The Yield Curve

I have often written about one of the few indicators in economics that has earned its reputation over the years, and for good reason. It has preceded virtually every US recession since World War II. I’m talking about the inverted yield curve.

The only recession in the modern era that occurred without an inverted yield curve was COVID, and that was an externally imposed shock, not a cyclically generated downturn. You were never going to get an inverted yield curve warning that a virus was about to shut down the global economy. It just can’t happen. If we are heading into something difficult this time, we’re probably not going to get an inverted yield curve telling us it is coming either. If we did get an inverted yield curve, it would probably be because we are already in a deep recession.

COVID scrambled the normal economic cycle, which may be the understatement of the decade, but so did the Fed's response: zero rates, massive balance sheet expansion, direct income transfers. We compressed years of adjustment into months.

We skipped something. We went from one kind of world directly into another and that transition left many of the old instruments pointing in the wrong direction. Speaker after speaker kept arriving at the same uncomfortable place during the conference: the old relationships are not behaving the way they used to. The old frameworks aren't working like they used to. In a departure from being your humble analyst, I would like to point out I was making this exact point over two years ago. We can no longer trust past correlations as a means to predict anything, especially markets and economies. Most were iffy at best, but now even more so.

And the old data is failing to demonstrate its intended purpose, not because it's lying, but because it isn't saying what it used to. Past performance is not indicative of future results.

The Labor Market

Last week I quoted David Rosenberg on the payroll revisions. I want to go deeper into what he said about the labor market, because the revision story is only the beginning. Rosie looked at the composition of where job growth, or lack thereof, has been coming from, and what that tells us about the broader economy.

"Health and education, employment, that's in a boom, 2.5% growth. The rest of the workforce, the other 82% of employment has actually gone down in the past year, and I'm supposed to believe this is a normal labor market on our hands."

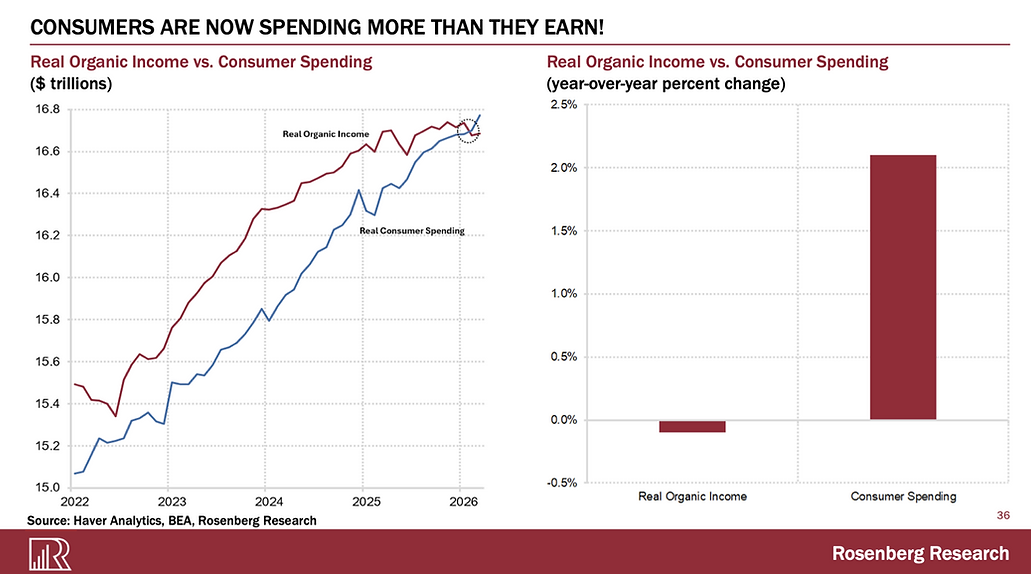

He also made a point about consumer income that I think gets lost in the headlines:

"Real organic income — from the national accounts, that is real personal income excluding government handouts — is negative. It's negative. Where's consumer spending? Up over 2%. But you see, because we're so narcissistic and we judge economic success because of how much we're spending..."

