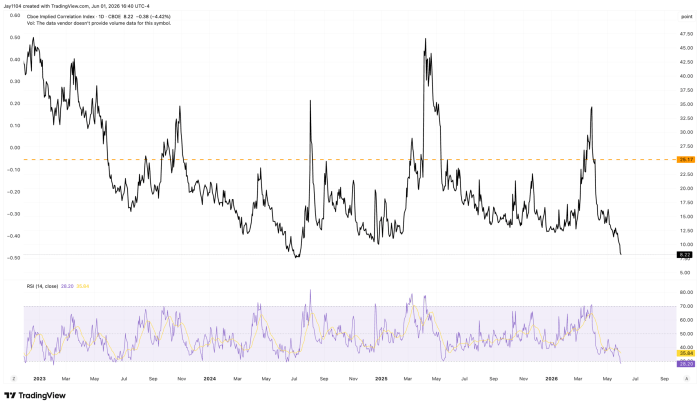

The S&P 500 finished the day higher by around 26 bps, while dispersion continued to rise and correlations moved lower. The 3-month implied correlation index closed at 8.22, its lowest level since July 2024, when it closed at 7.6.

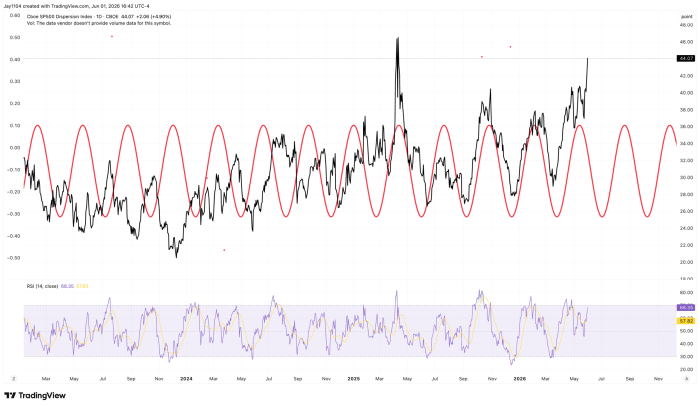

Meanwhile, the dispersion index rose to 44 today, closing at its highest level since April 2025.

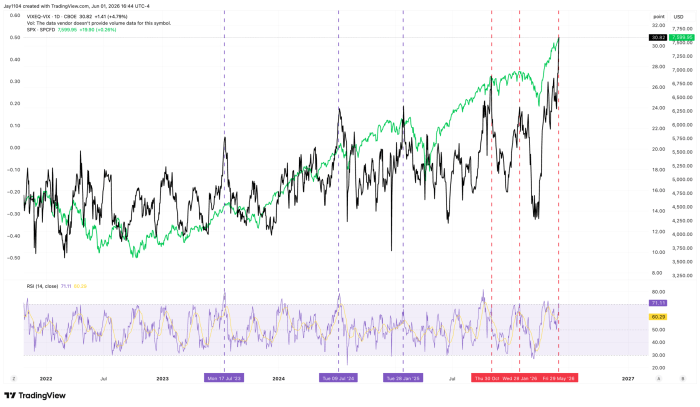

The reason this continues is that single-stock volatility keeps rising, with the spread between the VIXEQ and the VIX now at 30.8, its widest level on record. Historically, spikes in this spread have been associated with fairly sizable market pullbacks.

At some point, the trade will likely reverse, and the long single-stock volatility positions that have helped fuel this move will begin to unwind. When that happens, it could create a meaningful shift in market dynamics, as the index vol side unwinds too.

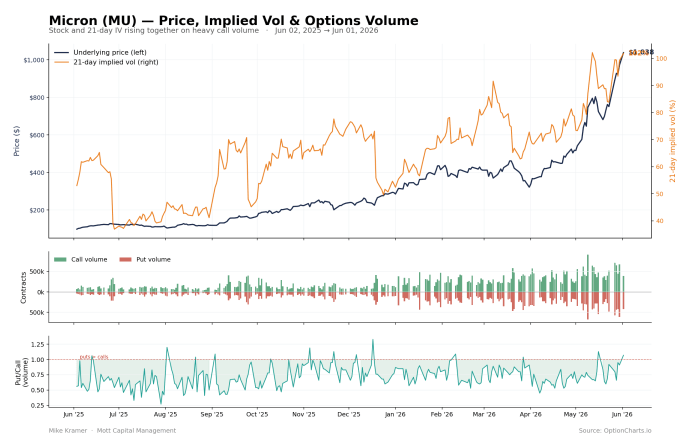

We can see that implied volatility for Micron (MU) continued to rise today, with the 21-day implied volatility rising to 101.9%. One thing I found interesting was that the put-to-call ratio rose to 1.07.

