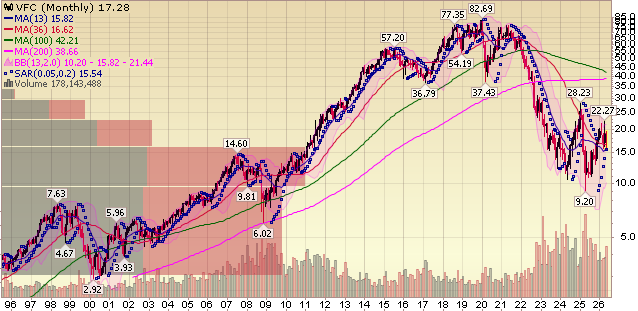

VF Corp (VFC) Update

For newer readers, here’s a quick overview of the key drivers behind our thesis on VF Corp, a global apparel and footwear leader with a portfolio of iconic brands, now firmly in the growth phase of its turnaround with significant operating leverage ahead:

It’s been nearly three years since Bracken Darrell took the helm at VF Corp, and he and his team have delivered on nearly every major objective outlined from day one.

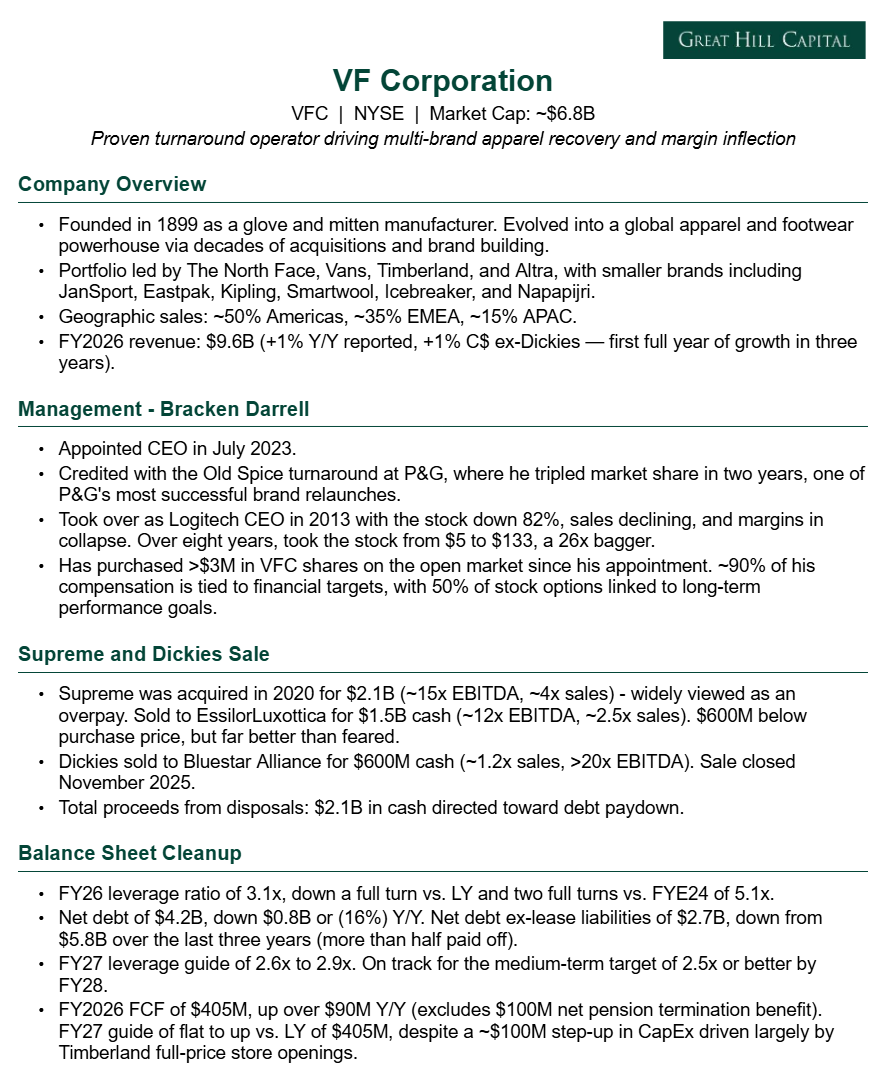

The turnaround was always a two-phase job, with the first phase centered on the unglamorous but necessary work of reducing costs and repairing an overleveraged balance sheet.

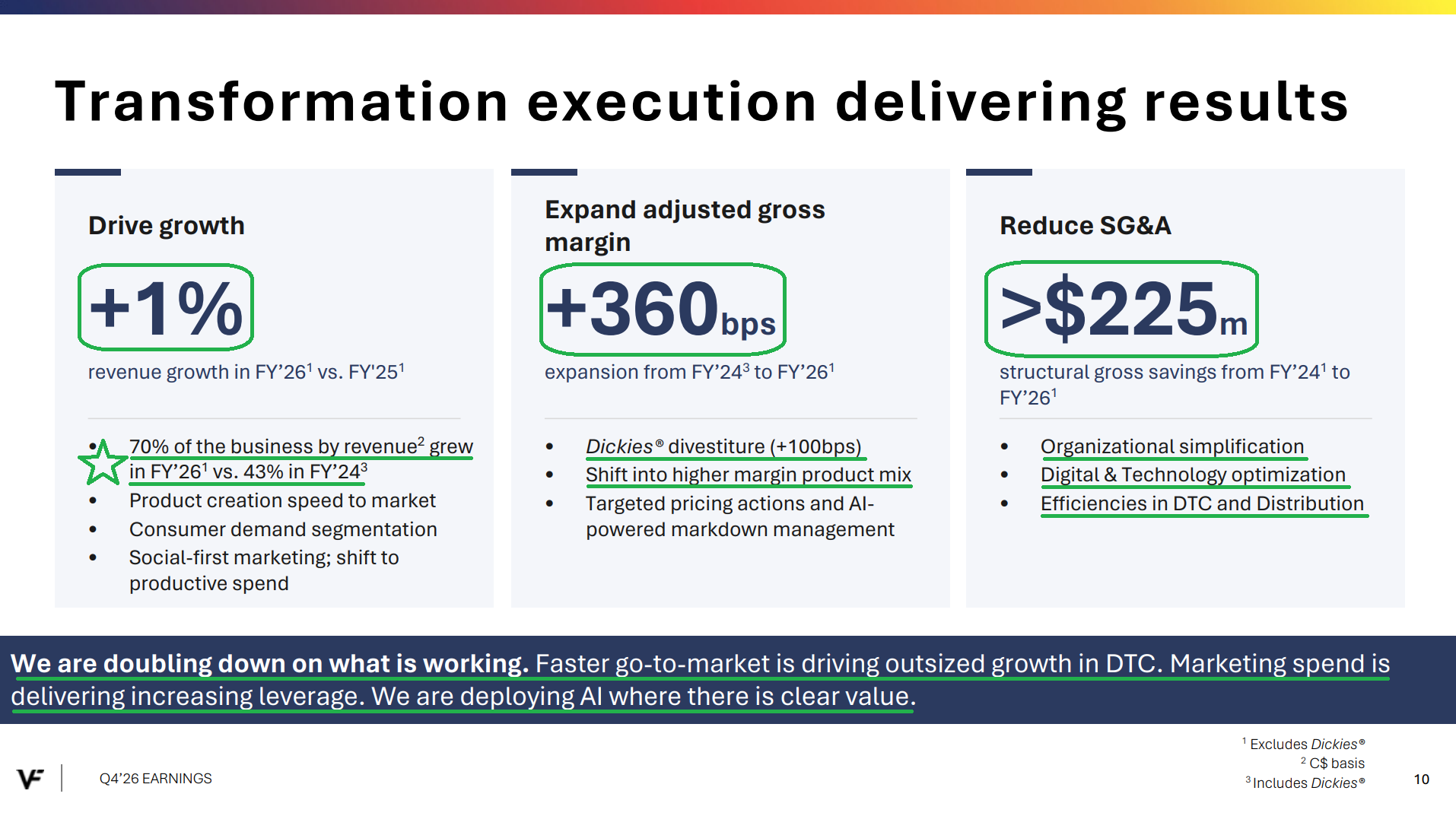

On the cost side, management has removed more than $225M of structural SG&A from the business since FY24. Those savings are now fully embedded in the run rate, helping expand operating margins by +220 bps to 7.0% while keeping the company on track to achieve its 10% operating margin exit rate target by FY28.

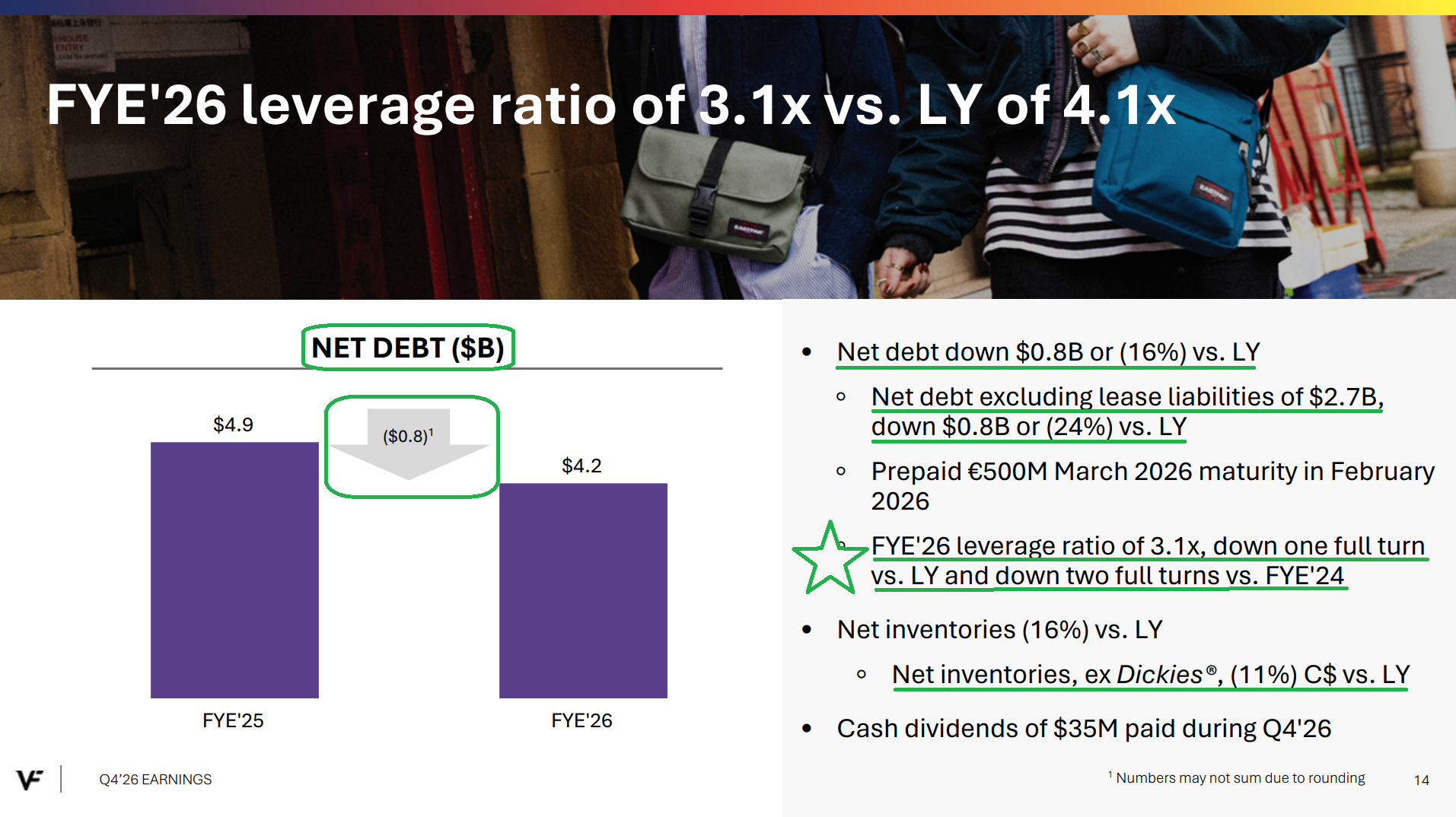

On the balance sheet, the divestitures of Supreme ($1.5B) and Dickies ($600M) helped reduce net debt (excluding lease liabilities) from $5.8B three years ago to $2.7B today. Leverage has fallen from 5.1x to 3.1x, putting any lingering solvency concerns firmly to bed and leaving VF on track to nearly reach its 2.5x leverage target a FULL YEAR ahead of schedule.

With both of those boxes now checked, the restructuring chapter of the turnaround is now in the rear view mirror, shifting the focus to something far more exciting: growth.

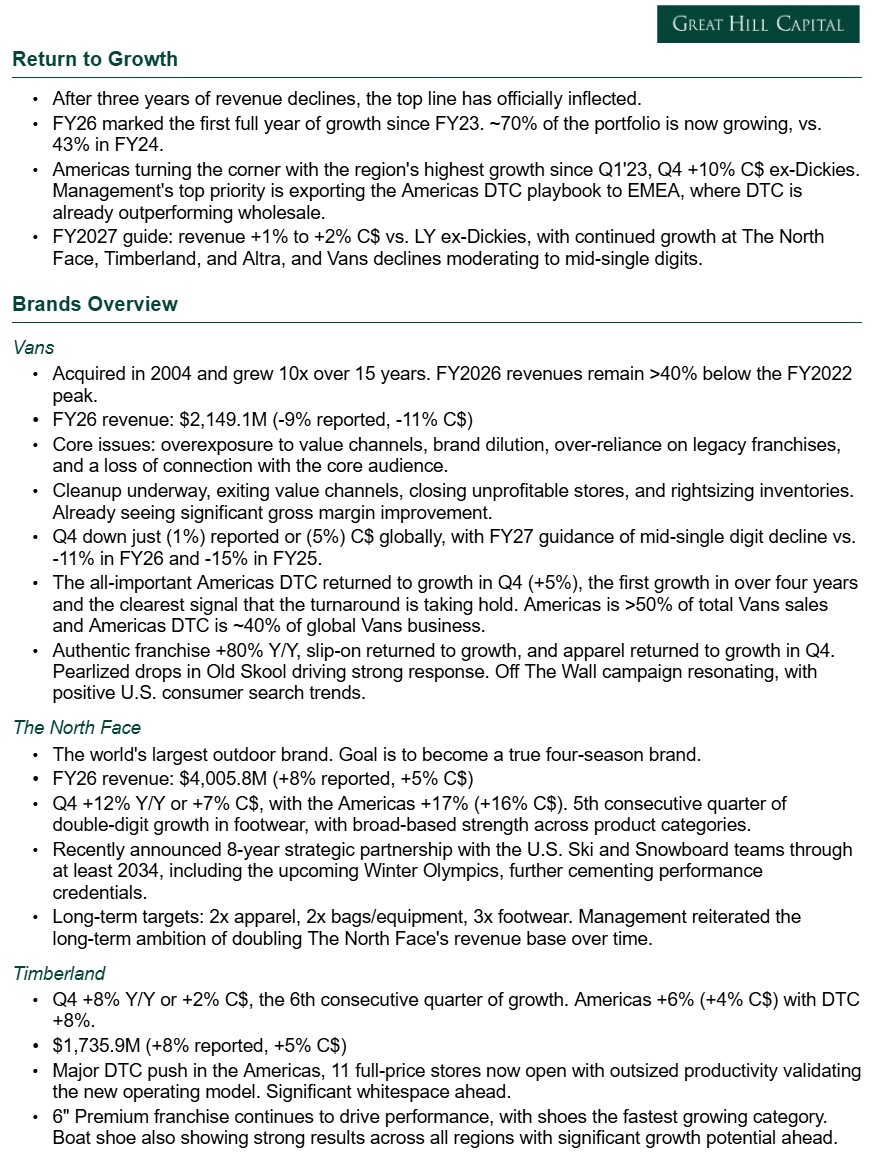

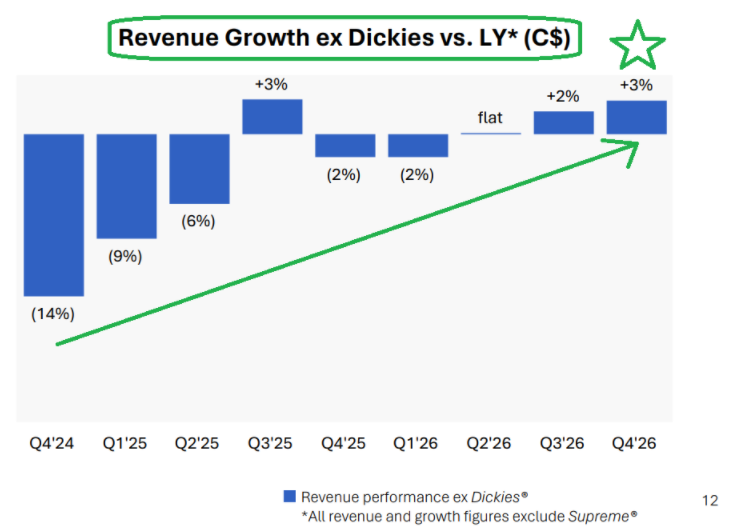

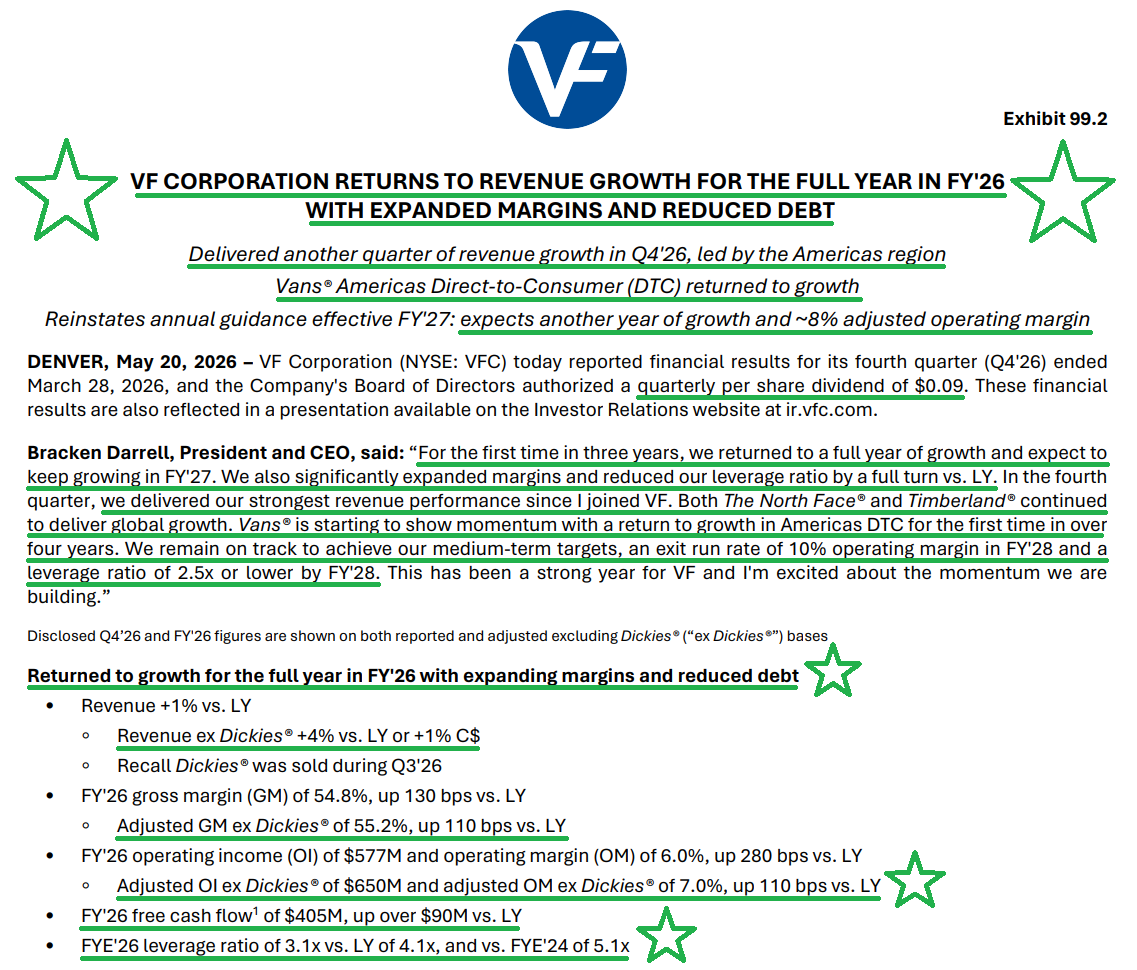

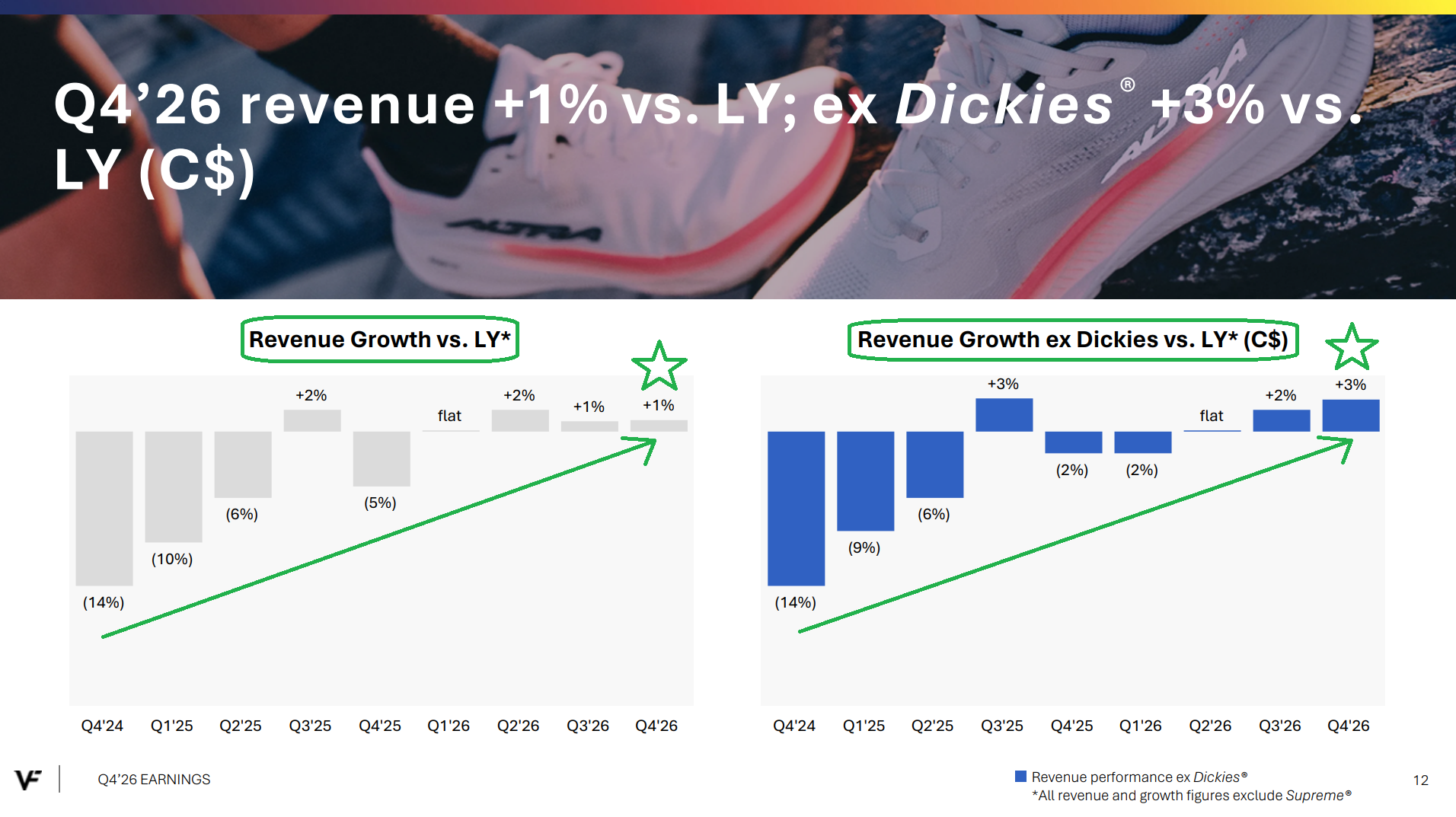

FY26 marked the first full year of revenue growth in three years, with revenue up +4% (+1% C$ ex-Dickies), while ~70% of the portfolio is now growing compared to just 43% in FY24.