The gap between what Americans earn and what they spend is being filled by a declining savings rate, now at 3.6%, down from 8% pre-COVID. At some point, that math stops working. We just don't know exactly when.

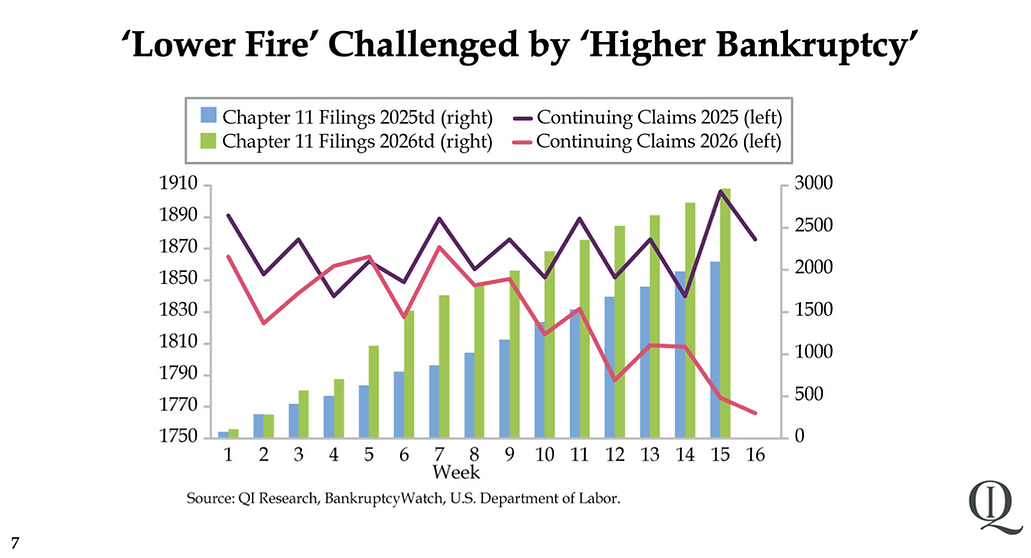

Danielle DiMartino Booth may have clocked it. She came to SIC not to debate whether recession is approaching because it may have already arrived. She pointed to something that doesn't get revised away, bankruptcy filings.

"If you see that continuing jobless claims in 2026 look better than 2025, then why are those Chapter 11 filings higher in 2026 than they are in 2025? Where are these people going? Why aren't they being picked up in the official data? We have to ask these questions because these bankruptcy filings are also hard data."

Her point is that the people disappearing from the jobless claims data aren't finding good jobs. They're falling into gig work, non-participation, underemployment. The official numbers look fine. The bankruptcy filings suggest something else is happening underneath. She called it outright: "there is some very conflicting data that we're dealing with right now." When you look at the broad data, a lot of it is conflicting. It’s the whole past performance thing.

Speaking of reframes, Jim Bianco has been one of my most valuable sources for many years. His slide presentations are magnificent, he has a screen where he can draw on the charts as he speaks, a bit like John Madden doing football analysis. His point was not that the labor market is strong. It’s that zero job creation is the new normal, and that it is arithmetic, not a crisis.

"How many jobs does the US economy need to create? The answer on that might be zero."

I will admit I had to sit with that for a moment. The fertility rate is at a 200-year low—1.62, well below the 2.1 replacement rate. Immigration has gone net negative. The working-age population is effectively flat. You do not need new jobs if you are not creating people to fill them. The unemployment rate has not spiked, not because the labor market is strong but because the supply of workers is not growing. Zero job creation used to signal economic distress. Now it may just signal demographics.

The BLS numbers the Fed is reacting to have been revised by amounts that should give everyone pause. What was reported as 1.7 million jobs created came in after revisions at 123,000. Off by 93%. Eleven of every twelve reported jobs were phantom. I have spent some time trying to think of a more polite way to describe what that means for policy decisions made on those numbers. I have not found one.

