition to expect de-escalation just before the edge. This is no longer disbelief; it is learned behaviour. Traders are no longer reacting to what is said, but to when it is usually walked back. Time, not language, has become the anchor.

But this time the backdrop carried a different tone. The sudden appearance of the Boeing (BA) E-4B Nightwatch drifting into operational visibility cut through the noise like a low-frequency signal the market could not ignore. This is not a trading headline; it is a system-level contingency asset designed for scenarios where command continuity matters more than optics. Its presence does not confirm escalation, but it changes the distribution of outcomes. The market does not need certainty; it only needs to widen the tails.

Oil picked up on that shift first, as it always does. The barrel is no longer trading flows; it is trading access, and access is binary. Crude firmed into the Asia open while equity futures hesitated, the divergence subtle but telling. When geopolitical risk shifts from rhetoric to readiness, oil transitions from narrative to mechanism. It stops reflecting probability and starts embedding consequence.

Equities, for now, are still dancing to the squeeze. Another short-covering wave pushed small caps higher, while the Nasdaq (QQQ) edged higher on selective strength, but the move lacked depth. This is not fresh buying, it is positioning repair. The Dow (DIA) lagged, caught between cyclical sensitivity and a macro backdrop that refuses to clarify. Underneath, the market still cannot reconcile growth resilience with rising cost pressure, and that tension is what keeps rallies shallow and fragile.

The macro data did nothing to resolve that tension. The services print reinforced the stagflation undertone, with prices accelerating even as hiring cools and demand holding just enough to prevent a clean slowdown. It is the kind of data that traps policy in a feedback loop. The Fed is not being guided; it is being cornered, forced into a reactive stance where every decision depends on what breaks first, inflation or growth.

Rates reflected that paralysis with quiet precision. The curve flattened, front-end sensitive to inflation risk, while the long end stayed anchored by the belief that policy will eventually contain inflation. For now, credibility holds. Long-term expectations remain stable, suggesting the market still trusts the Fed’s ability to navigate the corridor. But that trust is conditional, and oil is the variable that tests it.

Positioning is the wild card. Systematic flows that were forced out are now close to flipping back in, setting the stage for a reflexive rally if the geopolitical tone softens. But the presence of tail risk, now reinforced by visible contingency signalling, keeps discretionary money cautious. This is a market that wants to buy, but does not yet trust the ground beneath it.

So the tape holds in that uneasy equilibrium. TACO behaviour pulls one way, the doomsday circuit breaker pulls the other. Relief is expected, but escalation is no longer dismissed. And in that gap between expectation and possibility, volatility waits.

Coin Flip Time Squeeze Or Fade. ( Charts via The Market Ear)

Squeeze Or Fade.

The market has reached that familiar inflexion where price stops being a function of news and starts becoming a function of positioning. The flush has already done its work, weak hands cleared, leverage reset, and now the tape is leaning into resistance with just enough momentum to force the question every trader knows is coming. This is no longer about direction; it is about reaction. Squeeze or fade.

