GXO (GXO) Update

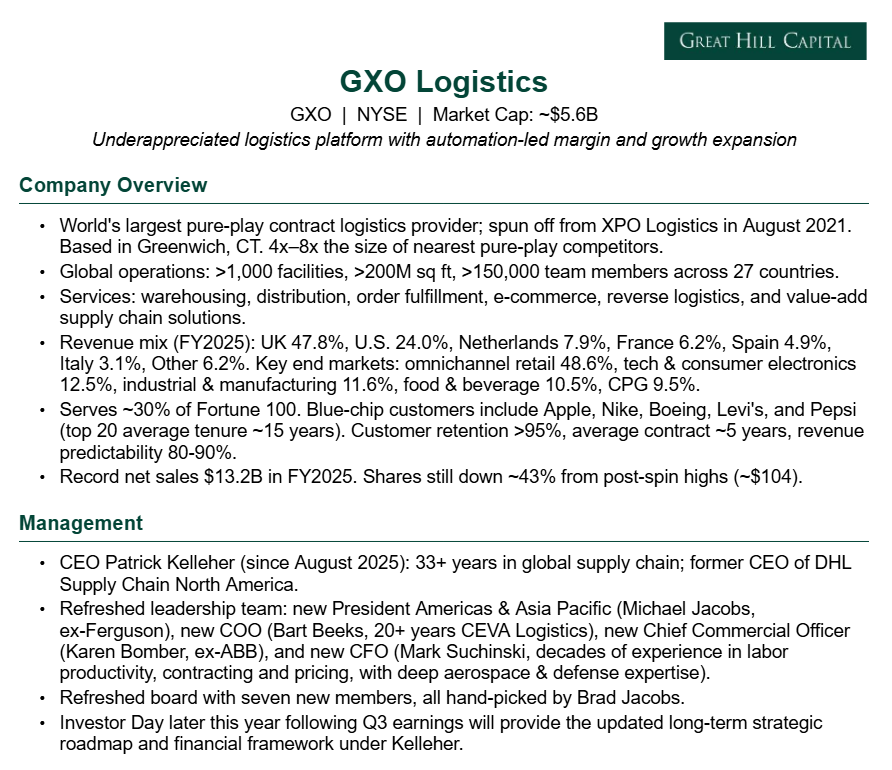

For newer readers, here’s a quick overview of the key drivers behind our thesis on GXO, the world’s largest pure-play contract logistics provider and one of the cleanest ways to play the restocking cycle against a backdrop of powerful secular tailwinds:

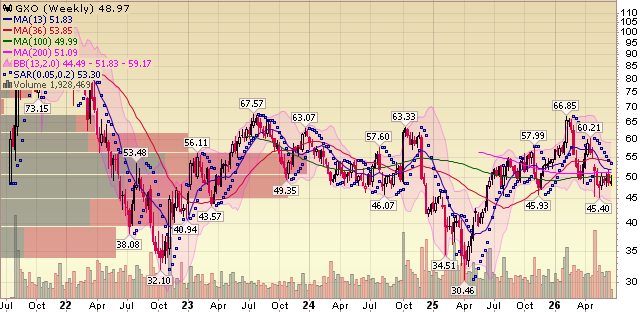

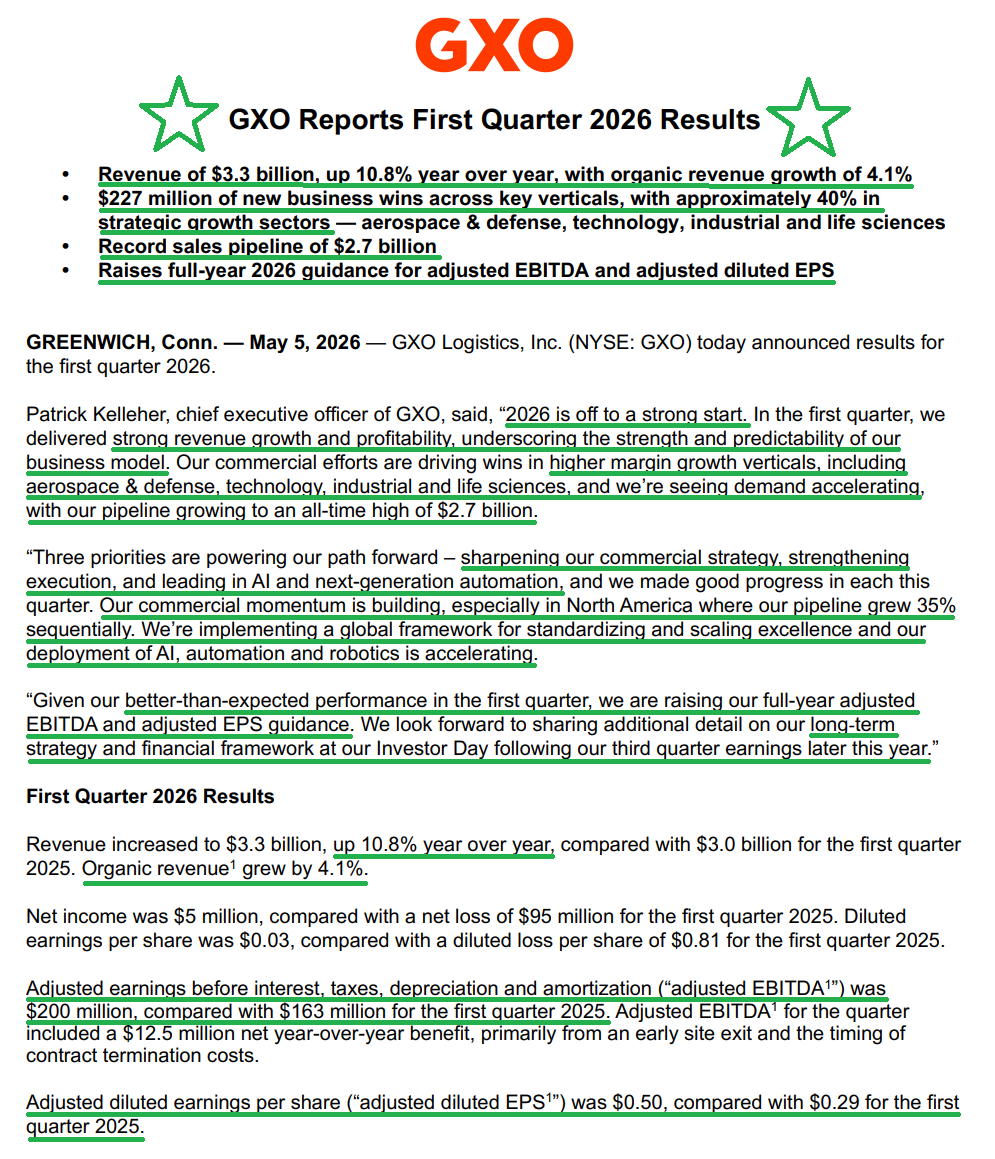

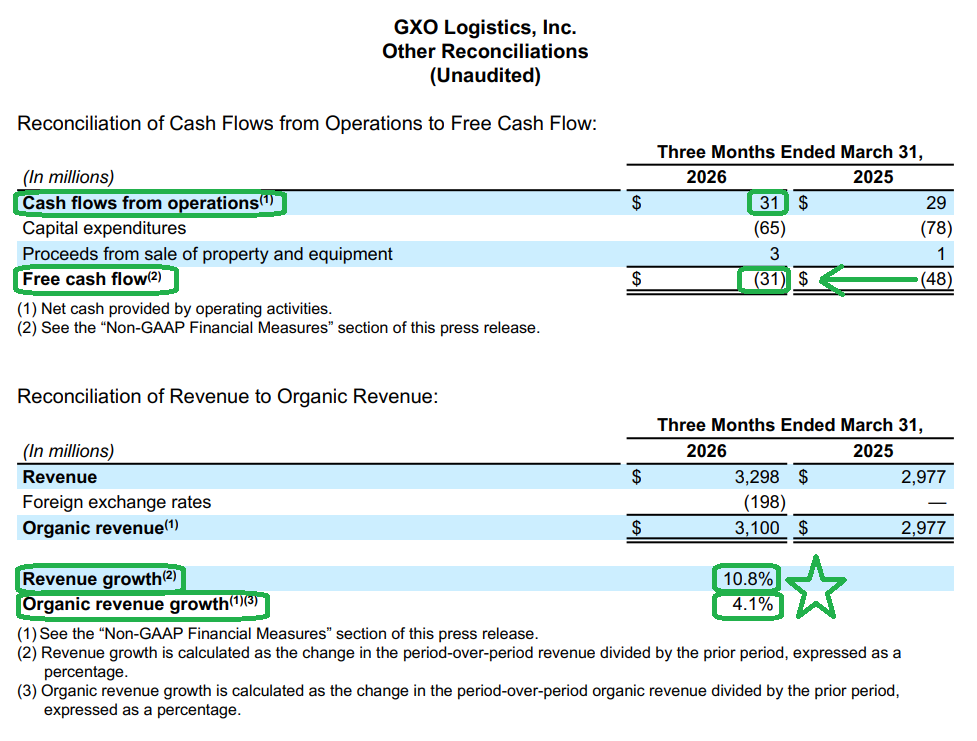

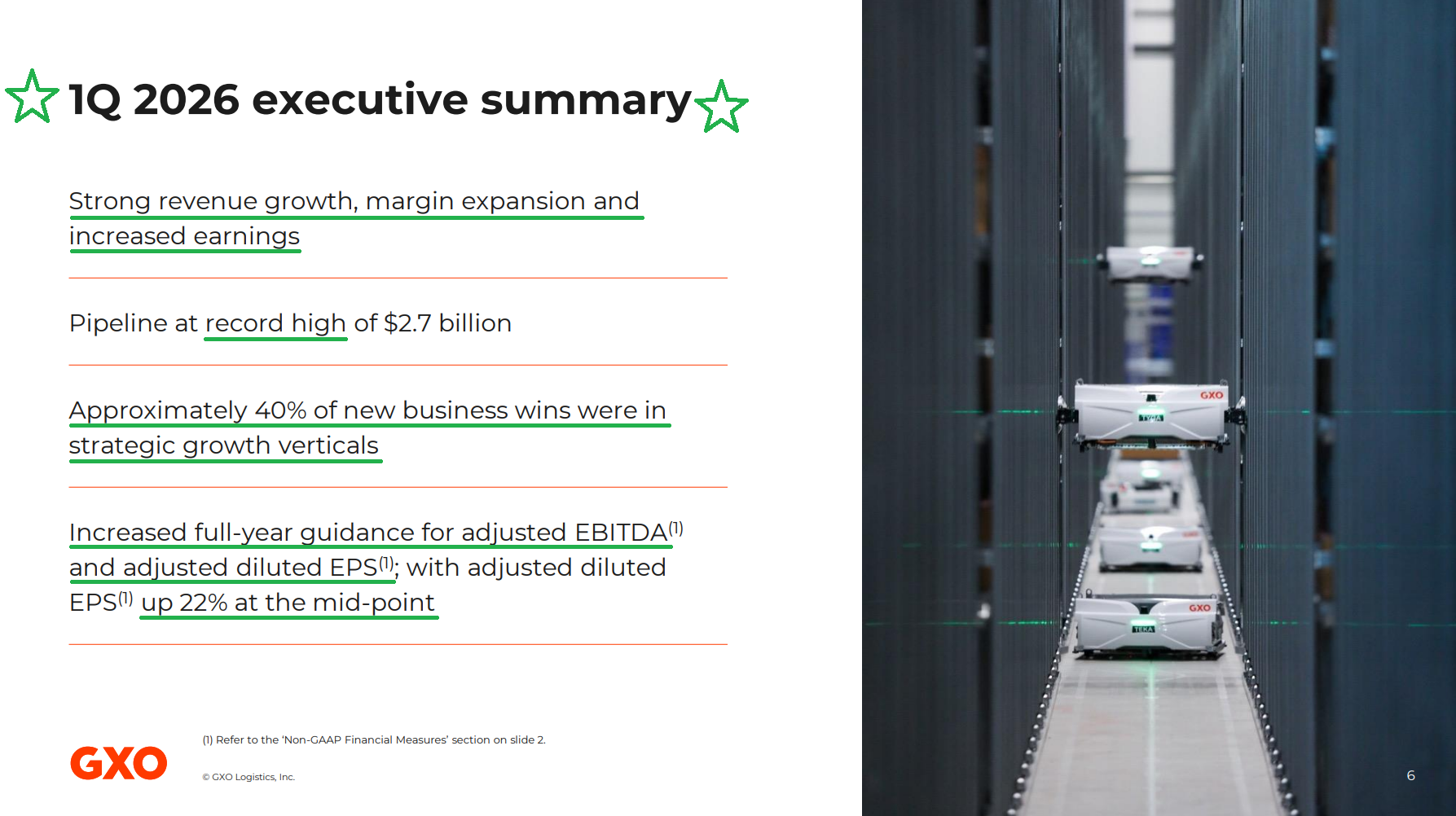

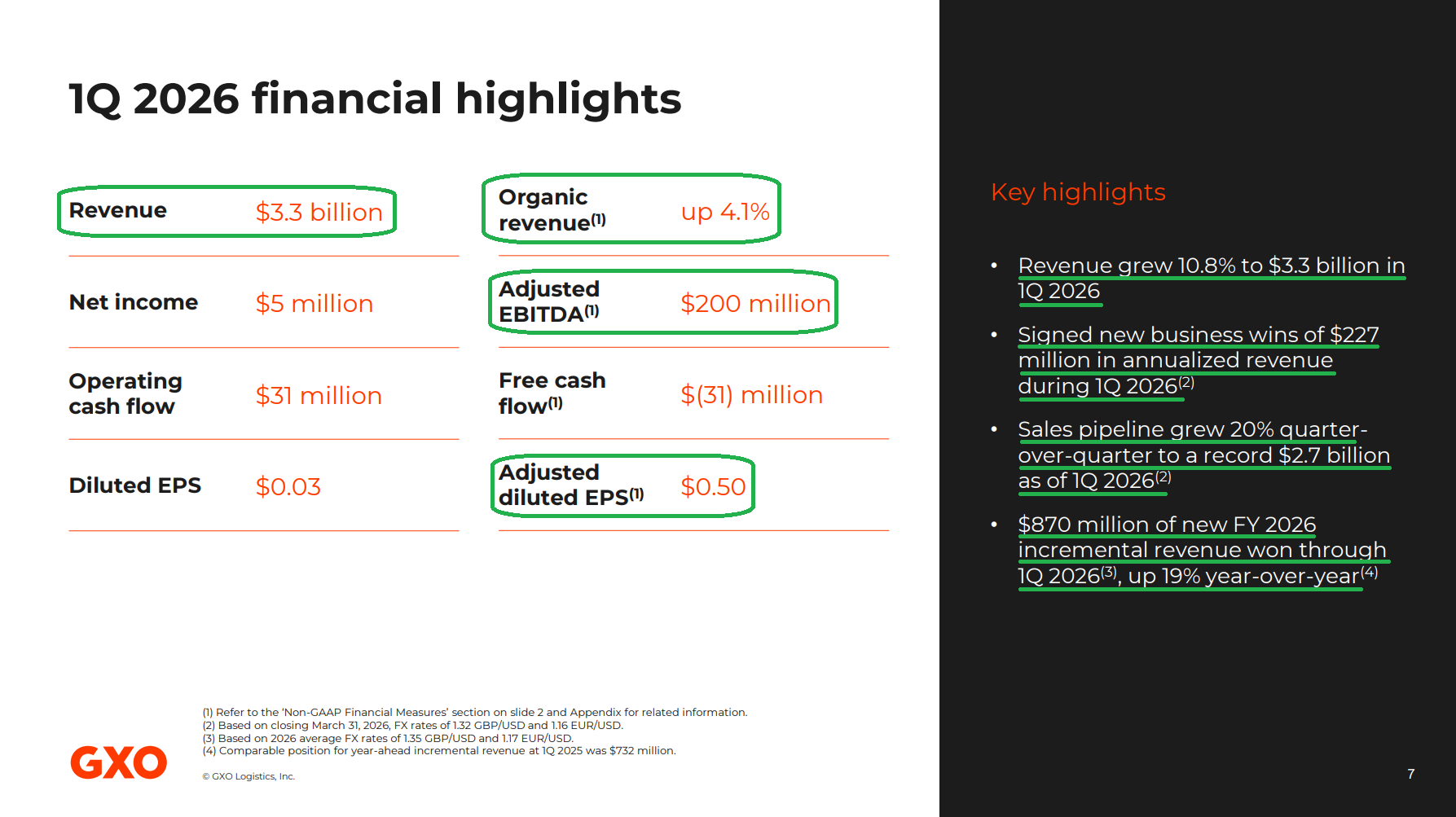

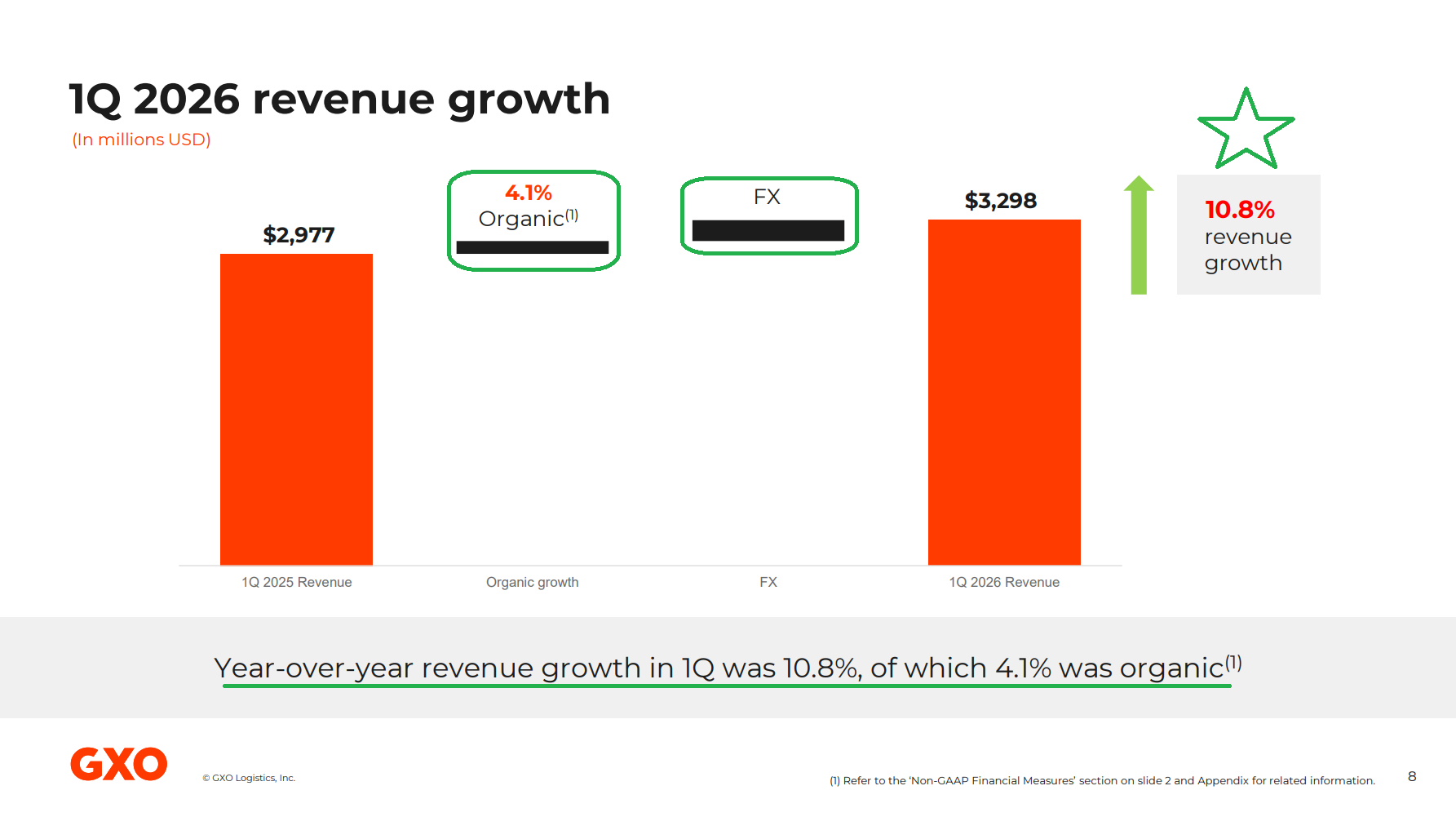

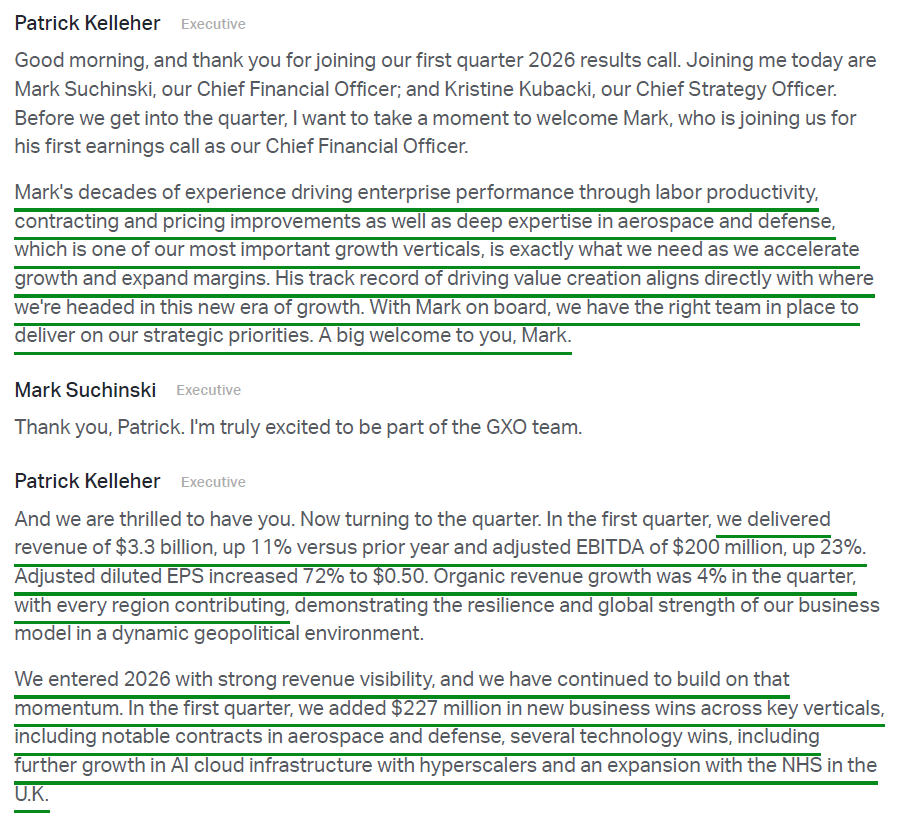

GXO kicked off 2026 on the right foot, posting a strong first quarter that beat expectations across the board. Revenue of $3.3B (+10.8% Y/Y) topped consensus by ~$80M, with the all-important organic growth figure accelerating to +4.1% from +3.5% in Q4 as every region contributed. Adjusted EBITDA of $200M (+23% Y/Y) came in ~$20M ahead of consensus, with margins expanding 60 bps to 6.1% and helping drive adjusted EPS of $0.50 (+72% Y/Y), well ahead of the $0.37 the Street was looking for.

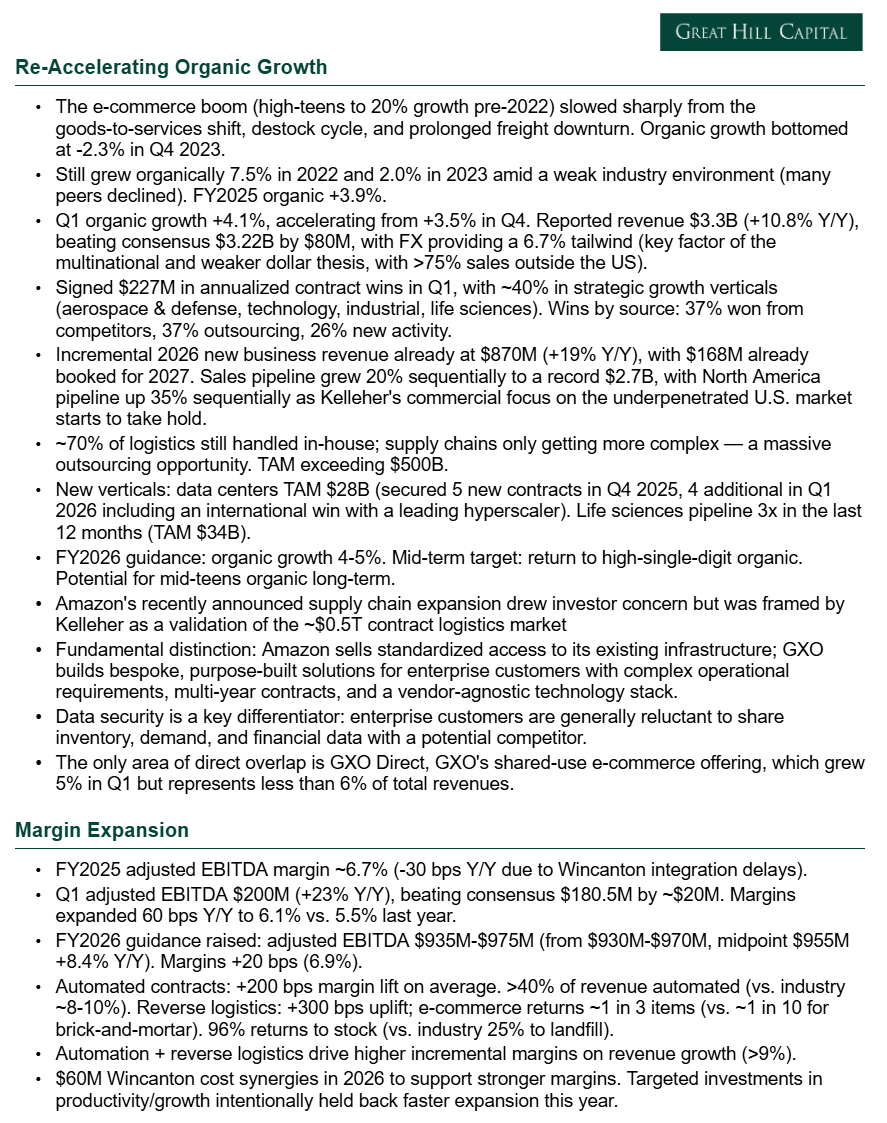

These strong results, combined with the contractual, high-visibility nature of the business, gave management enough confidence to raise full-year guidance after just one quarter, lifting both adjusted EBITDA and EPS, the latter now implying ~22% growth at the midpoint. What makes that confidence even more