I understand the reasons for that. They are very well known, although not written about much. The actual process is done over three months. Pre-pandemic the number was north of 75% that would report in the first month. Today it is 60% or less. Eventually 95% of businesses report by the third month. But that means a great deal of data comes in later and so naturally there will be revisions. That has historically been the case, but not revisions where 90% of the theoretical jobs get revised away.

Where did they come from? Our old friend, the birth-death model. Nothing conspiratorial here. Businesses are created and die every month. Part of a dynamic economy. And since the BLS does an establishment survey, by definition they are calling new startups because they are not established businesses. And businesses that die are not responding either so they don’t get that data.

But if you issued an employment report without making some assumption about the birth-death ratio, it would be significantly off. So the BLS uses a backward-looking model to forecast future employment from the birth death and businesses.

In essence, their model says that past performance IS indicative of future results. And historically, most of the time it is relatively in line. Where it is off is in changes as the economy either comes out of recession or is going into a recession and the historical backward-looking data doesn’t capture what’s actually happening in the current month.

During recessions or near-recessions, the model systematically assumes more business births than are happening, so the initial numbers end up too rosy. That said, lower first-closing response rates do increase the variance — the estimates become less reliable and more prone to large swings in either direction.

And between the two, we are getting historically high and unprecedented negative revisions, but because of what Bianco said above, it is not really impacting the unemployment rate. I will have to tell you that unemployment not going up significantly (10,000 new jobs a month is not significant, at least historically [note sarcasm]) and the unemployment rate staying benign was not on my bingo card.

That gets us back to the point I made earlier. Past performance does not indicate future results. We keep trying to interpret this economy using relationships and indicators built for a different world. Some still work. Some clearly do not. The difficult part, and I genuinely don't have a clean answer here, is figuring out which is which before the market figures it out for us.

Inflation, Again

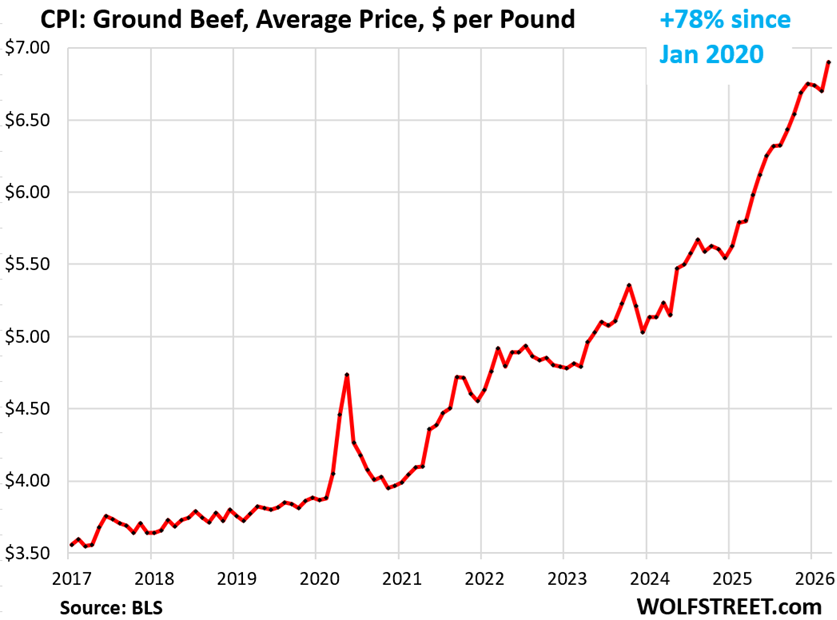

I wrote about inflation last week and had planned to leave it there. The data had other ideas. Inflation is proving far stickier than many expected, and not in ways consumers can easily ignore. Wolf Richter at Wolf Street published a food-price breakdown this week showing that ground beef is up 18.9% year over year to a record $6.90 per pound, steak up 17.1%, coffee up 29%. Since January 2020, food consumed at home is up 32%. My grocery bill would like a word with whoever decided inflation was transitory.

