Charles High Smith writes, “In the conventional investment perspective, risk-on assets (i.e. investments with higher risks and higher potential returns) such as stocks are on a see-saw with risk-off assets (investments with lower returns and lower risk, such as Treasury bonds). When risk appetites are high, institutional managers and speculators move money into stocks and high-yield junk bonds, and move money out of safe-haven assets such as gold and U.S. Treasuries.

But recently, markets are no longer following this convention. Safe haven assets such as precious metals and Treasuries are soaring at the same time that stock markets bounced strongly off the post-Brexit lows.

Risk-on assets (stocks) rising at the same time as safe-haven assets is akin to dogs marrying cats and living happily ever after.

What the heck is going on?

Why is the market acting so schizophrenic? What’s changed?”

The decades-long influence of Keynes and the central banks have turned the world on its ear. There are bubbles in stocks, bonds, commodities and, yes, “safe havens” as well.This may be the turning point.

VIX was clubbed on Thursday and again on Friday, even with potential systemic risk hanging over the markets. After all, the market still appears awesome, doesn’t it? As a result, it exceeded its “normal” decline of 30-50% back inside the Broadening formation by another 28%. However, payback is coming in a very big way. The entire Wave structure from last August is a huge Bullish Flag with a potential target that is well above the August high.

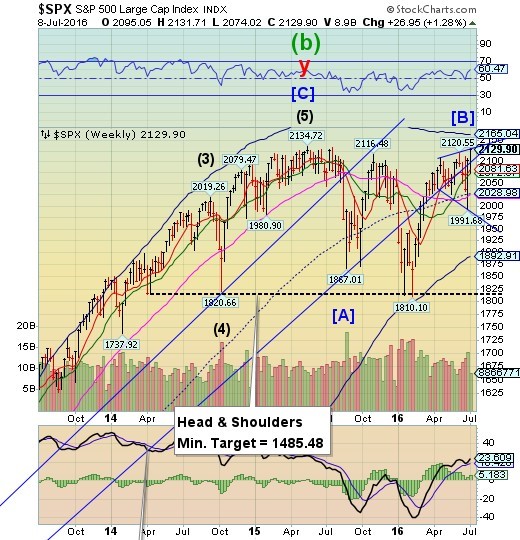

(Investing) From a big-picture VIX perspective, the price structure is pressing toward a test of its year-long support line -- in the vicinity of 12.75 -- while at the same time, SPX is pushing up toward a confrontation with every prior high since May 2015, between 2120 and 2134.72.

Friday's mid-day high was 2120.08, which corresponded to an intra-day VIX low at 13.38.

SPX reaches point 5 of tis Broadening Top.

SPX rallied to point 5 of its Orthodox Broadening Top at Friday’s close.This is known as the “terminal top” from which a decline may begin. A decline beneath 2100.00 may set a new sell- off in motion.So, who’s buying this rally?

(WSJ) A boost in hiring in June catapulted the S&P 500 right near its record closing high and lifted all major U.S. stock indexes back to where they were before the U. K. ’svote tol eave the European Union.

The S&P 500 rose 1.5% to close at 2129.90.

In intraday trade, it rose as high as 2131.71, climbing above its record closing level of 2130.82, hit on May 21, 2015.

(By the way, does anyone see the mismatched comparison in this article?)

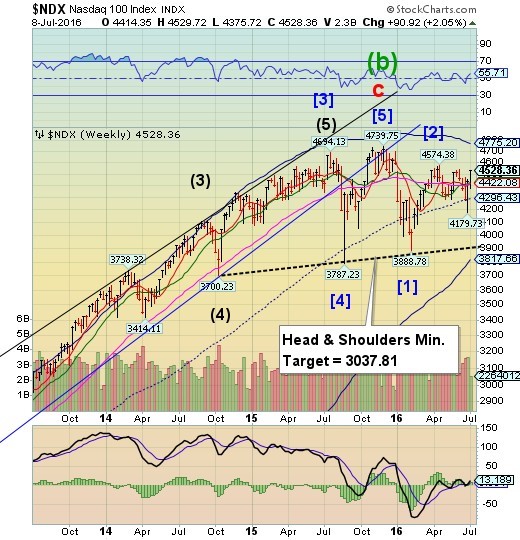

NDX surges, but stil has Y-T-D losses.

NDX surged, but could not overcome its June 6 high of 4536.55, nor could it make up the difference to the December 31 close at 4593.27, leaving a year-to-date loss.A failure beneath Long-term support at 4422.08 sets a potential panic decline in motion. The Head & Shoulders neckline at 3900.00 appears to be the next significant formation to be challenged. This appears to be the end of the summer rally and the beginning of seasonal weakness that may last several months.