impressive is what’s behind it. This isn’t guidance built on a rosy assumption of a volume recovery, despite signposts that suggest we’re still in the early innings of a broader logistics upcycle. Instead, management continues to assume flat overall customer volumes for the full year, a posture Kelleher has repeatedly called prudent. The primary driver behind the raise is the growing commercial traction GXO is seeing in North America, the company’s top strategic priority under Kelleher and arguably its single largest lever to reaccelerate organic growth.

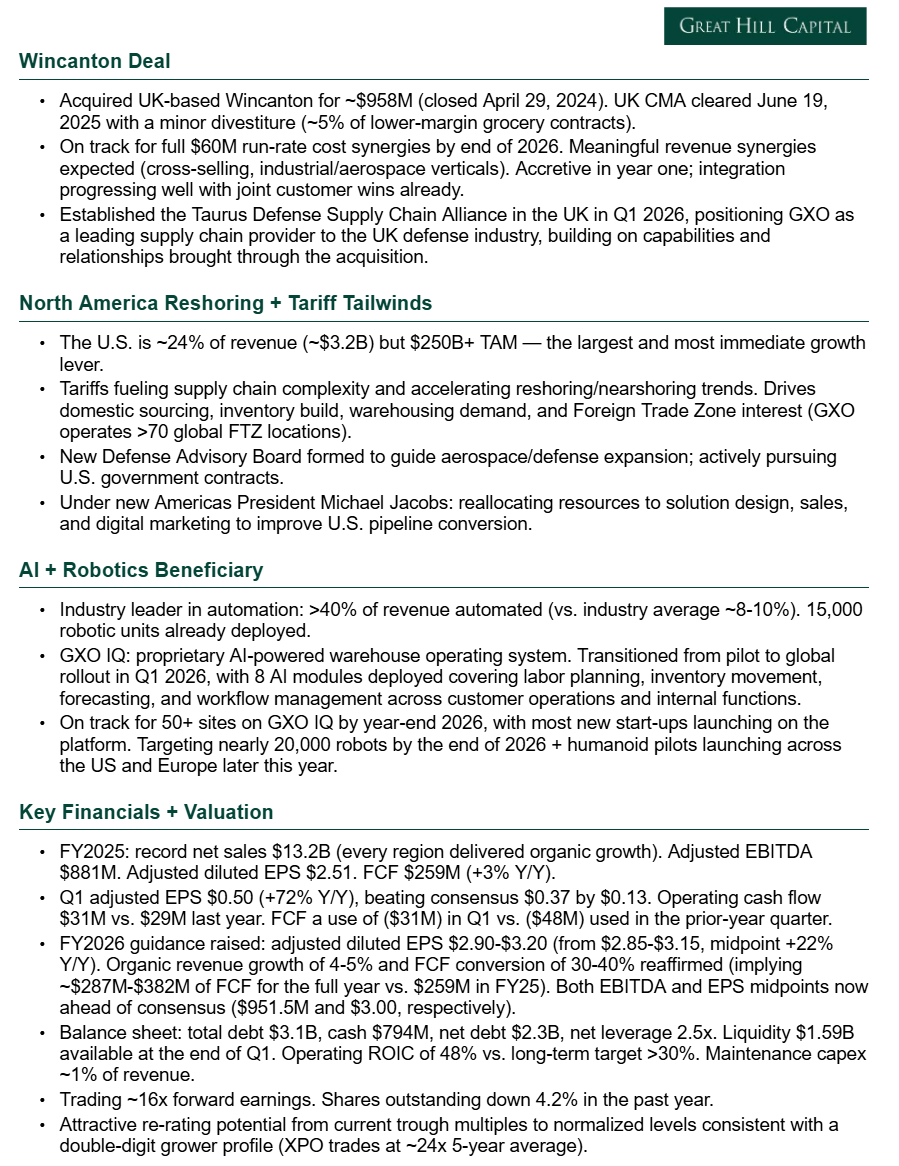

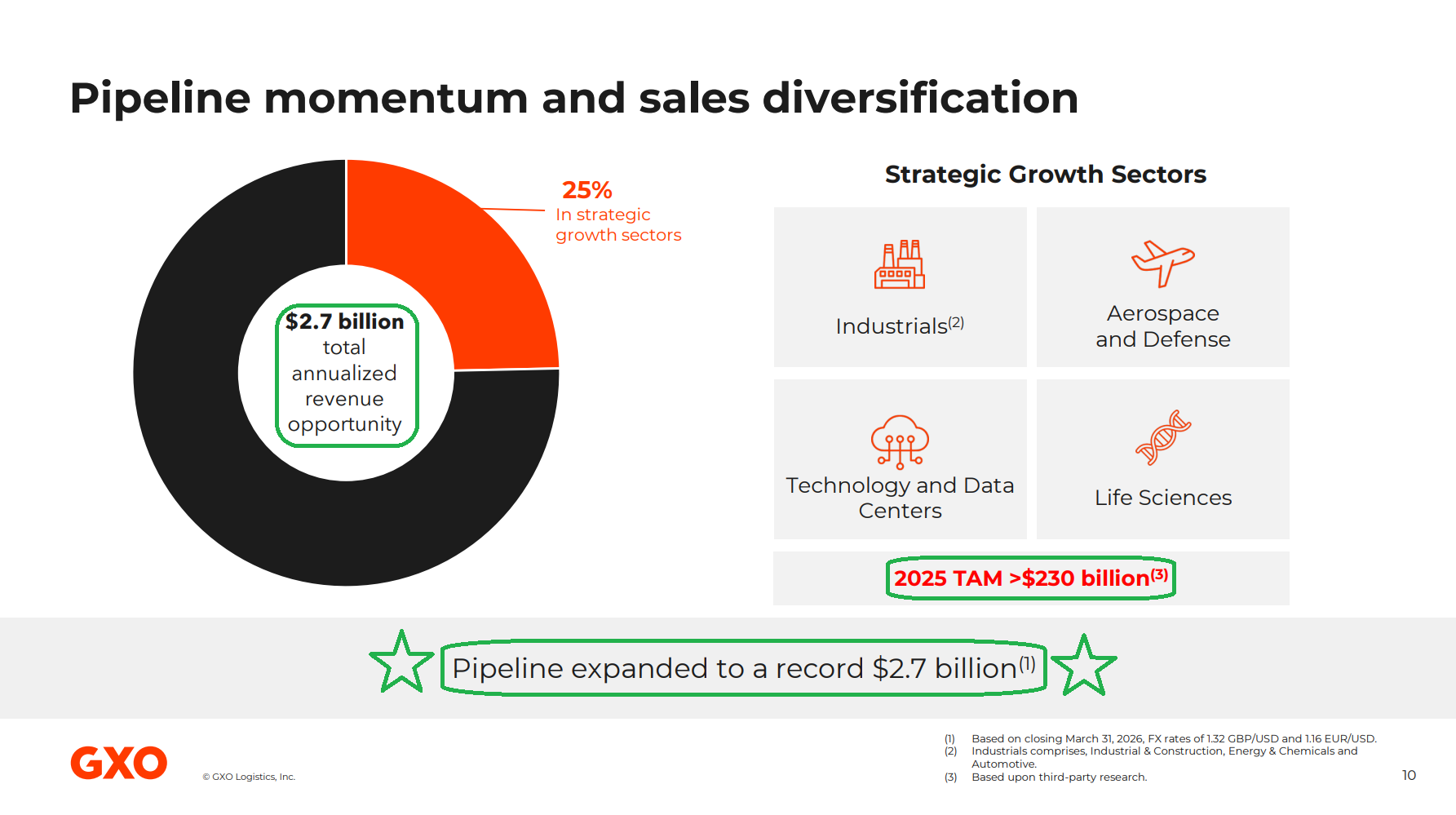

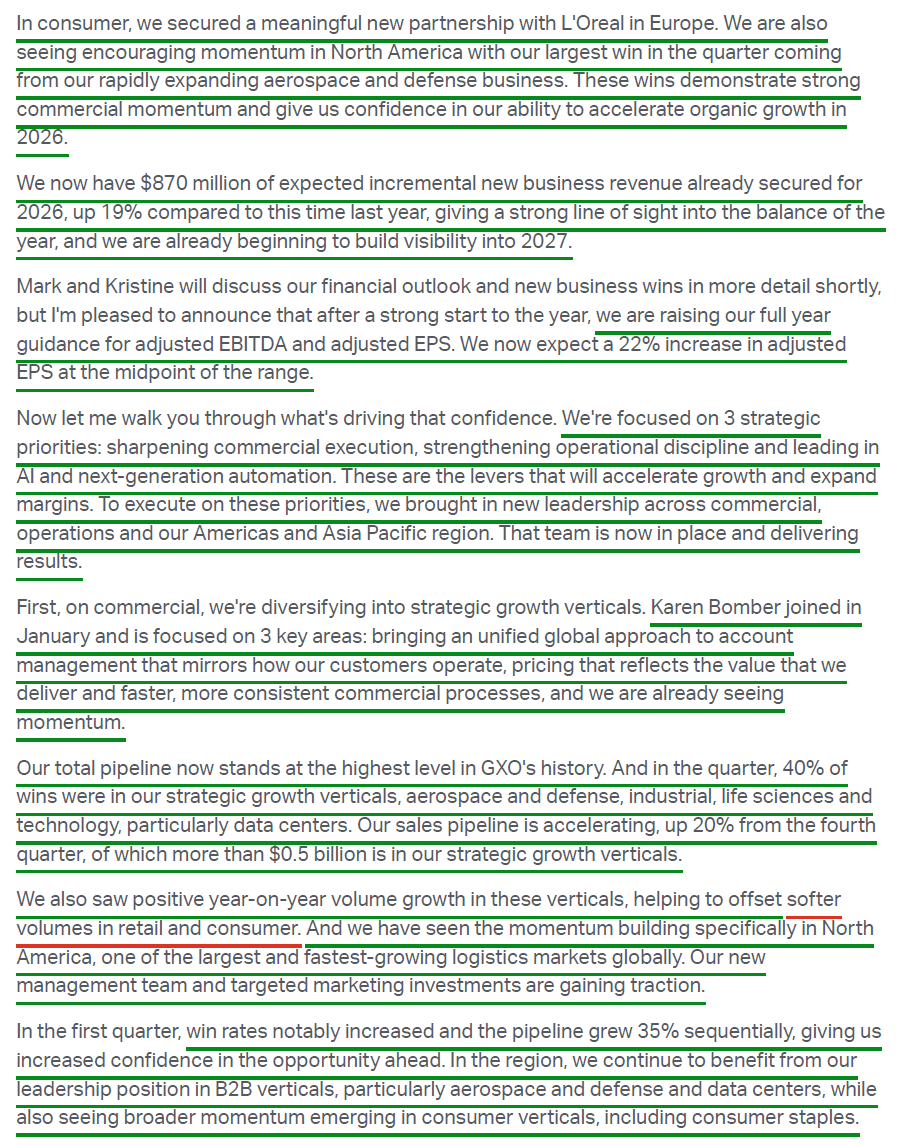

At just ~24% of revenue (~$3.2B) against a $250B+ TAM, North America remains GXO’s largest opportunity. It’s a market the company has long underperformed in and the one Kelleher was brought in to fix, having previously led DHL Supply Chain North America. Early signs of progress are already showing up in the numbers, with the North America pipeline increasing 35% sequentially and helping lift the total sales pipeline 20% to a record high $2.7B.