Source: Wolf Street

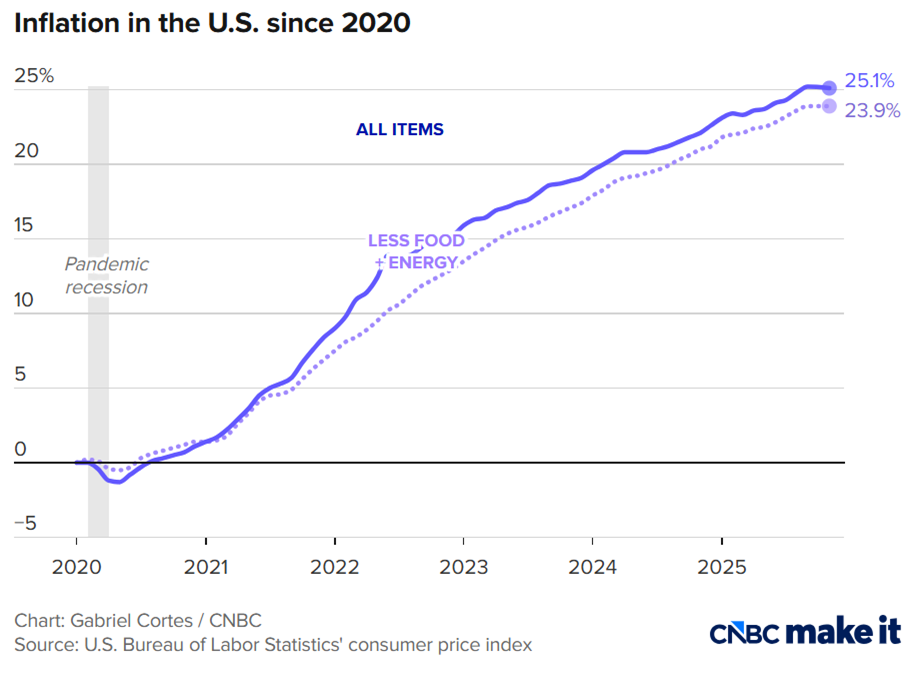

People do not experience inflation as a chart. They experience it every week at the grocery store. And these increases are landing on top of prices that were already painfully high. We are not talking about a fresh shock on a clean baseline. We are talking about acceleration on top of acceleration.

Source: CNBC

Most inflation charts show quarterly or annual inflation. In the real world we experience cumulative inflation, and the monthly number doesn’t mean much. So if the things we buy have seen a 25 to 30% inflation over the last five years, we experience it as 25%, not the 2-3% that it’s been in the last year.

At the same time, bond markets around the world are beginning to send a very different message than the one investors became accustomed to over the last 15 years. Peter Boockvar noted in his speech and then later updated his Substack this week that Japan's 30-year rose to 4.10%. UK long bonds are back to levels not seen since the 1990s. Germany's long bond yields are at 15-year highs even after the ECB cut rates by 200 basis points.

Source: Peter Bookvar

Peter described the corporate reality underneath the headline numbers at SIC in a way that I think captures the moment well:

"From a headline perspective, you can say, wow, the economy's doing great, but under the hood, how extraordinarily uneven and bifurcated it is."

During his presentation he mentioned that small business hiring within ADP went from 63,000 in the first quarter of last year to negative 200,000 from April through December. That was small businesses absorbing a cost shock and quietly contracting. The big numbers look fine. The small business numbers tell a different story. And that shows up in birth-death model revisions in the overall number.

We now appear to have weakening labor conditions and renewed inflation pressures developing simultaneously. That is an uncomfortable corner for any central bank to find itself in. It is a particularly uncomfortable corner for a Fed chair who has been in the job for one week.

The Warsh Situation

Kevin Warsh is inheriting a Fed in a genuinely difficult position. Inflation pressures appear to be reaccelerating even as parts of the labor market weaken underneath the surface. The bond market is already showing signs of discomfort with the idea of premature easing.