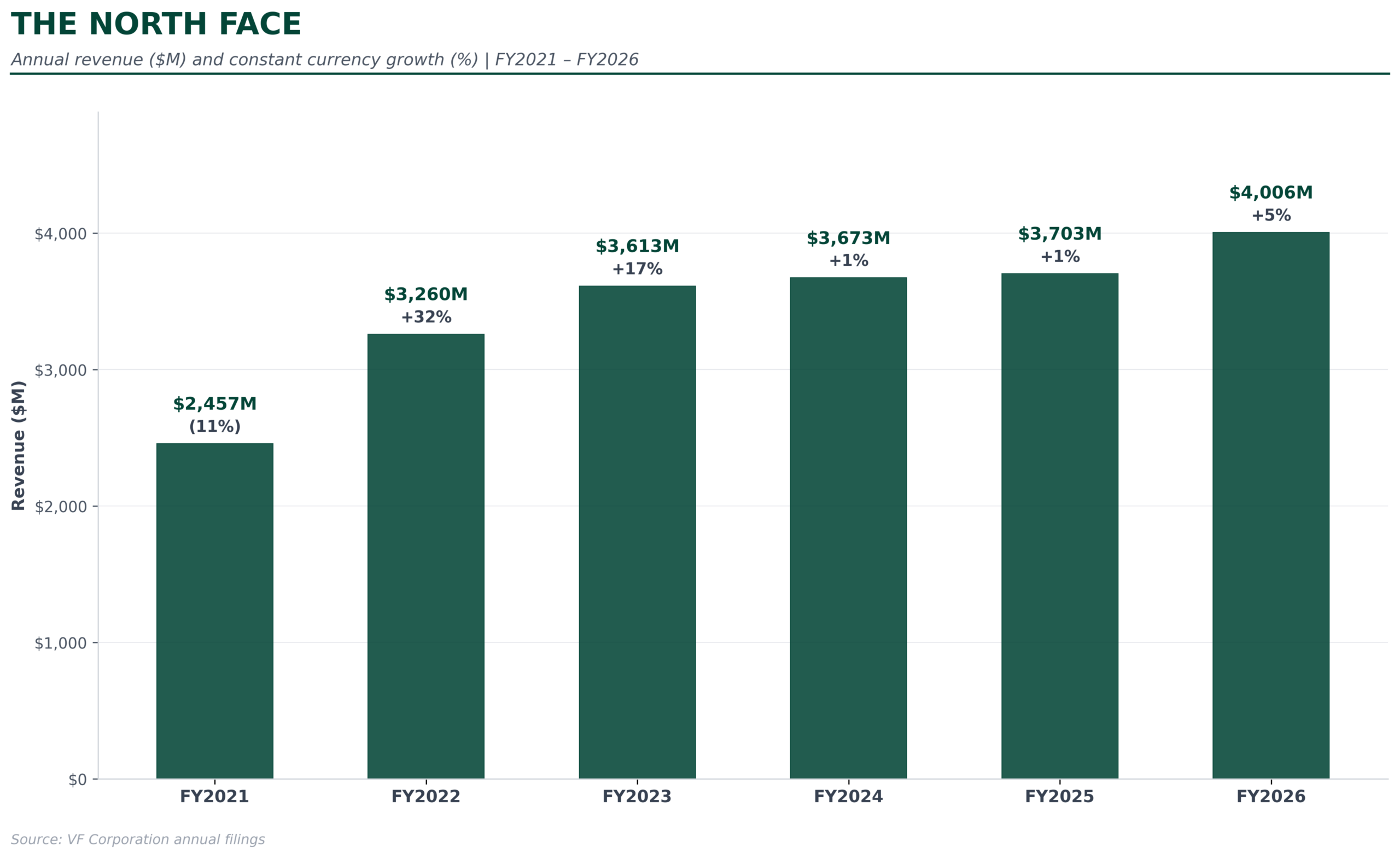

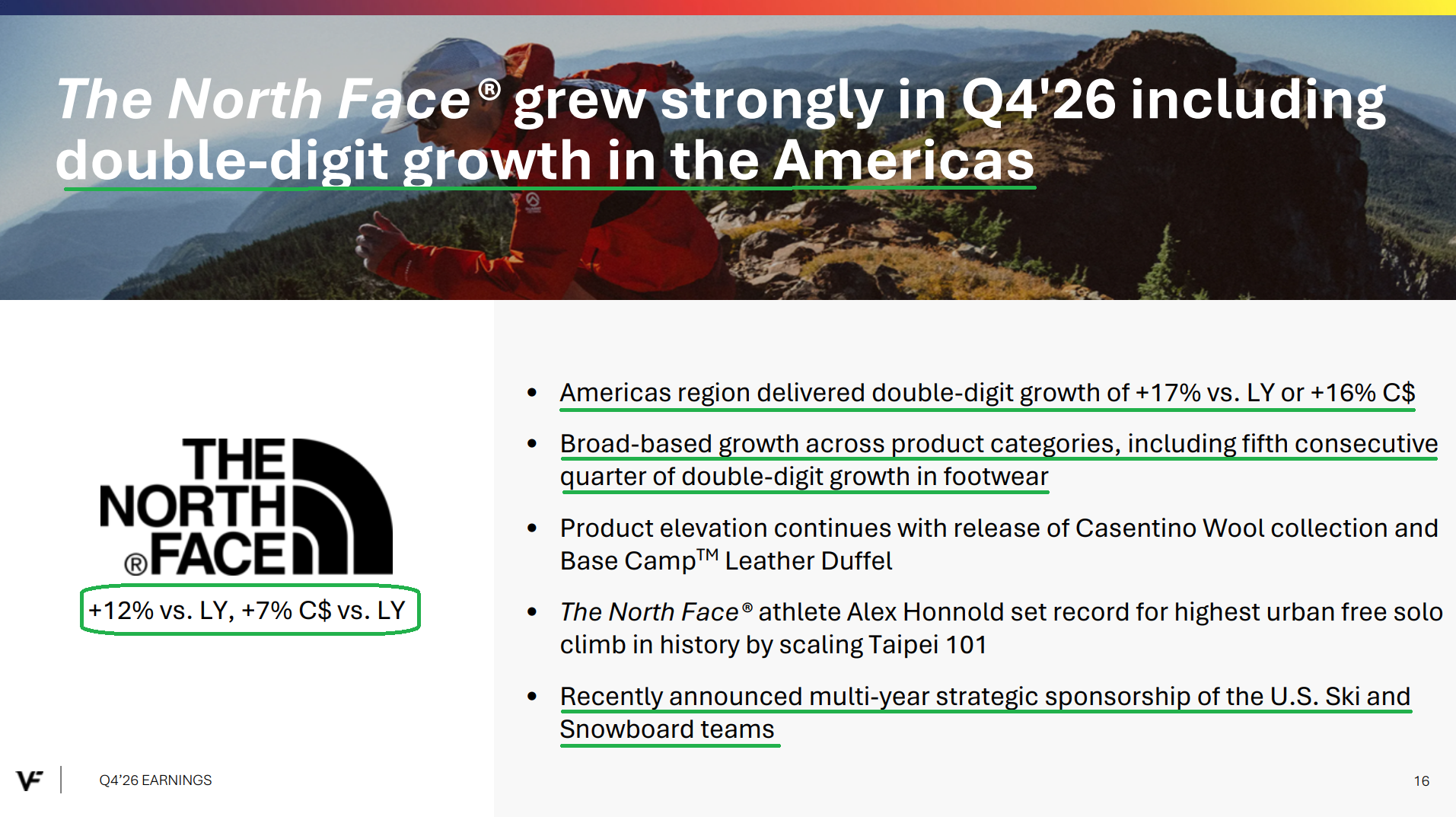

Starting with The North Face, the brand continues to fire on all cylinders, growing +12% (+7% C$) to $935M in Q4 and +8% (+5% C$) to $4.0B for the full year. Management still sees the brand as only scratching the surface of its long-term potential, reiterating its target of doubling the business over time with multiple levers still to pull: category expansion, market share gains, and further elevation into premium price points.

The brand also recently landed a high-profile, eight-year partnership with U.S. Ski & Snowboard, outfitting America’s top winter athletes across the next two Olympic cycles.

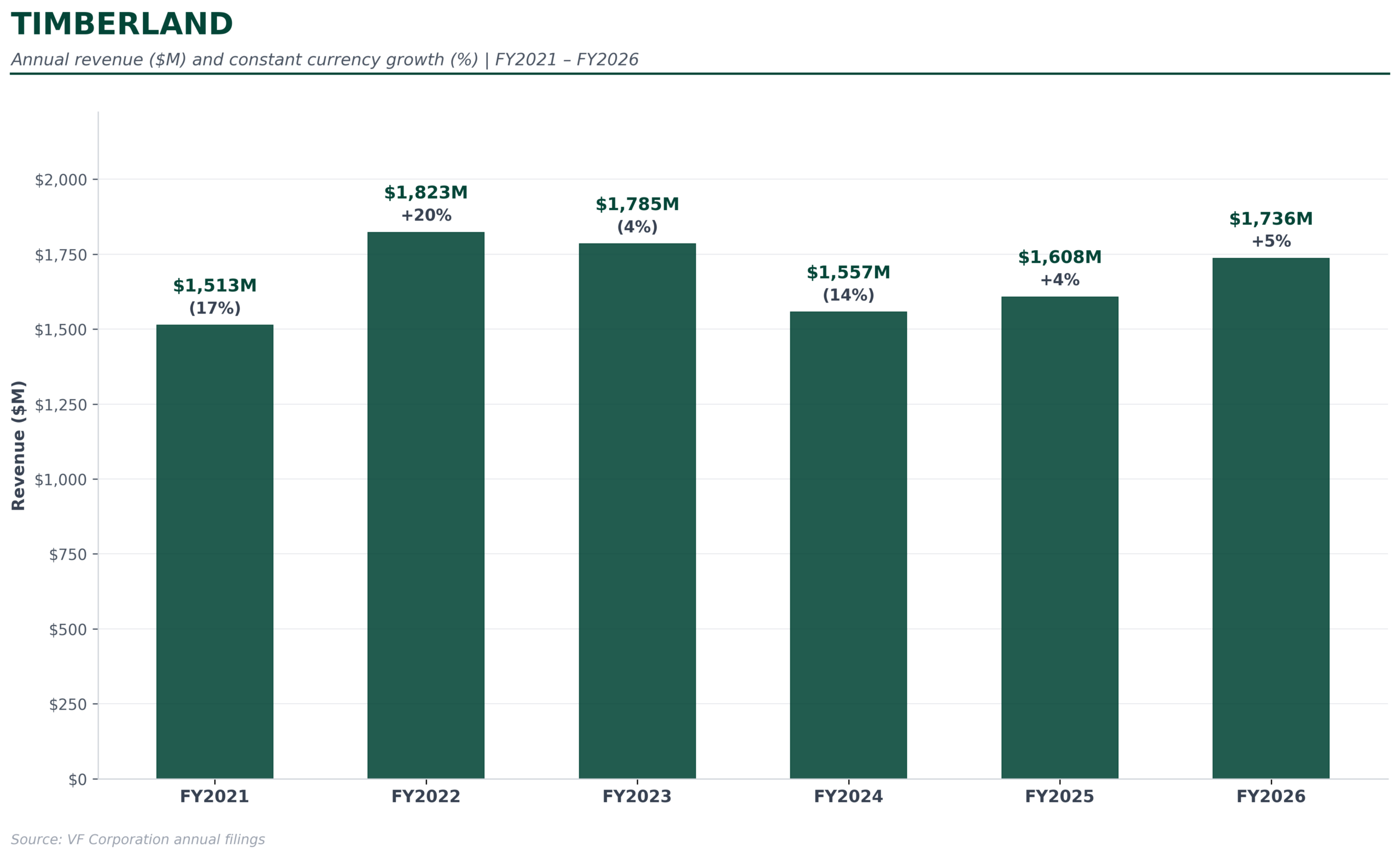

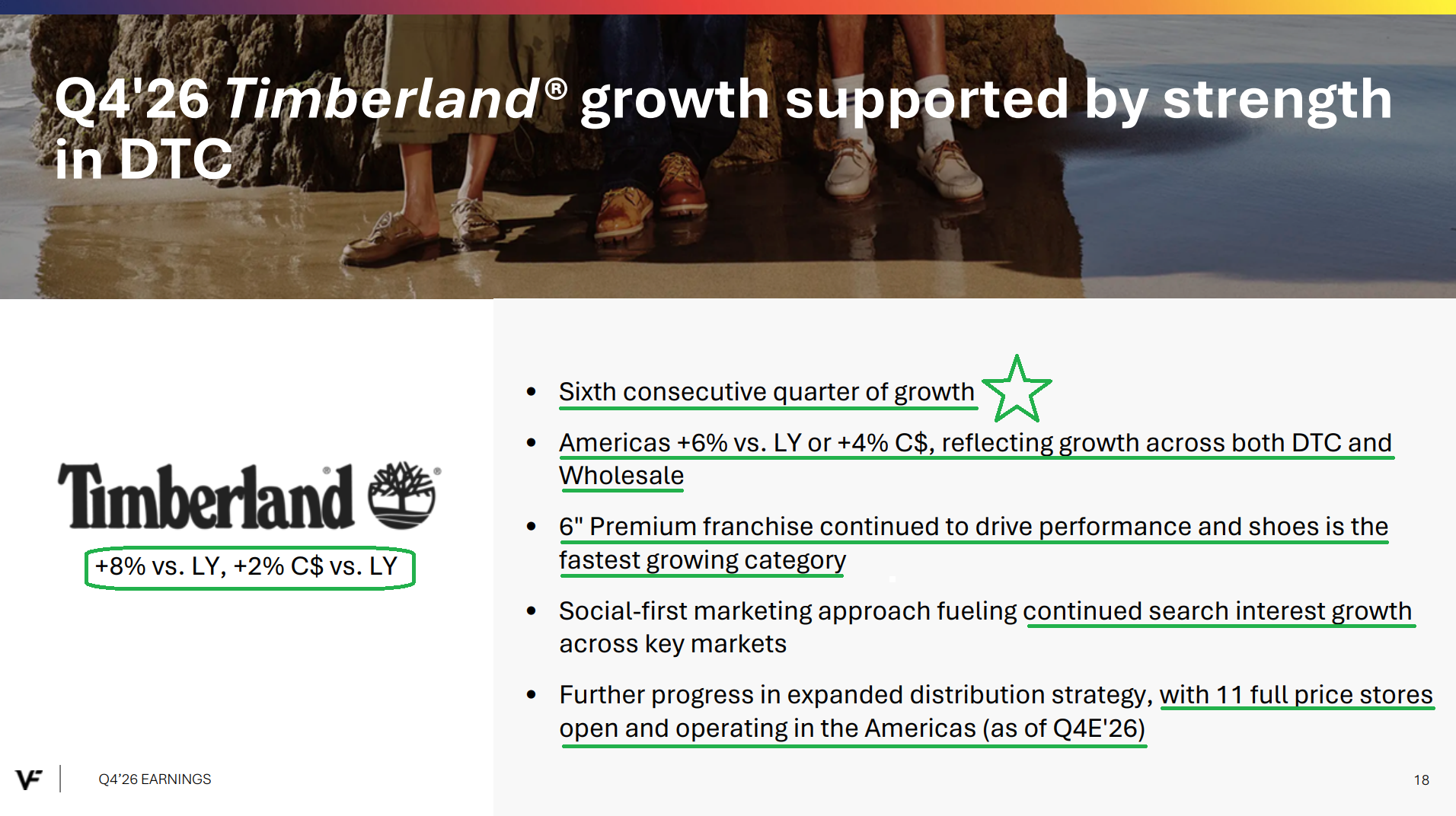

Timberland, meanwhile, is finally beginning to move beyond its biggest challenge: becoming more than just the Yellow Boot. The brand posted its sixth consecutive quarter of growth, with revenue increasing +8% (+2% C$) to $405M in Q4 and +8% (+5% C$) to $1.74B for the full year.

Despite its iconic status, Timberland remains significantly underpenetrated. Management is expanding distribution through an accelerated DTC push, with the U.S. full-price store base now at 11 locations and more planned for FY27. Combined with growing traction in the boat shoe platform and a comprehensive apparel reset arriving this fall, the brand appears to have the right pieces in place to finally break out of the ~$1.7B revenue range where it has largely been stuck since VF acquired it in 2011.