Perhaps even more encouraging than the headline growth is where those wins are coming from. ~40% of the $227M in Q1 wins came from strategic growth verticals including industrials, life sciences, technology and data centers, and aerospace and defense, where GXO landed its largest single contract of the quarter with an A&D customer in North America. This is the strategic pivot Kelleher set out to execute from day one, now starting to show up in the numbers in his third full quarter at the helm.

Now, to the elephant in the room.

The big story heading into earnings wasn’t GXO’s results at all. It was Amazon (AMZN).

Just two days before GXO reported earnings, Amazon announced an expanded supply chain offering, opening its logistics network to third-party shippers beyond marketplace sellers. In typical manic fashion, Mr. Market wasted no time pricing in a crack in the GXO moat, sending shares down as much as 18% on the news for the worst single-day decline since the company became public.

This shoot-first, ask-questions-later reaction is a textbook example of the voting machine nature of public markets in the short run, creating exactly the type of dislocation we look for while we wait for the weighing machine to have its say.

As we’d expect, management’s reaction to the announcement was far more measured than the market’s response. In fact, Kelleher framed Amazon’s entry not as a threat, but as validation of the market opportunity. The reality is that contract logistics is a nearly half-trillion-dollar market, with only ~30% currently outsourced to 3PLs like GXO. There is simply too much runway left in the market for this to be a winner-take-all outcome.

Even with Amazon’s expanded offering, the model remains largely volume-first and standardized, focused on selling access into the spare capacity of its own network. GXO, by contrast, operates a fundamentally different model, providing customers with standalone, customized logistics solutions supporting highly complex operations. These relationships are sticky by design, with average contract durations of ~5 years and customer retention rates north of 95%.

Beyond the operational complexity that standardized solutions don’t address, there is also a trust component that shouldn’t be overlooked. You’d be hard-pressed to find enterprises willing to hand the keys to a potential competitor with full visibility into their inventory, demand, and financials, a structural advantage for a pure-play like GXO.

The only real overlap is GXO Direct, the company’s shared-use e-commerce offering, which grew ~5% in the first quarter and accounts for less than 6% of total revenue.

These factors, along with GXO’s limited overlap, give us all the comfort we need that competitive fears are overblown.

Looking past the Amazon noise, we continue to view much of what the market sees as headwinds in the current environment as tailwinds for GXO. Geopolitical tensions, supply chain disruptions, tariffs, and reshoring initiatives all increase operational complexity for businesses and, in many cases, force full logistics network redesigns.

With supply chains getting more complicated and the cost of getting them wrong rising, handing the problem to a specialist starts to look increasingly attractive. With ~70% of logistics still managed in-house, the potential customer base remains a $500B+ market that only gets larger as supply chains become more complex.

Not to mention, in a market increasingly focused on separating AI beneficiaries from AI cost centers, it’s hard to think of a better-positioned beneficiary than GXO. We have long believed that if AI truly becomes the productivity boom investors have priced in, many of the biggest winners will be “boring,” everyday businesses that can apply it in practical ways to drive productivity and profitability, rather than those left funding the buildout and footing the bill.

For GXO, that opportunity comes through GXO IQ, the company’s proprietary AI-powered warehouse operating system, which moved from pilot to global rollout this quarter and remains on track for 50+ sites by year-end. The platform now includes eight AI modules deployed across labor planning, inventory movement, forecasting, and workflow management across both customer operations and internal functions.

Clearly, there is plenty to be excited about when it comes to GXO today, with the next major catalyst being the long-awaited Investor Day under Kelleher, scheduled after third quarter earnings. That’s where the market will finally get a roadmap for what a structurally higher margin base looks like and how organic growth can reaccelerate as the restocking cycle continues to play out. We suspect it will also be the point where investors begin to wake up to the secular drivers we’ve been pounding the table on.

Until then, the things we care about most, accelerating organic growth and margin expansion, are precisely what GXO is delivering under Kelleher, and we look forward to what should be an important Investor Day later this year.

Q1 Earnings Breakdown

10 Key Points

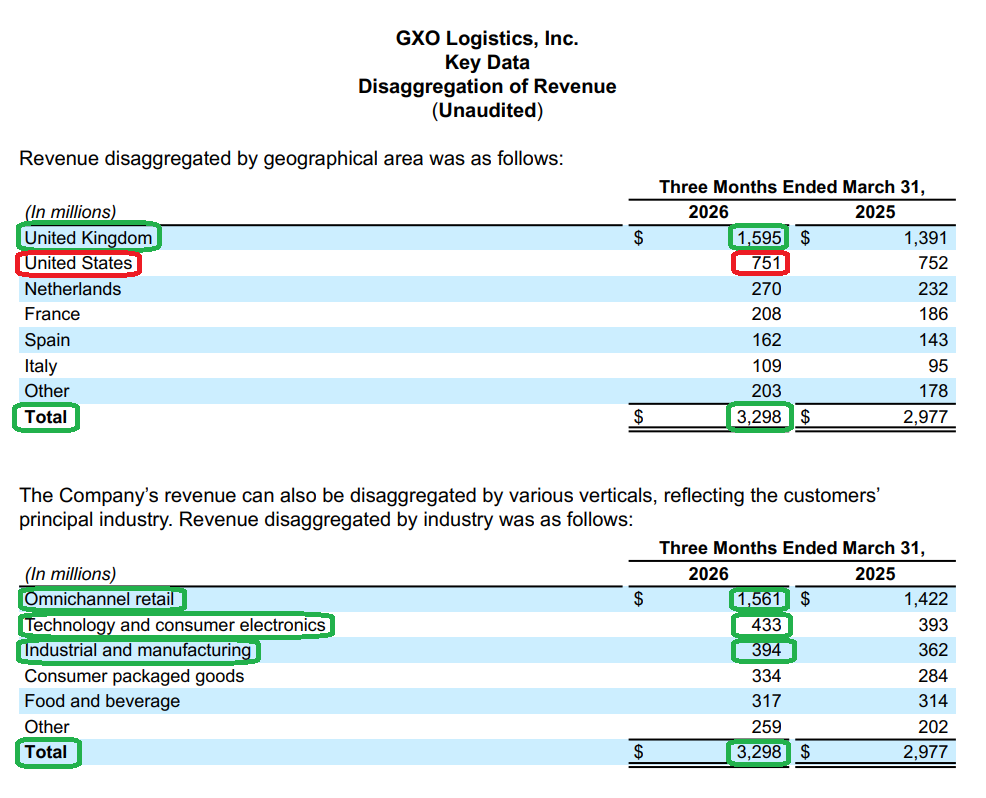

1) Q1 revenue came in at $3.3B (+10.8% Y/Y), beating consensus of $3.22B by ~$80M. Organic growth accelerated to +4.1% from +3.5% in Q4, with every region contributing. Volumes were flat in aggregate and in line with management’s expectations, with B2B strength across aerospace, defense, industrial, technology, and life sciences offsetting softer B2C volumes in retail and CPG. FX contributed a 6.7% tailwind (~$198M), with more than 75% of GXO’s revenue generated outside the United States.

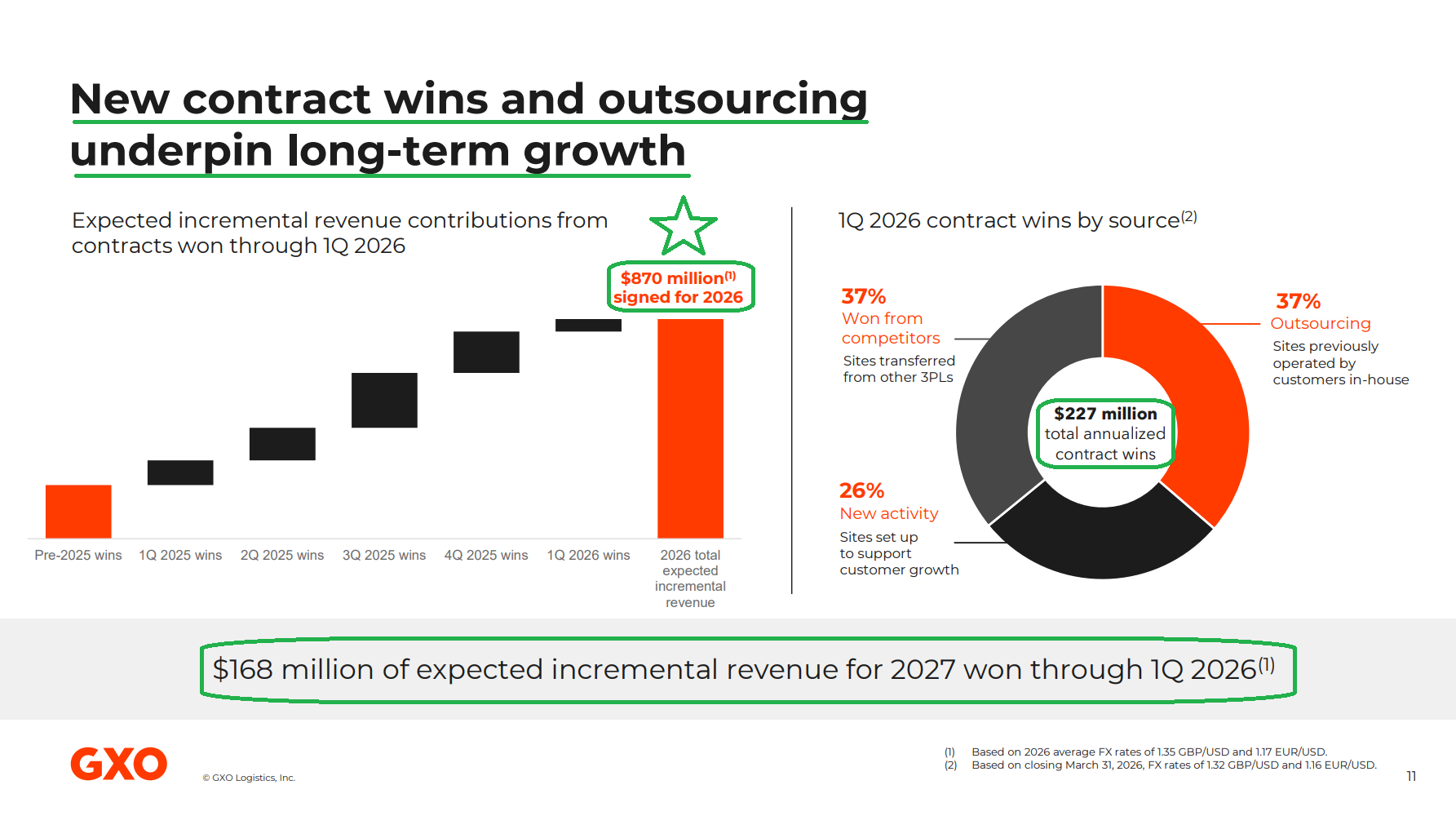

2) GXO signed $227M in annualized new business wins during Q1, with ~40% coming from strategic growth verticals. By source, wins broke down as 37% taken from competitors, 37% from outsourcing, and 26% from new activity. Notable wins included Raytheon (RTX), BAE Systems (BAESY), and L’Oréal (LRLCY), along with four additional data center contracts, one of which was an international win with a leading hyperscaler. GXO now has $870M of expected incremental FY2026 revenue locked in, +19% versus the comparable position a year ago, with $168M of incremental 2027 revenue already booked.

3) The total sales pipeline grew 20% sequentially to a record $2.7B, the highest in GXO’s history. ~25% is concentrated in strategic growth verticals, including aerospace and defense, technology and data centers, life sciences, and industrials, against a combined TAM exceeding $230B. North America led the way, with the NA pipeline growing 35% sequentially and win rates increasing during the quarter, driven by early commercial traction from Kelleher’s push to capture a larger share of the underpenetrated U.S. market. The remaining ~75% of the pipeline sits in core verticals, including omnichannel retail and consumer, with strategic vertical expansion adding to the base business rather than pulling from it.

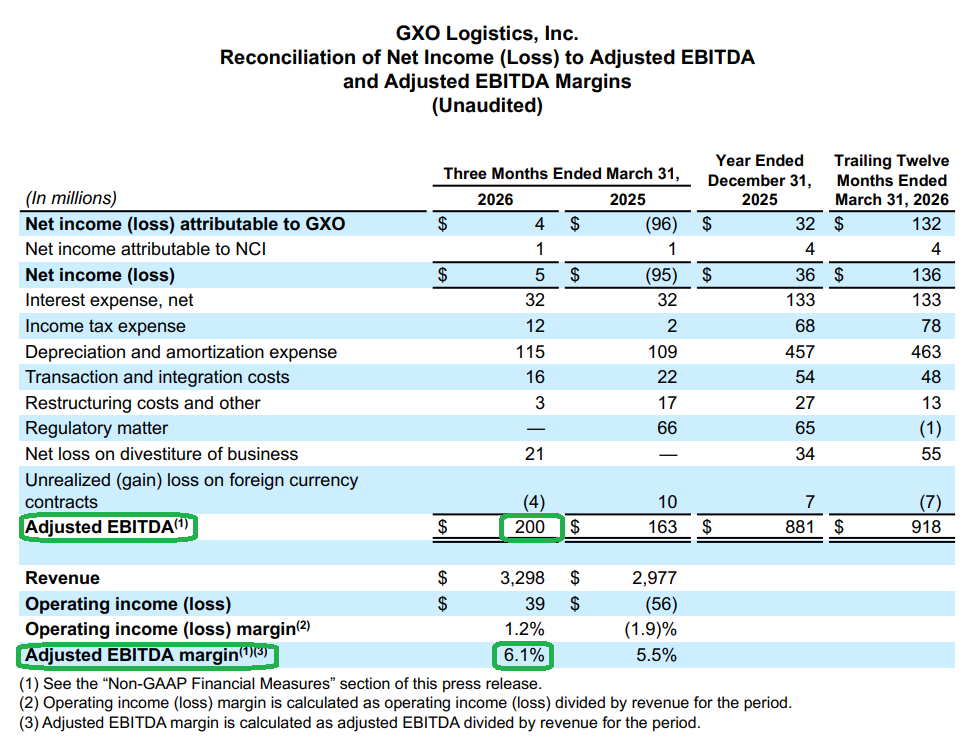

4) Adjusted EBITDA came in at $200M (+22.7% Y/Y), beating consensus of $180.5M by ~$20M. Adjusted EBITDA margins expanded 60 bps Y/Y to 6.1% from 5.5% a year ago, driven by strong underlying business performance as well as a $12.5M net Y/Y benefit from an early site exit and the timing of contract termination costs deferred into the remainder of the year. Management cited early traction from the GXO Way, the company’s new global operating framework focused on standardizing execution at scale, along with improvements in labor productivity, contracting, and pricing as key contributors. Adjusted diluted EPS came in at $0.50 (+72.4% Y/Y), ahead of consensus of $0.37.

5) The Wincanton (WIN) integration remains on track, with management reiterating its $60M run-rate cost synergy target by year-end 2026. New CFO Mark Suchinski expressed confidence in achieving that target and sees room for upside beyond the original estimate, with significant revenue synergies expected over time. On the defense front, Wincanton proved instrumental this quarter in establishing the Taurus Defense Supply Chain Alliance in the UK, positioning GXO as a leading supply chain provider to the UK defense industry and opening a meaningful new growth avenue in one of the company’s highest-priority verticals.

6) GXO addressed investor concerns around Amazon’s recently announced supply chain expansion head-on, with Kelleher framing it as validation of the ~$0.5T contract logistics market, ~70% of which remains in-sourced. Amazon sells standardized access to its existing infrastructure, while GXO builds bespoke solutions for enterprise customers with complex operational requirements and multi-year contracts on a vendor-agnostic technology stack. Data security was also cited as a key differentiator, as enterprise customers are generally reluctant to share inventory, demand, and financial data with a potential competitor. The only area of direct overlap is GXO Direct, GXO’s shared-use e-commerce offering, which grew 5% in Q1 but represents less than 6% of total revenue.

7) GXO IQ, the company’s proprietary AI-powered warehouse operating system, reached a key milestone in Q1, transitioning from pilot to global rollout with a go-live at a large consumer products site. Deployment continues to accelerate across North America and Europe, with management on track to reach its target of 50+ sites on GXO IQ by year-end. With eight deployed AI modules already in production covering labor planning, inventory movement, forecasting, and workflow management, the platform is generating AI-driven productivity improvements across both customer warehouse operations and internal functions, including HR, IT, and finance. GXO also plans to launch additional humanoid robot pilots across the U.S. and Europe later this year, building on its existing first-mover position in warehouse robotics.

