There are signs of divergence in the platinum and palladium markets as investors remain bullish on platinum, while bearish sentiment appears to be taking control of the palladium market.

Both platinum and palladium have given up a substantial percentage of their 2025 gains in the recent correction. Platinum is down 36 percent to around $1,600. Meanwhile, palladium has fallen 38 percent and is trading around $1,230 an ounce.

Both metals have seen a decline in investor participation over the last few months, including in the demand for CME, GFEX, and exchange-traded products.

Metals Focus analysts noted that while the price action “remains firmly within the broader precious metals sell-off,” there appears to be growing divergence between the two markets. This is most apparent in futures trading.

While investors have reduced exposure to platinum, they have generally maintained “a constructive stance,” but there are signs of bearishness in the palladium sector.

According to Metals Focus, the divergence has become more obvious over the last two months. Investors have steadily rebuilt short positions in palladium futures. After a brief return to net longs in early 2026, managed money positions in palladium reverted to net shorts in March and have since become progressively more bearish. Metals Focus analysts said, “By early June, net shorts exceeded 400koz for the first time since October last year, although positions remain well below the elevated short levels recorded during 2024–25.”

Platinum also charted a decline in investor interest, following gold and silver lower. However, Metals Focus analysts said the bearish sentiment has been much less pronounced and was primarily driven by a reduction in net long positions. While the number of short positions increased at the same time, the action was much less dramatic than in the palladium market. In fact, platinum has maintained a net long position throughout this period.

Supply and Demand Dynamics

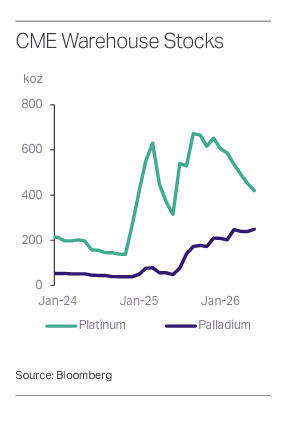

Tariff worries have had a significant impact on both platinum and palladium. Significant amounts of metals flowed into the U.S. as tariff concerns mounted. Platinum inventories in CME vaults increased by 142 percent last year. Meanwhile, palladium inventories rose from 39,000 ounces to 210,000 ounces, a 445 percent increase. Inventories of both metals remain elevated today.

This displacement of metal led to localized shortages and helped drive the price of both platinum and palladium higher last year.

Tariff concerns have eased, and it appears investors were beginning to adjust to the new normal as the broader precious metals market came under pressure due to the Iran conflict and elevated inflation concerns.

As Metals Focus put it, “What began as a physical market dislocation gradually evolved into a broader investment theme.”

“Futures positioning expanded, ETP holdings rose, and GFEX introduced a new pool of speculative liquidity in late 2025. By January 2026, both metals had become part of the wider precious metals rally. When sentiment turned towards precious metals after the Iranian conflict, which led to a dramatic shift in interest rate expectations, causing both platinum and palladium to correct sharply.”

However, the unwind has not been uniform.

“Platinum positioning recovered after periods of stress and remained positive by mid-June. Palladium briefly improved before deteriorating steadily through May and June. This suggests investors are not exiting the PGM complex indiscriminately. Instead, they are increasingly differentiating between a platinum market that retains a base of support and a palladium market facing more immediate challenges from weaker demand expectations and stronger secondary supply.”

Much like silver, the platinum market faces a structural deficit with demand outstripping mining and recycling supply.

In 2025, the platinum market ran its fourth straight market deficit, with demand outstripping supply by a record 1.08 million ounces. Looking ahead, the World Platinum Investment Council projects modest market deficits this year with supply shortfalls running in the 300-400k range through 2030.

Policy Changes Impacting Platinum and Palladium Markets

According to Metals Focus, several policy changes created headwinds for palladium. The EPA announced it would delay Tier 4 vehicle emissions standards by two years. According to analysts, this will have a more significant impact on the palladium market because of its heavier exposure to gasoline auto-catalyst demand.

Around the same time, the U.S. International Trade Commission ruled that Russian palladium imports do not “materially injure” U.S. industry, removing the prospect of additional trade restrictions.

“The USITC decision was not bearish in the conventional sense, but it removed a potential upside risk. As investors reassessed demand expectations, the absence of additional restrictions on Russian palladium imports reinforced the view that the market may be more adequately supplied than previously assumed.”

There has also been increased recycling activity for both metals. However, it has been more pronounced in the palladium sector.

Finally, Metals Focus noted that platinum demand enjoys a broader base, with jewelry and other industrial applications adding to offtake.

Metals Focus summarized the divergence between the two metals, asserting, “In effect, platinum investment has lost some momentum, while palladium has lost more conviction.”

The question is whether a price divergence will follow this divergence in market activity.

“For now, platinum and palladium have corrected at a similar pace. However, the market is increasingly expressing different views on their respective fundamentals.”

Comments

Log in or sign up to join the conversation.