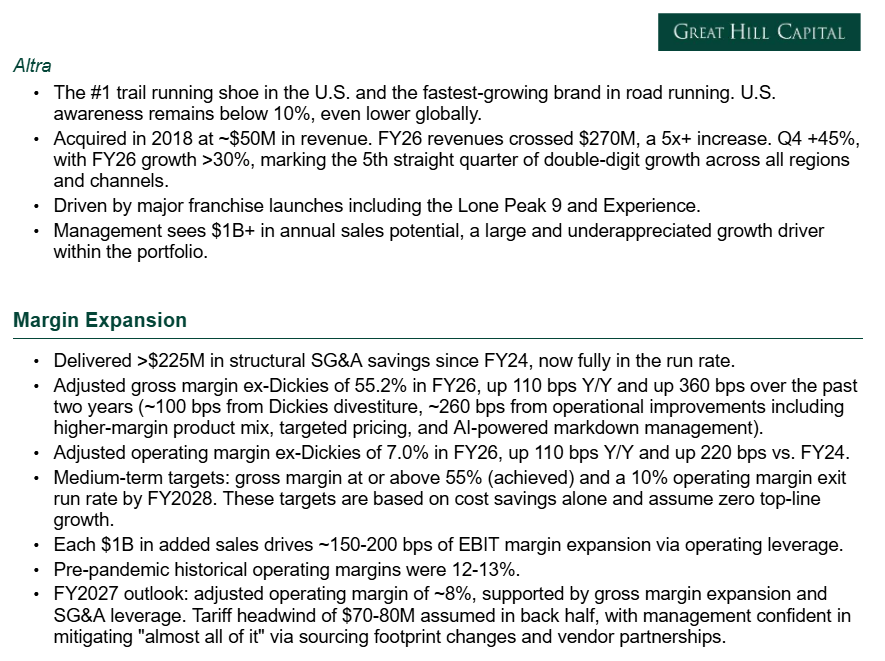

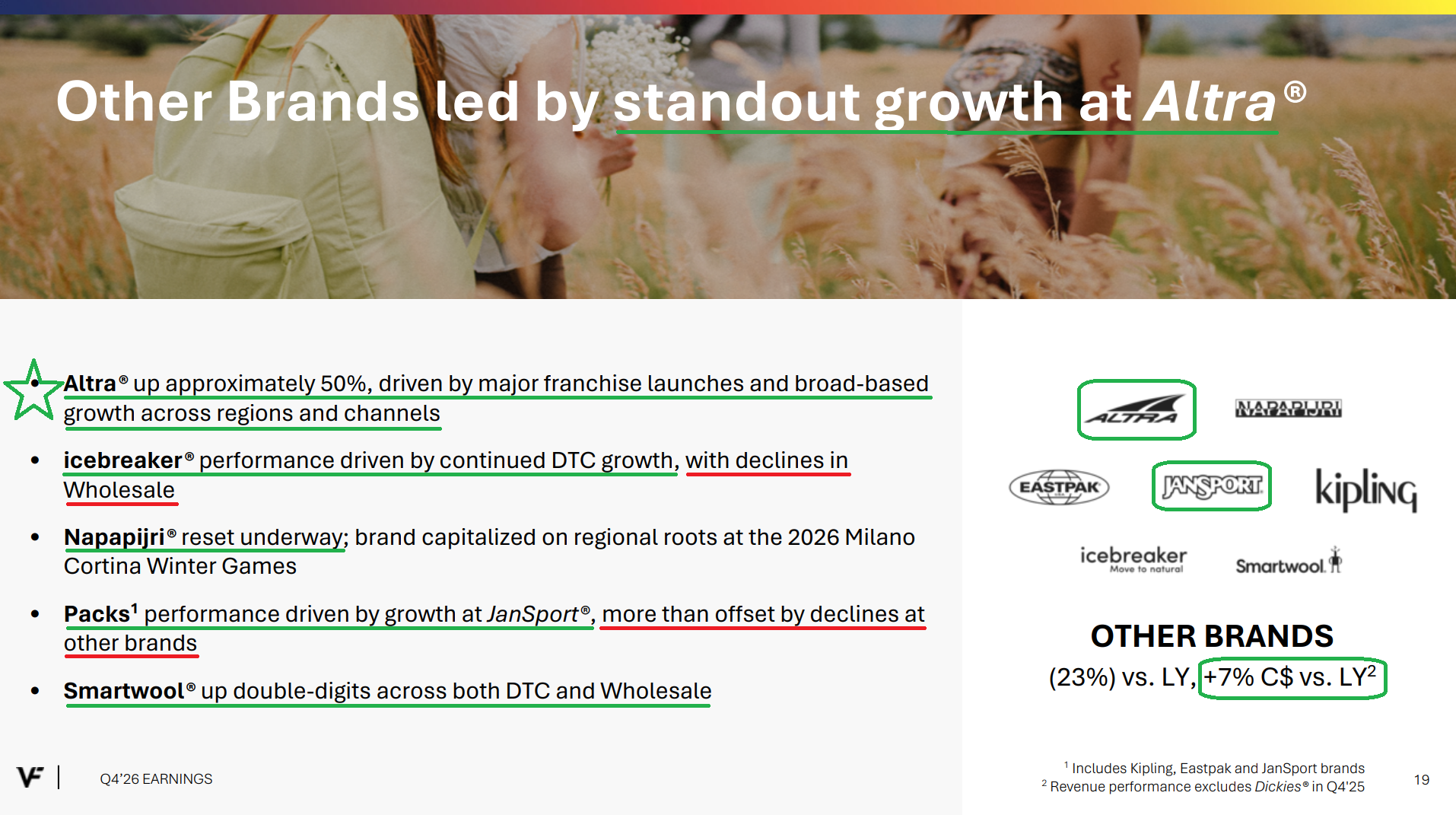

Then there’s Altra, the #1 trail running shoe brand in the U.S. and a breakout star that management has only recently begun talking about. Revenue grew ~45% in Q4, marking a fifth consecutive quarter of double-digit growth, while full-year sales reached >$270M, up from just ~$50M when VF acquired the brand in 2018.

With brand awareness still below 10% in the U.S. and even lower internationally, Altra is still in the early innings of what management sees as a $1B+ opportunity.

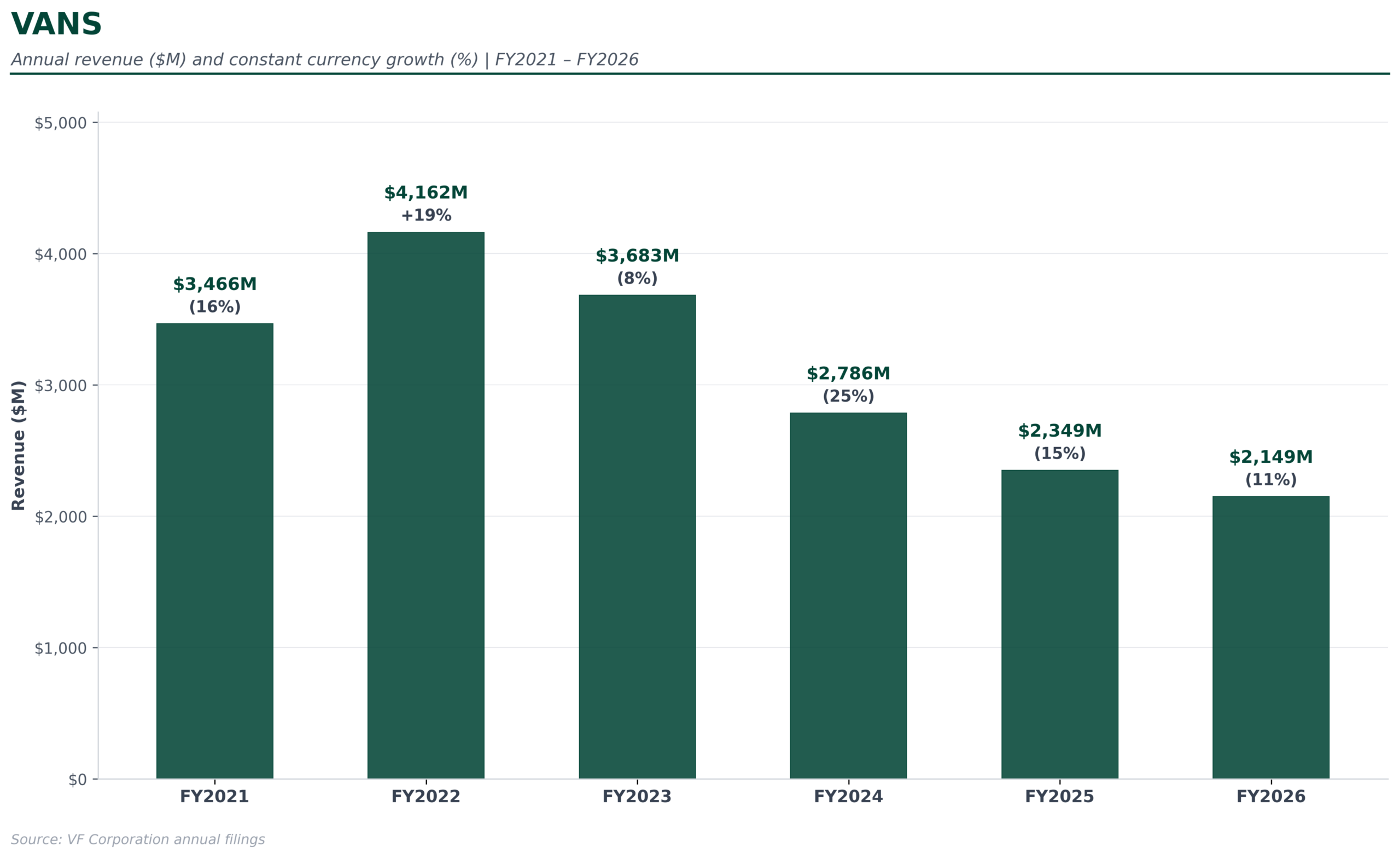

And last, but certainly not least, Vans, the final domino in this turnaround.

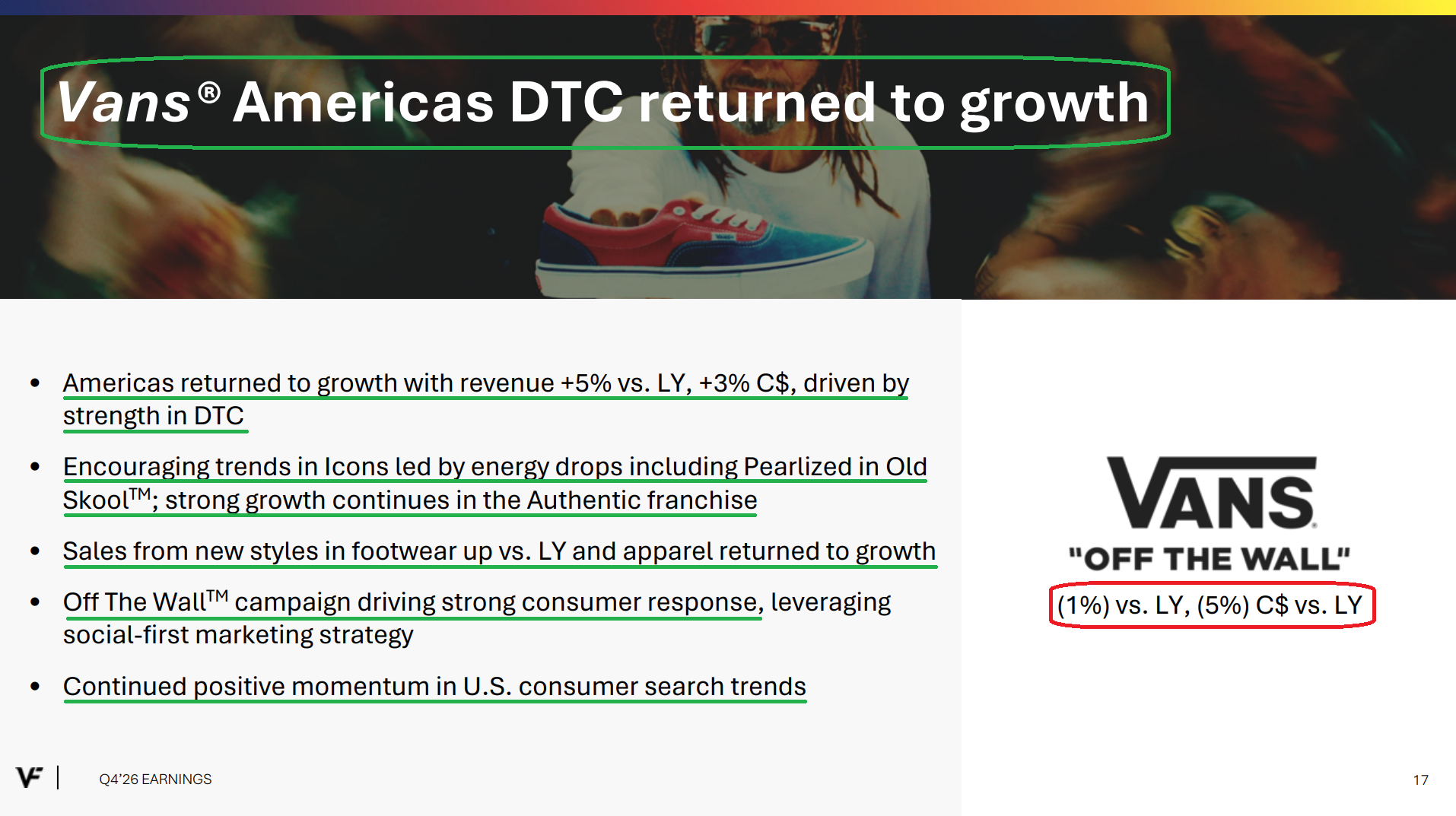

While FY26 marked Vans’ fourth consecutive year of revenue decline, with sales falling -9% (-11% C$) to $2.15B, it also contained what will likely prove to be the most important development in the entire VF story: an inflection in the Americas.

Americas DTC returned to growth for the first time in nearly four years during Q4, increasing +5% (+3% C$) and snapping a streak of 14 consecutive quarterly declines.

The importance of this inflection cannot be overstated.

The Americas account for more than half of total Vans revenue, while Americas DTC alone represents ~40% of the global business. Where the Americas go, Vans goes, serving as a leading indicator with a trickle-down effect that flows into wholesale and eventually the rest of the world.

There is no question that brand heat is building in the Americas. The Authentic franchise grew more than 80% in Q4. Slip-ons returned to growth. Apparel is gaining traction. And while certainly not encouraged, there have even been reports of fights breaking out at Vans stores over limited-edition product releases. For a brand that lost its cultural relevance and saw revenue decline from a peak of ~$4.2B to ~$2.1B today, fights breaking out over new product is not the worst problem to have.

While management guided for another year of declines at Vans in FY27, improving to just a mid-single-digit decline, we would not be surprised to see upside to that outlook. This is an under-promise-and-over-deliver management team that likely wants to see how back-to-school and the holiday season play out before getting out over its skis.

That said, with the Americas already turning (and expected to grow again in FY27), along with a number of catalysts on the horizon, including an expanded Warped Tour, culture-led marketing initiatives, high-profile collaborations, continued traction in premium product launches, and positive search trends, we expect the Vans inflection to arrive sooner than the market is currently bracing for.

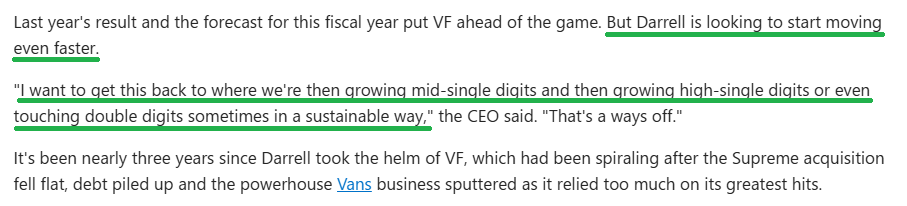

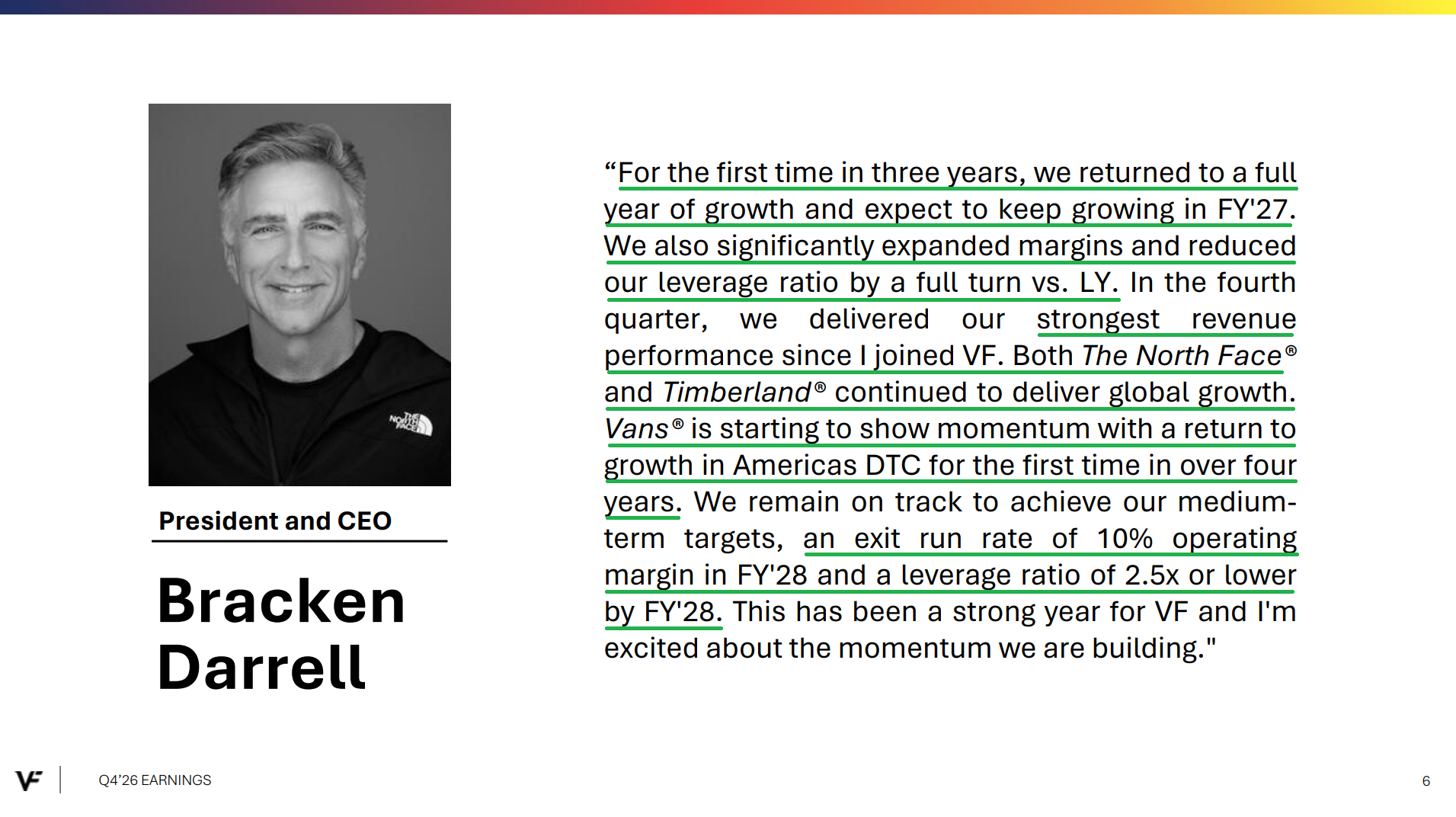

Put all of the momentum across the individual brands together, and what you have is a portfolio of iconic brands that is just beginning to return to growth mode, with ambitions, in Bracken Darrell’s own words, that go far beyond low-single-digit growth:

Source: WWD

Three years ago, the investment debate centered on whether VF could stabilize the business and repair the balance sheet.

Today, that debate has shifted to growth, and “Growth Bracken” is just getting started.