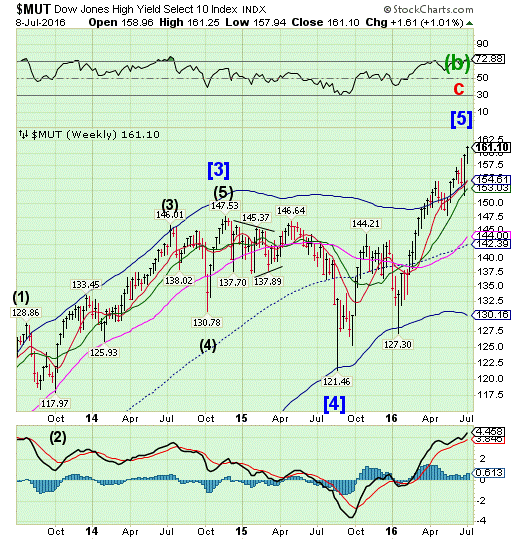

High Yield Bond Index makes a blow-off top.

The High Yield Bond Index made a blow-off top to its highest point, ever. Note that it reacts to the same pivots as equities, making its high on the same day as the SPX. Investors should now be on the alert for a decline beneath its Intermediate-term support at 153.03 for a probable sell signal. Did the strong issuance of corporate investment grade (IG) bonds crowd out High Yield last week?

(ZeroHedge) The M&A deal was just the beginning. As Reuters reports, the scramble for IG debt is on full force today:

- AT LEAST TEN INVESTMENT GRADE COPRORATE BOND DEALS EXPECTED TO SELL THURSDAY - MKT SOURCES

- DISNEY, AMERICAN HONDA FINANCE, RAYMOND JAMES, SUNOCO, SUMITOMO AMONG ISSUERS EXPECTED - MKT SOURCES

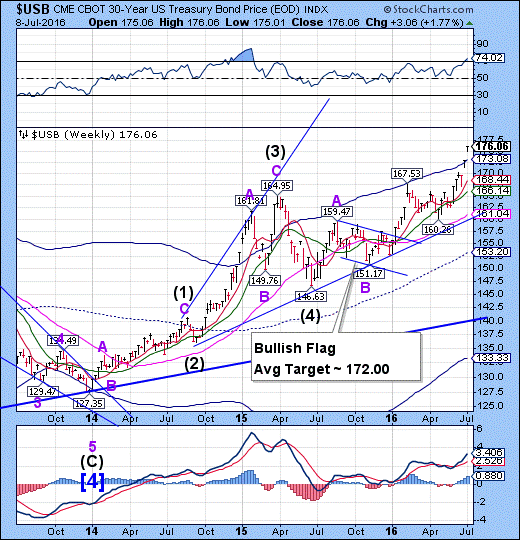

USB exceeds its target in a throw-over.

The Long Bond gapped higher as it exceeded all long-term and short-term targets.The problem is that throw-overs are unsustainable and that the cyclical period of strength has run beyond its normal time.Prepare for a reversal early next week.A decline beneath its Cycle Top at 173.08 may be the first indication that the rally may be over..

(WSJ) The yield on the 10-year Treasury note set a record low on Friday despite an encouraging employment report, underscoring the growing influence of global factors in setting benchmark U.S. interest rates.

The 10-year yield settled at 1.366%, narrowly beating out the previous record closing low of 1.367% set on Tuesday. It hit an intraday low of 1.321% on Wednesday and closed Thursday at 1.387%

Yields fall as bond prices rise.

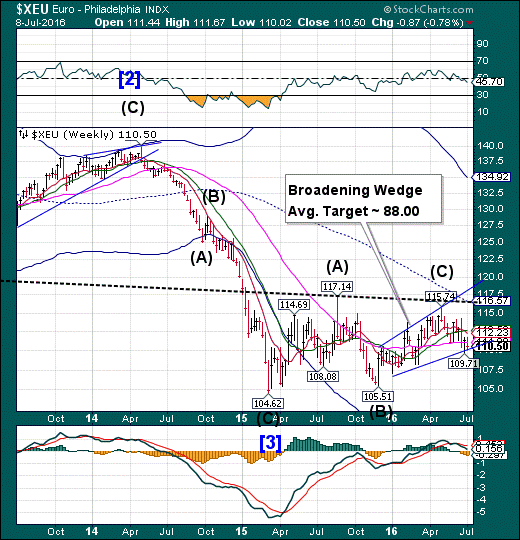

The Euro is between trendline support and Long-term resistance.

