Stocks finished the day lower, with the S&P 500 falling by more than 1.6%. The move came despite a CPI report that was largely in line with expectations. The only notable surprise was core CPI, which rose by 0.2% month over month, slightly below estimates of 0.3%. The drop in the market likely had little to do with the CPI report and more to do with the rising tension in the Middle East.

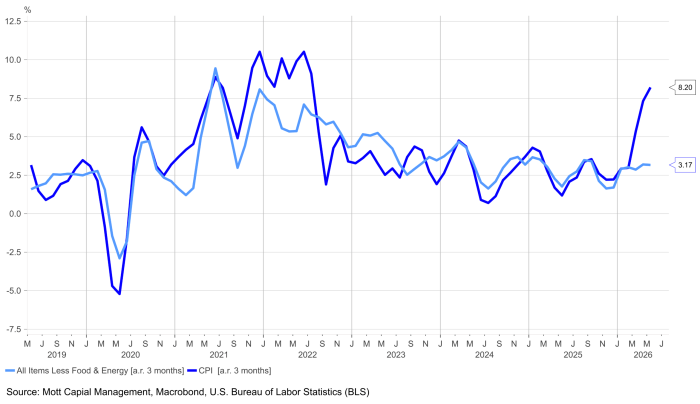

The bigger takeaway is that headline inflation has been running at more than an 8% annualized rate over the past three months, while core CPI has been running at roughly a 3.2% annualized pace. That suggests underlying inflation pressures remain elevated, even if the monthly data did not deliver any major surprises.

Looking at CPI swaps for June is probably still a bit premature, but for now, the market is pricing year-over-year inflation at around 4%, which would actually be a modest improvement. However, we are only midway through the month, and gasoline prices have been declining until recently.

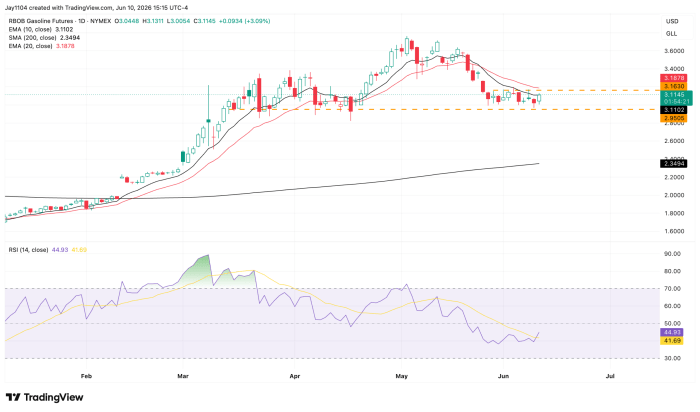

Today, gasoline prices rose by roughly 3%, with RBOB reaching resistance at its 10-day exponential moving average. If gasoline prices continue to move higher from here, I would expect inflation swaps to begin pricing in higher headline inflation readings as well.

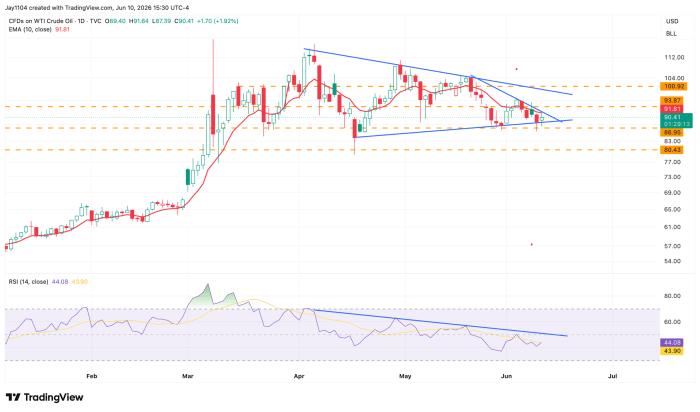

Where inflation goes from here will largely depend on what happens to gasoline and oil prices. Right now, tensions in the Middle East are escalating again, and oil prices are rising. Not by much, but the chart remains bullish in my view, and I still think oil ultimately heads higher over time.