Q4 Earnings Breakdown

10 Key Points

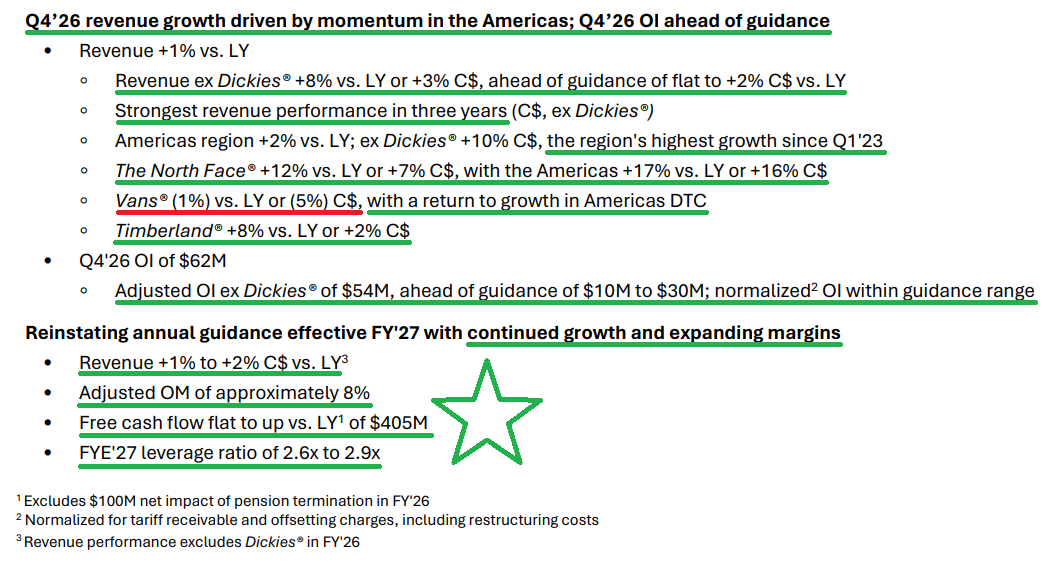

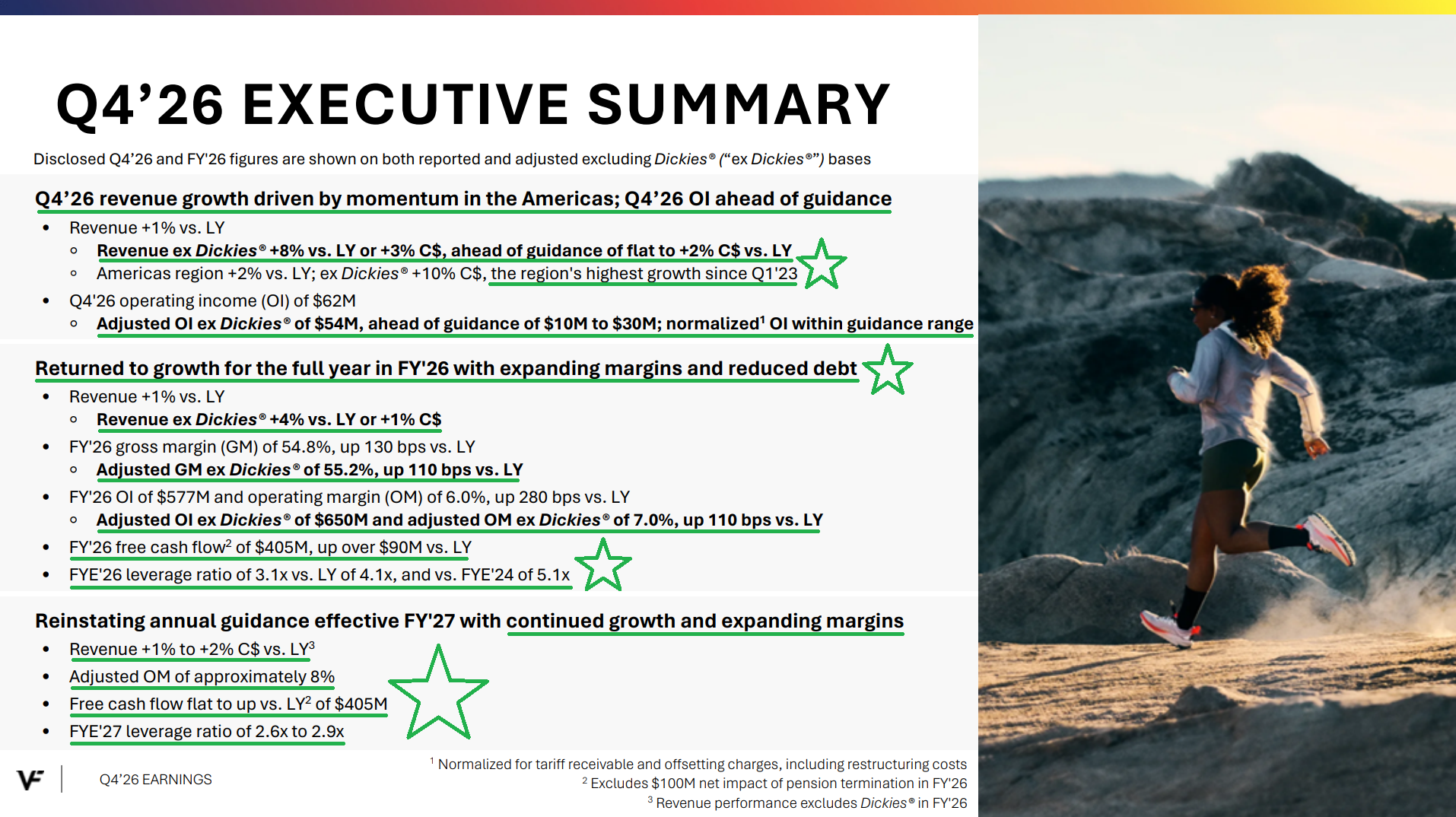

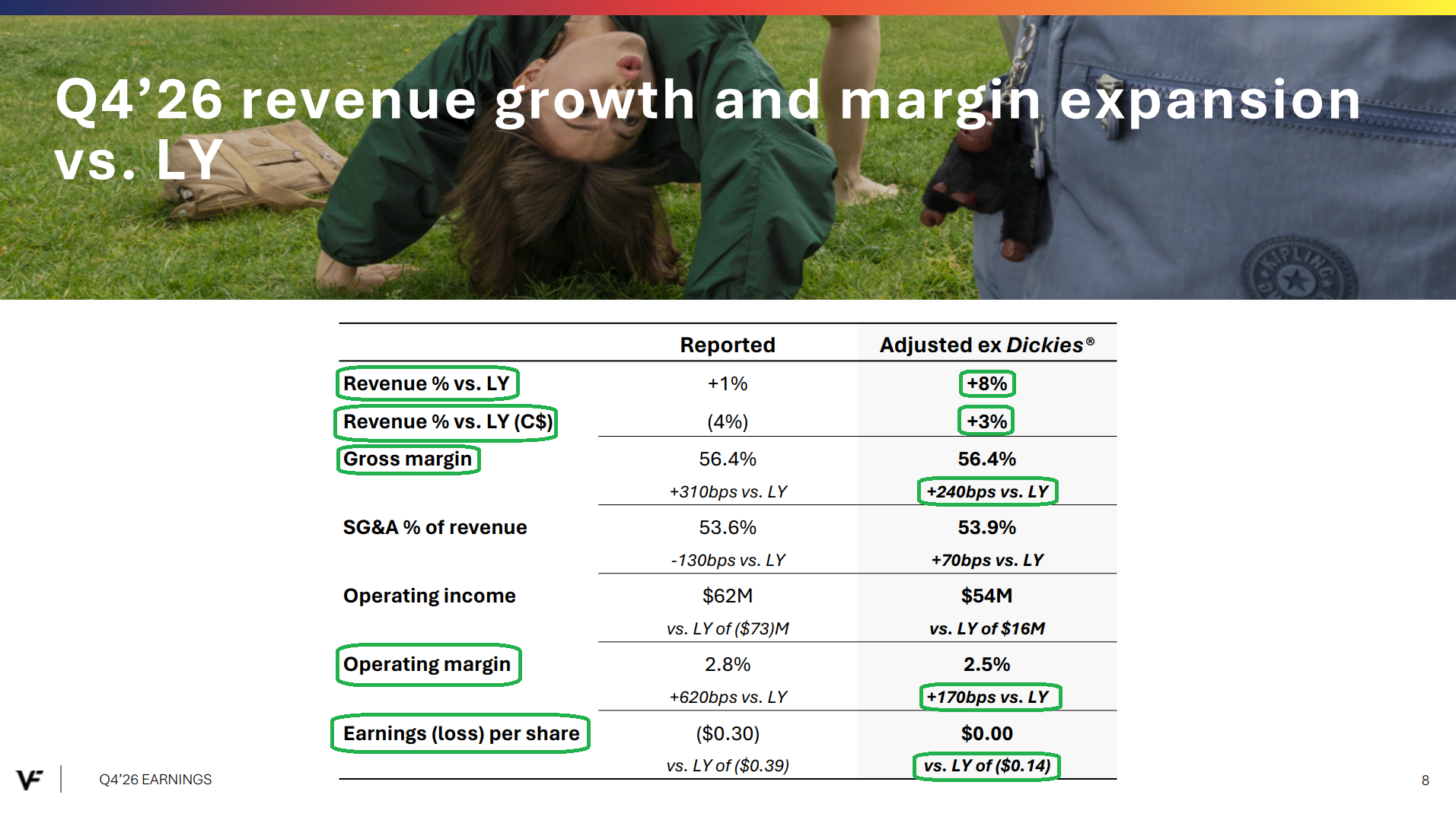

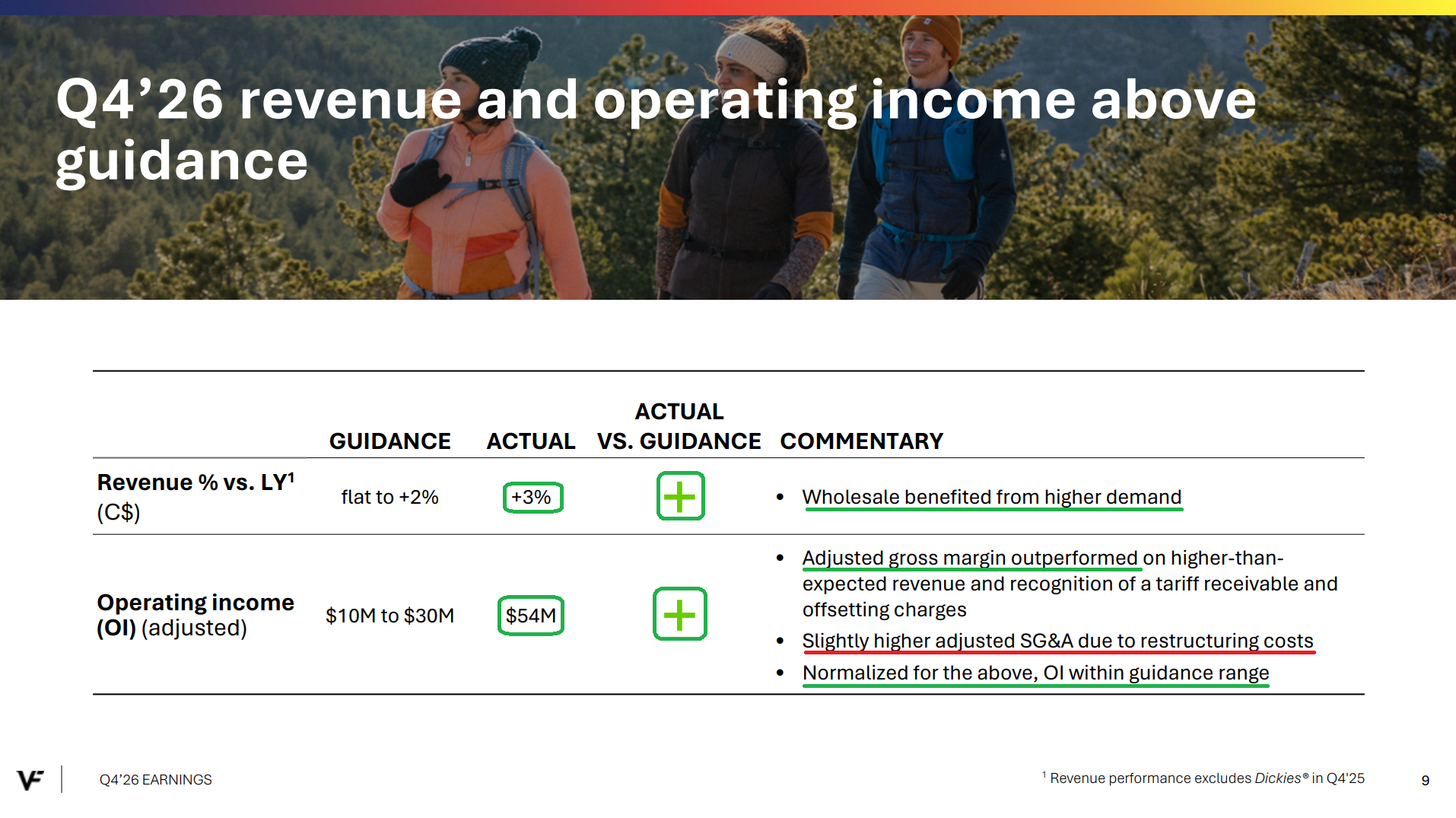

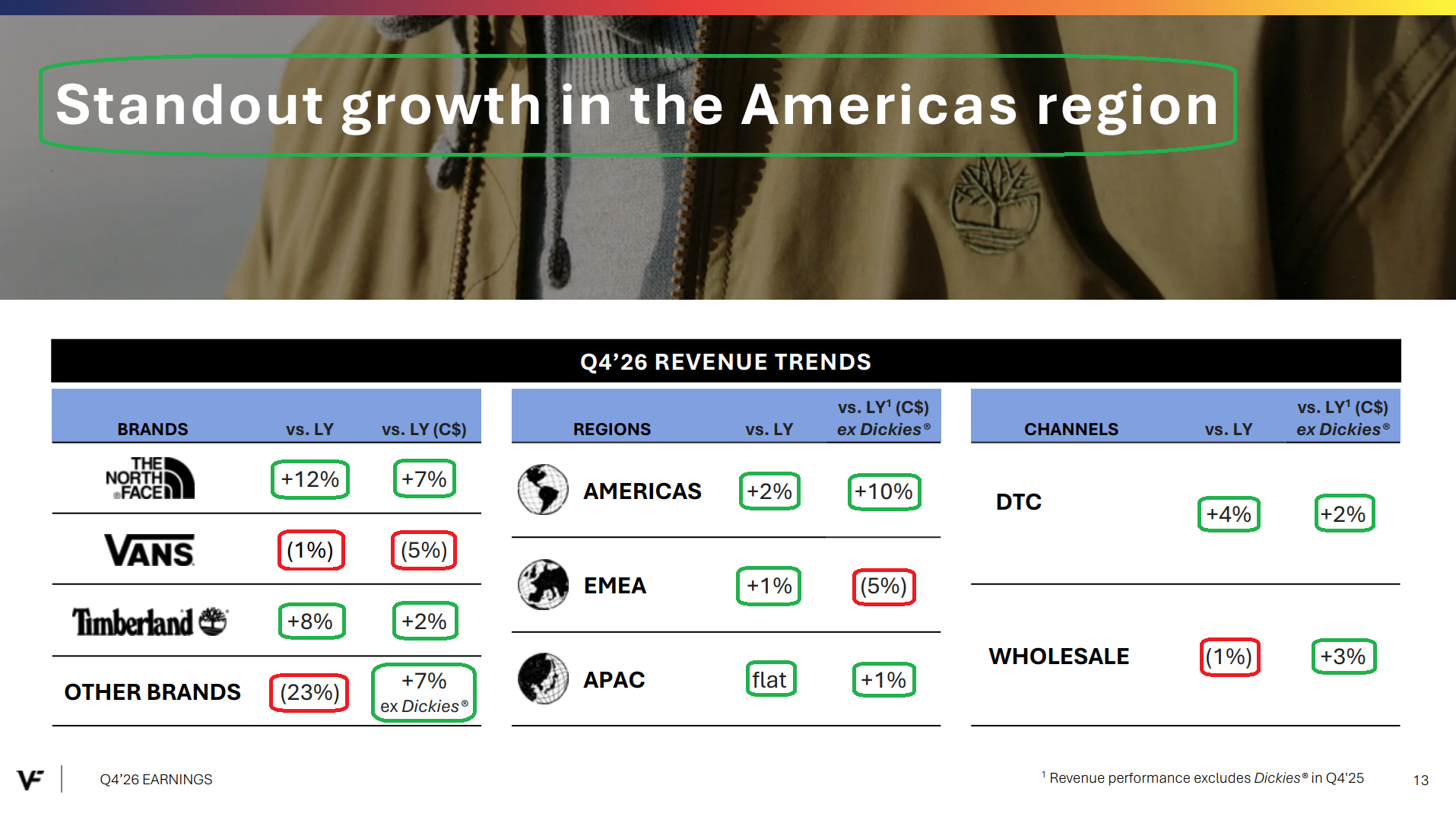

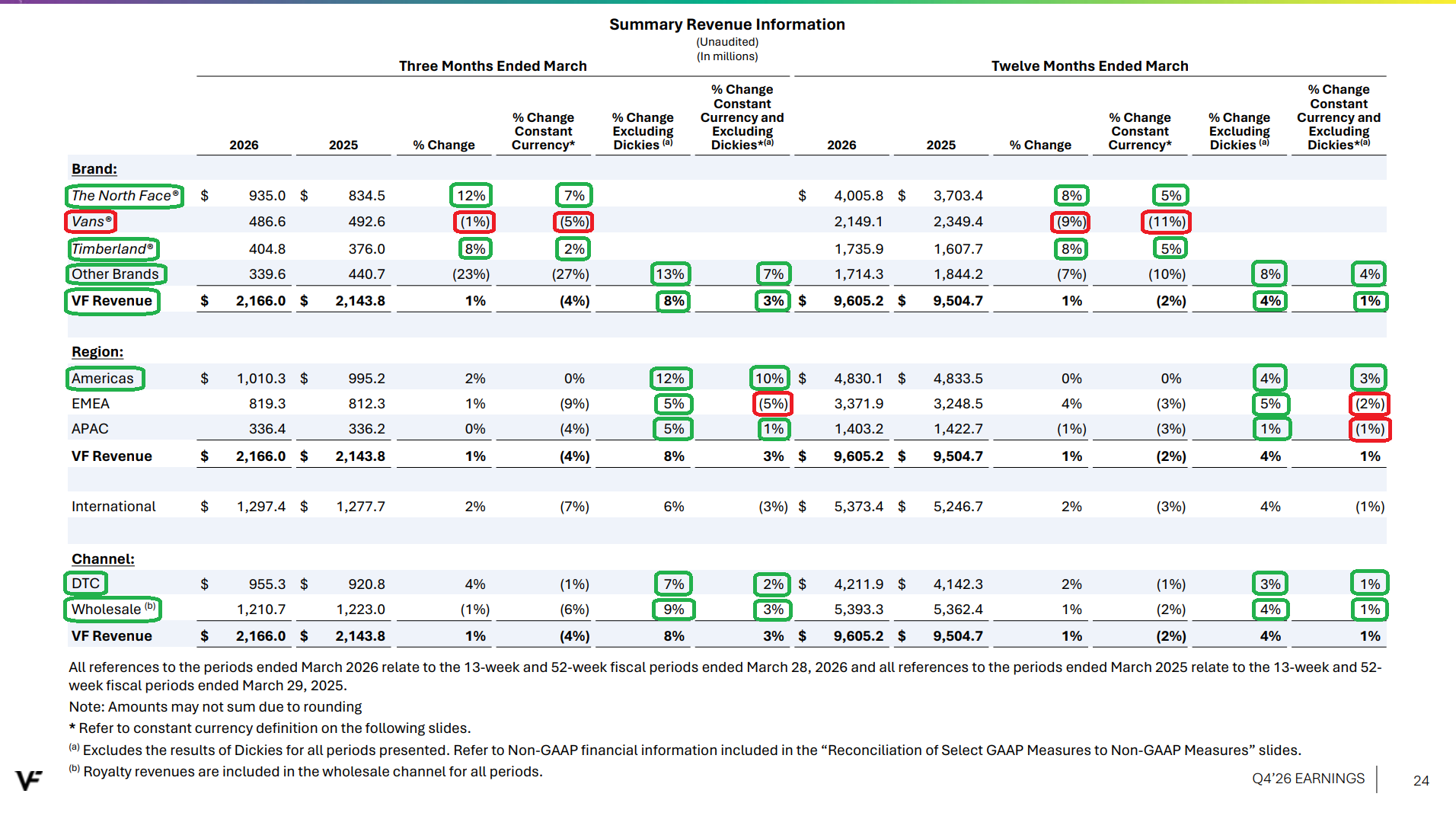

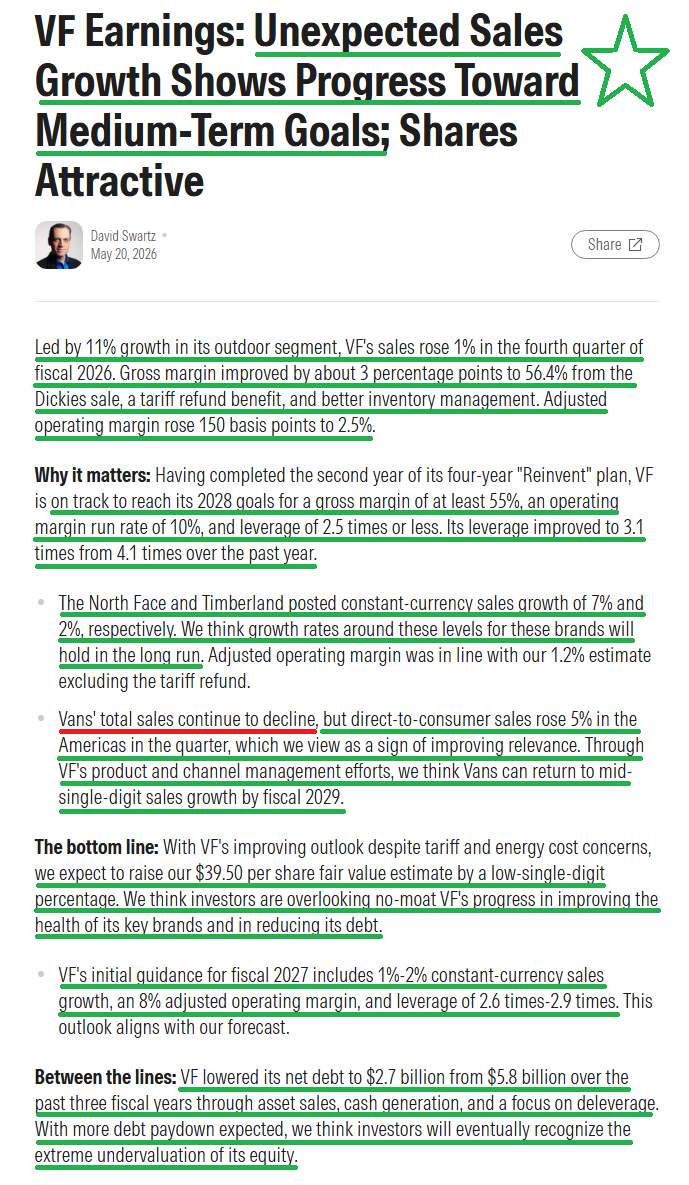

1) VFC reported Q4 revenue of $2.17B (+8% Y/Y or +3% C$ ex-Dickies), beating consensus of $2.13B and prior guidance of flat to +2% C$, marking the strongest top-line performance in three years. By region, the Americas grew +2% reported or +10% C$ ex-Dickies, the region’s highest growth since Q1 2023, while EMEA was +1% reported or (5%) C$ and APAC was flat reported or +1% C$. For the full year, revenue grew +4% or +1% C$ ex-Dickies, marking the first full year of growth in three years, with ~70% of the business by revenue now growing compared to just 43% in FY24.