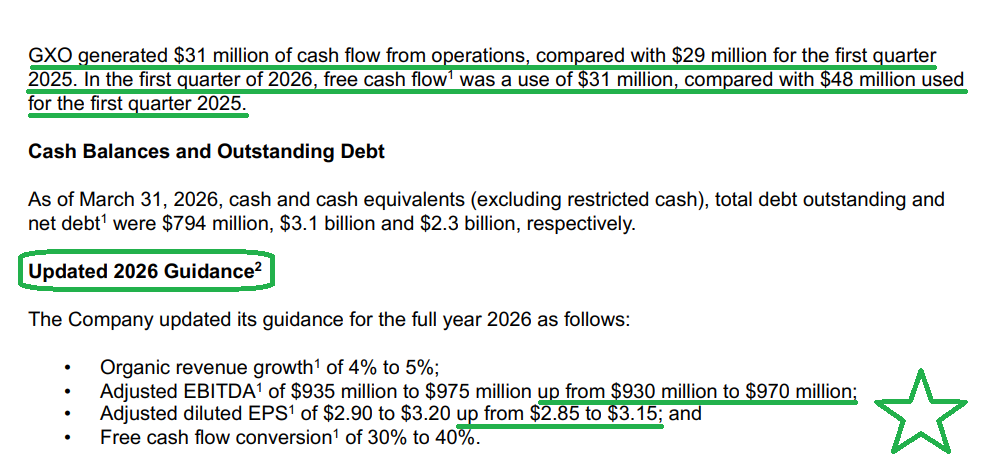

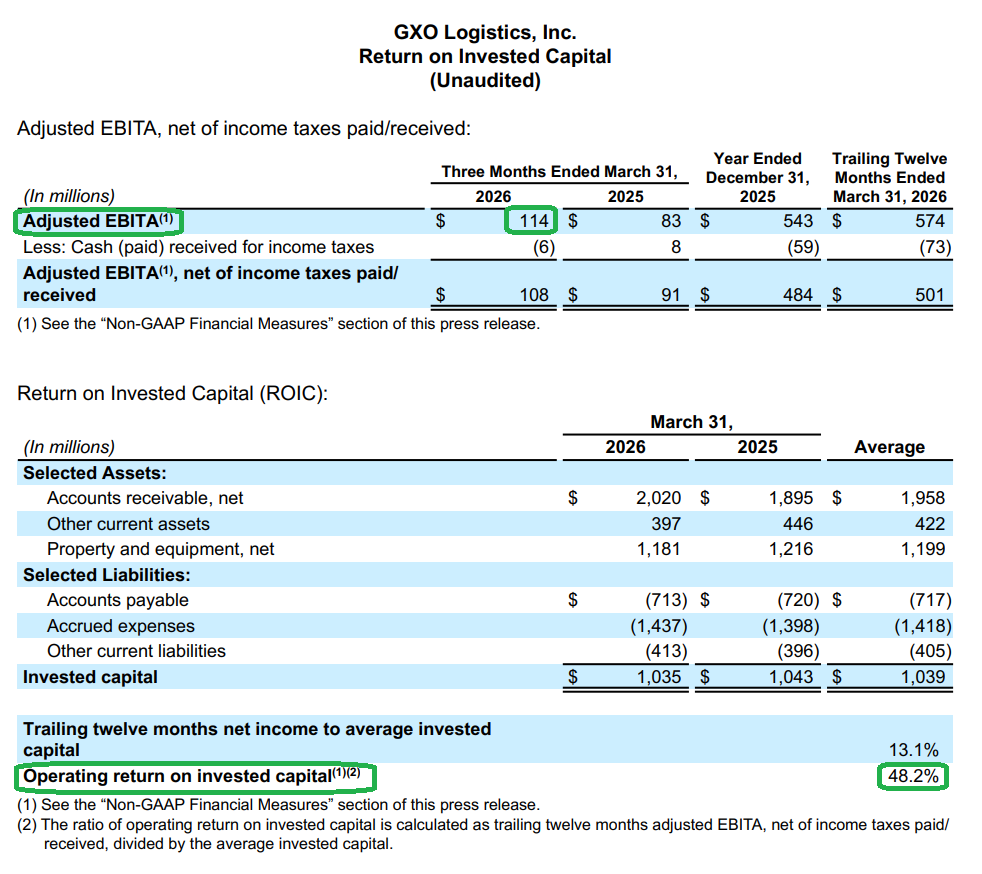

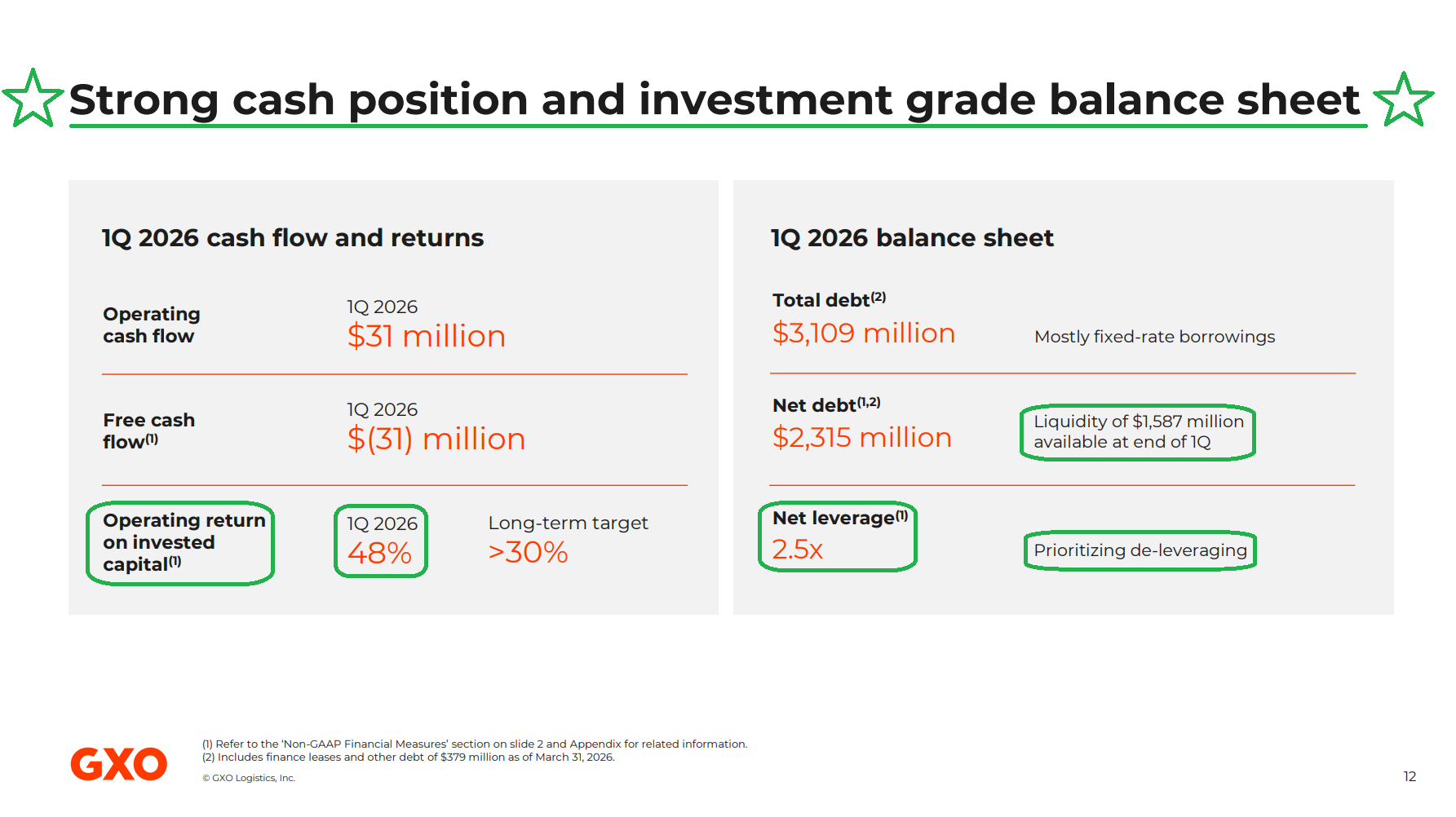

8) Operating cash flow came in at $31M versus $29M in the prior-year period, while free cash flow was a use of ($31M) versus ($48M) in Q1 2025, with the outflow in line with typical Q1 seasonality. Operating ROIC came in at 48.2% on a trailing twelve-month basis versus a long-term target of greater than 30%. Full-year FCF conversion guidance of 30-40% was reiterated, implying ~$334M of free cash flow at the midpoint, a ~29% increase versus $259M in FY2025.

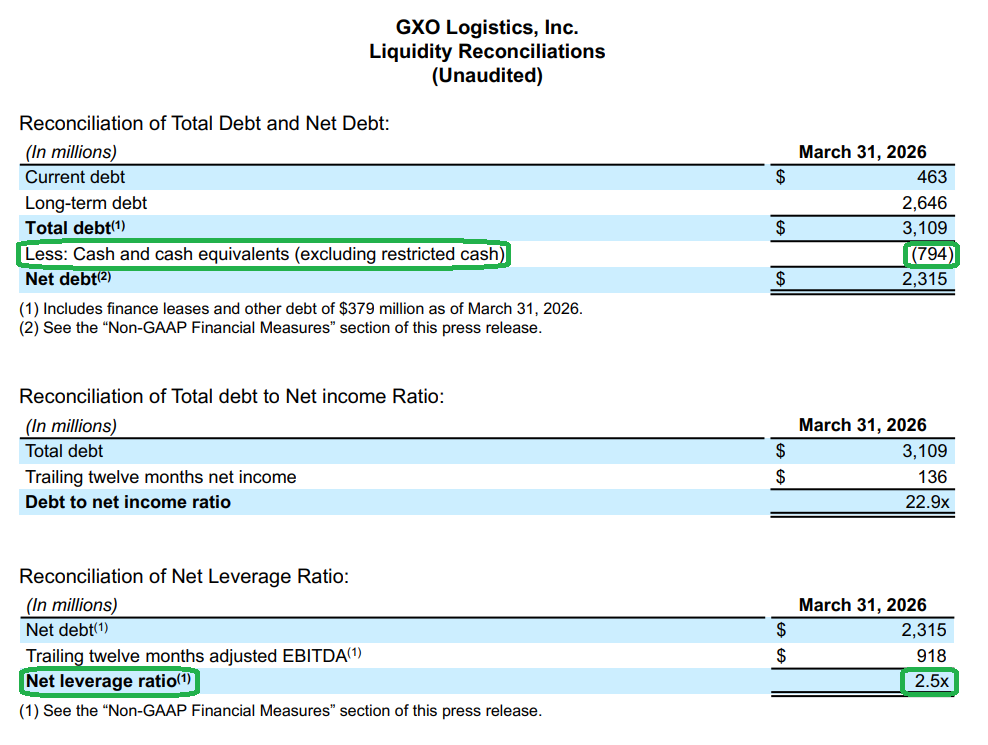

9) GXO ended Q1 with $794M in cash, total debt of $3.1B, net debt of $2.3B, and net leverage steady at 2.5x, with total liquidity of $1.6B. The balance sheet carries an investment-grade rating from all three major agencies, with borrowings predominantly fixed-rate. Further deleveraging remains the top near-term capital allocation priority, with M&A not currently on the agenda.

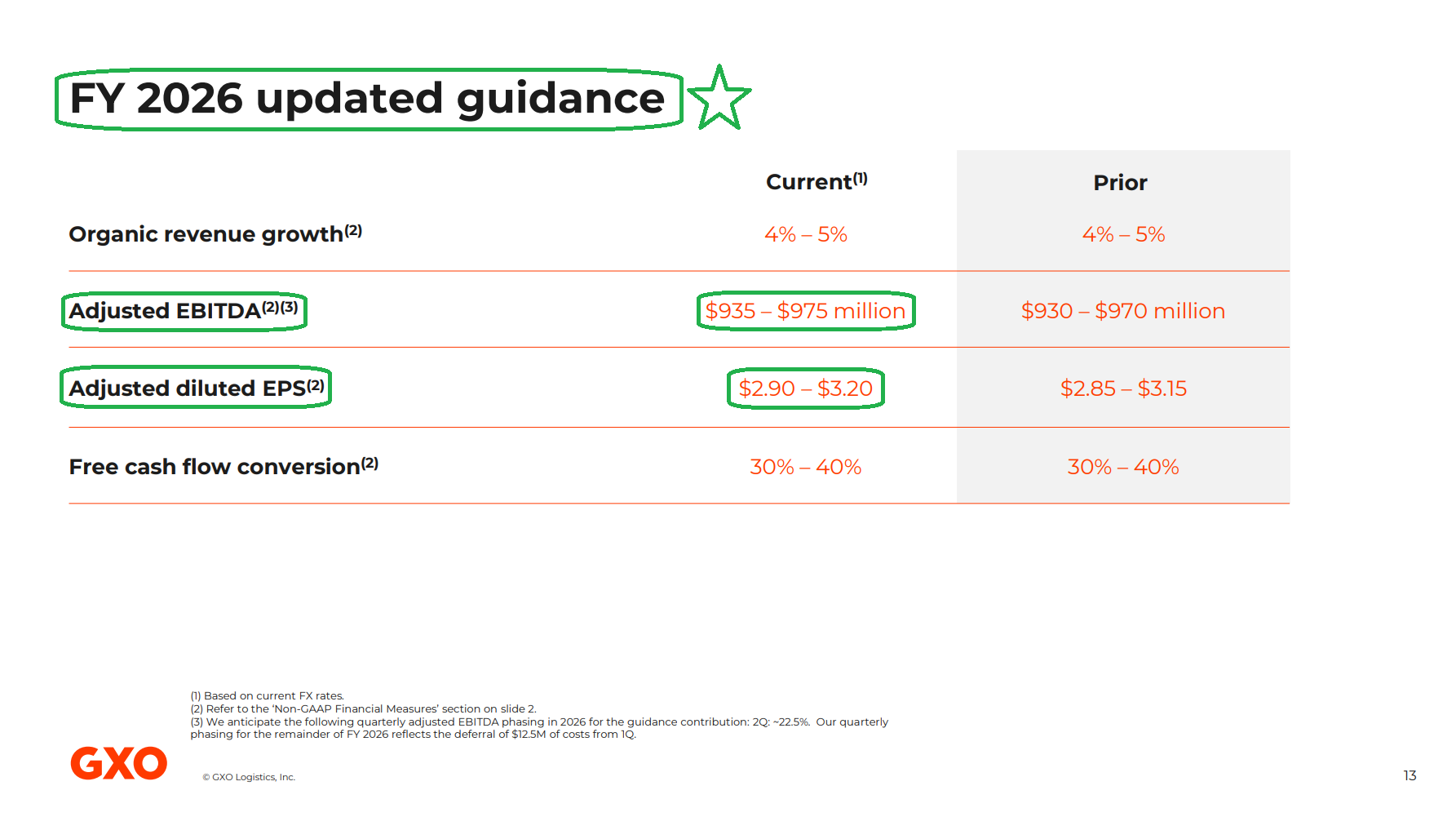

10) Management raised full-year FY2026 adjusted EBITDA guidance to $935M-$975M (from $930M-$970M) and adjusted diluted EPS to $2.90-$3.20 (from $2.85-$3.15), representing +22% EPS growth at the midpoint. Organic revenue growth guidance of 4-5% was reaffirmed, with Q2 expected to track in line with Q1 before accelerating in the back half as new business ramps. Guidance continues to assume flat customer volumes, which management characterized as prudent. Investor Day, scheduled following Q3 earnings, will outline a three-year strategic roadmap, including organic growth targets, margin expansion opportunities, and the company’s long-term financial framework.

Earnings Call Highlights

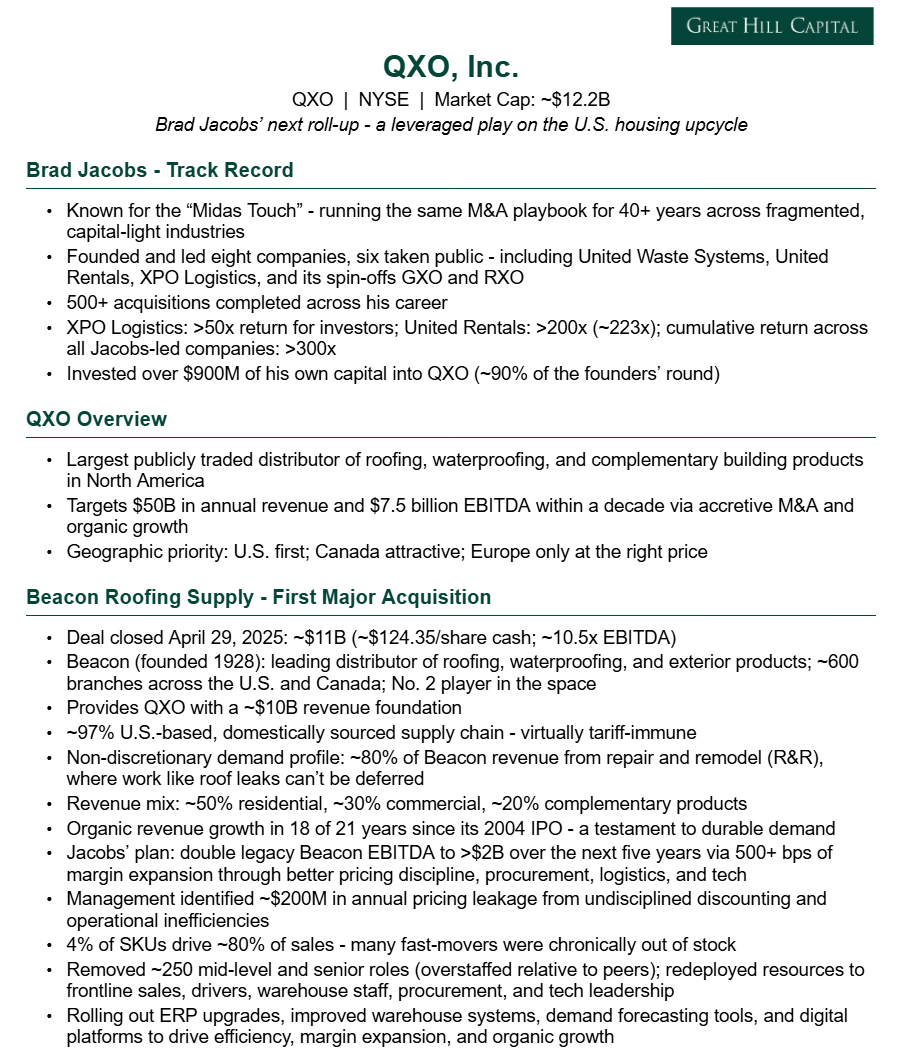

QXO (QXO) Update

For newer readers, here’s a quick overview of the key drivers behind our thesis on QXO, Brad Jacobs’ latest venture and one of our favorite arms dealer plays on a U.S. housing market recovery:

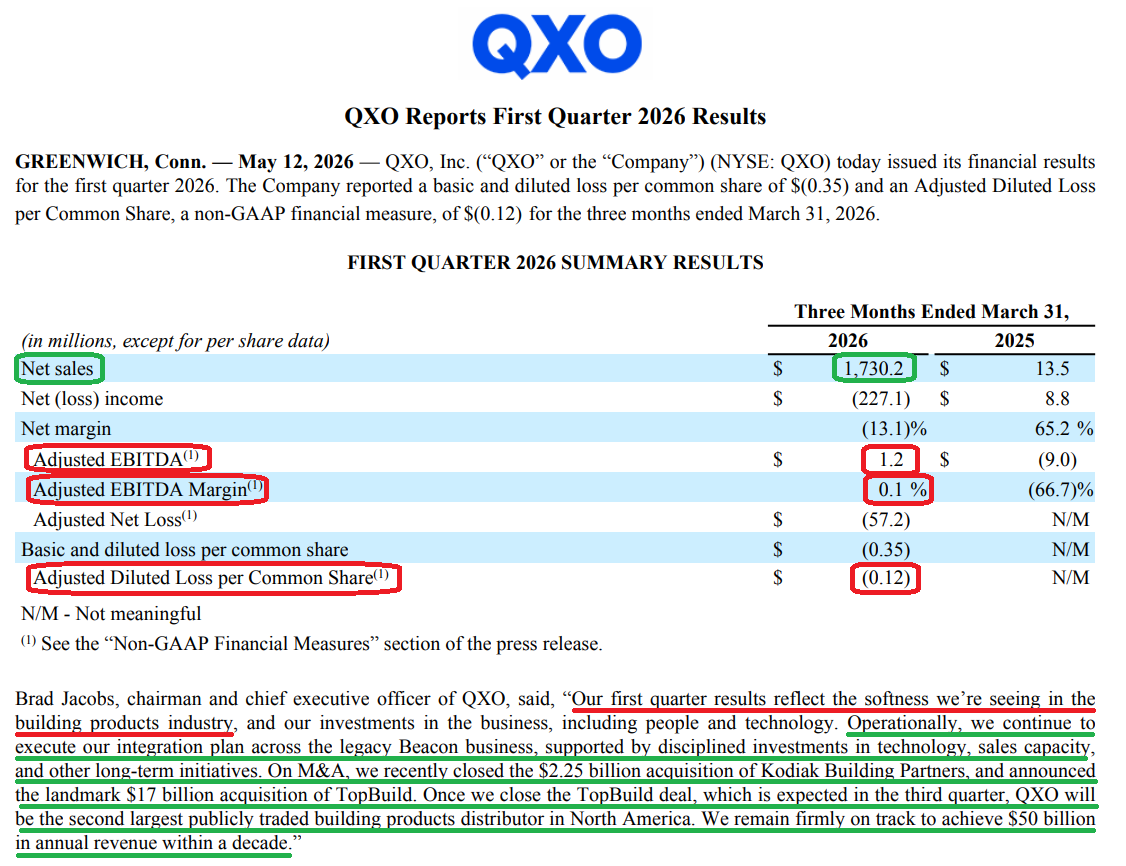

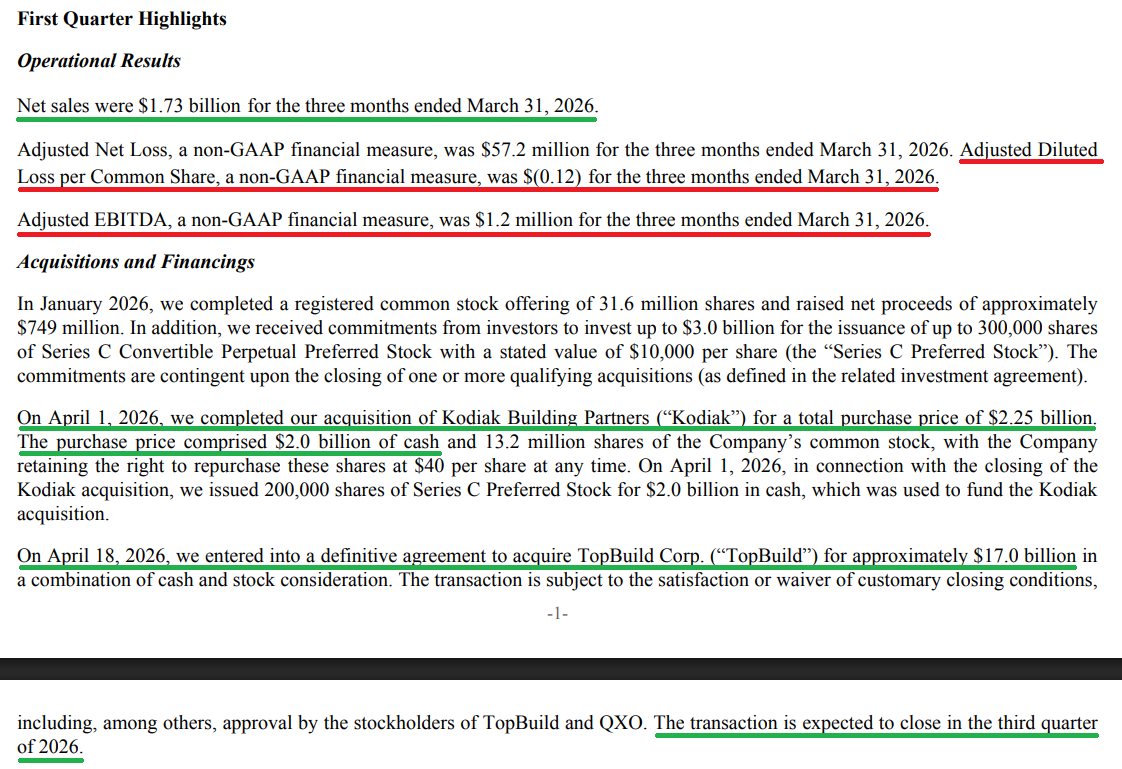

QXO’s first quarter came with few surprises, with continued weakness across the building products industry weighing on near-term results amid elevated mortgage rates and a subdued residential backdrop. Net sales came in at $1.73B, ~9% below legacy Beacon (BECN)’s $1.91B in the prior-year period, while gross margin of 23.7% ran ~80 bps below Beacon’s standalone 24.5%. Combined with elevated spend across systems, sales capacity, and personnel, the near-term print is exactly what you would expect in the early stages of integration at a cycle trough.

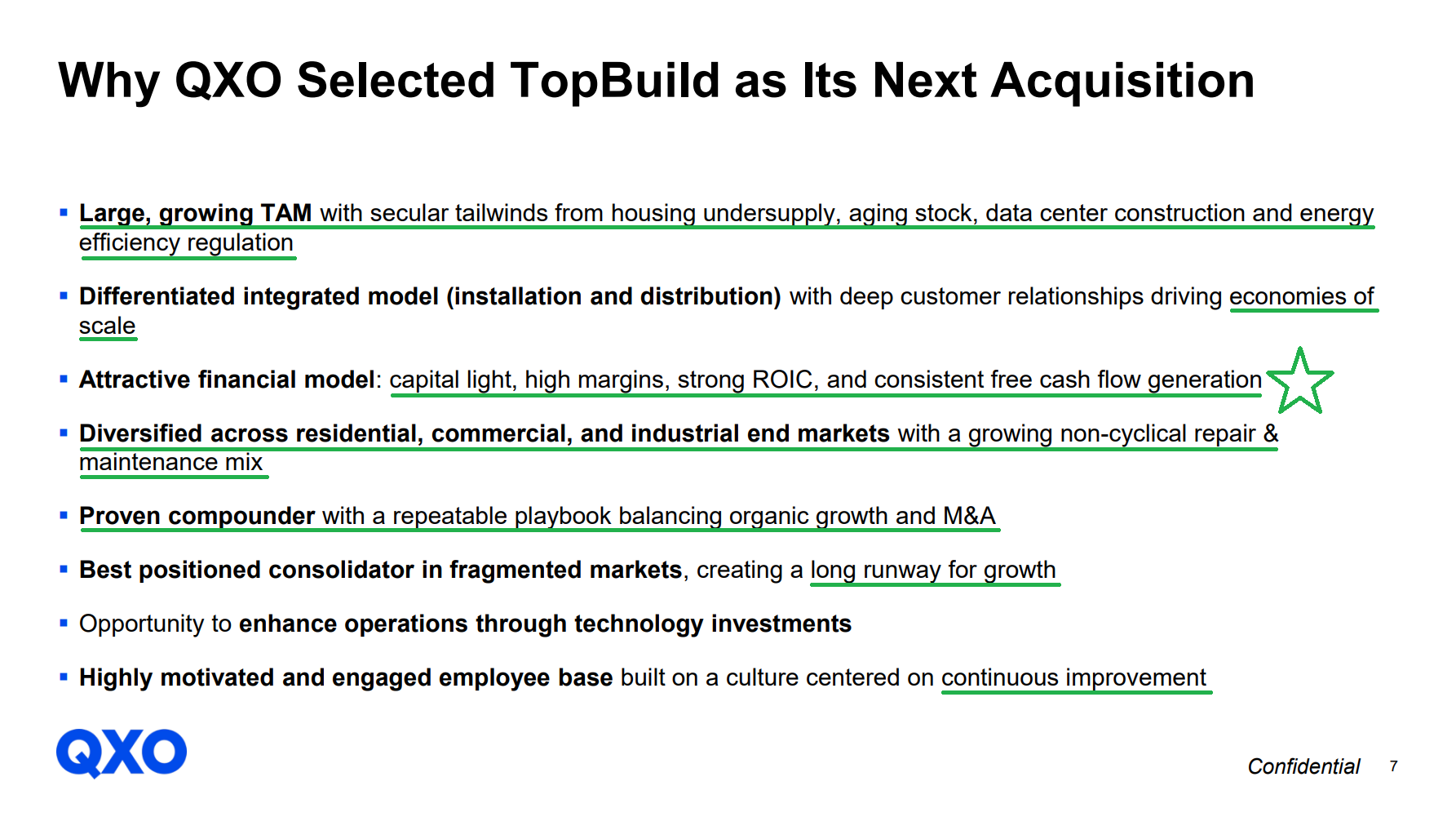

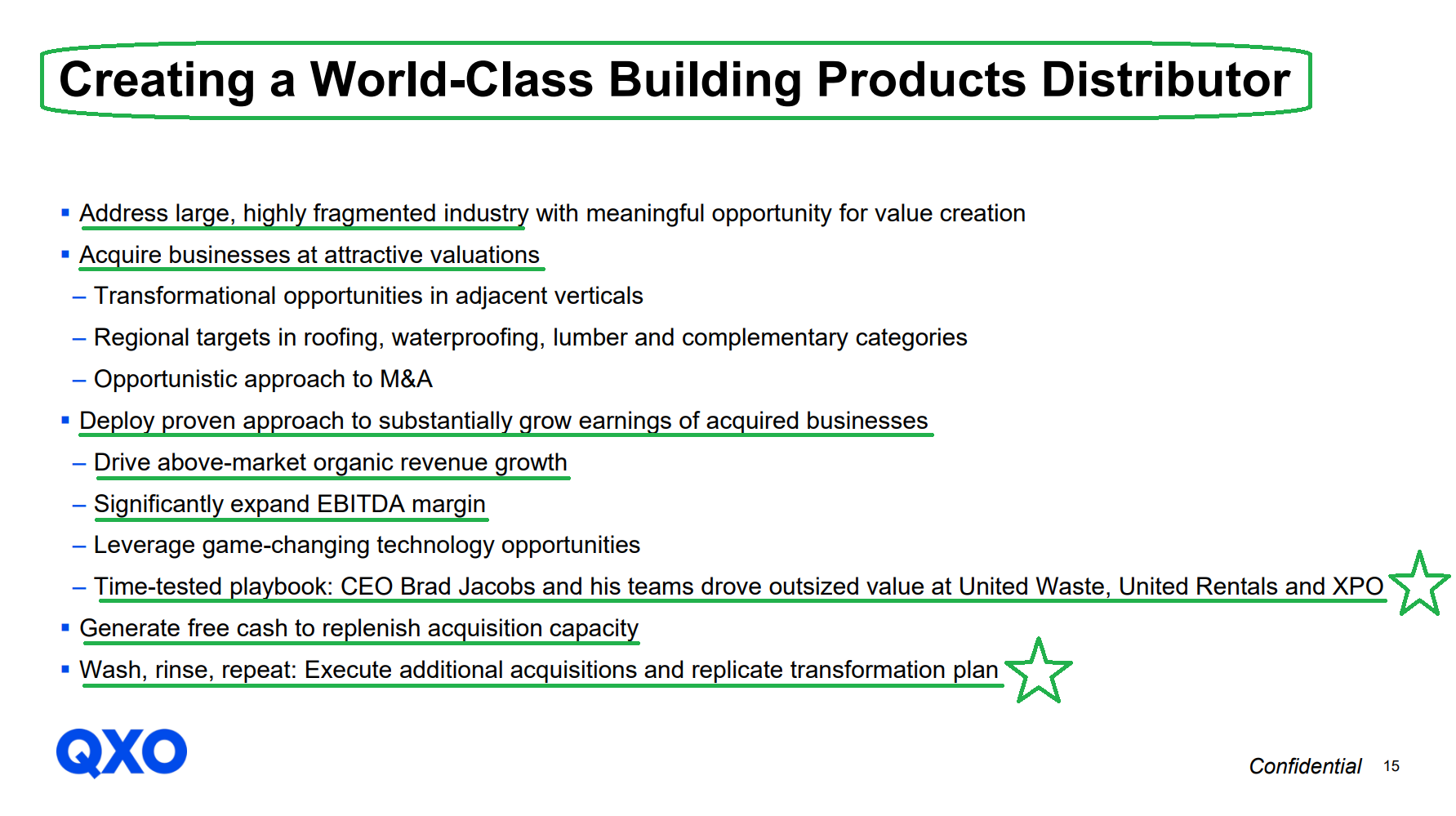

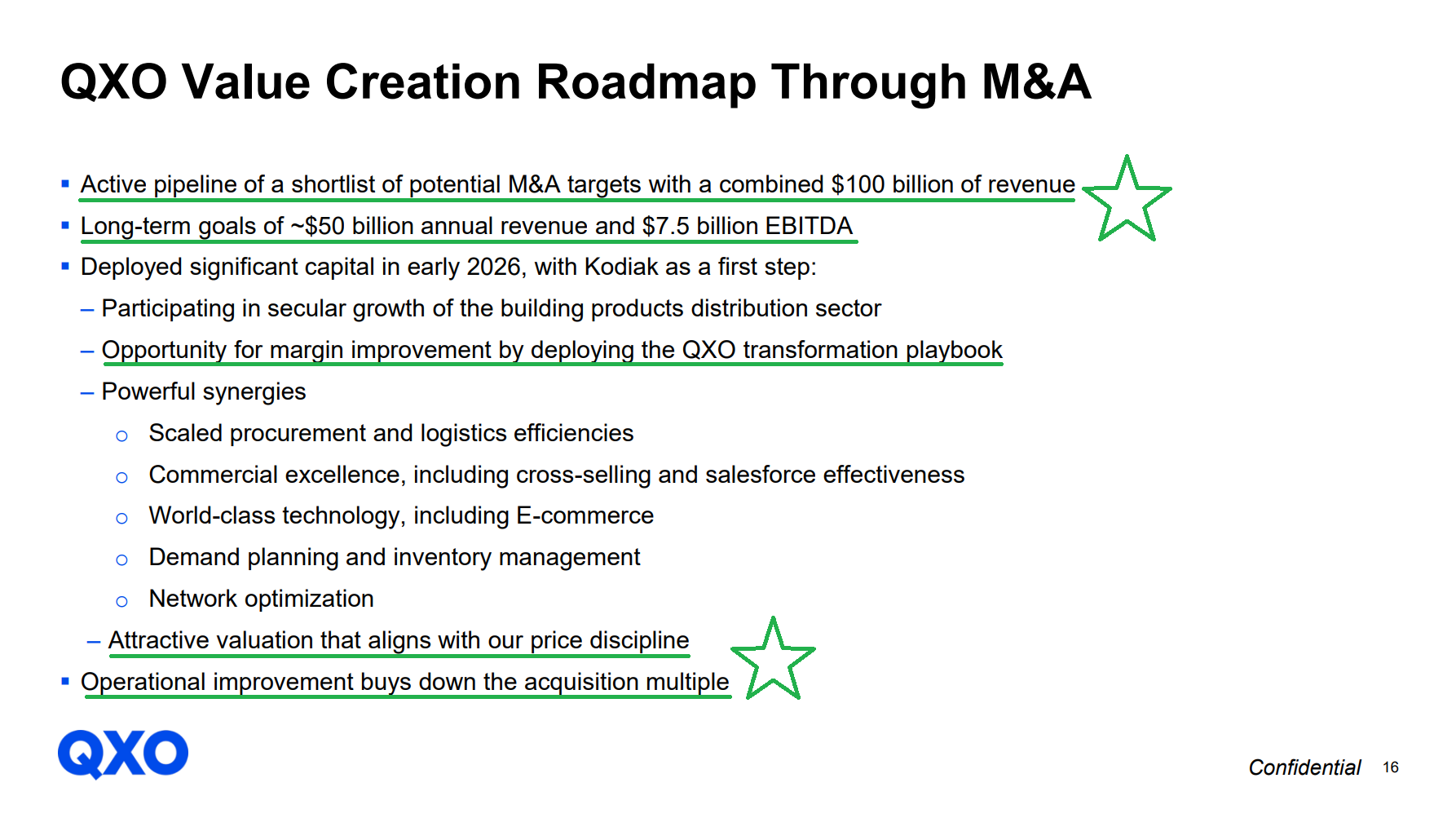

As we have said from the very beginning, the QXO investment case was never about any single quarter and has always been about the roll-up strategy across the ~$800B building products distribution industry, with Brad Jacobs targeting a ~$50B revenue platform over the next decade. In fact, the longer housing remains in the gutter, the more attractive the pipeline of high-quality assets becomes, giving QXO the opportunity to shop from the industry’s clearance rack while waiting for the cycle to turn.