The Euro bounced from the lower trendline of its Broadening Wedge formation, but closed beneath Long-term support/resistance at 111.00.A break of the trendline may put the Euro back into a bear market with the loss of that key support.The next area for a bounce may be the 104.00 to 106.00 area as it retests it former lows.

(Bloomberg) The International Monetary Fund urged the European Central Bank to consider expanding its asset-purchase program if inflation in the euro area doesn’t rise from current low levels.

“Given the very weak outlook for inflation, the ECB should stand ready to ease further if inflation remains below its anticipated adjustment path,” IMF staff said Friday in an Article IV report on the euro area. “Dis-inflationary pressures remain strong with 11 countries reporting negative inflation in May” and “with second-round effects weighing on core inflation.”

EuroStoxx retests its Cycle Bottom support.

The EuroStoxx 50 Index retested its Cycle Bottom support only to make a partial retracement. The trend is clearly down and the bouncetemporarily relieves its oversold condition. A resumption of the decline beneath the neckline at 2615.00 may trigger an even stronger sell-off.

(Reuters) European shares rose on Friday, ending a week of losses on a positive note with Milan outperforming thanks to a rally in its battered baking stocks.

Equities got a boost late in the session from a stronger-than-expected jobs report in the United States.

The pan-European STOXX Europe 600 rose 1.6 percent but still ended the week with a loss of

1.5 percent due to persistent worries over the economic and political fall-out of Britain's vote on

June 23 to leave the European Union.

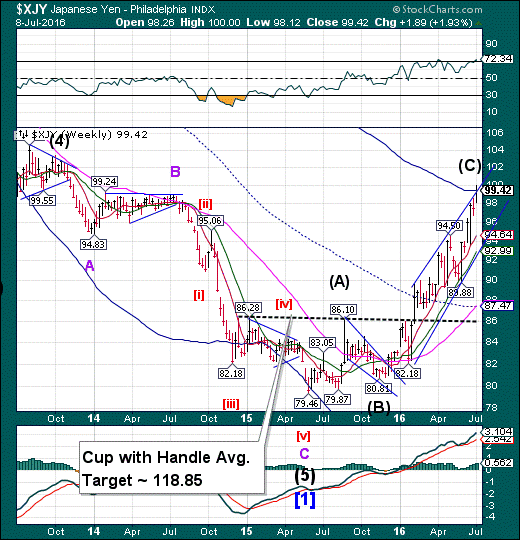

The Yen throws over its Cycle Top.

The Yen threw-over the upper trendline of its trading channel and its Cycle Top resistance. Last week I suggested, “Round numbers are attractors, so it is probable that the rally may continue to 100.00, or at least make another attempt at it.”The probable period of strength may last a few more days, if not the remainder of the week. A breakout above the Cycle Top may lengthen the rally.

(Bloomberg) The yen is the best-performing Group-of-10 currency this year as the U.K.’s decision to leave the European Union spurs expectations that the Federal Reserve will hold rates for longer while stoking demand for safer assets.

Here are four charts to show why the yen may keep rising. Rising External Surplus The 10-month moving average of Japan’s current-account surplus is at its highest level since 2010 on rising investment income. The yen’s value against a basket of its peers tends to track the current account with a 12-month lag.

The Nikkei revisits the neckline.

The Nikkei declined back to its Head & Shoulders neckline, suggesting that the decline beneath the neckline may resume in earnest.A failure to hold above the neckline may bring on the panic phase of the decline..

(Investing) Japan stocks were lower after the close on Friday, as losses in the Real Estate, Trading and Retail sectors led shares lower.

At the close in Tokyo, the Nikkei 225 fell 1.11%.

The best performers of the session on the Nikkei 225 were Nippon Light Metal Holdings Co. (T:5703), which rose 2.37% or 5.0 points to trade at 216.0 at the close. Meanwhile, Tokyo Electron Ltd. (T:8035) added 1.90% or 158.0 points to end at 8490.0 and NEC Corp.(T:6701) was up 1.64% or 4.0 points to 248.0 in late trade.

The worst performers of the session were Asahi Glass Co., Ltd. (T:5201), which fell 8.24% or 44.0 points to trade at 490.0 at the close. Furukawa Co., Ltd. (T:5715) declined 5.38% or 7.0 points to end at 123.0 and Mitsui Fudosan Co., Ltd. (T:8801) was down 4.50% or 96.0 points to 2039.0.