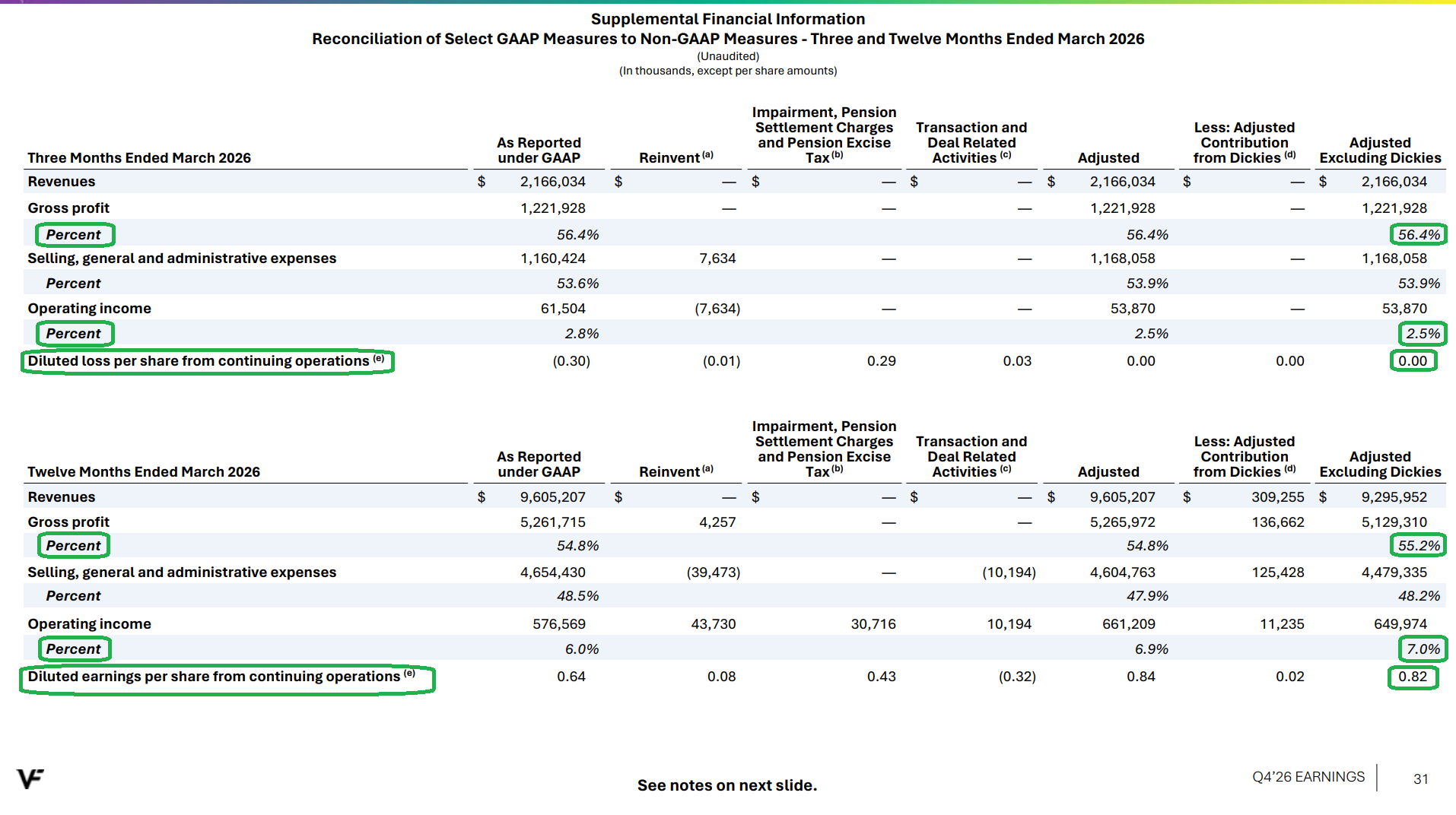

2) Adjusted gross margins ex-Dickies came in at 56.4% in Q4, up 240 bps Y/Y. For the full year, adjusted gross margins ex-Dickies reached 55.2%, up 110 bps Y/Y and up 360 bps over the past two years (~100 bps from the Dickies divestiture and ~260 bps from operational improvements including higher-margin product mix, targeted pricing actions, and markdown management). This already puts VFC ahead of its FY28 target of 55%, with further upside now expected given the cleaner ex-Dickies portfolio mix.

3) Adjusted operating income ex-Dickies of $54M was well ahead of guidance of $10M to $30M, with normalized operating income (excluding the tariff receivable and offsetting restructuring charges) coming in within the guidance range. Adjusted operating margins ex-Dickies came in at 2.5% in Q4, up 170 bps Y/Y. For the full year, adjusted operating margins ex-Dickies reached 7.0%, up 110 bps Y/Y and up 220 bps vs. FY24, with adjusted OI ex-Dickies of $650M.

4) The North Face reported Q4 revenue of $935M (+12% Y/Y or +7% C$), with the Americas region delivering double-digit growth of +17% (+16% C$). For the full year, TNF revenue grew to $4.0B (+8% Y/Y or +5% C$), driven by broad-based growth across product categories, including the fifth consecutive quarter of double-digit growth in footwear. Management reiterated the long-term goal of doubling The North Face’s revenue base over time, with multiple levers including category growth, market share gains, new category expansion, and product elevation to higher price points.

5) Vans reported Q4 revenue of $487M, down (1%) Y/Y or (5%) C$, while the all-important Americas DTC business returned to growth of +5% (+3% C$) for the first time in over four years, an acceleration following the Americas e-commerce return to growth in Q3 (+4%). The Authentic franchise grew +80% Y/Y, slip-on returned to growth, and apparel also returned to growth in Q4. For the full year, Vans revenue was $2.15B, down (9%) Y/Y or (11%) C$, a solid improvement from the (15%) decline in FY25. Management expects Vans to decline in the mid-single-digit range in FY27, with continued Americas DTC growth throughout the year. The Americas region represents more than 50% of total Vans sales and Americas DTC is ~40% of the global Vans business, making it the most important inflection point in the entire Vans turnaround, with brand heat building first in Americas DTC before an expected flow into wholesale and then the rest of the world.

6) Timberland reported Q4 revenue of $405M (+8% Y/Y or +2% C$), marking the sixth consecutive quarter of global growth. The Americas grew +6% (+4% C$), with strength across both DTC and wholesale channels. DTC growth accelerated to +8%, driven by the 11 full-price stores now open and operating in the region. The 6″ Premium franchise continues to drive performance, with shoes the fastest-growing category, while the boat shoe continues to show strong results across all regions with significant growth potential ahead. Starting this fall, management is resetting the apparel selection to better match the footwear offering, with a focus on building out the women’s business. For the full year, Timberland revenue grew to $1.74B (+8% Y/Y or +5% C$), with management confident the brand can become much larger over time.

7) Altra grew ~45% in Q4, marking its fifth consecutive quarter of double-digit growth across all regions and channels. For the full year, Altra grew more than 30% to over $270M in revenue, driven by major franchise launches including the Lone Peak 9 and the Experience. Brand awareness remains very low (sub-10% in the U.S. and even lower internationally), leaving substantial runway, with management continuing to see Altra as a $1B+ brand opportunity over time.

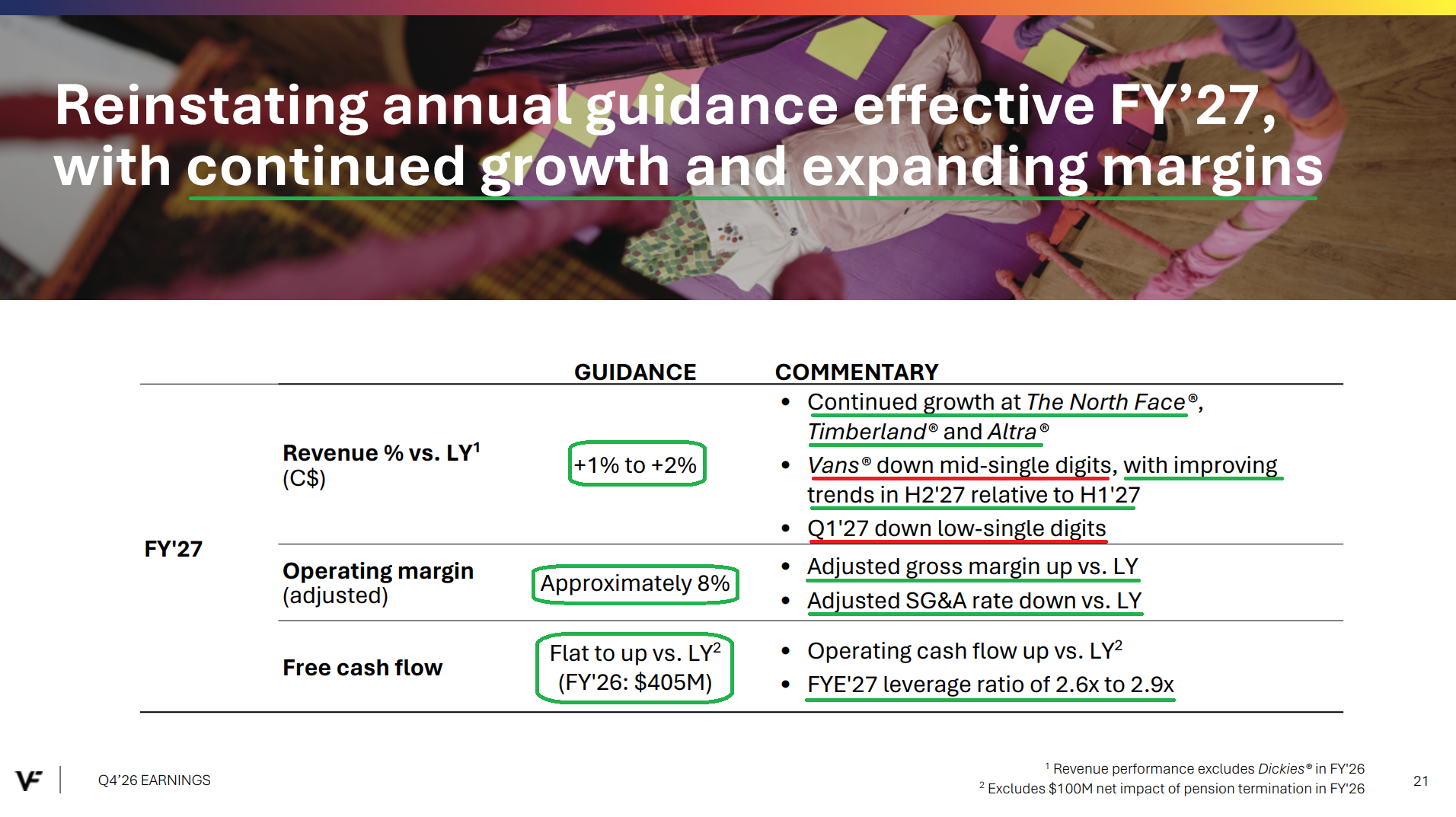

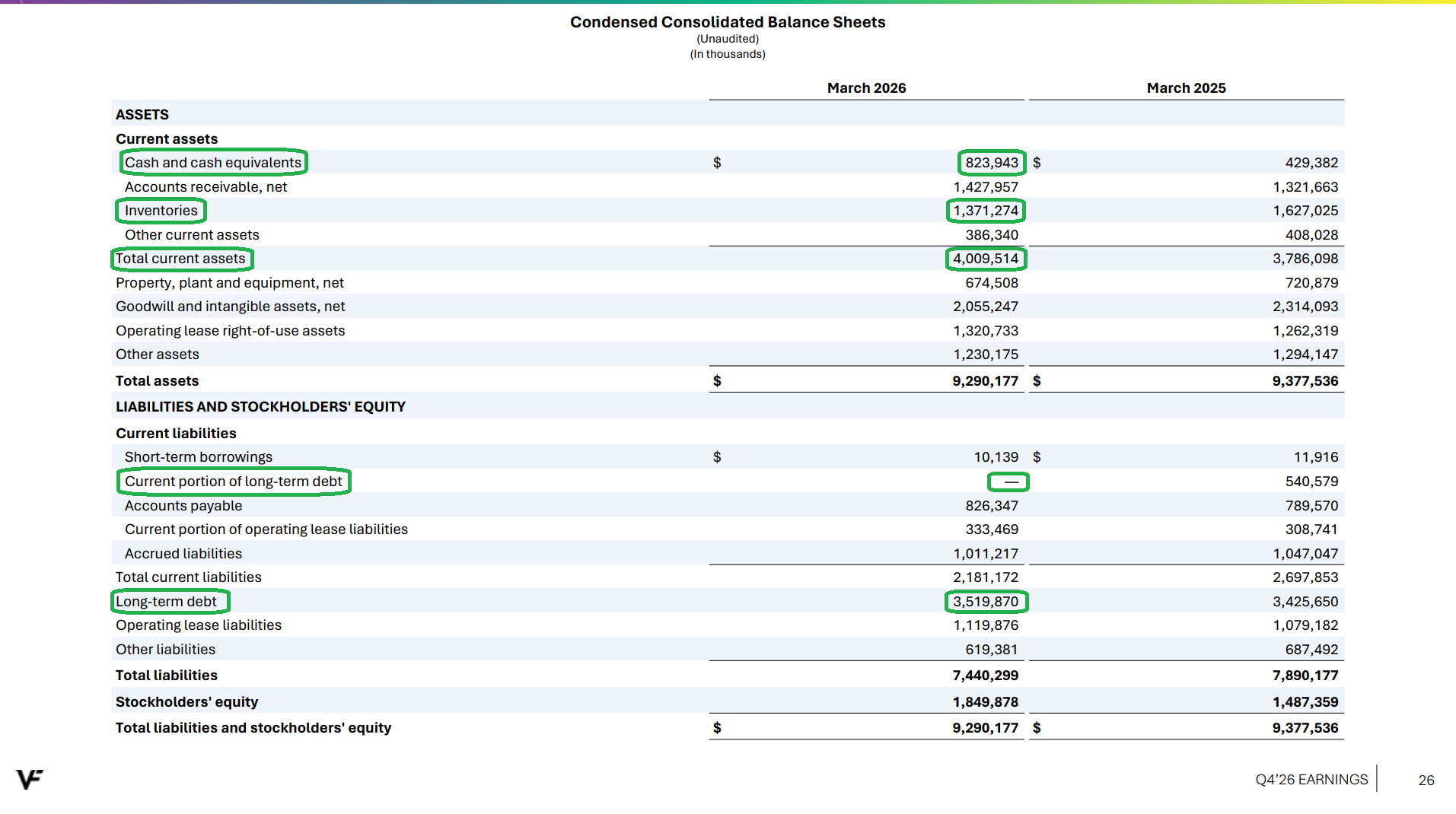

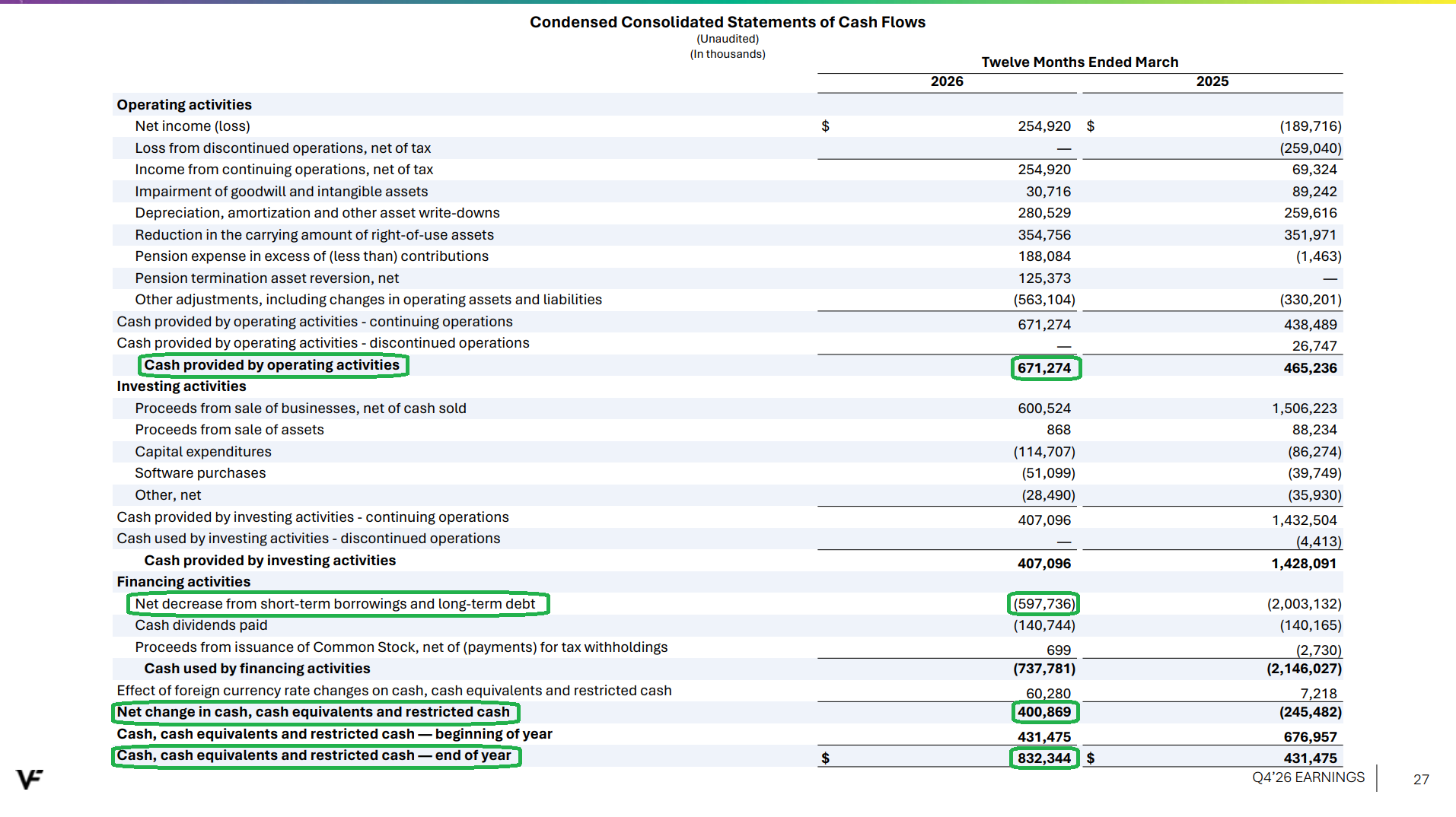

8) Net debt ended the year at $4.2B, down $0.8B or (16%) Y/Y, with net debt excluding lease liabilities of $2.7B now down from $5.8B three years ago. The FY26 leverage ratio of 3.1x is down a full turn vs. LY and two full turns vs. FY24’s 5.1x, with management guiding to a FY27 leverage ratio of 2.6x to 2.9x, putting the company on track to reach its medium-term target of 2.5x or lower by FY28. Net inventories ex-Dickies were also down 11% C$ Y/Y, driven by continued inventory discipline across the organization.

9) Free cash flow reached $405M in FY26 (excluding the $100M net pension termination benefit), up over $90M Y/Y and well ahead of management’s prior guidance for FCF to be flat to up Y/Y. For FY27, management guided to free cash flow flat to up vs. FY26’s $405M, despite a ~$100M step-up in CapEx driven largely by the continued rollout of Timberland full-price stores.

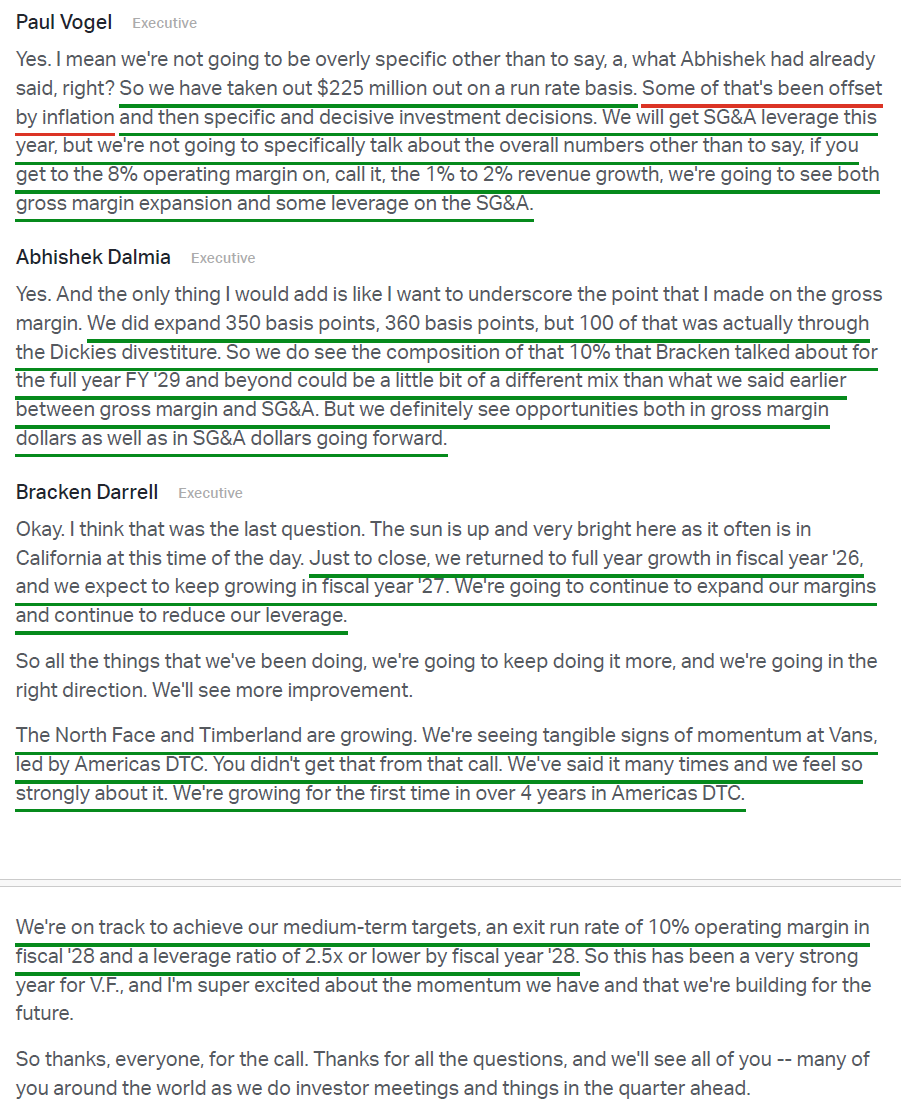

10) Management reinstated annual guidance for FY27, calling for revenue growth of +1% to +2% C$ ex-Dickies, with continued growth at The North Face, Timberland, and Altra, partially offset by the mid-single-digit decline at Vans. FY27 revenue is expected to face a ~100 bps headwind from the Middle East conflict, partially offset by a ~50 bps benefit from the 53rd week, while Q1 results are expected to be impacted by wholesale timing shifts. Adjusted operating margin is expected to be ~8%, supported by gross margin expansion and SG&A leverage. Management assumes a $70-80M tariff headwind in the back half of FY27 but expects to mitigate “almost all of it” via sourcing footprint changes and vendor partnerships. Most importantly, management reaffirmed its medium-term target of a 10% operating margin exit run rate in FY28, clarifying that VFC will hit 10% sometime during FY28 and FY29 should be 10% or better.

