The US election night casts its shadow ahead. The risk of lingering uncertainty in the coming days paired with rising Covid-19 numbers has sidelined reflation hopes. The ECB has not backed up its promise for December action with increased purchase volumes - the past weeks appeared more dedicated towards straightening out imbalances vs. the capital key.

Source: ECB, ING

Overnight: RBA joins the bandwagon

The Reserve Bank of Australia joined the group of central banks adding to already impressive easing packages by cutting both its cash rate and target 3Y yield to 0.1%, their all-time low. It also committed to buy A$100bn of 5-10Y debt over the next 6 months.

Improving risk sentiment put government bonds on the back foot in the overnight session although much depends on the result of today's US election. The risk of contested results should dim risk appetite until well into tonight in our view.

Post election uncertainty sidelines reflation hopes

Or economist has outlined the implications of the different election outcome scenarios in detail here. With the final election results potentially not known for days, markets appear more inclined to reduce risks. Yesterday’s surprisingly strong ISM manufacturing release has failed to reignite the reflation trade with 10Y US treasury yields instead falling below 0.85% again.

In Europe Lagarde’s easing pre-commitment last week has already managed to put a wedge between US and EUR rates dynamics. The 10Y Bund yield has largely traded in a -0.64 % to -0.62% range since the ECB meeting. The hopes for a comprehensive package at the December policy meeting have also kept spreads of periphery bonds over Bunds in check. As we have pointed out before, the main hawkish risk now lies in the discussion of how such a package might look.

Last week Austria’s Holzmann dampened hopes for a rate cut (not part of our expectations either). Yesterday ECB’s Mersch dismissed the notion that some of the pandemic emergency purchase programme’s (PEPP) flexibility could be inherited by the more standard purchase programmes (APP incl. PSPP). Our economists believe a QE expansion via the latter is likely, but market enthusiasm for that option could be dampened if Mersch's considerations catch on.

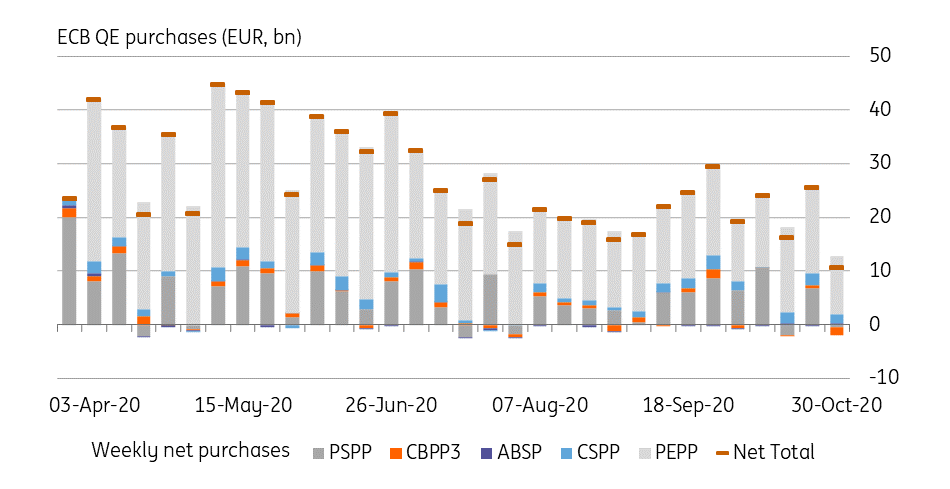

ECB: No added signal via current purchase volumes

Those that hoped the ECB could send a signal by stepping up its weekly purchase volumes were disappointed – at least for now. Last week's net purchase volume even dropped compared to the previous week, with pandemic emergency purchases (PEPP) falling to €10.8bn from €25.7bn. Public sector net purchases were even slightly negative last week, which does suggest that sizeable redemptions are distorting the overall picture, also in PEPP. The release of the ECB's weekly financial statement today should provide more clarity.

The ECB also provided more detailed data for the entire month of October, unfortunately not for PEPP this time as data for this programme is made available only every other month. The country split under PSPP, which accounted for 75% of overall purchases in the month, suggests that the ECB is trying to straighten out imbalances in the allocations. It purchased above capital key implied volumes in Germany and the Netherlands where a deficits versus the key had accumulated and below the key in France and Italy, where purchases had previously been larger. Net supra purchases were also negative in the month.

The EU’s €17bn SURE transaction which settled on 27 October would have come too late in the month as no primary market purchases are allowed for the ECB. That said, the EU sent out a RFP to banks for a next transaction potentially as early as next week.

Today’s events: US factory orders, ECB Knot

The data calendar has little to offer with mainly the US factory orders of note, but eyes should be set on the US elections starting today and with results for some states known before the European open. ECB’s Knot could give more hints regarding the central bank’s internal discussion of what tools to deploy in December. Ther is also a Eurogroup meeting that is attended by ECB's Lagarde and Panetta.

In primary markets Austria will reopen a 20Y bond (€0.69bn) and Germany taps an inflation linked bond (€0.5bn).

Comments

Log in or sign up to join the conversation.