We expect the Fed to be at best cautiously optimistic today but members forecasting a hike by end-22 could constitute a communication accident. In Europe, the debt tsunami continues with long-end deals from Germany and Finland.

Fed today, dovish but beware the dot plot

The main event today will occur after the European close but its proximity is likely to drive price action anyway. To be perfectly clear, our economics team does not expect the Fed to subscribe to the improvement in sentiment since last week. Granted, some indicators, jobs primarily, are flashing amber but the risk of a growth accident later this year is simply too great to express anything else than cautious optimism.

On policy, we are not expecting any change to a QE guidance that features no target purchase amount. There is scope for the Fed to introduce Yield Curve Control (YCC) later this year as a form of tapering, or to reinforce the message from forward guidance. An acknowledgement that one of QE’s aims, to restore market functioning has largely been reach is conceivable, but the attention is more likely to be on the projection material.

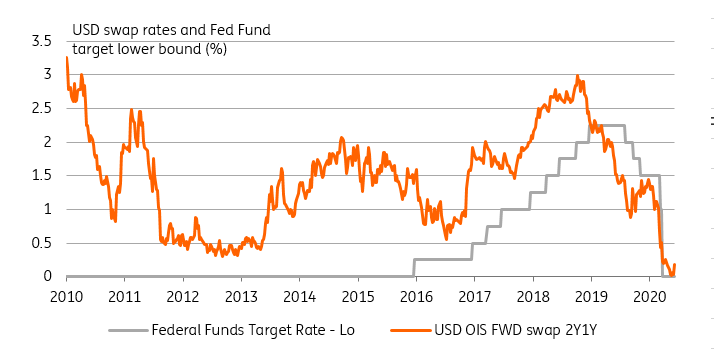

As our US economist noted, a hike forecast for 2022 would be the final nail in the coffin for rate cut expectations. Despite the rise in front-end USD rates since last week, this is far from being the central scenario discounted by the OIS curve. If it isn’t strongly qualified with forward guidance, and/or YCC, we see room for a correction higher in 2Y forward starting 1Y OIS swap for instance.

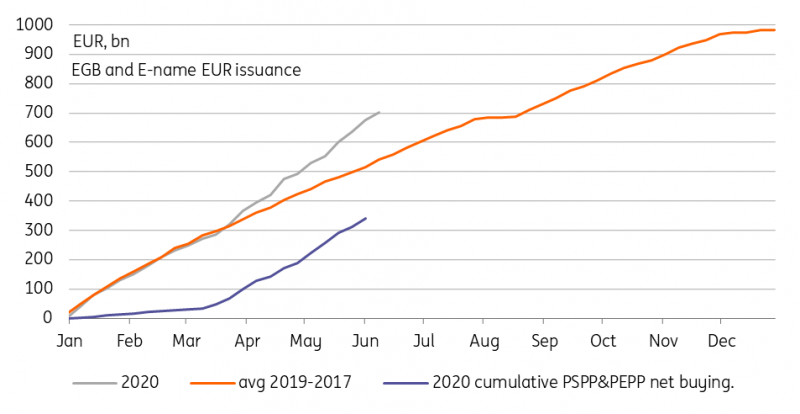

The debt tsunami continues, but so does the ECB buying

Yesterday was an extraordinary day in primary markets with €21bn sold across three syndicated deals on top of close to €6bn in regular auction sales. With ECB bond purchases ensuring a favourable market backdrop the demand for the deals was more than healthy. The combined books for the three syndicated deals showed an interest of more than €160bn. Nonetheless, such supply volumes do leave marks in the market with the spreads of peripheral governement bonds having widened notably, 10Y Spain now trading more than 10bp wider versus Germany since the start of the week for instance. Yesterday's deals in more detail:

- Spain sold €12bn in a new 20Y bond, against a €78bn book. It has been Spain’s fourth bond launch with an initial size of €10bn or greater this year and means that the country has now completed 66% of its bond funding target for the year – although one has to add that (upward) revisions are becoming more frequent.

- Ireland sold €6bn in a new 10Y with a book of €69bn which means that 80-90% of this year’s envisaged bond funding target has been reached.

- Greece sold €3bn in a new 10Y with a book of €15.8bn, implying that 94% of its initial funding target has been reached. Greek government bonds have only been added to the ECB’s list of purchases with the introduction of the PEPP in March.

The bond supply flurry continues today with Finland having mandated banks with the sale of a new 20Y bond, joining Germany in the syndicated tap of its 30Y bond. Both should price today and we expect the deal sizes to be at least €3bn each although success in yesterday's deals could provide an incentive to sell more. This come on top of a regular Portuguese bond auctions today of up to €1.5bn.

ECB net buying matches the supply flurry

Source: Bloomberg, ECB, ING

Today's events: Fed meeting and more supply

Today's supply slate in Europe includes the 30Y Germany and 20Y Finland deals mandated yesterday. Portugal will also sell 6Y and 10Y debt.

Not that the ECB's stance needs much clarification but Muller, Kazimir, and Schnabel are scheduled speakers. The latter in particular should be closely watched as she revealed overnight that the ECB is looking at the pros and cons of price-level targetting. We are less likely to get information about plans for a bad-bank offloading soured loans from Eurozone bank balance sheets,

In data, the US CPI is the most important release although its relevance might be less than usual given the shift in spending patterns during lockdown.

Comments

Log in or sign up to join the conversation.