Earnings Call Highlights

Morningstar Analyst Note

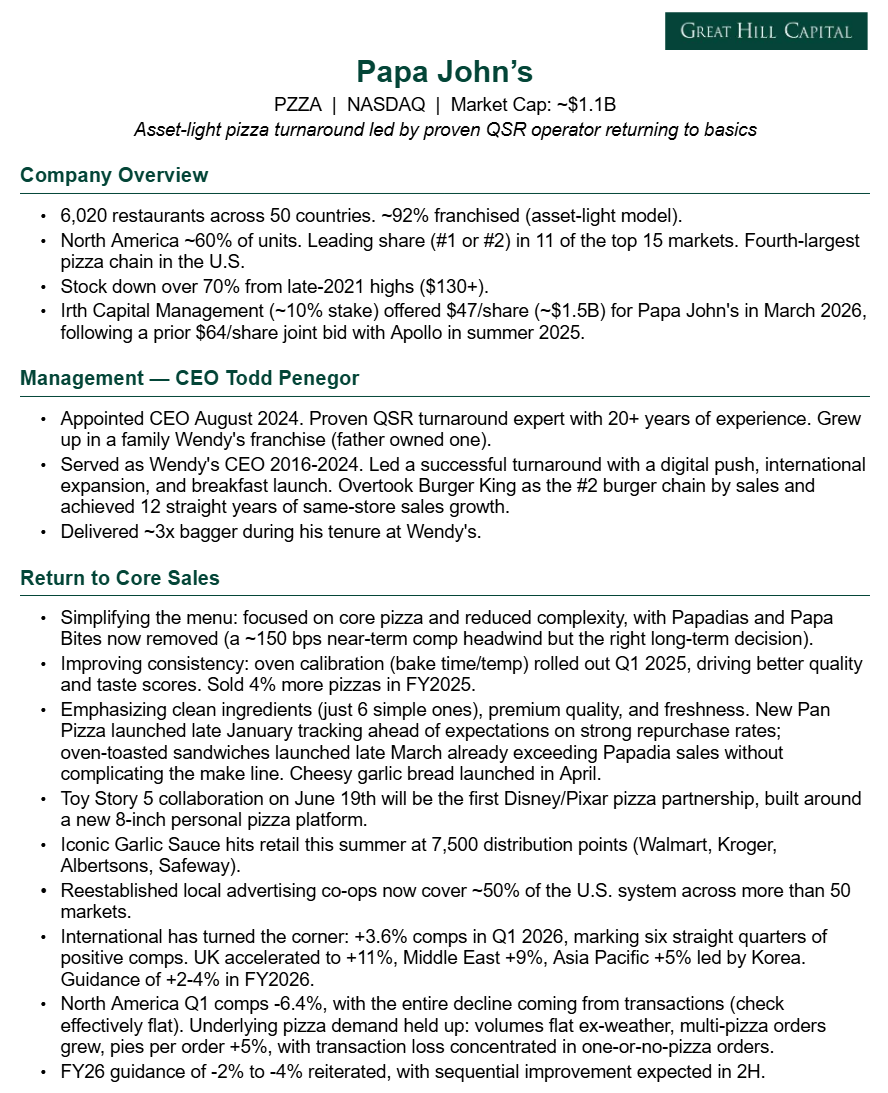

Papa John’s (PZZA) Update

For newer readers, here’s a quick overview of our thesis on Papa John’s, a global leader in the pizza QSR category, where a proven operator is driving a back-to-basics turnaround after years of self-inflicted missteps:

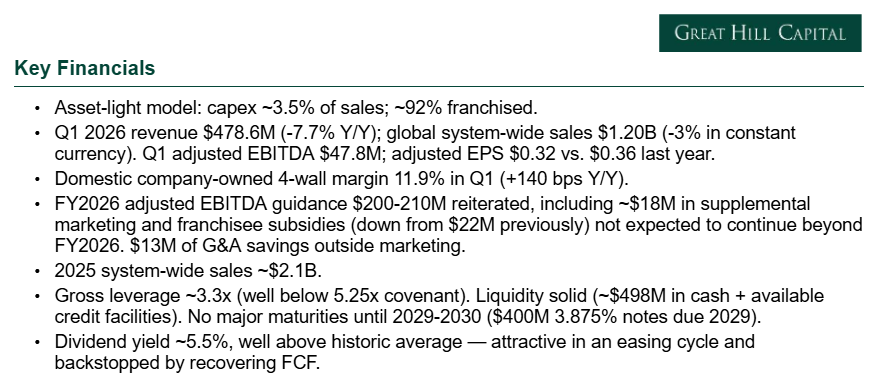

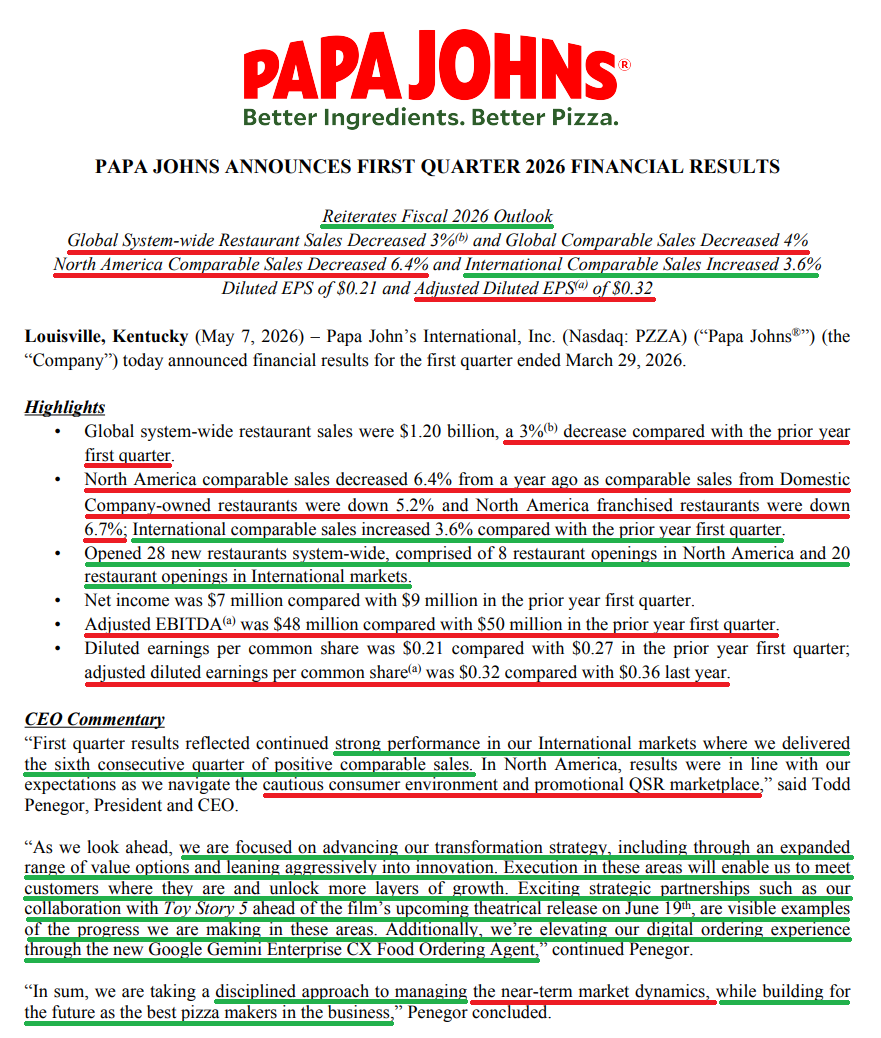

Papa John’s faced continued pressure in Q1, as a cautious consumer and an aggressively promotional QSR backdrop weighed on North America results.

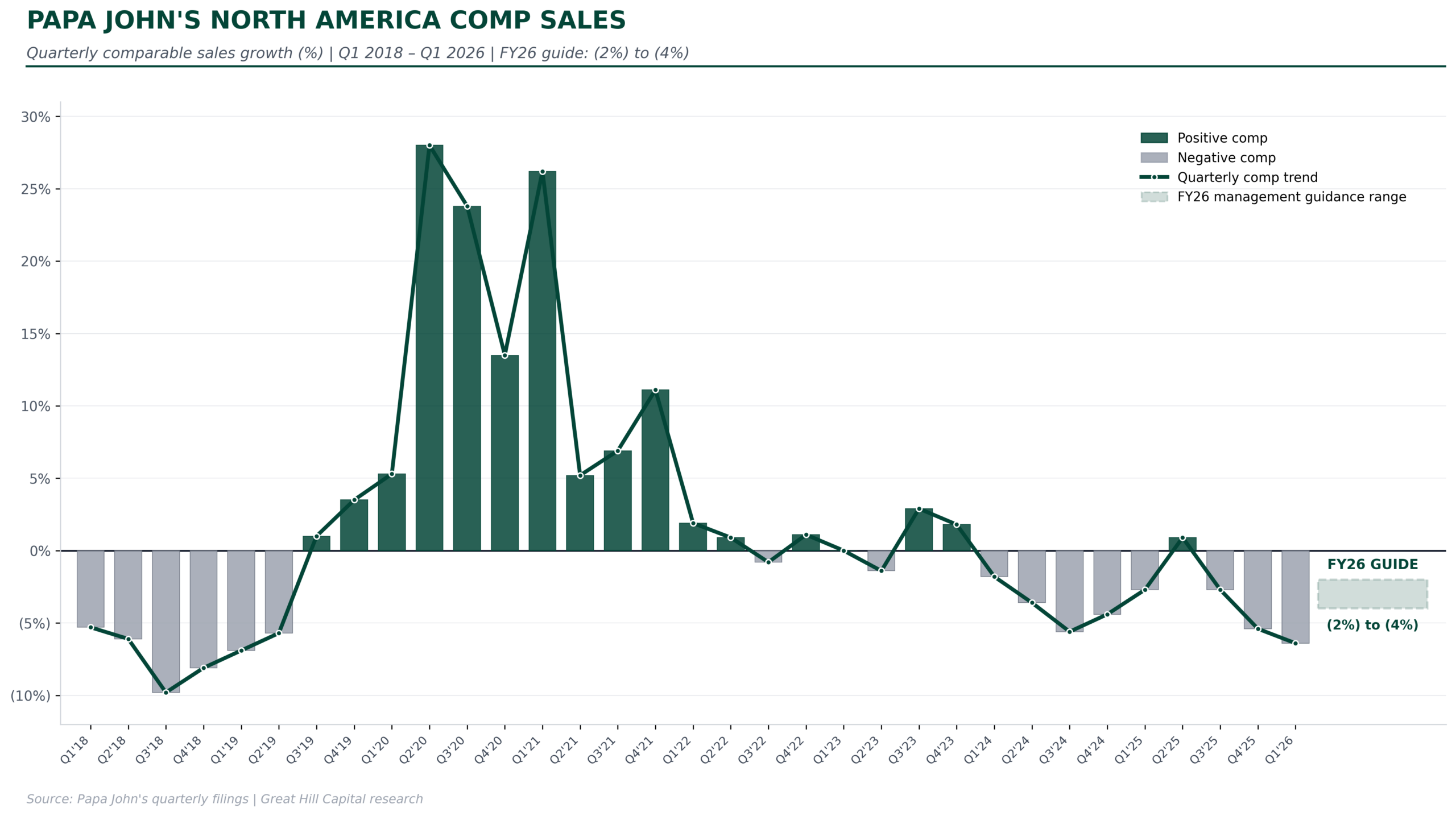

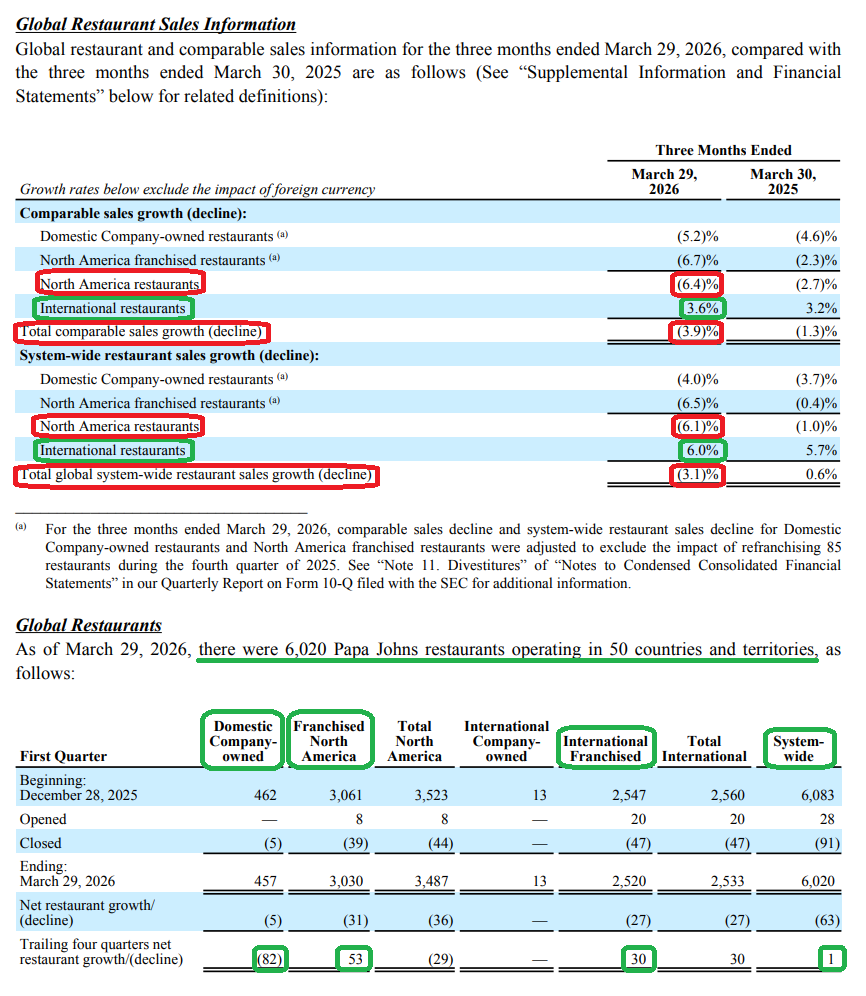

North America comps fell -6.4% Y/Y, missing expectations of -4.6% and pulling NA systemwide sales to $868.9M (-6% Y/Y).

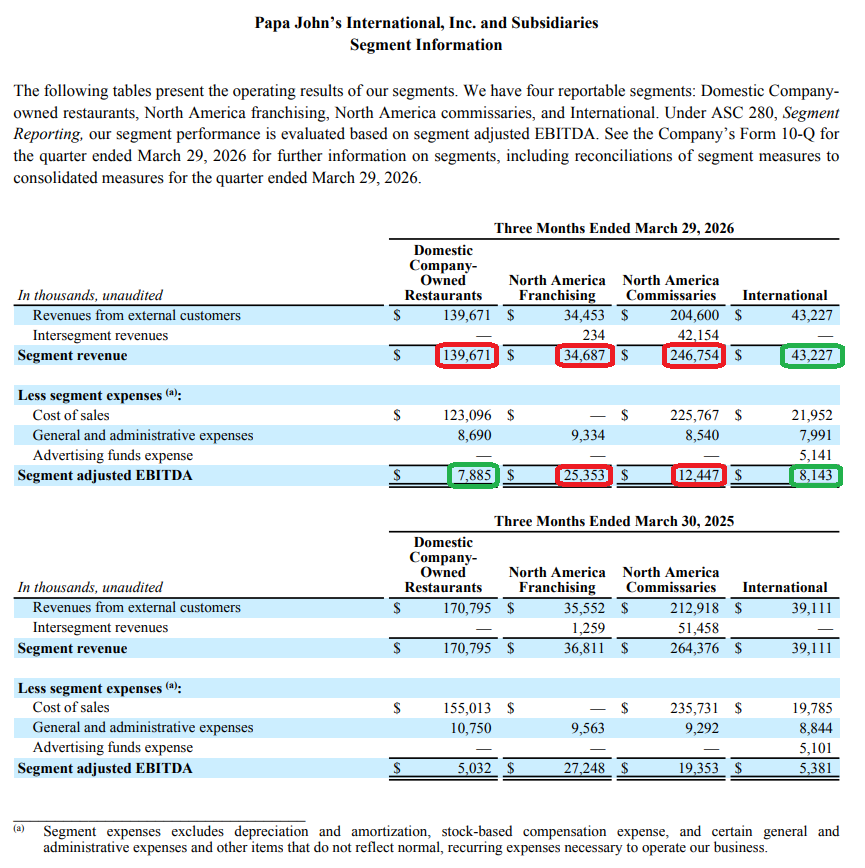

International continued its run of outperformance, with comps +3.6% to mark a sixth straight quarter of positive growth, while segment systemwide sales increased +6% C$ to $333.4M.

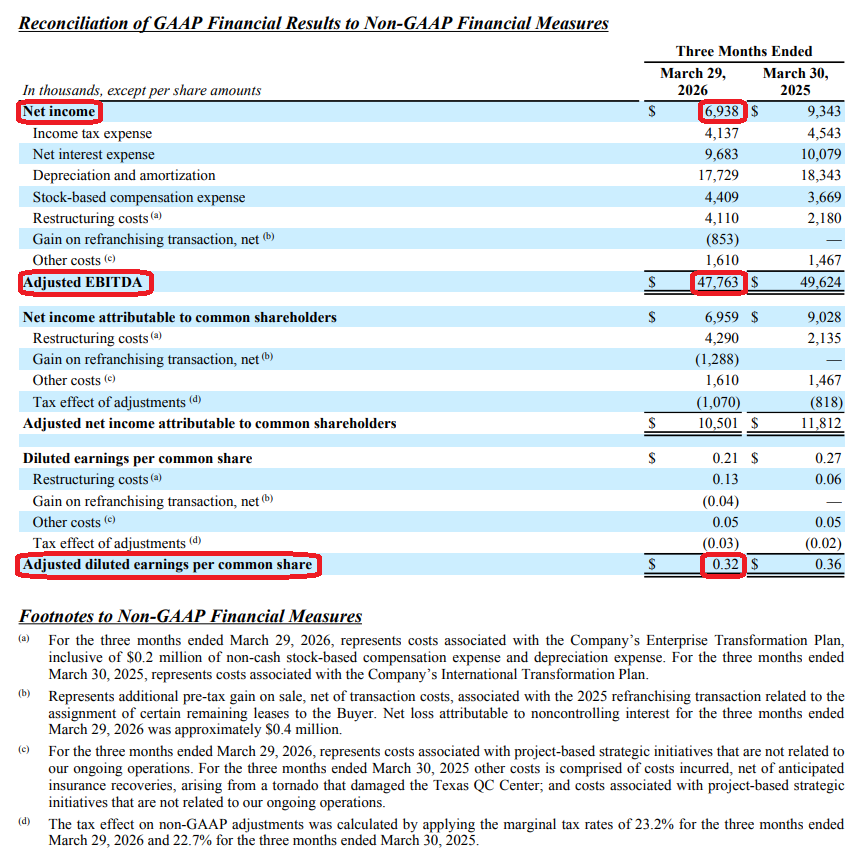

These strong results overseas weren’t enough to offset weakness at home, with International accounting for only ~15% of total adjusted EBITDA. As a result, adjusted EBITDA fell -3.7% to $47.8M, missing consensus expectations of $51.2M.

At this stage of a turnaround, ugly headline numbers like those seen in the first quarter are to be expected. At the end of the day, we are buying a stock that is down ~70% from its all-time highs, an entry point that more than compensates us for the -3.9% decline in global comps seen during the quarter.

What matters to us is not a single quarter’s results, but what management is doing to FIX the business over the long term. On that front, the picture is far more encouraging than the headlines suggest, with the right ingredients in place to drive a turnaround over the next few years and reward us handsomely in the process.

A key part of the turnaround playbook is a rebuilt innovation pipeline that is finally putting compelling products back on the menu and getting traffic in the door.

Leading that charge is Pan Pizza, the first major launch of 2026 and the brand’s first new crust platform in nearly a decade. Following its nationwide rollout in late January, Pan continues to track ahead of expectations, supported by strong repurchase rates. Management is building awareness and extending the rollout into priority international markets as part of a broader push toward premiumization and, ultimately, a Michelin star ambition.

In late March, the company launched oven-toasted sandwiches, opening an entirely new category aimed at increasing participation across both dayparts. Early results have been encouraging, with the sandwiches generating strong incremental sales and already outselling Papadias, a now-discontinued “rhythm breaker” alongside Papa Bites that once clogged the make line with operational complexity.

Management also announced that its cult-favorite garlic sauce will hit retail shelves nationwide this summer across ~7,500 distribution points, including Walmart (WMT), Kroger (KR), Albertsons (ACI), Safeway, and H-E-B. The move creates yet another incremental revenue stream while extending brand awareness beyond the four walls of the restaurant.