Maybe it means something, maybe it doesn’t, but it is the first time in a while that put volume has exceeded call volume. From the looks of the data, call volume was also weaker today than it has been recently. That could matter because, as implied volatility rises, call options become increasingly expensive, and at some point, you would expect demand for calls to begin to subside.

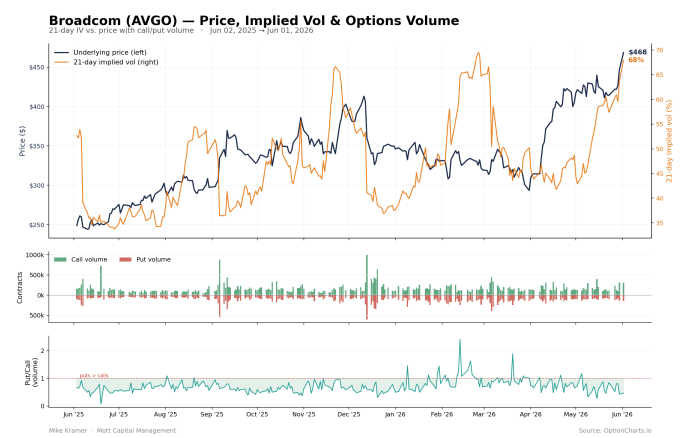

The point is that, with implied volatilities rising across many stocks in the semiconductor space, including names like IBM, this is one reason we continue to see dispersion rise and correlations fall. Broadcom (AVGO) is another stock experiencing a sharp increase in implied volatility, with the key difference being that it is scheduled to report earnings on June 3 after the close.

The thing to watch is what happens after Broadcom reports. Implied volatility should fall sharply following the earnings release. Whether that triggers a broader cascade across the rest of the sector will be something worth monitoring.

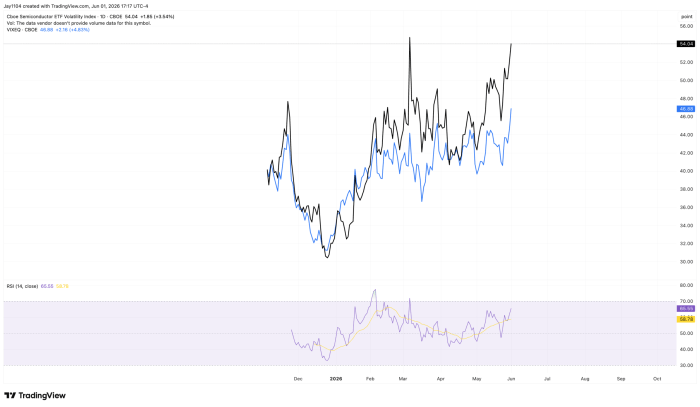

The SMH implied volatility index, for which we have a very small sample size, closed at 54. This appears to be the key IV index to watch over the next few days, considering that the VIXEQ and VXSMH have closely followed one another.

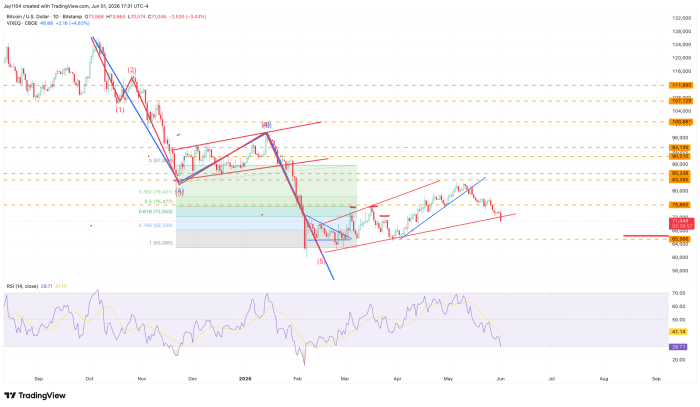

Finally, my preferred liquidity gauge, otherwise known as Bitcoin (BTC.X), fell by more than 3% today and broke below an uptrend around $72,000 that can be traced back to February. I do not think a decline to $66,000 can be ruled out at this point, as that appears to be the next meaningful level of support.

Comments

Log in or sign up to join the conversation.