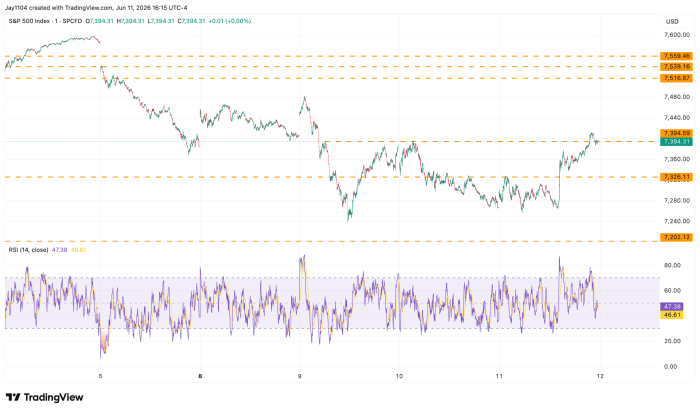

Stocks finished the day higher following some late-breaking news on the Middle East conflict. Headlines come and go, and whether this latest development has any lasting impact remains to be seen.

The most notable aspect of today’s rally is that it effectively took the S&P 500 back to yesterday’s highs, where it ultimately closed.

One could easily argue that because the market largely looked through the war the entire time, there is little reason for stocks to rally on this news. If the market had already priced in the conflict and its potential outcomes, then today’s move may simply reflect a shift in positioning rather than any meaningful change in fundamentals.

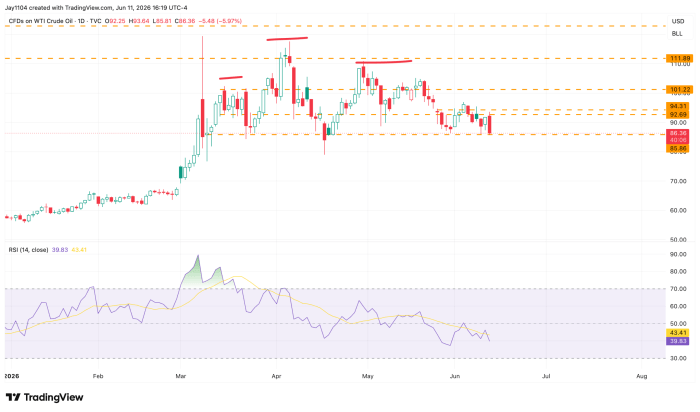

Oil also fell on the day, dropping back to support around $86 in WTI. That support level has been tested numerous times and continues to hold. Perhaps there is a fundamental reason for that, or perhaps there is not. Either way, that has been the pattern for quite some time now.

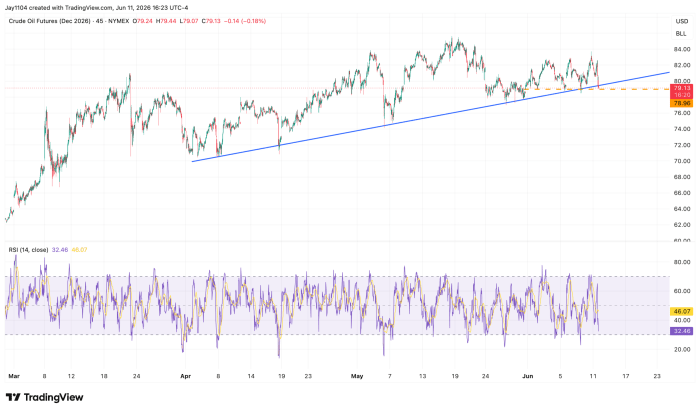

Perhaps more importantly, December WTI continues to trade around $80 and was down on the day, but not by as much as the front-month contracts. This suggests that while near-term supply concerns may be easing, the market continues to price in relatively elevated oil prices further out on the curve.

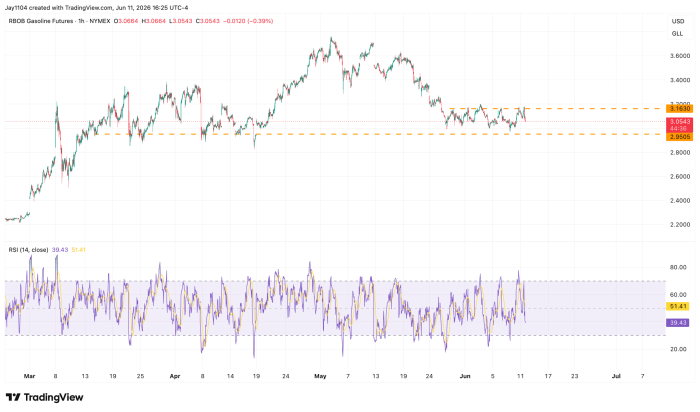

Meanwhile, gasoline prices barely fell.

Oil and gasoline prices remain choppy, with neither breaking support nor resistance in any meaningful way. That suggests that even if the war is over and the Strait reopens, oil may still be priced at a higher overall price level.

To achieve the disinflation needed to bring CPI all the way back down below 3%, oil and gasoline prices will need to fall. Otherwise, month-over-month inflation rates may slow, but the year-over-year rate of change will likely remain above 3% through the end of 2026 due to base effects.

The Fed probably does not need to raise rates, but I think it would be hard for them to cut rates.

Something to think about.

Comments

Log in or sign up to join the conversation.