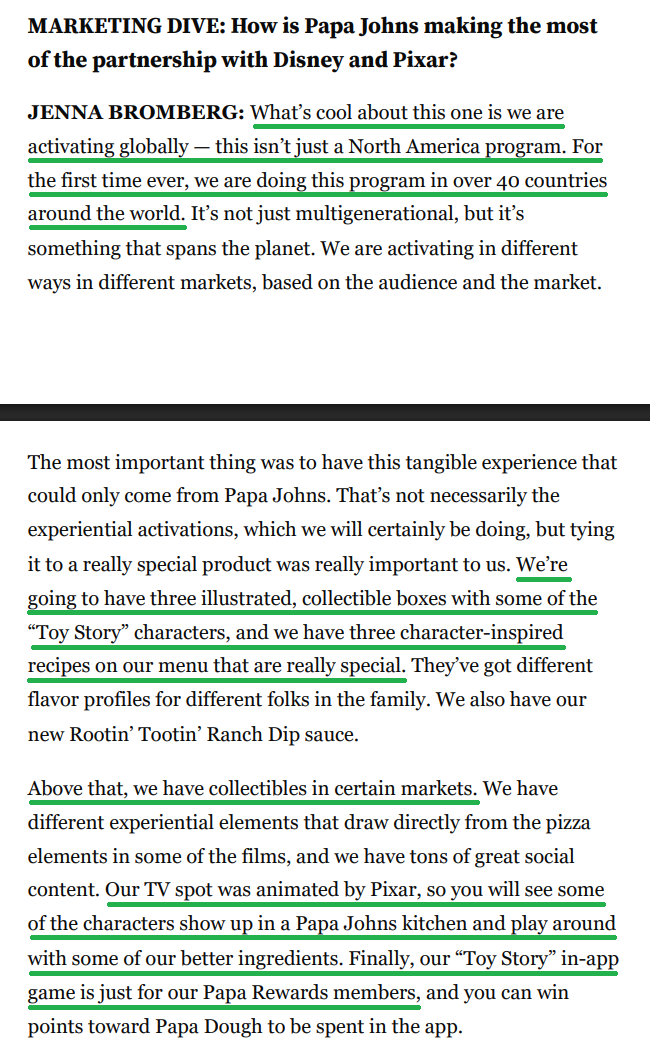

At the same time, Papa John’s is leaning into high-profile partnerships to build momentum, headlined by a recently announced collaboration with Disney (DIS) and Pixar tied to the upcoming release of Toy Story 5, its biggest cultural push yet. The campaign spans 43 markets and includes themed personal pizzas, custom packaging, and four Pizza Planet experiences, all built around a new 8-inch personal pizza platform that management views as a strong customer acquisition vehicle going forward. As longtime readers know, we also own Disney, which makes this a nice overlap across two of our holdings.

Below is a transcript of an interview with Papa John’s CMO Jenna Bromberg, who discusses the partnership and, just as importantly, the return of local marketing co-ops. These co-ops were instrumental in building the Papa John’s brand in the first place, were later phased out in favor of a national marketing strategy under prior management, and are now being stood back up. Today, ~50% of the U.S. system is supported by local co-ops across 50+ markets, which we view as one of the more underappreciated drivers of the turnaround.

Each of these initiatives is doing exactly what management set out to do: improving mix, driving add-ons, and expanding the addressable market. Taken together, they form a combination of top-line catalysts that we believe can support a strong recovery in the back half and beyond.

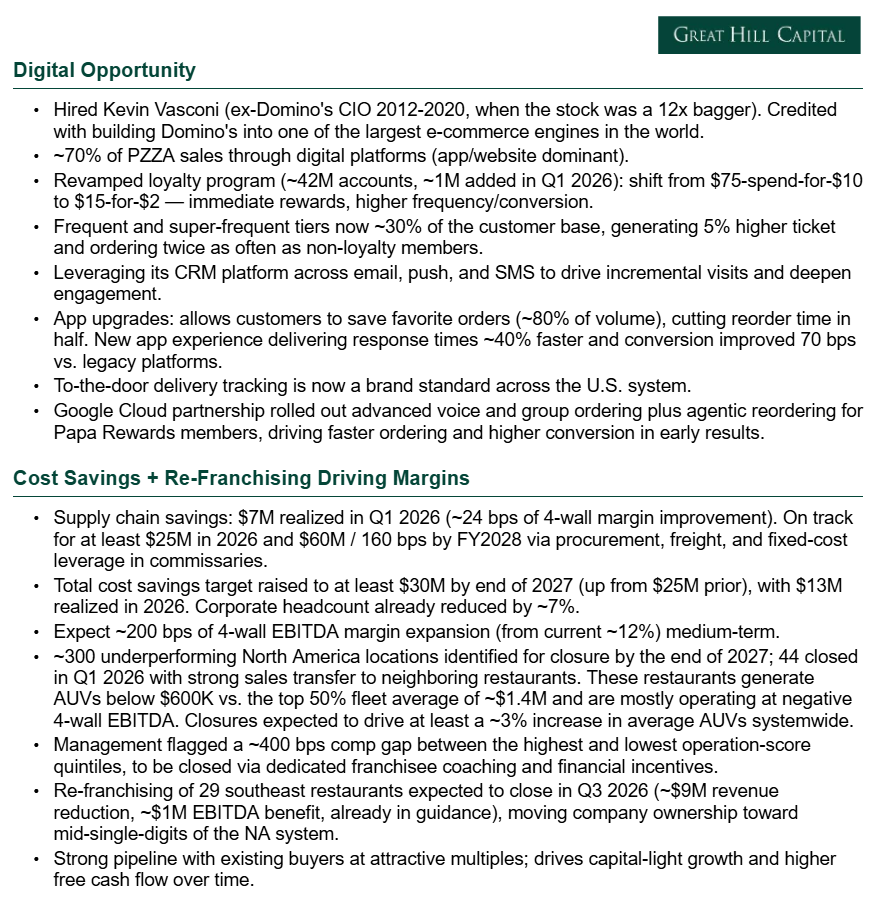

In the meantime, management is undertaking the serious and long-overdue heavy lifting required to improve profitability. The company is executing a plan to remove ~$90M of costs from the business through supply chain savings (~$60M) and G&A reductions (~$30M) by FY28, a program expected to drive ~200 bps of 4-wall EBITDA margin expansion over the medium term.

PZZA is also taking a page from the same playbook that successfully turned around international operations, closing ~300 underperforming North America locations by the end of 2027. These units generate AUVs below $600K compared to a top-half fleet average of ~$1.4M, with many operating at negative 4-wall EBITDA.

Lastly, management is accelerating re-franchising activity as it works toward reducing company ownership to the mid-single digits of the North America system, a shift that leaves Papa John’s with a more asset-light, higher-free-cash-flow model. Even after closing the 85-restaurant transaction in Q4, the domestic company-owned fleet still accounts for ~13.1% of the North America system as of Q1. Management continues to see a strong pipeline of buyers at attractive multiples, including a 29-unit transaction in the Southeast expected to close by Q3.

None of this work is flashy or glamorous. It is operational blocking and tackling, the type of work a turnaround at this stage requires and what you would expect from a management team focused on long-term value creation rather than the next headline.

That level of execution and focus is also not consistent with a management team looking to sell the company at the bottom of the cycle, despite the steady drumbeat of reports surrounding Irth Capital’s offer.

These bottom-of-the-cycle bids are familiar territory for us and for Papa John’s. We’ve seen the same pattern of lowball offers emerge across several early-stage turnarounds we have held, whether GOOS, GXO, PYPL, or now PZZA. In each case, our view has been the same: there is far more value in executing the turnaround successfully than accepting an in-the-hole buyout that robs shareholders of the upside ahead.

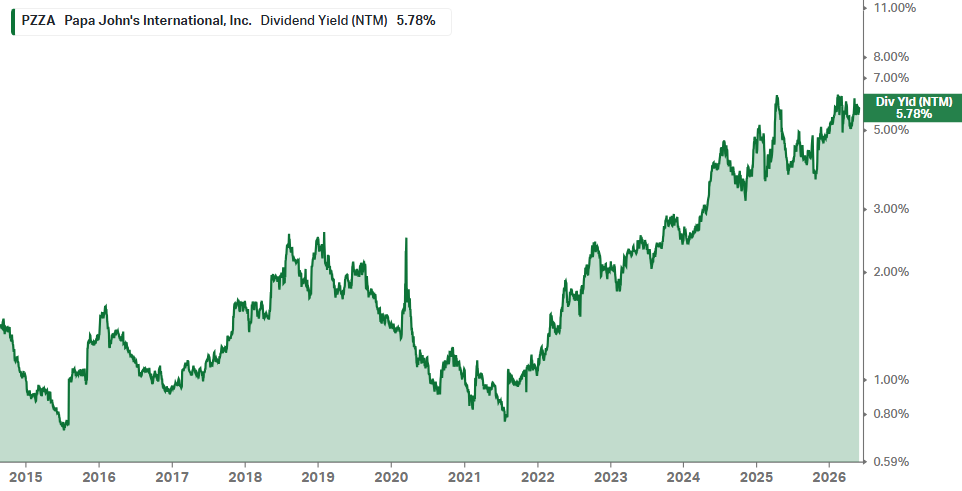

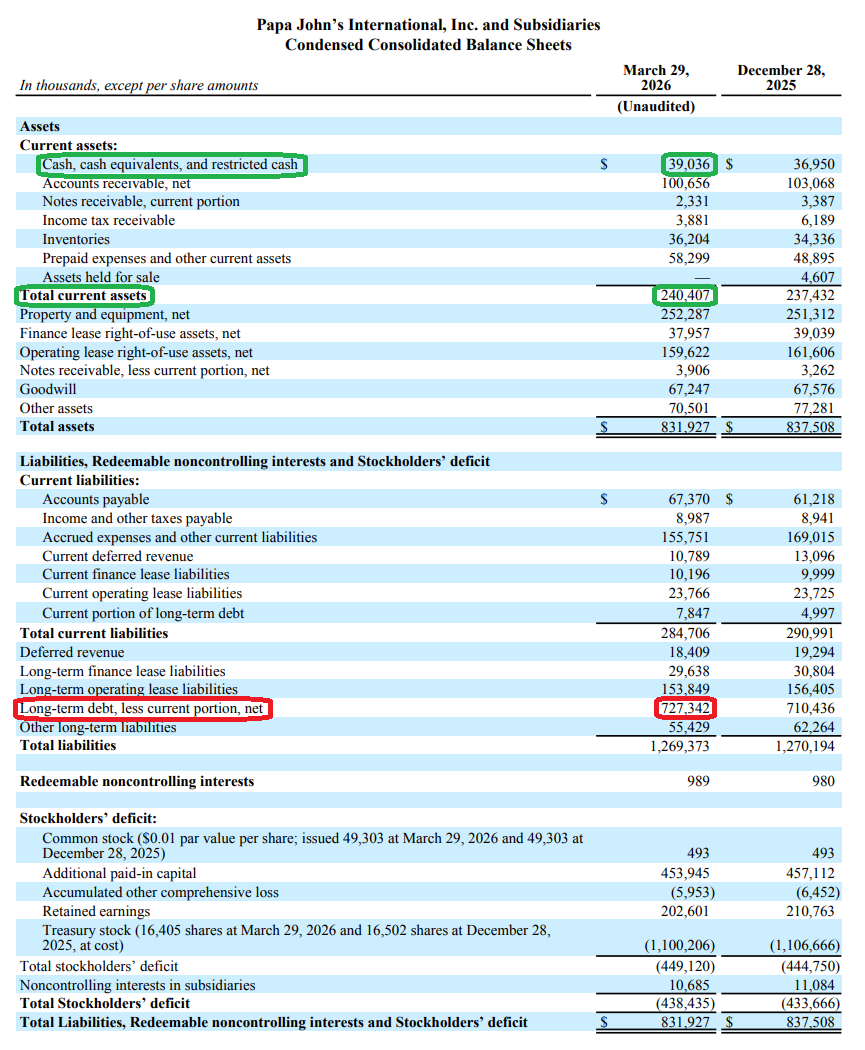

We’d much rather sit back, give management time to execute, and lock in a ~5.8% forward dividend yield, the highest available to investors at any point in PZZA’s operating history, all supported by a balance sheet with no major maturities until the end of the decade.

Sooner or later, the market will come back to a simple truth: Americans love pizza. That isn’t going anywhere, and neither are we.

Q1 Earnings Breakdown

10 Key Points

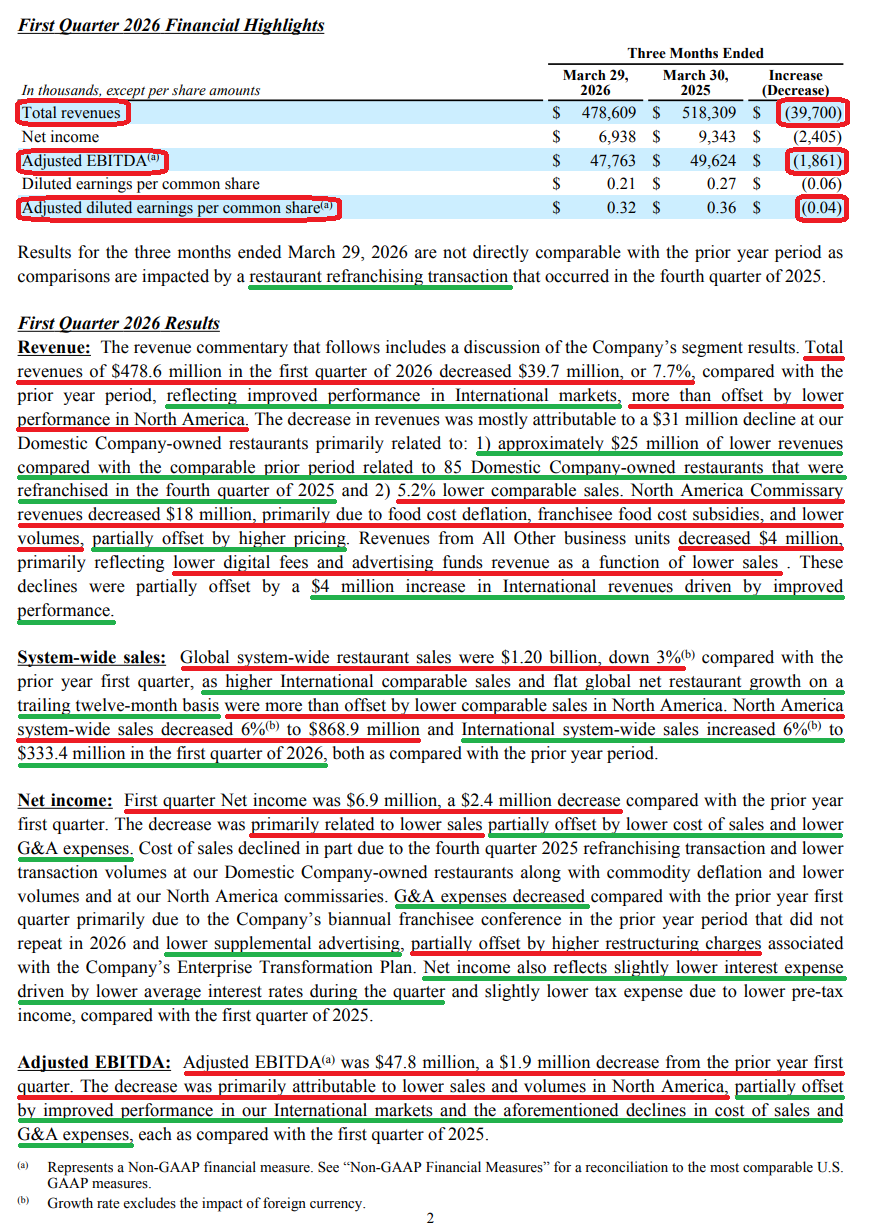

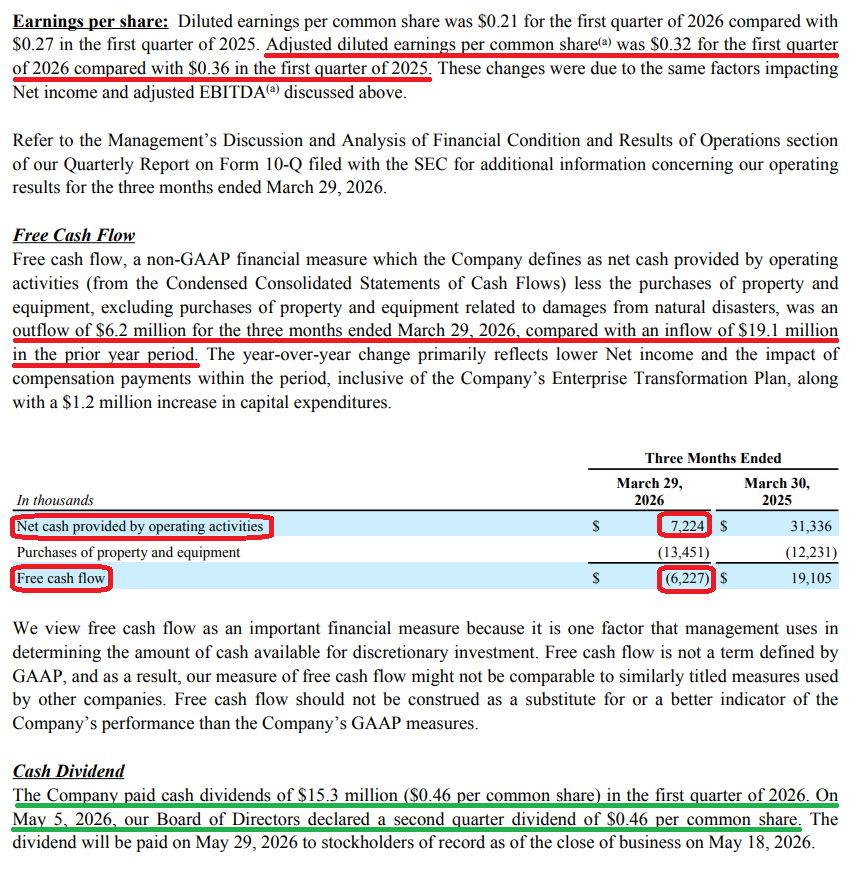

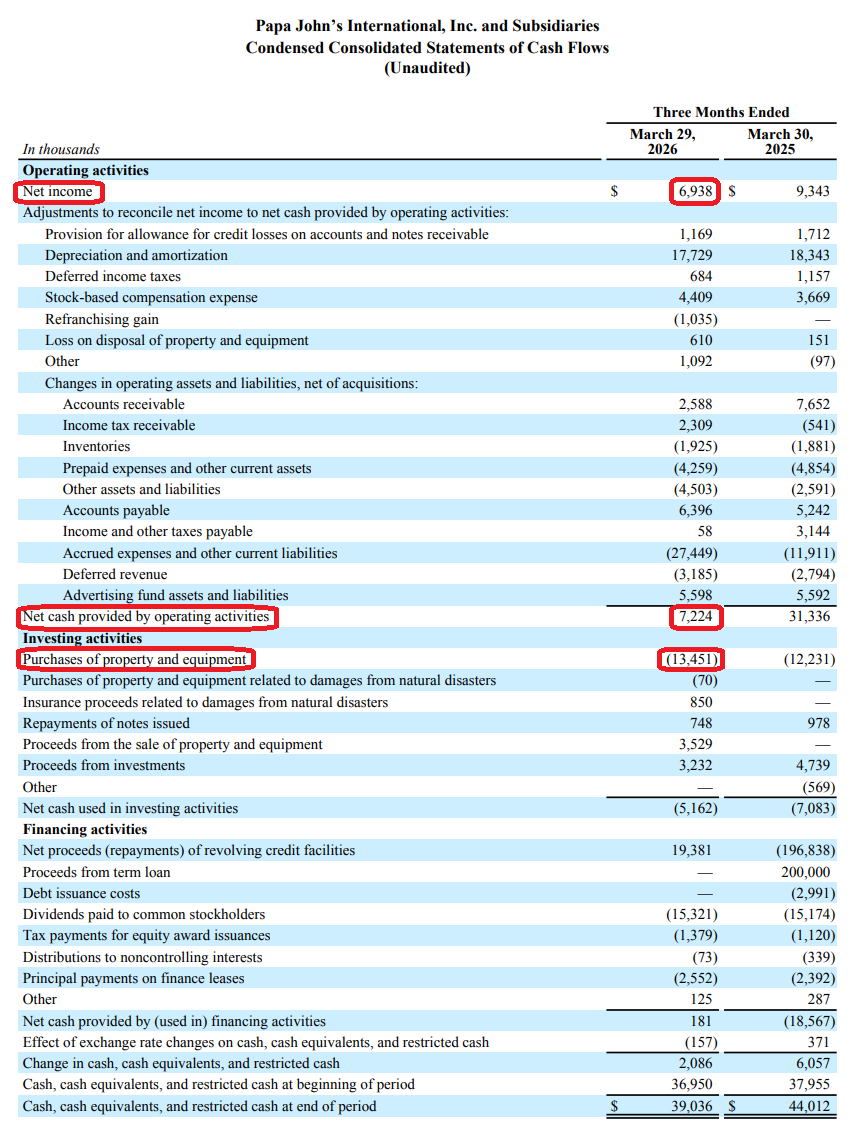

1) Q1 revenue came in at $478.6M (-7.7% Y/Y), missing consensus of $485.5M. The decline was driven by a ~$31M drop at domestic company-owned restaurants, of which ~$25M was attributable to the Q4 2025 re-franchising of 85 corporate restaurants, with the remainder reflecting a 5.2% comp decline at remaining company-owned stores. Global systemwide sales were $1.20B (-3% Y/Y in constant currency), with global comps down 3.9%.