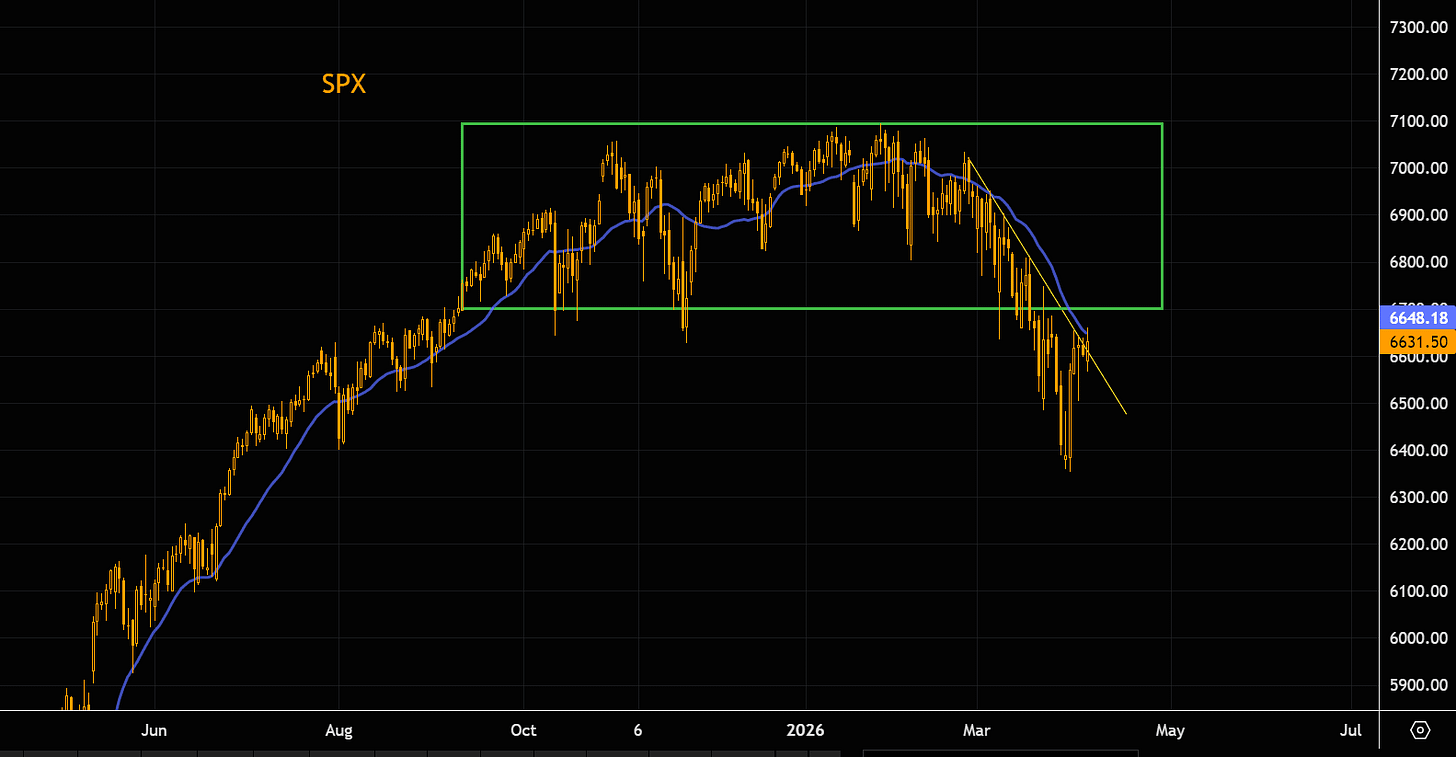

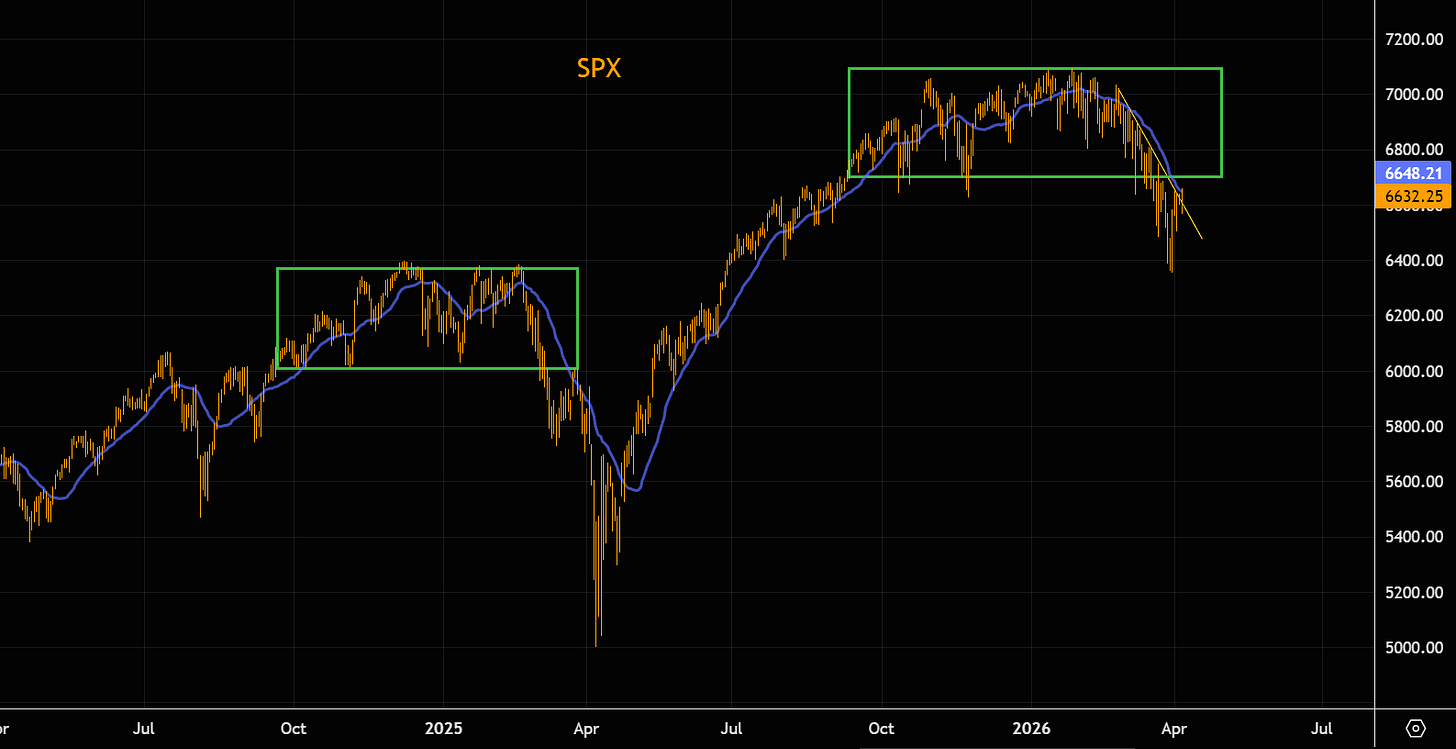

The S&P (SPY) is pressing against the underside of its own narrative, nudging above the downtrend and probing the 21-day moving average like a lock that may or may not give. A clean break higher does not just signal strength; it forces it, because above these levels, the market stops being discretionary and starts becoming mechanical. But the ceiling is not theoretical. The 6700 futures zone sits there like a pressure plate, a level that has rejected prices before and will demand real conviction to break. This is where rallies either accelerate or suffocate.