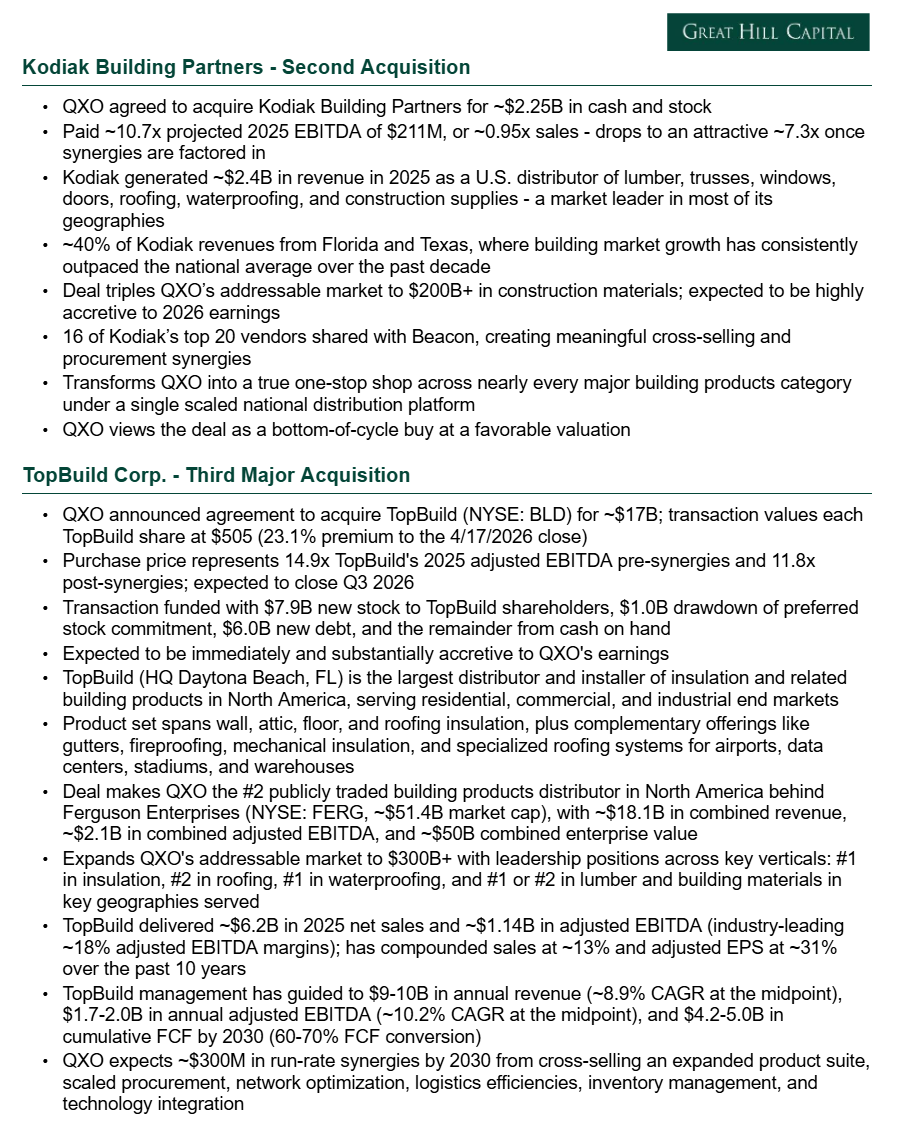

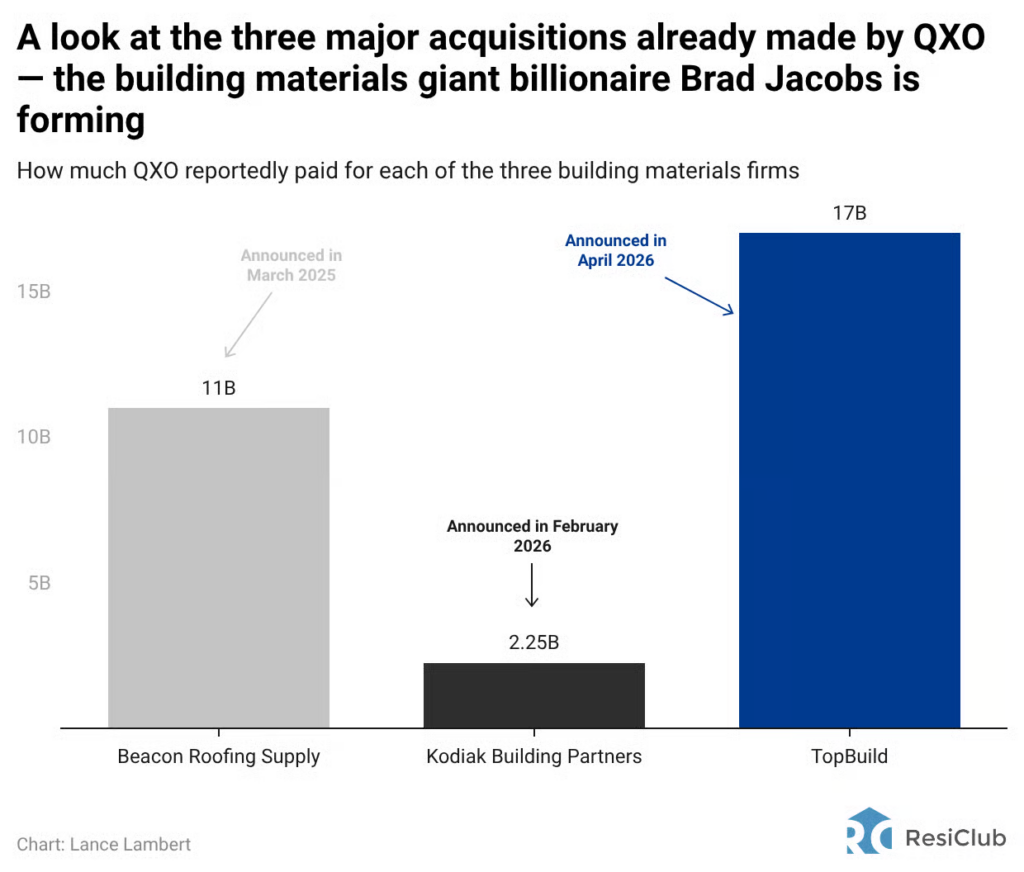

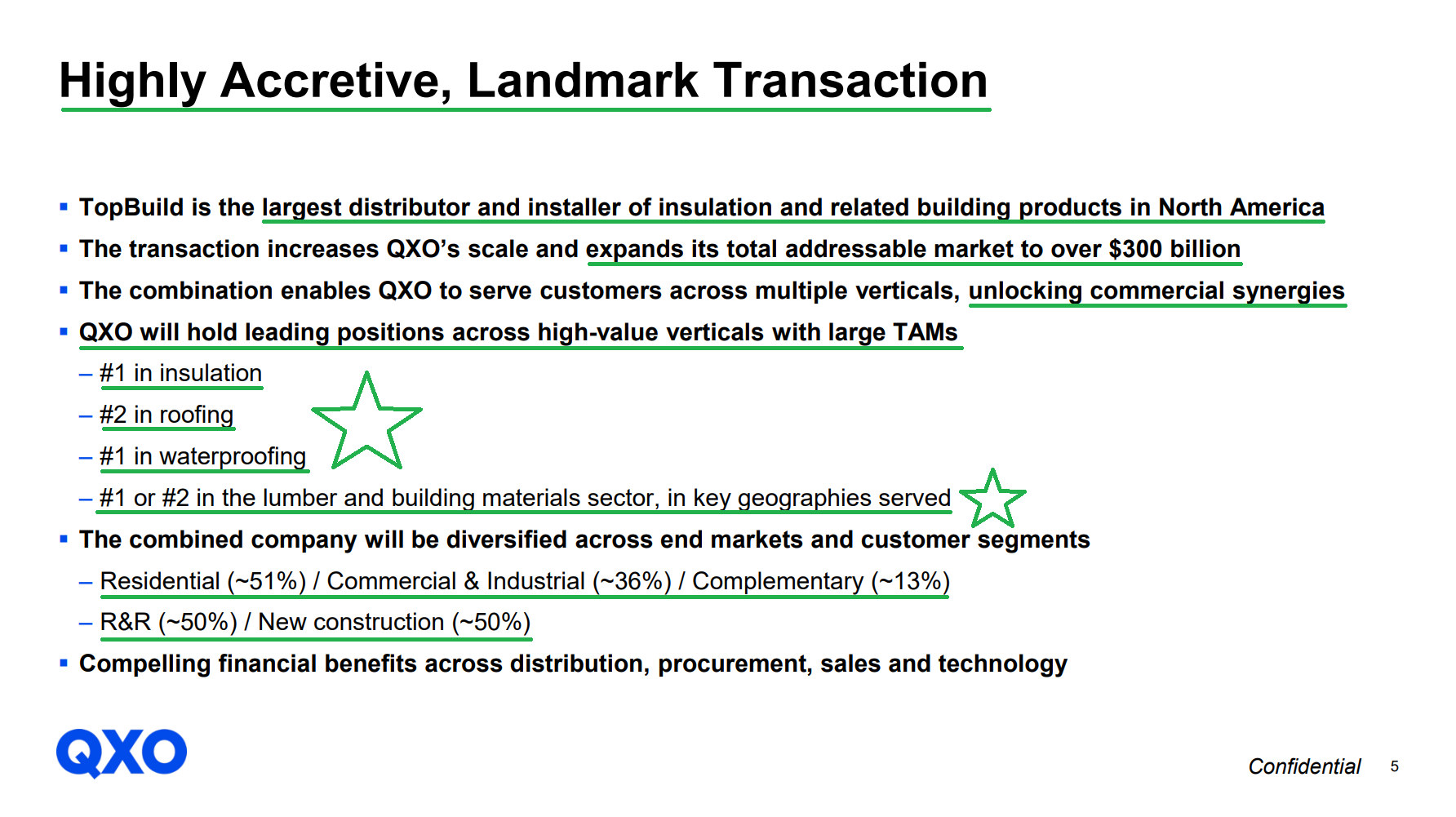

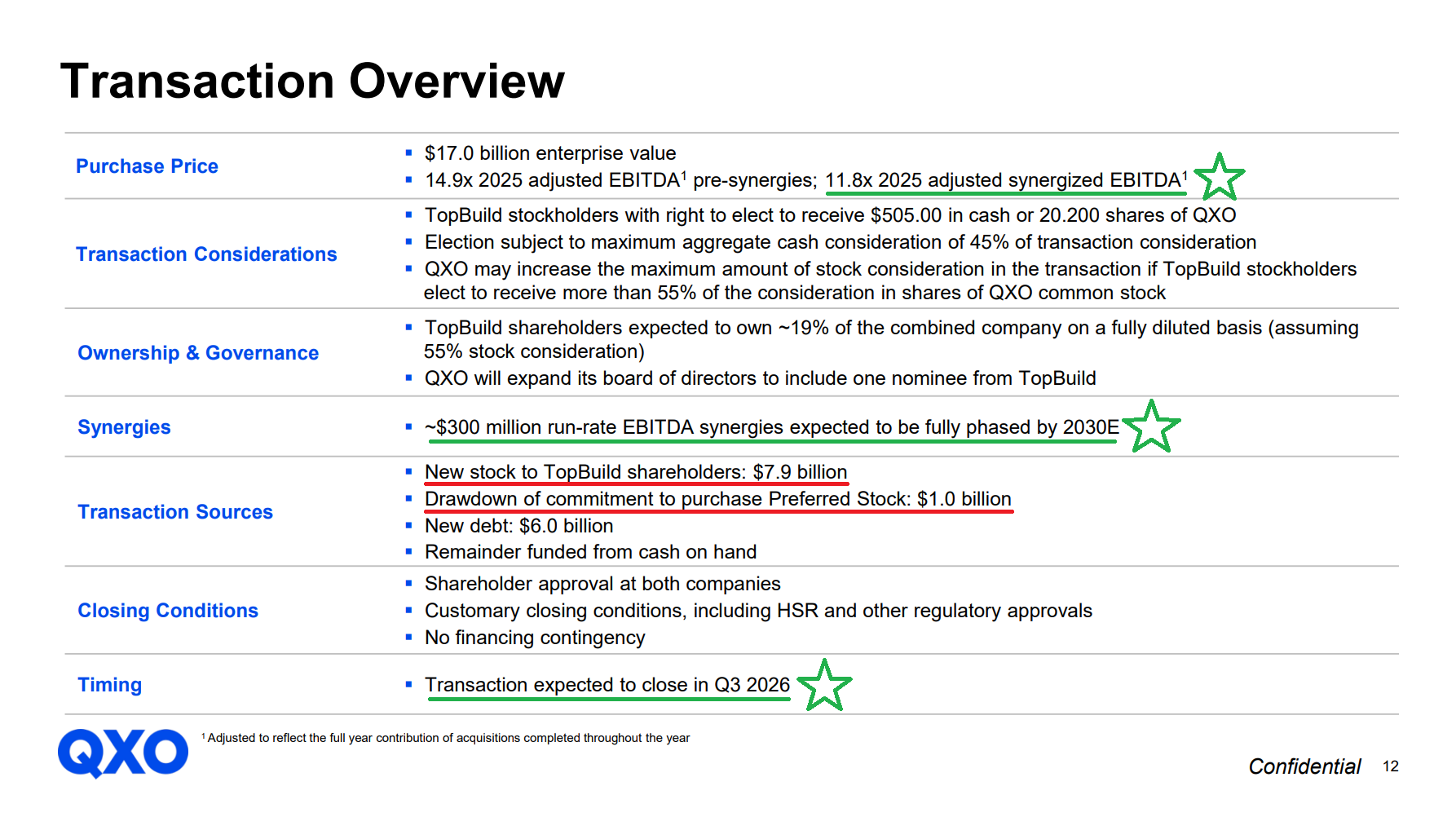

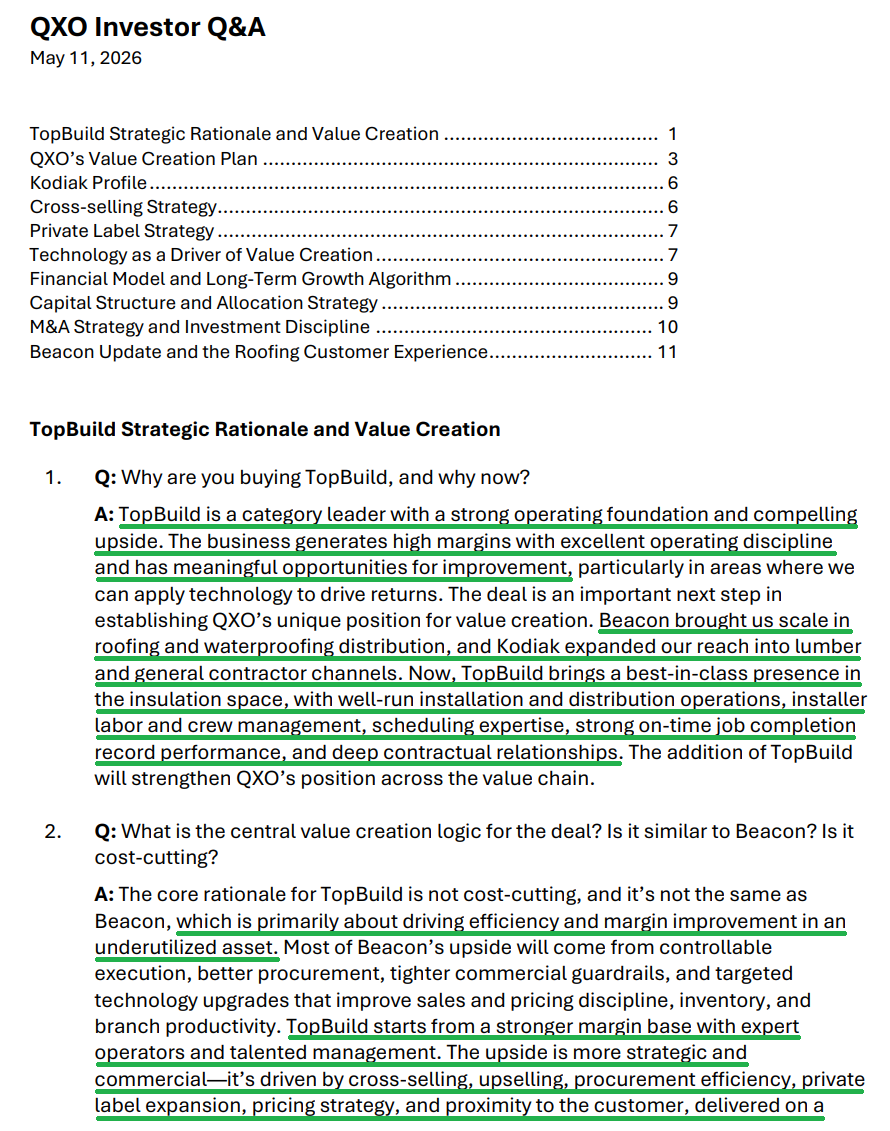

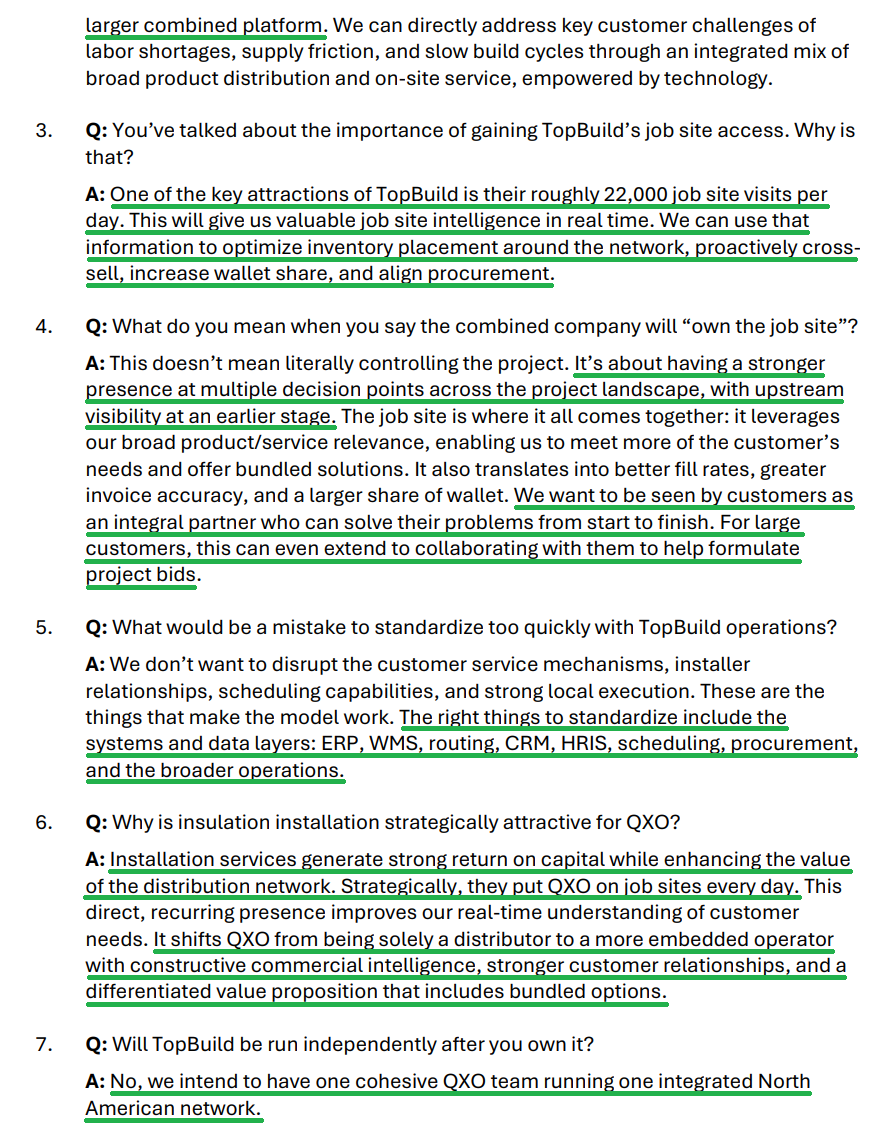

On that front, the quarter’s real news broke weeks before the print rather than in it. On April 18, QXO announced a definitive agreement to acquire TopBuild (BLD), the largest distributor and installer of insulation in North America, for an enterprise value of ~$17B. Expected to close in Q3 2026 and be highly accretive, the transaction is QXO’s biggest swing yet toward its goal of building a ~$50B revenue platform, following the ~$11B acquisition of Beacon Roofing in early 2025 and the $2.25B purchase of Kodiak Building Partners that closed on April 1.