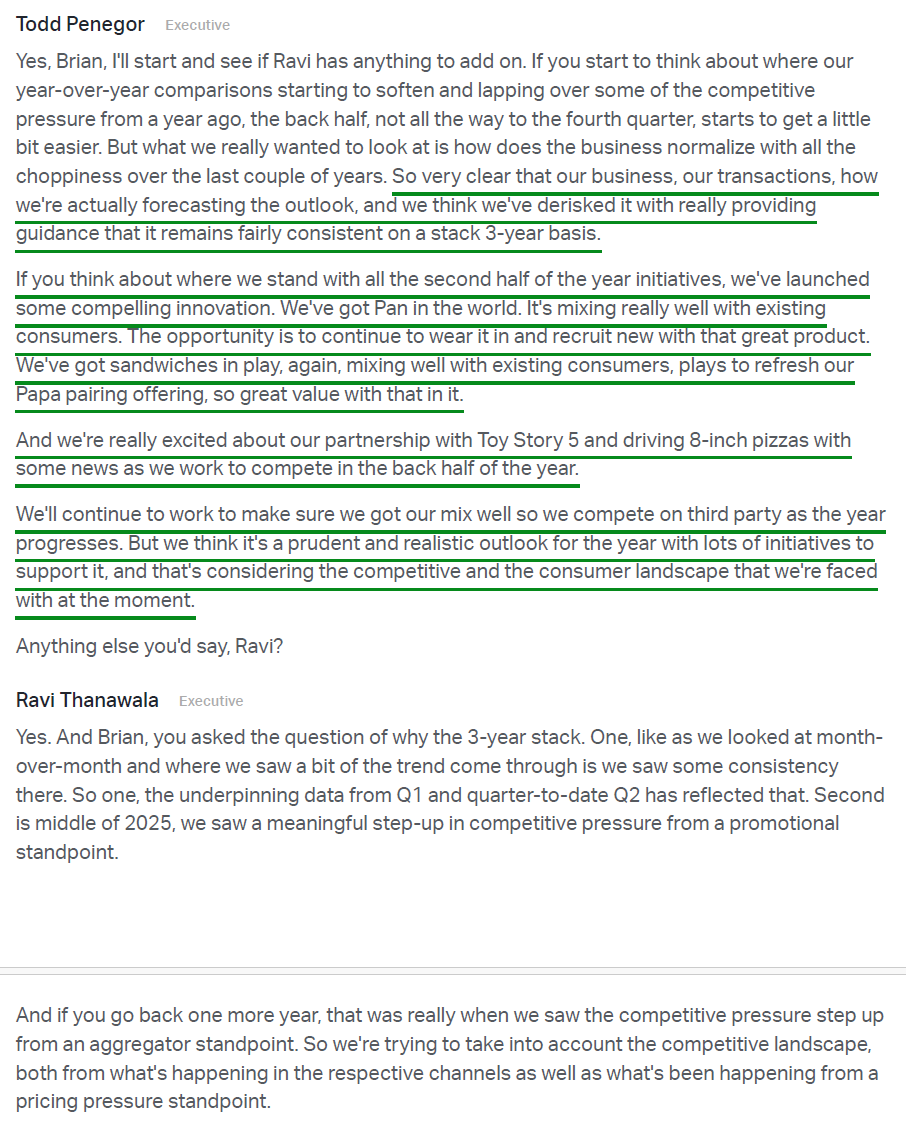

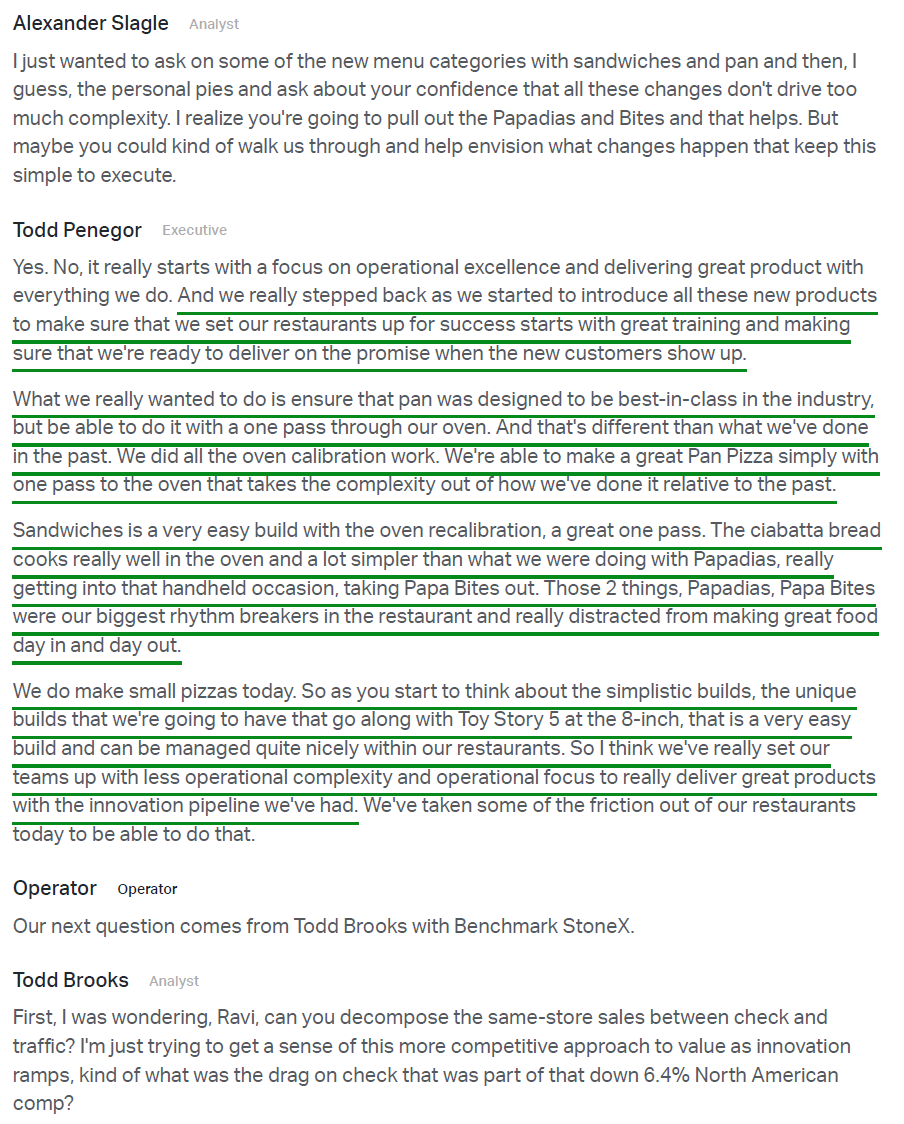

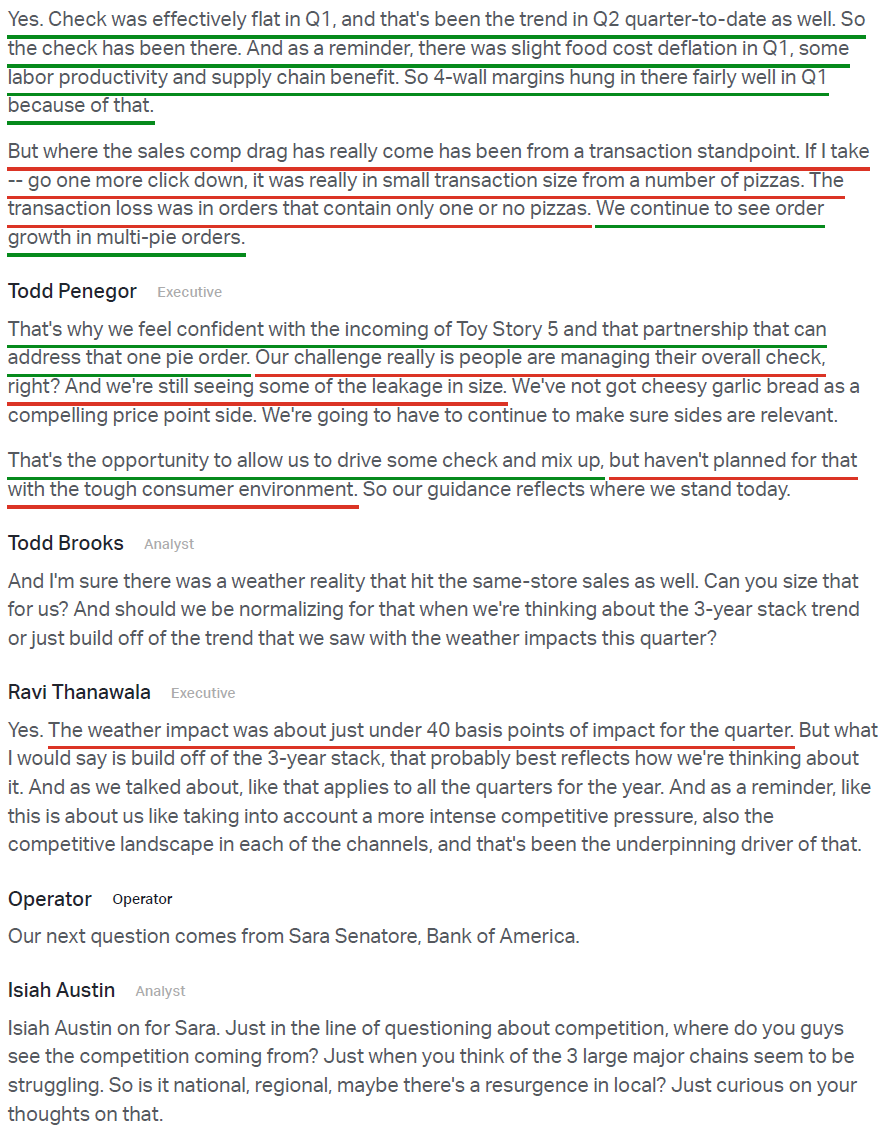

2) North America Q1 comps came in at -6.4% Y/Y, below consensus of -4.6%, as a cautious consumer and an aggressive QSR promotional backdrop weighed on results. Company-owned comps declined 5.2% and franchised comps fell 6.7%, resulting in a 6% decline in NA systemwide sales to $868.9M. The decline was entirely transaction-driven, with check effectively flat, while severe weather across two weeks of the quarter was a ~40 bps headwind. Underlying pizza demand remained stable, with volumes flat ex-weather, multi-pizza orders growing, and pies per order up 5%, while weakness was concentrated in one-or-no-pizza transactions.

3) International remains the clear bright spot, with Q1 comps +3.6% Y/Y, marking six consecutive quarters of positive comp sales. Strength was broad-based across focus markets: the UK accelerated to +11% (vs. +7% in Q4) on stronger execution and increased media investment, the Middle East rose +9% on sustained transaction growth, and Asia Pacific gained +5% led by continued strength in Korea. International systemwide sales increased 6% in constant currency to $333.4M, with 20 new restaurants opened across the segment during the quarter.

4) Q1 adjusted EBITDA came in at $47.8M (-3.7% Y/Y), missing consensus of $51.2M. The decline was driven by NA volume deleverage and elevated commissary food costs (to be recovered through pricing in subsequent quarters), partially offset by international strength, lower G&A, and lower supplemental advertising. Domestic company-owned 4-wall EBITDA was $16.6M at an 11.9% margin (+140 bps Y/Y), holding up better than expected on supply chain benefits and disciplined value execution. NA Commissary segment EBITDA margin was 5%, down 230 bps due to franchisee food cost subsidies, higher food costs, and lower volumes.

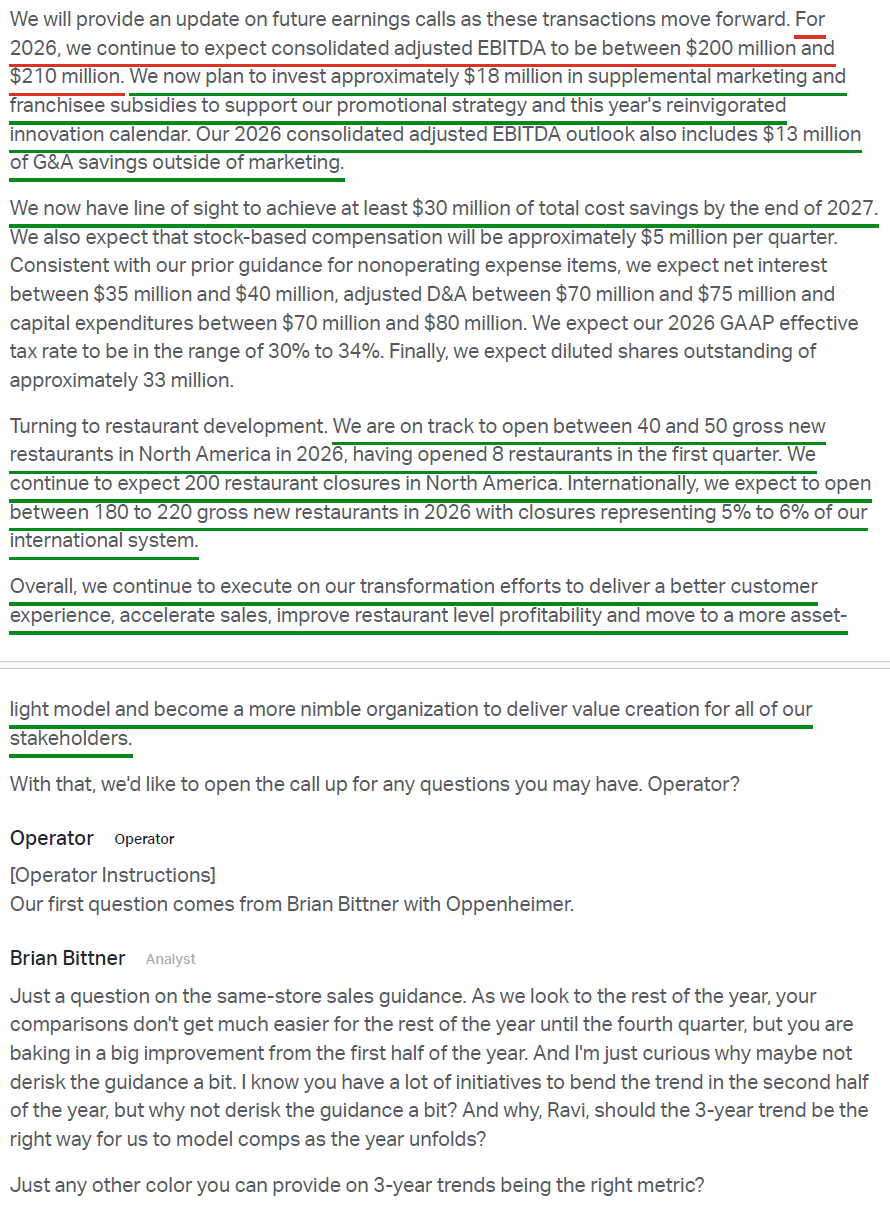

5) Management continues to execute on right-sizing the cost structure, capturing $7M in supply chain savings in Q1 (~24 bps of 4-wall margin improvement) and remaining on track for at least $25M this year, with at least $60M / 160 bps targeted by 2028. The total cost savings target was also raised to at least $30M by the end of 2027 (up from $25M prior), with $13M of G&A savings outside marketing expected in 2026. Together, these initiatives keep PZZA on a clear path to at least 200 bps of total 4-wall EBITDA improvement over the medium term, driven by supply chain savings, labor and market optimization, and portfolio rationalization.

6) On portfolio optimization, PZZA closed 44 of the 300 identified underperforming NA locations in Q1, with early results showing strong sales transfer to neighboring restaurants. These sites are primarily decade-old franchise units with AUVs below $600K that predominantly generate negative EBITDA. Management also highlighted a ~400 bps comp gap between the highest and lowest operation-score quintiles, which it plans to narrow through dedicated coaching and financial incentives for franchisees. On the re-franchising front, the sale of 29 Southeast restaurants is expected to close in Q3 2026 (~$9M revenue reduction and ~$1M EBITDA benefit, both already included in guidance), further reducing company-owned locations toward the mid-single digits of the NA system and incrementally shifting PZZA toward a more asset-light, higher-free-cash-flow model over time.

7) PZZA’s rebuilt innovation pipeline is beginning to drive momentum, with two new platforms launched in the first three months of the year alone. Pan Pizza, which launched in late January, is tracking ahead of expectations on strong repurchase rates, with plans to expand into priority international markets. Oven-toasted sandwiches launched in late March are already exceeding Papadia sales without complicating the make line, and Cheesy Garlic Bread followed in April as a value add-on. Beyond the menu, PZZA is leaning into brand partnerships to drive customer acquisition, headlined by a Toy Story 5 collaboration, built around a new 8-inch personal pizza platform management views as a future acquisition vehicle. PZZA is also rolling out its iconic garlic sauce at retail this summer across 7,500 distribution points (Walmart, Kroger, Albertsons, Safeway), a new sales layer that extends the brand beyond its restaurants and expands the top line.

8) PZZA continues to rebuild its local marketing strategy, with ~50% of the U.S. system now supported by local co-ops across more than 50 markets. To support the effort, PZZA plans to invest ~$18M in supplemental marketing and franchisee subsidies in 2026 (trimmed from ~$22M previously), helping get the co-ops on their feet as local operators align around a unified market strategy. Management expects the reestablished co-ops to let operators compete more effectively at the local level through better coordination between national marketing programs and local efforts, with benefits building throughout the year.

9) Progress on the digital front continues, with Papa Rewards loyalty members now approaching ~42M (~1M added in Q1), while frequent and super-frequent tiers now represent ~30% of the customer base, generating 5% higher ticket sizes and ordering twice as often as non-loyalty members. Management is also engaging customers more frequently through targeted, personalized communications across email, push, and SMS to drive incremental visits and deepen engagement. On the experience side, to-the-door delivery tracking is now a brand standard across the U.S. system, while the Google (GOOGL) Cloud partnership rolled out advanced voice and group ordering plus agentic reordering for Papa Rewards members, with early results showing faster ordering and higher conversion.

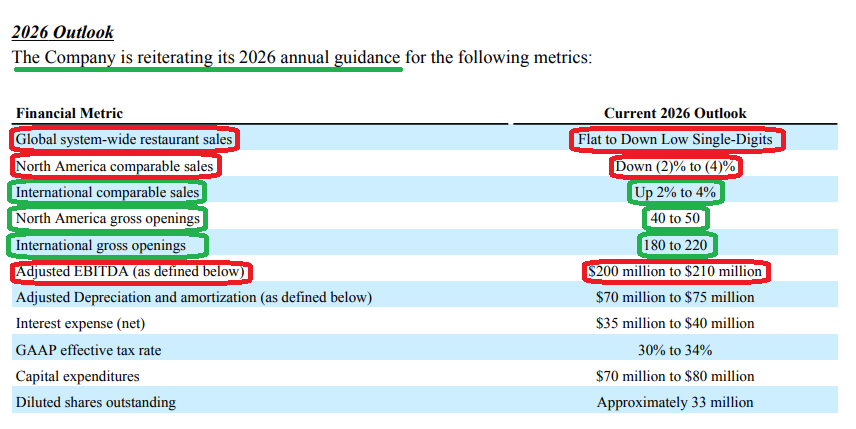

10) FY26 guidance was fully reiterated, calling for global systemwide sales flat to a low-single-digit decline, NA comps of -2% to -4%, international comps of +2% to +4%, and adjusted EBITDA of $200M to $210M. Management expects sequential top-line improvement through 2H26 as the rebuilt innovation pipeline, co-op activations, the Toy Story 5 collaboration, and a sharpened aggregator strategy compound. PZZA still expects 40 to 50 gross NA openings and 180 to 220 international openings, alongside ~200 NA closures.

Earnings Call Highlights

General Market

The CNN “Fear and Greed Index” ticked down to 57 this week from 61 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

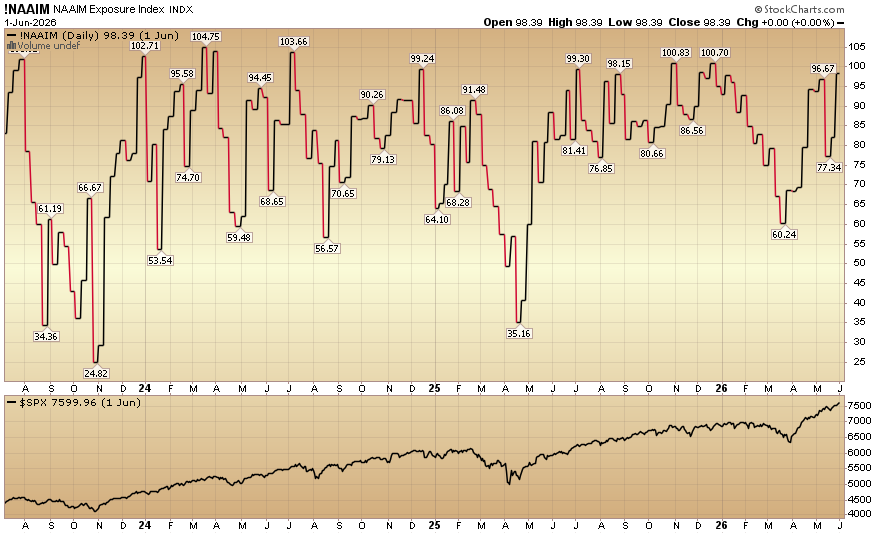

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 98.39% equity exposure this week from last week’s 82.02%.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms

Comments

Log in or sign up to join the conversation.