Source: LSEG Workspace

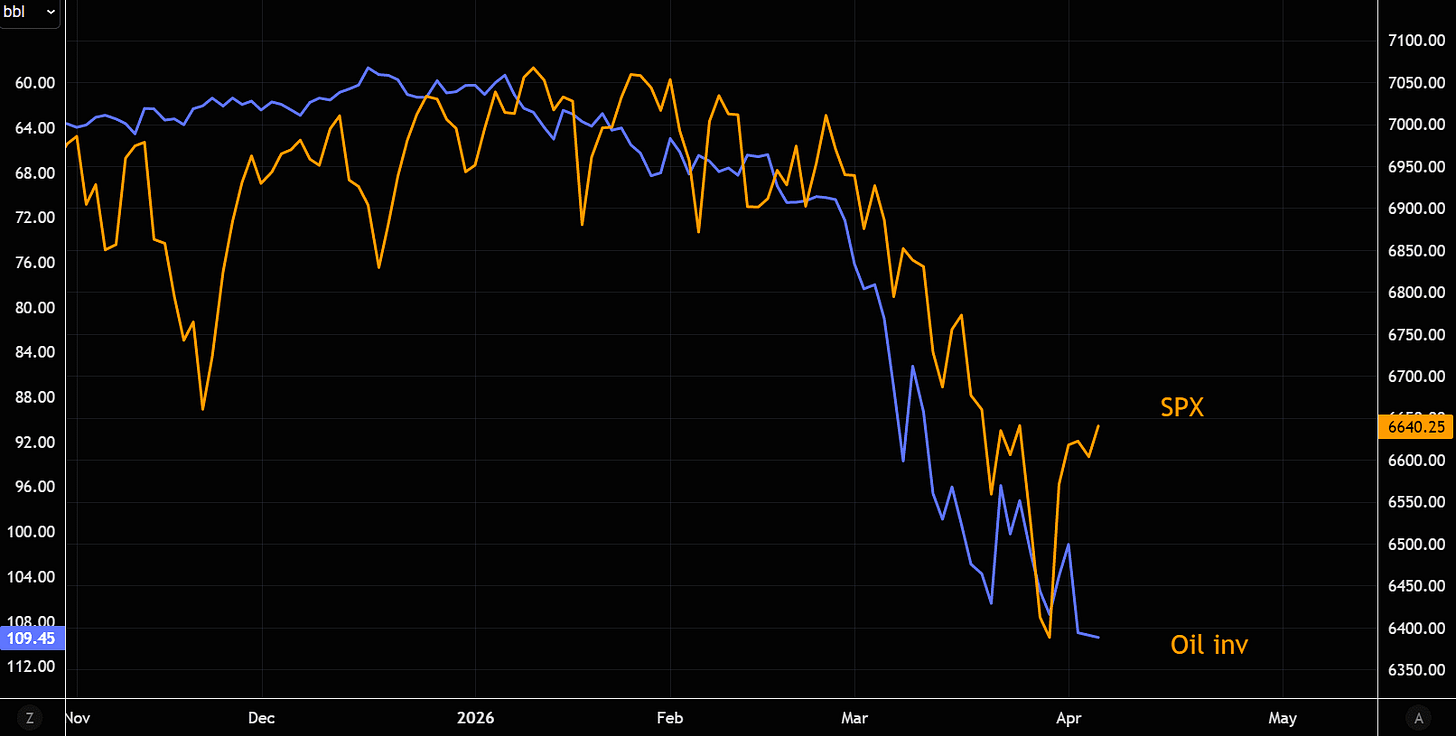

What makes this moment more nuanced is the shifting relationship with oil. Since the Iran conflict began, equities have traded like a derivative of crude, every tick in the barrel echoing through risk assets. Now that the linkage is starting to loosen. Equities are inching forward while oil remains pinned near extremes, and that divergence is the market asking a deeper question. Do you trust forward-looking equities discounting resolution, or do you trust a commodity still pricing constraint? One is anticipating relief, the other is embedding risk. This is the coin flip !!!!

Source: LSEG Workspace

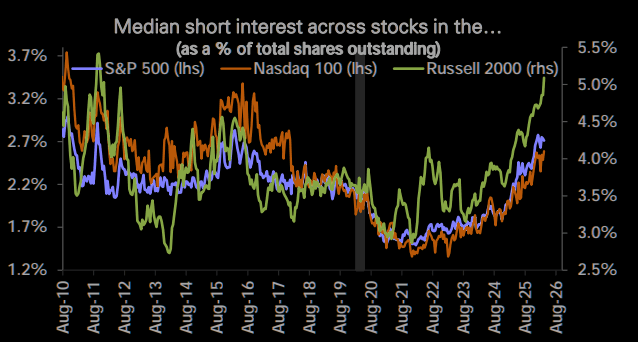

Underneath the surface, the short base is quietly rebuilding. Not the fast money, not the day traders, but the broader structural short that accumulates over time when conviction fades, and uncertainty lingers. The Russell (IWM) in particular has become the expression of that view, a pressure point that does not matter until it suddenly does. Because when positioning builds in size, it does not unwind gradually. It snaps.