For now, oil appears to be consolidating just below its 10-day exponential moving average in what looks like a triangle pattern. A breakout from that formation could signal the next leg higher and potentially put a move back above $100 per barrel into play.

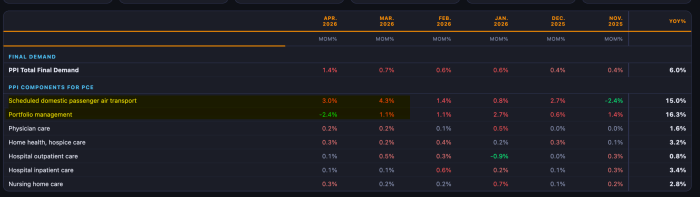

Tomorrow brings the PPI report, and there are a few components the market is likely to focus on more than others—namely, those that feed directly into the PCE report. One of the most important will be portfolio management fees.

Given the stock market’s sharp rally in April and May, there is a good chance that strength could show up in portfolio management fees. Because those fees feed into the PCE calculation, a strong upside reading could have implications for future PCE inflation readings, which is why the market will be paying close attention.

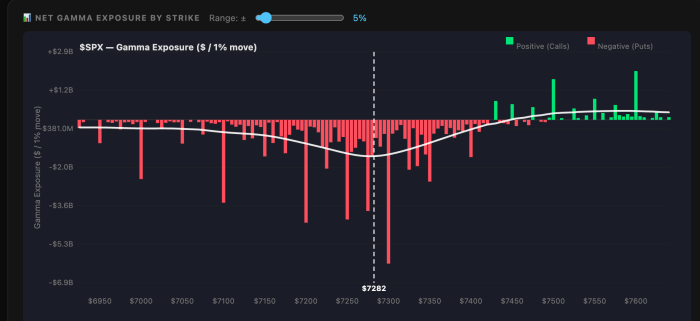

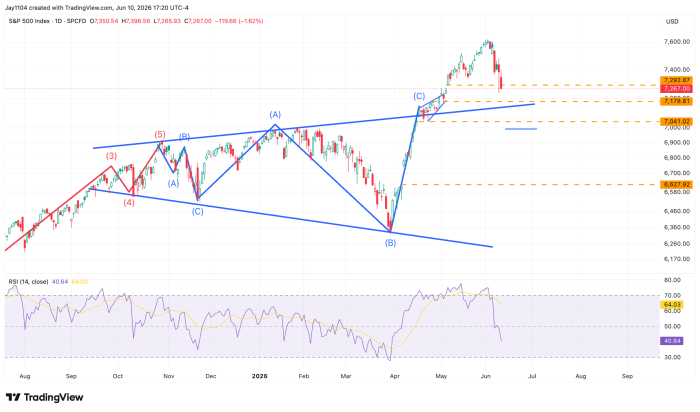

As for the S&P 500, it has closed below the 7,300 put wall, which could allow the index to move lower toward 7,200. That does not necessarily mean the market will decline, but it does open the door for further downside from here.

Things could start to get interesting for a couple of reasons. One is that the next technical support area comes in around 7,170. Additionally, the rising trend line that formed the upper boundary of the megaphone pattern I wrote about a few months ago, when the market was first breaking out, is coming back into play and could create what would be considered a throwover.

It will be something to watch, especially if we eventually break below 7,200.

The ECB meets tomorrow and is expected to raise rates by 25 basis points, taking the deposit rate to 2.25% from 2.0%. Markets are also pricing in another 25-basis-point hike in September.

The focus, however, will be less on tomorrow’s rate increase and more on the timing and likelihood of that second hike. Investors will be paying close attention to how Christine Lagarde frames the policy outlook and whether her comments reinforce expectations for further tightening later this year.

Comments

Log in or sign up to join the conversation.