Jacobs joined CNBC shortly after the announcement to discuss the deal in detail and what the combined platform will look like, with the full interview included below:

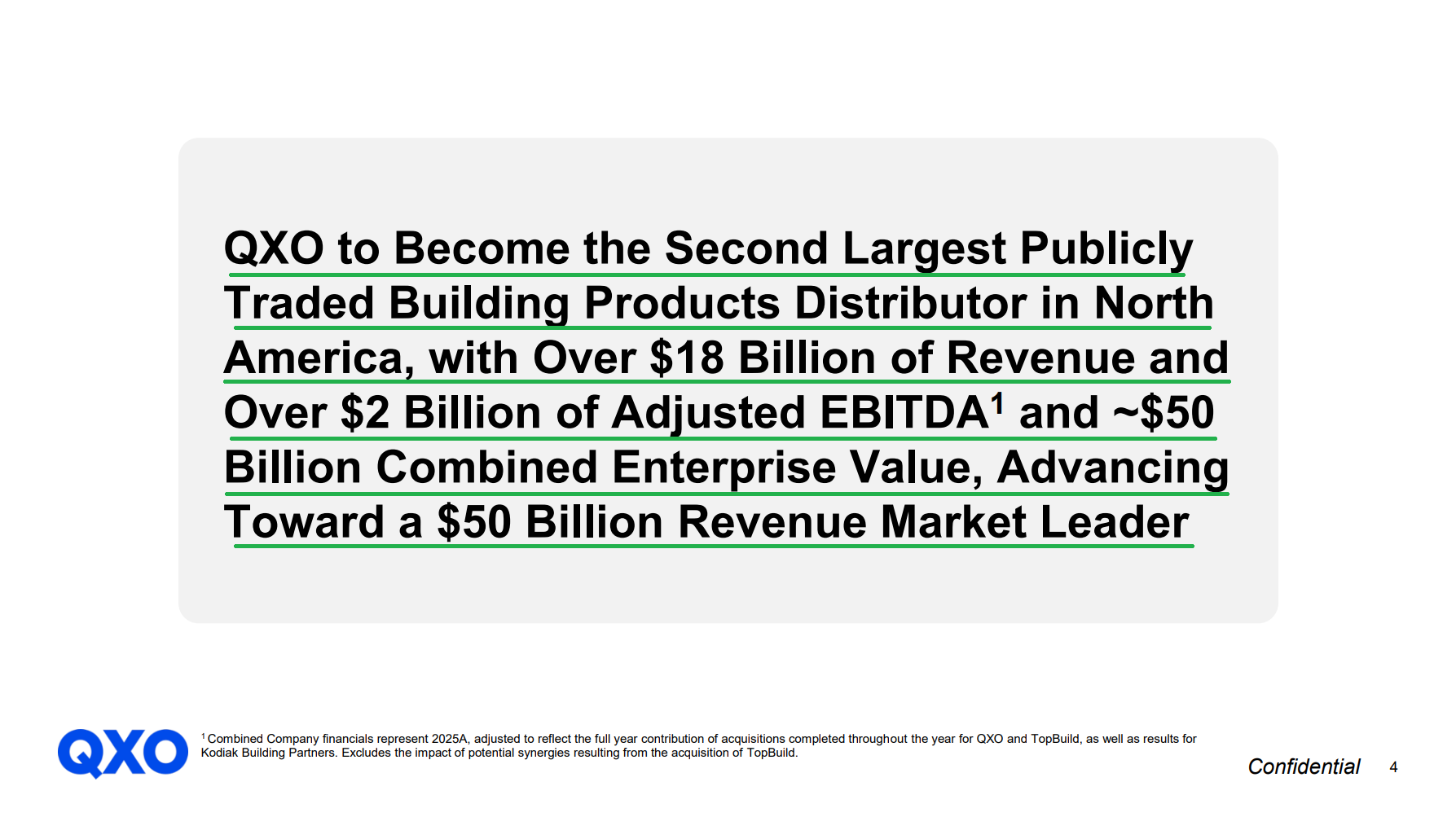

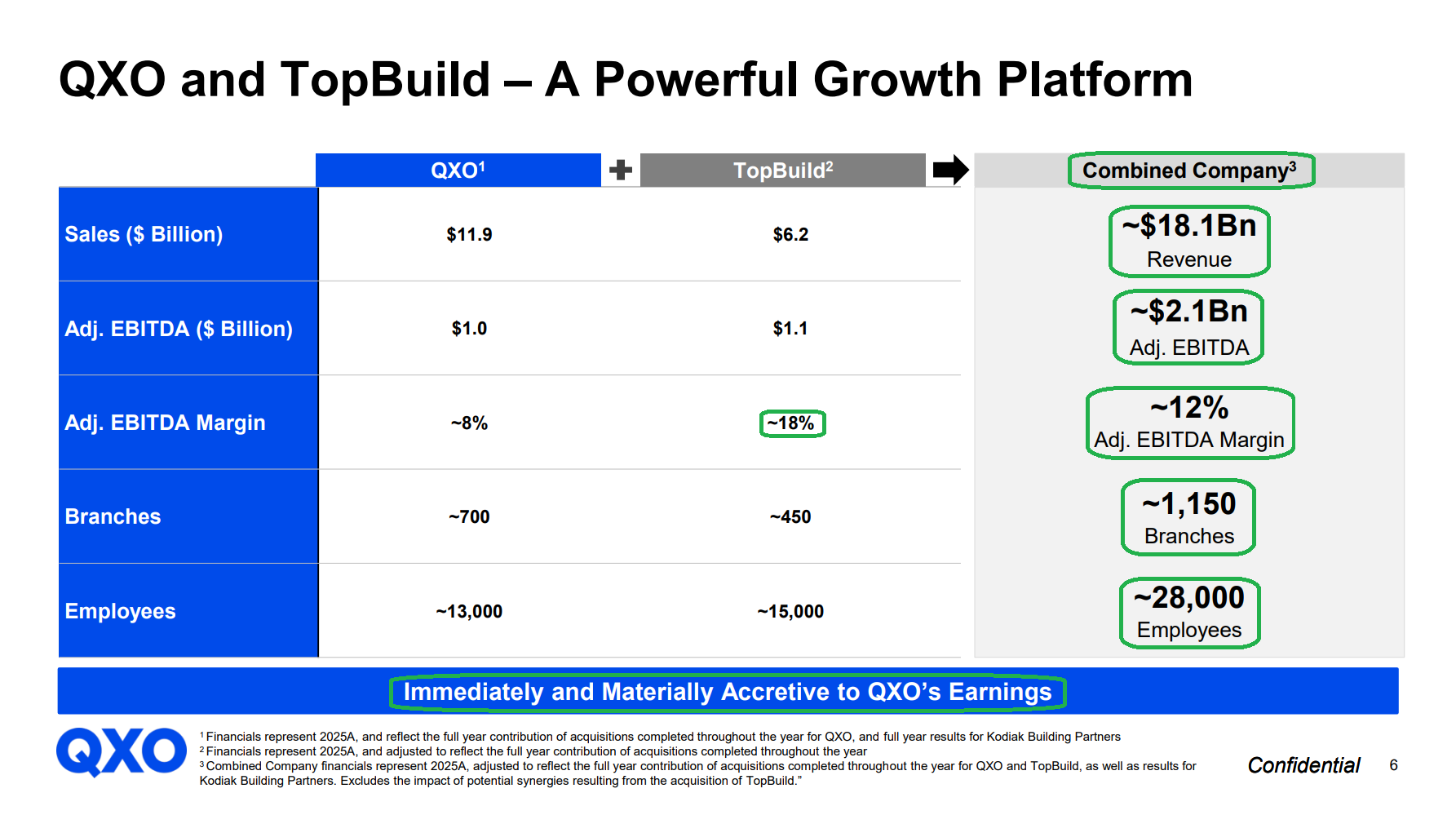

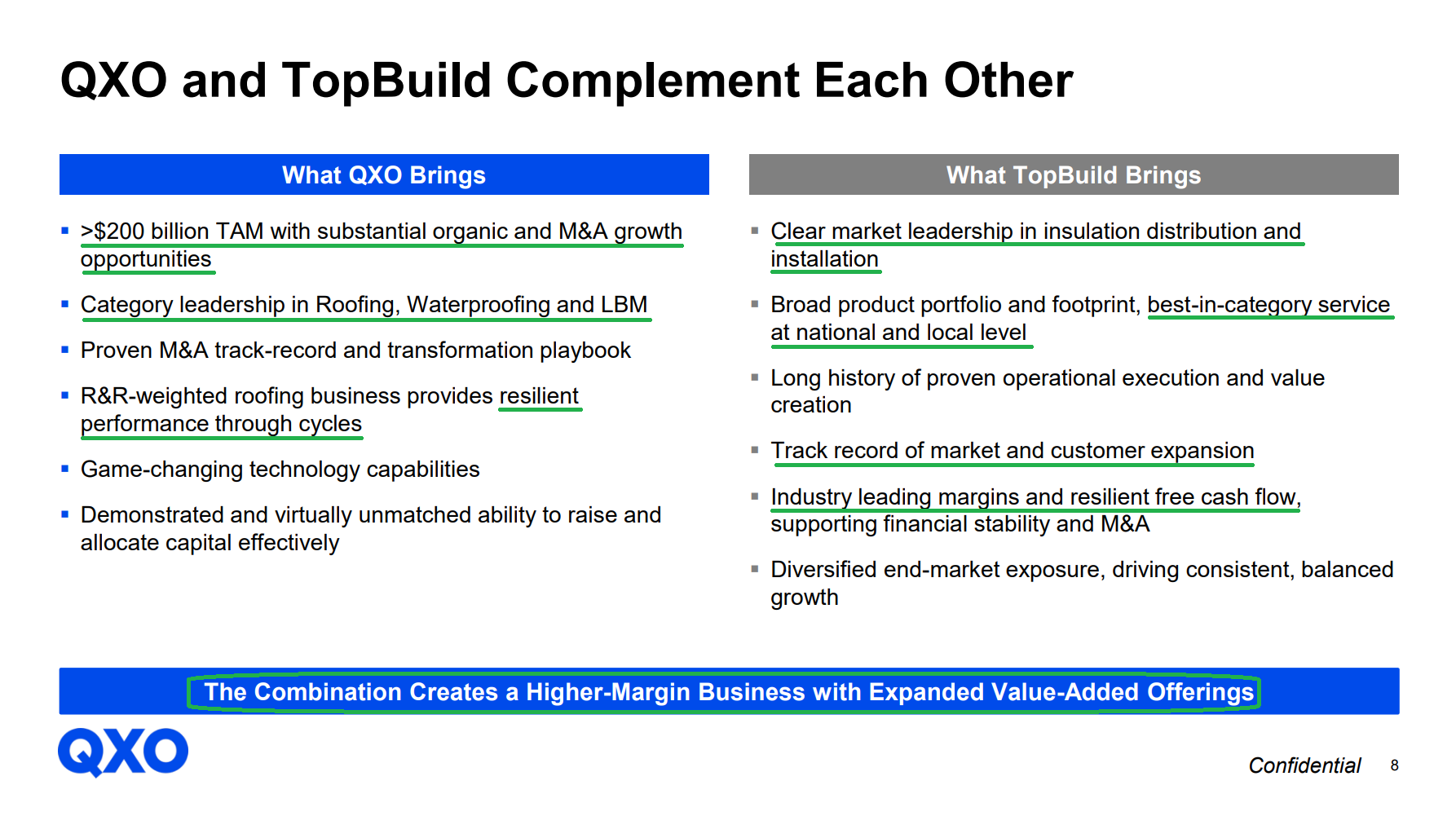

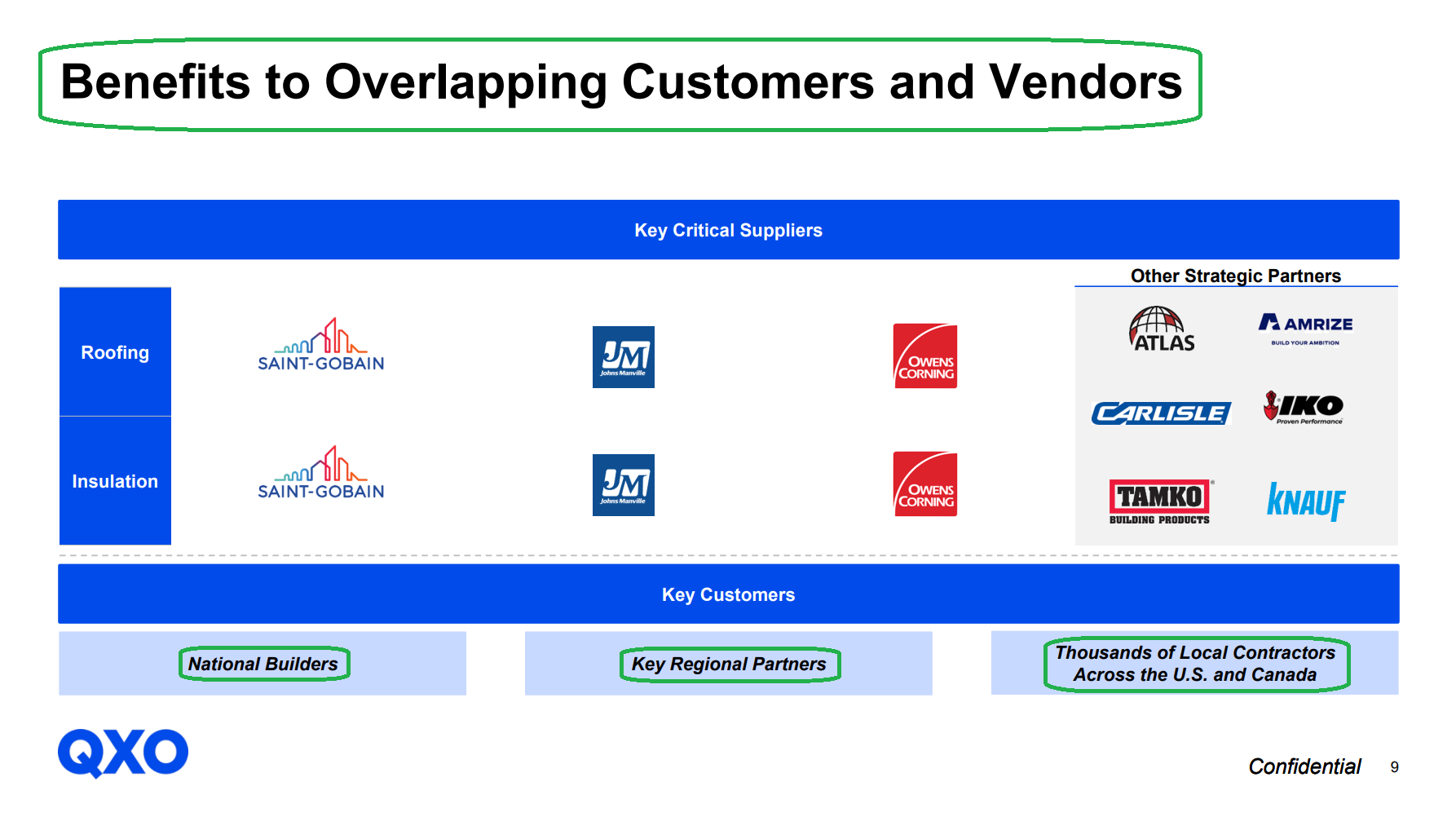

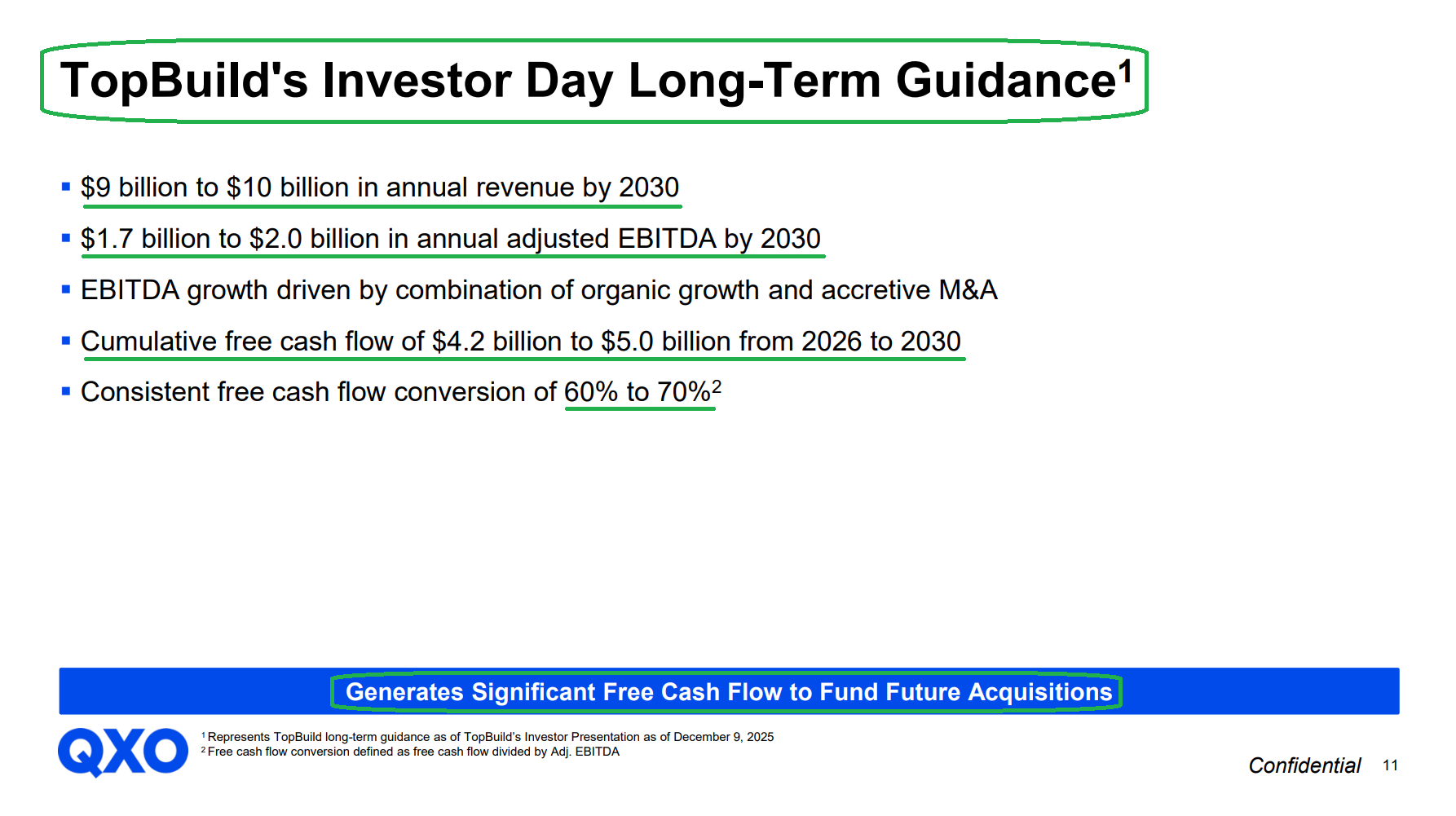

Strategically, the TopBuild acquisition is a game changer for the QXO story, starting with scale alone. The combined company generated ~$18.1B of revenue and ~$2.1B of adjusted EBITDA in 2025, with a combined enterprise value knocking on the door of ~$50B. The deal vaults QXO into the position of the second-largest publicly traded building products distributor in North America, behind only Ferguson (FERG), while adding ~$6.2B of incremental revenue and expanding the platform to a ~$300B+ addressable market. It also extends leadership across key categories, with #1 positions in insulation and waterproofing, #2 in roofing, and #1 or #2 positions in lumber and building materials across key geographies.

The combined platform also shifts toward a structurally higher and more durable earnings profile. Right now, QXO operates at ~8% EBITDA margins with heavy exposure to residential markets and ~80% of the mix tied to repair-and-remodel. TopBuild, by contrast, brings industry-leading ~18% margins and greater exposure to commercial and industrial end markets, including data centers, airports, warehouses, and stadiums. The result is a more balanced mix, shifting toward a ~50/50 split between repair-and-remodel and new construction, in turn creating a combined ~12% margin profile and leaving the company far less dependent on a purely residential cycle.

The final piece is proximity to the job site, arguably the most underappreciated aspect of the combined platform. TopBuild’s installation business places QXO on ~22,000 job sites daily, in turn providing real-time visibility into construction activity and demand patterns that supports cross-selling and higher wallet share per customer. It ultimately moves QXO toward a true one-stop shop, able to bundle insulation, roofing, waterproofing, and building materials into a single relationship for builders and contractors who would rather manage one supplier than five.

The market has yet to embrace any of these upside drivers. Combined with the broader backdrop of higher rates and ongoing input cost pressure, QXO shares have remained under pressure since the announcement. The debate comes down to two points of contention, both of which we view as overblown.

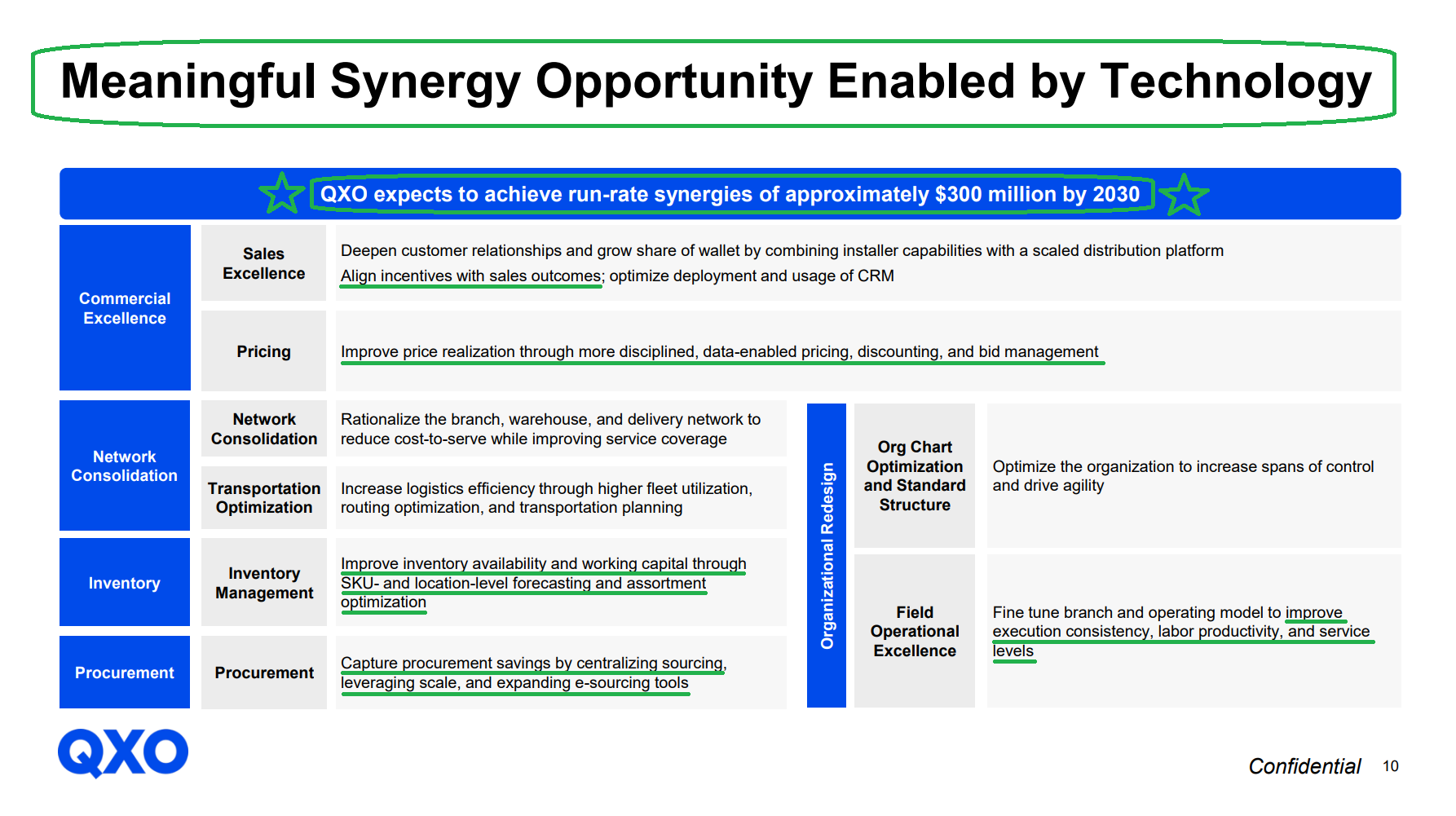

The first is price. Beacon was acquired at ~10.5x EBITDA and Kodiak at ~10.7x, making TopBuild at 14.9x look, at first glance, like a stretch. We see it differently. Beacon was a fixer-upper, an underutilized asset bought to be improved through pricing discipline and procurement. TopBuild is the opposite: a best-in-class operator already running ~18% margins, acquired not for what can be stripped out of it but for what it brings to the platform through cross-selling and commercial synergies. Including the expected ~$300M of run-rate synergies by 2030, the effective multiple steps down to ~11.8x, with further upside from execution over time. On that basis, it looks like a fair price for a high-quality asset, especially in the context of QXO’s cost of capital, which brings us to the next point.

The transaction is financed with ~$7.9B of new stock issued to TopBuild shareholders, ~$6.0B of new debt, a ~$1.0B preferred draw, and the remainder from cash on hand, leaving TopBuild holders with ~19% of the combined company on a fully diluted basis. While we are never fans of dilution as shareholders, this has to be viewed in the context of QXO’s cost of capital and the broader capital arbitrage strategy at work. Jacobs has run this framework across every platform he has built: raising equity ahead of large moves and issuing it at strength, then using it to acquire high-quality assets at cheaper relative valuations. In the case of QXO, management issued equity at ~$23.80 in January and struck the TopBuild equity component at an implied ~$25 per share, compared to the current share price of ~$16.94. For those concerned about dilution, just ask United Rentals (URI) shareholders, who were rewarded with a >200x bagger, or XPO (XPO) shareholders, who saw a >50x bagger for stomaching it during the buildout phase. Not to mention, Jacobs remains the largest single shareholder following his ~$900M initial investment, with any dilution occurring alongside shareholders rather than over them.

At the end of the day, Brad Jacobs continues to execute on the QXO strategy he set out to build. The goal of reaching ~$50B of revenue and ~$7.5B of EBITDA within the next decade remains firmly intact, with the combined Beacon, Kodiak, and TopBuild platform already locking in over a third of that trajectory just ~18 months into the platform’s formation. From here and while we wait for the housing cycle to turn, the focus shifts from transformational M&A to integration and execution, though anyone who has followed Jacobs over the years knows a great deal will never be left off the table…

TopBuild Acquisition Breakdown

Investor Q&A May 2026 Highlights

Quick Alibaba (BABA) Update

We wanted to put out a quick update on recent headlines and noise around Alibaba and other Chinese equities. A steady stream of so-called headwinds, many of which we view as overblown, has weighed on sentiment. In no way has it changed the fundamental story or our investment case. We’ve used recent weakness as a buying opportunity and continue to lean in. Below is our latest Alibaba deep dive, along with brief commentary on key recent headlines:

Pentagon Military List Designation: Alibaba was added on June 8 to the U.S. DoD Chinese Military Companies (CMC) list alongside BYD (BYDDY) and Baidu (BIDU), joining nearly every major Chinese tech name (Tencent (TCEHY), Huawei, DJI, etc.). The designation is procurement-related, carries no sanctions, and doesn’t affect normal business operations in the U.S. or elsewhere given no exposure to U.S. defense procurement. Alibaba has filed suit, arguing the listing is a mistake with no basis. Similar designations have previously been successfully challenged and removed (Xiaomi (XIACY)). While inclusion on the list makes for a headline, it has zero revenue or earnings impact.

618 / Subsidy Crackdown: The 618 mid-year shopping festival came in softer amid ongoing regulatory pressure on excessive discounting across e-commerce platforms. Ahead of the event, regulators met with the five major platforms on subsidies, false promotions, and “cut-throat competition,” continuing the push away from subsidy-driven growth that has eroded margins across the sector. This follows draft rules from the State Administration for Market Regulation targeting prolonged subsidy programs in food delivery and instant commerce. While the market’s initial reaction was negative, we view the crackdown as a long-term positive, with the subsidy war that has weighed on Alibaba’s profits likely past peak and earnings growth set to reaccelerate.

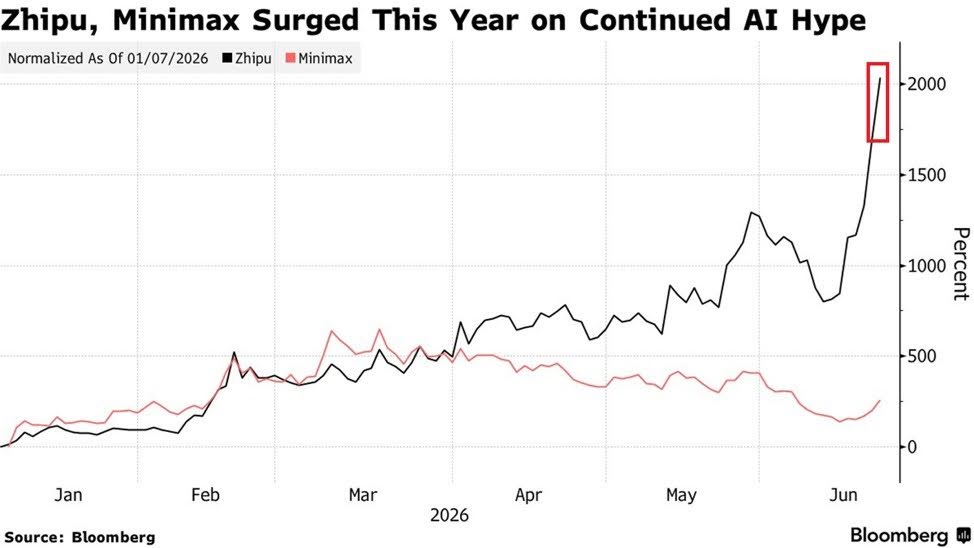

China AI Ecosystem: While money has rotated away from Chinese internet and consumer names in favor of AI “pure plays,” investors seem to have forgotten who sits at the center of the Chinese AI ecosystem: Alibaba. As China’s #1 full-stack AI player, Alibaba combines the country’s #1 cloud platform (~38% market share, larger than the combined share of the next three providers), proprietary chips, leading open-source models, and strategic stakes in names such as Zhipu, MiniMax, Moonshot, and 01.AI through compute-for-equity arrangements. The irony is that many of the AI “winners” attracting investor attention today are backed by Alibaba and run on Alibaba Cloud. Shares of Zhipu are up ~2,000% this year and MiniMax has gained ~260%, yet both sit squarely within Alibaba’s ecosystem. To put the disconnect into perspective, Zhipu now carries a market cap of ~$130.0B despite generating just ~$105.0M of revenue in 2025. By comparison, Alibaba Cloud alone generated ~$22.9B of revenue last year, while Alibaba as a whole generated ~$148.4B of revenue and carries a market cap of ~$240.0B. Complete silly season!

Consumer Weakness: Chinese consumer confidence has fallen to one-year lows, while May retail sales declined 0.6% Y/Y, marking the first contraction since the economy reopened in late 2022. We continue to view this as a cyclical rather than structural issue, with weak sentiment creating the potential for additional policy support to help drive a recovery. Meanwhile, the market remains fixated on near-term consumer weakness despite Cloud and AI increasingly driving the story.

Government Data Centers: China’s ~$295B data center buildout over the next five years sparked concerns that government-funded capacity could undercut private cloud operators, with Alibaba the most exposed. Analysts at Citi (C) pushed back on this view, and we certainly agree, arguing the reaction is overdone and not a zero-sum outcome for hyperscalers like Alibaba. Capacity is expected to broaden AI access for state-owned companies and smaller businesses that cannot afford higher token costs, while private players continue to serve higher-value enterprise workloads. Rather than a headwind, this could even be additive for Alibaba via lower capex intensity and greater flexibility to allocate capital toward chips, models, and higher-value AI services.

Buybacks: Just as we have been leaning into weakness amid headline-driven volatility, management has followed suit with reinstated buybacks, with Alibaba repurchasing ~1.9M shares over the past two days. With a net cash position of ~$38B (~$59B excluding long-dated debt), the company continues to have plenty of dry powder to retire more cheap shares should weakness persist.

General Market

The CNN “Fear and Greed Index” ticked down to 28 this week from 44 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

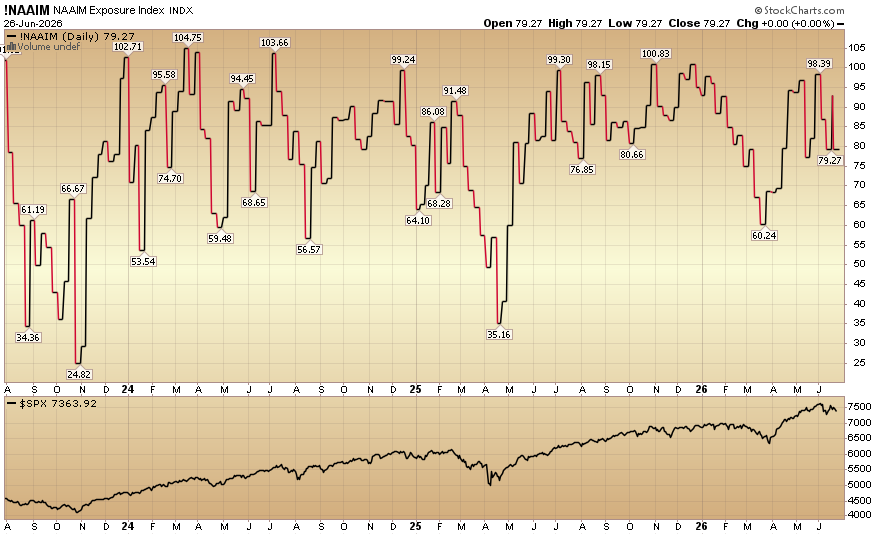

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) held steady at 79.27% equity exposure this week.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms

Comments

Log in or sign up to join the conversation.