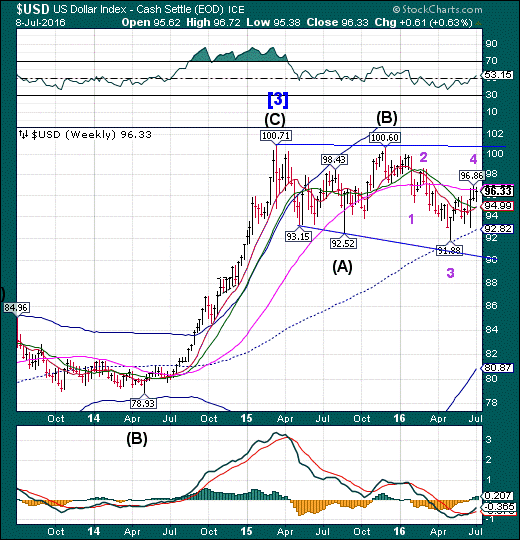

U.S. Dollar challenges Long-term resistance.

USD continued to challenge its Long-term resistance at 96.55 for a third week. The Cycles Model suggests that a decline may commence in the next week.

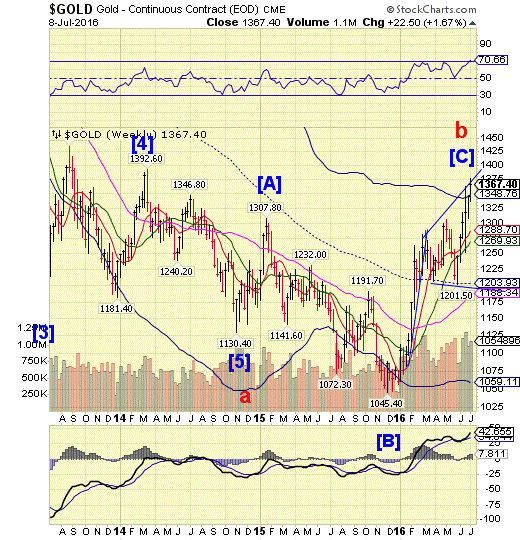

Gold makes a new high point in the Broadening Top.

Gold made a strong pullback, but went for the top trendline of its Orthodox Broadening Top for a second time. Last week I mentioned, “Next week may be instructive whether this is a bona-fide reversal.” The probe higher was needed to complete a topping pattern within the formation.

(CNBC) Gold had a hard time making up its mind about Friday's jobs report.

In the 20 minutes before the number came out, gold futures first rose about $10, before promptly giving up those gains. At the second before the number was released at 8:30 a.m. EDT, gold was sitting at $1,356.5 per troy ounce.

On the initial news that the nonfarm payrolls number was more than 100,000 above economists' expectation, gold did what one would probably expect, given the precious metal's function as a bet on market fear and on more stimulative Federal Reserve policy: It gapped down on heavy volume, bottoming out at $1,336.3 in the minute after the release.

Yet once that level was hit, gold staged a major turnabout, rising as high as $1,371.8 at 9:15 EDT.

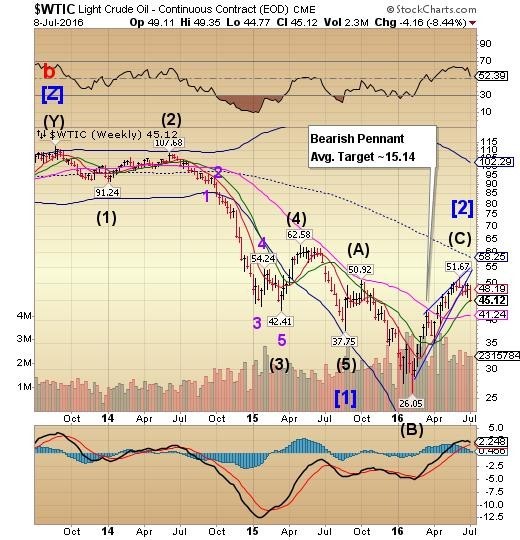

Crude begins its decline.

Crude declined to its Intermediate-term support at 45.10 this week.A failure at this support may be viewed as a sell signal for crude. It suggests an initial drop to challenge the prior low at 26.05 with a more substantial decline to follow.

(OilPrice) OPEC has captured its largest share of the oil market since 1975, which could be seen as a vindication of the cartel’s strategy over the past two years. But it also creates vulnerabilities for the U.S. and others, who are once again increasingly dependent on the Middle East for oil.