Source: DB

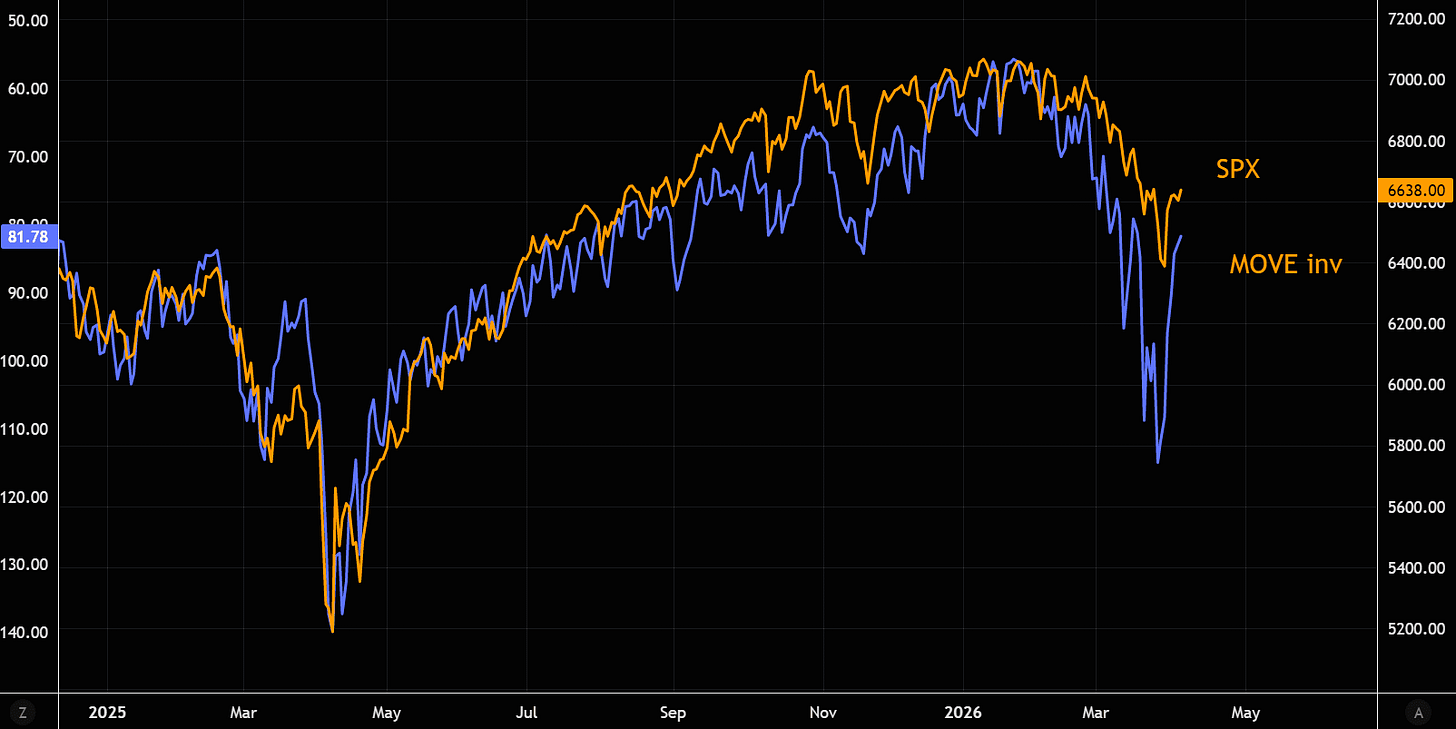

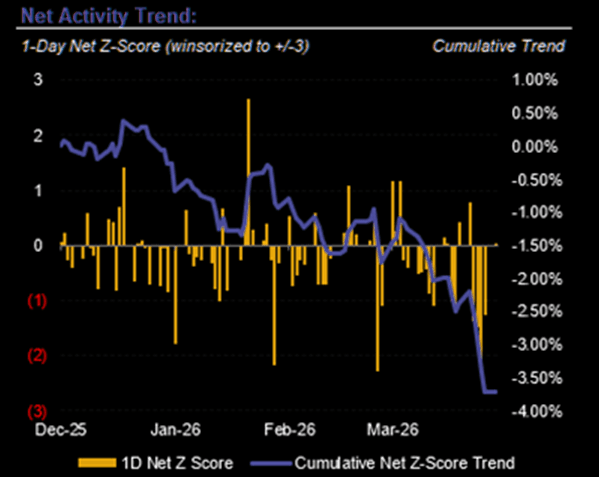

That snap risk is being reinforced by the rates complex. The equity market has always been sensitive to bond volatility, and right now that signal is flashing again. As the MOVE index compresses, the cost of uncertainty falls, and with it the barrier to re-risk. Lower volatility in rates is not just a macro signal; it is a mechanical trigger. It invites systematic flows back into equities, and those flows do not wait for confirmation. They anticipate it.

Source: LSEG Workspace

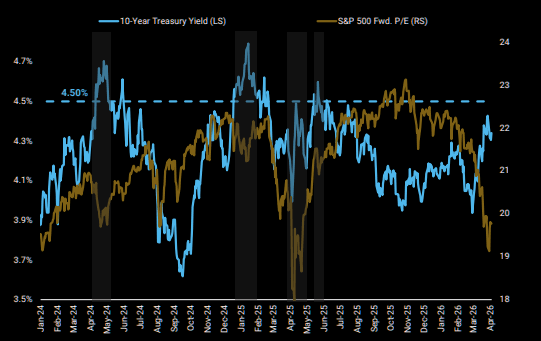

At the same time, the 10-year yield is hovering around a level that carries real consequences. The 4.5 per cent zone has historically acted as a fault line where valuation begins to compress and multiples lose oxygen. Stay below, and equities can breathe. Break above, and the entire framework tightens. This is not an abstract threshold. It is where duration starts to matter again.

Source: MS

And yet, markets rarely bottom on comfort. They bottom on improvement at the margin, when the rate of deterioration slows before the data itself turns. That dynamic is beginning to whisper through the tape. The worst of the selling in mega-cap tech may already be behind us. The magnitude of the recent unwind ranks among the largest on record, yet forward earnings remain intact. That creates a gap, and markets have a habit of closing gaps when positioning becomes too one-sided.

It is this disconnect that makes the current setup so potent. Exposure is low, sentiment is fragile, but the earnings engine is still running. In other words, the fuel is there, but the confidence is not. And when those two drift too far apart, the resolution tends to be violent.

Source: LSEG Workspace

But there is a catch. The pattern is familiar. Almost too familiar. The path the market is tracing echoes last year’s sequence, right down to the bounce that followed the initial selloff. And markets that feel familiar often betray that familiarity. Because when everyone sees the same setup, positioning leans the same way, and that is when the tape chooses the opposite.

Comments

Log in or sign up to join the conversation.