That creates echoes of earlier Fed moments, particularly the Volcker era. People forget how ugly that period really was. Volcker was burned in effigy by homebuilders. Farmers drove tractors to Washington to protest. Members of Congress sent him angry letters. The political pressure was enormous. He held anyway. That is what it took. Although Reagan didn’t reappoint him.

Not because the situations are identical. They clearly are not. Debt levels are dramatically higher today, financial markets are far more leveraged, and political tolerance for economic pain is considerably lower. But the core tension is recognizable: inflation remains persistent while markets and politicians both pressure the Fed toward easier policy. Who doesn’t like cheap money?

The market is now pricing roughly a 50% probability of another rate hike before year-end. Not cuts. Hikes. That is the bond market sending Warsh a message before he has even held his first press conference.

Is Warsh up to the challenge? I think yes. He understands the institution's pathologies at a deep level. He criticized QE from the inside. He wrote "Defining Deviancy Up" in 2009, one of the great speeches in the history of central banking, warning about exactly the path we have been on. If you have not read that speech, you should, as it will tell you a great deal about the man that is now the new Federal Reserve chair. It holds up remarkably well 17 years later. Being right and being handed the keys to fix it are two very different things.

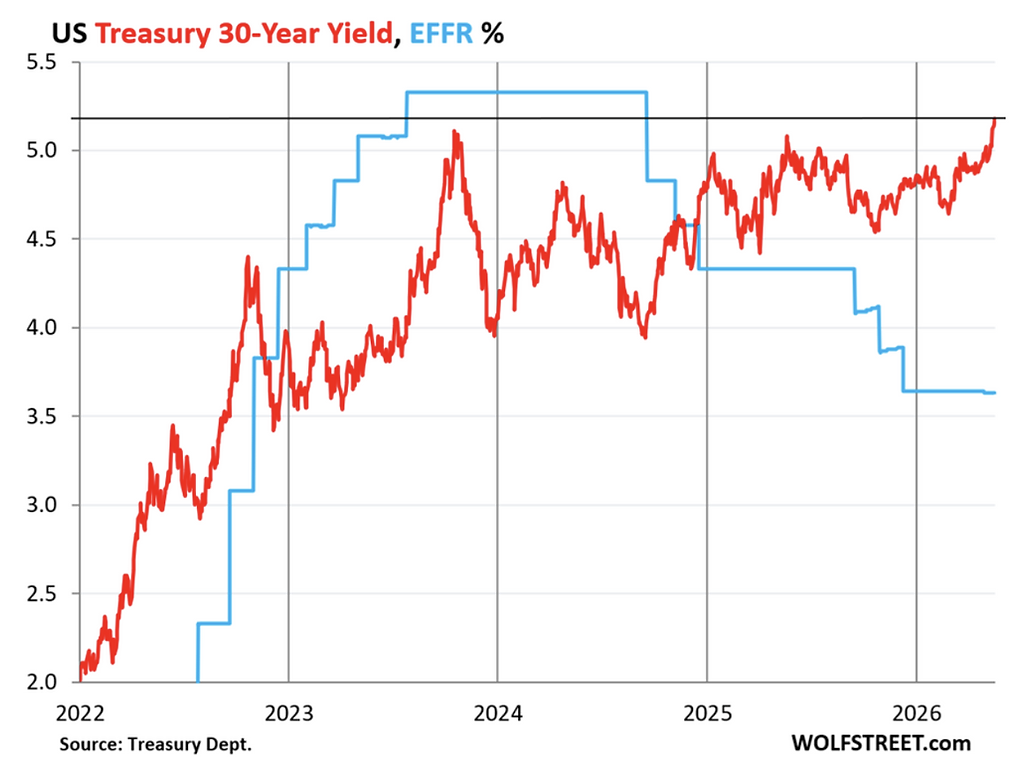

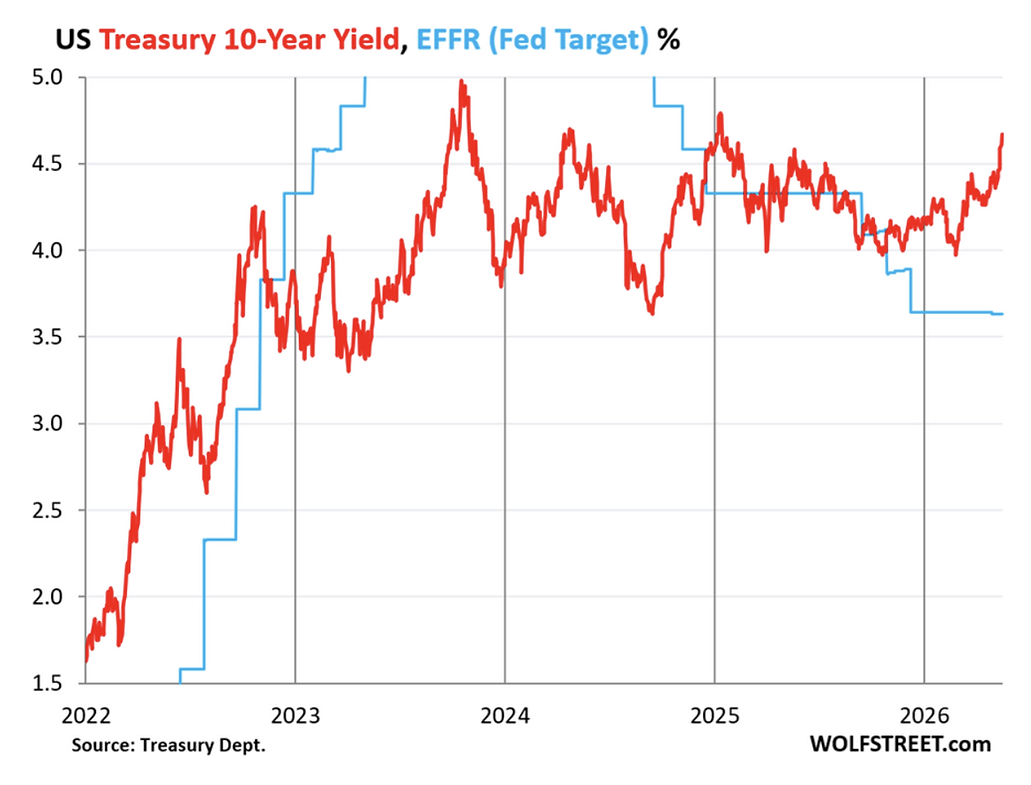

As I write this, the 30-year Treasury yield has risen to 5.19%, the highest since June 2007. The 10-year is at 4.67%, up 70 basis points since the end of February.

Source: Wolf Street

Source: Wolf Street

The bond market is telling us something the Fed does not want to hear. Wolf Richter described it as an ugly trifecta: surging inflation spreading beyond gasoline into services and food, with business-facing inflation now running at 6.0%, driven by services, a Fed threatening to look through that inflation rather than respond to it, and a tsunami of new debt the market has to absorb with no serious effort in Washington to address the deficits producing it. I think that's directionally correct.