OPEC and its de facto leader Saudi Arabia have pursued market share over the past two years, and with great success. Rather than curtailing production in order to prop up prices, OPEC members ran horrific budget deficits and kept output elevated. That crushed crude oil prices, and has forced many high-cost drillers out of the market – and continues to do so. Even though the overall benefit to OPEC is questionable given the huge revenue losses, OPEC has emerged with its largest market share in forty years.

Shanghai Index attmepts a rally out of its consolidation.

The Shanghai Index rallied above its sideways consolidation but did not regain its mid-cycle resistance at 3109.51. The Cycles Model suggests that a decline may begin next week,. lasting through the end of the month.

(ZeroHedge) As we have covered ad nauseam, companies who rushed to perform the most altruistic of favors to workers by raising wages are now facing the realization that profitability simply can't be maintained, and thus are taking measures to cut costs (ie: firing people or reducing hours).

Our current title holder for most actions taken as a result of trying to appease the living wage crowd is WalMart of course, who has already closed stores and fired massive amounts of people as a result of increasing wages. More efforts are also on the way, recall that WalMart is also testing the use of drones in distribution facilities in order to facilitate even more layoffs.

Now, just as the case was with Starbucks, WalMart is tinkering with employee work hours in order to try and figure out a way to reduce costs but make it appear as though that isn't the case. This time, however, the company is testing it out in China, which unlike the US is unionized and will be much more disruptive to operations as the unions begin to protest the change in hours.

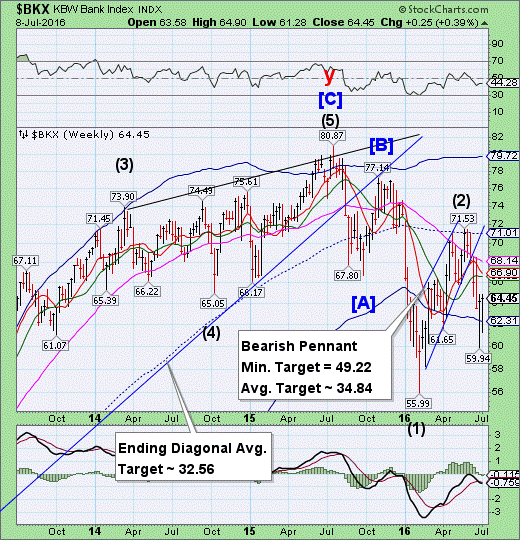

The Banking Index challenges the Cycle Bottom again.

-- BKX bounced out of its Master Cycle low on June 27. A second week of attempted rally did not get BKX appreciably higher. Should the bounce be finished, the decline may resume through early August..

(ZeroHedge) Next week the second quarter earnings season begins in earnest (as usual with Alcoa reporting after the close on Monday), with some 5% of the S&P reporting Q2 results, a number which will rise to 89% by August 5.

During this period, most corporate buybacks, arguably the only source of stock buying, will remain in a blackout period. Whether this means the S&P will again remain rangebound for the next 4 weeks is unclear: with rampant central bank intervention now a daily fixture of "markets", it remains a folly to attempt any predictions.

A more interesting question will be what earnings will be reported. As is widely known, Q2 will be the fifth consecutive quarter of declining earnings, the first time this has happened since the financial crisis. Curiously, in just the past week, analysts have further taken down their estimates, with average EPS now seen a declining 5.6% from a year ago, compared to a drop of 5.4% as of June 30 (with revenue set to drop by 0.7% Y/Y).

(ZeroHedge) When most recently reporting on the latest European banking crisis, yesterday we observed a surprising development involving Deutsche Bank, namely the bank's decision to quietly liquidate some of its shipping loans. As Reuters reported, "Deutsche Bank is looking to sell at least $1 billion of shipping loans to lighten its exposure to the sector whose lenders face closer scrutiny from the European Central Bank.

"They are looking to lighten their portfolio and this includes toxic debt. It makes commercial sense to try and sell off some of their book," one finance source said. Deutsche Bank, which has around $5 billion to $6 billion worth of total exposure to the shipping sector, declined to comment."

This confirms what had long been speculated, if not confirmed, namely that German banks have been some of the biggest lenders to the shipping sector, a sector which has since found itself in significant trouble as a result of the ongoing slowdown in global trade.

(ZeroHedge) Have no fear, Banco Popolare has run its own stress test (on itself) and has stated that it is "resilient to shocks." However, it appears investors do not believe them as Italian banks, led by Monte Paschi (which as a reminder is under a short-sale ban) plunged to new record lows.

Banco Popolare SC said stress tests using the same criteria as the European Banking Authority’s review later this month show the Italian lender’s “resilience” to adverse shocks.

This is far from over!!

Comments

Log in or sign up to join the conversation.