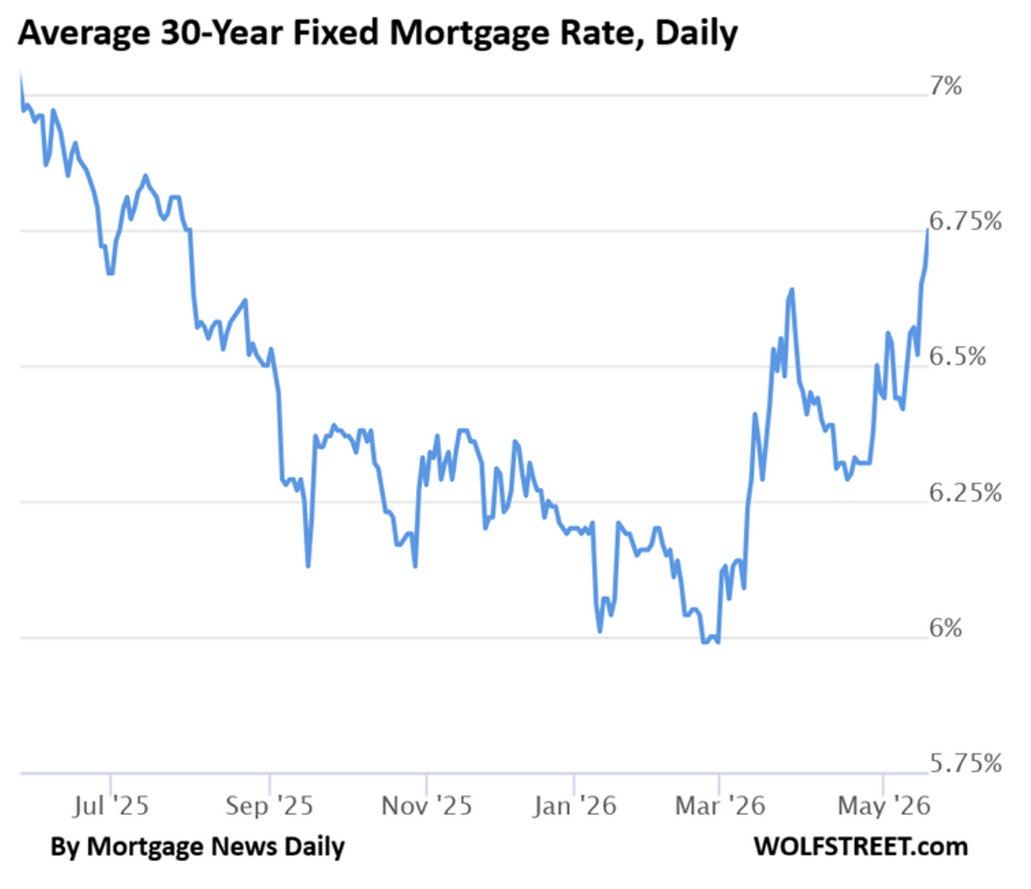

Sidebar: The Fannie (FNMA) and Freddie (FMCC) problem is not getting nearly enough attention and let me explain why. The government tried to reduce mortgage rates by having Fannie Mae and Freddie Mac buy back their own MBS. To fund those purchases they sold their Treasury holdings. Two of the biggest institutional Treasury buyers became net sellers. The policy designed to help housing pushed Treasury yields higher in the process. The 30-year fixed mortgage rate hit 6.75% (now 6.65%) this week, and whatever remained of the hope for sub-5% mortgages is now very difficult to imagine. Though that is down from over 7% one year ago.

Source: Wolf Street

Consider what the bond market is saying. The Fed cut rates. The long bond rose anyway. Before the Fed began cutting in 2024, the 30-year Treasury yield was below the federal funds rate. Today there is a spread of roughly 156 basis points between them. That is not what you normally see after a cutting cycle. I should note, that for much of Powell’s chairmanship, the Fed was behind the curve, and disastrously so in 2021.

That is not a normal relationship. My own read, and I could be wrong, but it looks as though the bond market is telling Warsh something very specific. Looking through inflation is not going to work here. The arithmetic increasingly points toward hikes, not cuts. Voters have a long memory when it comes to inflation. They have a history of holding presidents accountable for it. Just ask Jimmy Carter.

The bond market appears increasingly concerned about three things happening simultaneously: persistent inflation pressures, rapidly expanding federal deficits, and a Fed that may ultimately prove reluctant to tighten financial conditions aggressively enough to contain either. You can see why Warsh has no easy moves here.

And this is before we even begin talking seriously about debt issuance, refinancing needs, or the growing fiscal pressures several SIC speakers warned about repeatedly.

More from the SIC next week…

Comments

Log in or sign up to join the conversation.